Linerless Labels Market Size, Share & Industry Analysis, By Adhesion Type (Permanent, Removable, Repositionable, and Others), By Printing Technology (Direct Thermal, Thermal Transfer, Laser, Inkjet, and Others), By Application (Food & Beverage, Pharmaceuticals & Personal Care, Retail, Logistics and Others), By Component (Facestock, Adhesive, and Release Coating) and Regional Forecast, 2026-2034

Linerless Labels Market Size & Future Outlook

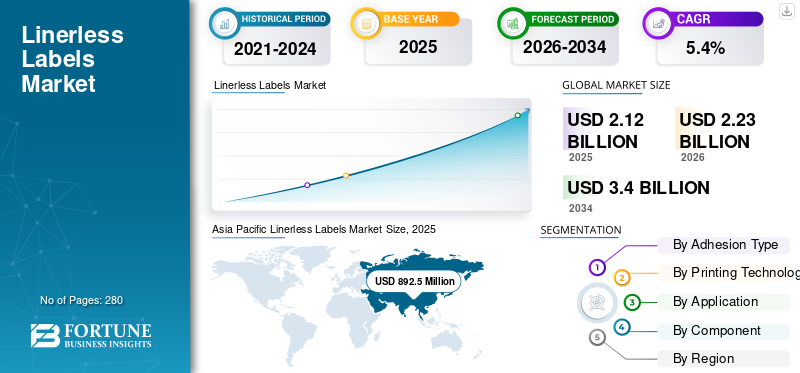

The global linerless labels market size was valued at USD 2.12 billion in 2025. The market is projected to grow from USD 2.23 billion in 2026 to USD 3.40 billion by 2034, exhibiting a CAGR of 5.40% during the forecast period. Asia Pacific dominated the Linerless Labels Market with a market share of 38.3% in 2025. Moreover, the linerless labels market in the U.S. is projected to grow significantly, reaching an estimated value of USD 584.66 million by 2032, driven by advancements in printing technologies among manufacturers.

The rising demand for convenience foods is the primary factor responsible for this market's growth. As the world moves towards biodegradable and eco-friendly products, manufacturers are focusing on developing sustainable and innovative labeling solutions. For instance, ID Label introduced a new eco-friendly linerless label called Eco Tote Renew in February 2020.

Labeling is an important part of creating a brand image. Brand owners have raised an increasing requirement of labels to run continuous promotional campaigns, produce seasonal and regional variants, and respond to markets more dynamically. An adhesive label often features a face stock, adhesive, and release liner. But with increasing concerns about liner waste generated, linerless labels are gaining considerable impetus in the packaging & labeling industry.

Linerless labels, also called liner-free labels or backless labels, are specially designed to discard the liner by replacing it with a release coating laid on the label after the printing of contents. A study by Ravenwood Packaging projects a 40% decrease in the label roll weight, accounting for large margins due to a decrease of liner cost and a reduction in inventory space used. Furthermore, rejection of release liner reduces the chances of industrial mishaps created by their smooth-coated surfaces, thus promoting the adoption of such labels in food & beverage and logistics industries.

Download Free sample to learn more about this report.

Global Linerless Labels Market Key Takeaways

Market Size & Forecast:

- 2025 Market Size: USD 2.12 billion

- 2026 Market Size: USD 2.23 billion

- 2034 Forecast Market Size: USD 3.4 billion

- CAGR: 5.4% from 2026–2034

Market Share:

- Asia Pacific dominated the linerless labels market with a 38.3% share in 2025, driven by rapid growth in e-commerce, expansion of FMCG and retail sectors, and increasing demand for sustainable and cost-effective labeling solutions across China, India, and Southeast Asia.

- By printing technology, direct thermal printing accounted for the largest market share, favored for its cost-efficiency and wide use in food, retail, and logistics labeling.

- By component, facestock held the dominant share due to its integral role in label durability, print quality, and compatibility with a wide range of packaging materials.

Key Country Highlights:

- United States: Market growth is supported by increasing automation in retail and logistics, rising demand for recyclable packaging materials, and advancements in label printing technology.

- China: The booming e-commerce industry and stringent packaging regulations are accelerating the adoption of linerless labels, especially among food delivery and logistics service providers.

- India: Government initiatives promoting sustainable packaging and the growth of organized retail and FMCG sectors are boosting linerless label adoption.

- Europe: Demand is driven by regulatory mandates on waste reduction and traceability, especially in the pharmaceutical and food sectors, encouraging use of linerless solutions.

LINERLESS LABELS MARKET TRENDS

Download Free sample to learn more about this report.

Development of Linerless Labels with Novel Adhesives and Release Coatings for Specialty Applications

Linerless labels have proved to be an attractive alternative to conventional pressure-sensitive labels due to the denunciation of backing liners. But, early these labels couldn’t use strong adhesives to avoid them from sticking together. Market players such as RR Donnelley, Ravenwood Packaging, and Skanem are investing in developing labels with specialized adhesives and release coatings to solve this problem. With continual research, liner-free labels for specialty applications such as frozen foods, microwavable products, and pharmaceutical packaging have become possible. Furthermore, repositionable labels have gained significant impetus as they can be reused with the development of such adhesives and release coating combinations. Asia Pacific witnessed a growth from USD 12.67 Billion in 2017 to USD 13.82 Billion in 2018.

LINERLESS LABELS MARKET GROWTH FACTORS

Growth in the Food & Beverage Industry Providing a Strong Base for the Growth of the Linerless Labels Market

Food products are sold off the shelves on the basis of brand recognition. As labeling is an important part of branding, the usage of eye-catching yet food-safe labels has observed considerable growth in this industry. Food products such as ham, bacon, and fruits are packaged with rolled liner-free labels, especially in Asian and Latin American countries such as Japan, Brazil, and Southeast Asia. Furthermore, with stringent regulations regarding the information to be printed on the food products packaging, the demand for larger labels has grown significantly. But, as these labels can include 30% more print than the traditional labels, they can efficiently replace these traditional labels without changing the dimensions, making them cost-effective for the food & beverage industry clientele. The growth in the food & beverage industry is evident to fulfill the hunger of about 7 billion people across the globe. This growth will also transform into the linerless labels market growth during the forecast period.

E-commerce to Provide a Pathway to the Growth of this Market

E-commerce has strongly rooted itself in developed economies and is growing by leaps and bounds in emerging economic powerhouses such as China and India. Such large traffic of goods requires a tracking system for goods to safeguard the delivery of the product to the correct recipient. For tracking of goods, the packages are marked with labels printed with codes and descriptions of the consignor and consignee. It is predicted that by 2025, about 200 billion parcels per annum will be transferred via e-commerce companies, resulting in a growing demand for labels. But, traditional labels create a large amount of waste in the form of the release liner, further resulting in an additional cost to the logistics service provider. Thus, e-commerce companies are increasingly adopting backingless labels for printing labels for packages, thereby providing a pathway for the growth of the market.

RESTRAINING FACTORS

Restrictions in Label Shaping to Impede the Market Growth

A critical challenge affecting the growth of the market is the inability of manufacturers to produce labels in different shapes and sizes than regular parallelogram structures. As the labels are generally packaged in rolls, it becomes difficult to lay the adhesive layer over the release coating layer in such shapes, which may lead to the loss of labels. With manufacturers constantly seeking unique branding products, these regular shapes may not fulfill their demand for a unique trademark, thus restricting the growth of the market.

LINERLESS LABELS MARKET SEGMENTATION ANALYSIS

By Adhesion Type Analysis

Repositionable Segment to Gain Impetus during the Forecast Period

The market is classified into permanent, removable, repositionable, and others based on adhesion type. Labels are generally used only as packaging and branding and are thus discarded after a product is consumed. However, with increasing concerns regarding waste and pollution across the globe, companies are seeking reusable labels that can be recollected from the market and repositioned on new products. Thus, such a repositionable segment is expected to gain strong impetus during the forecast period.

On the other hand, the permanent segment currently holds the largest volume share owing to heavy demand for such liner-free labels from the logistics and retail sectors.

By Printing Technology Analysis

Direct Thermal Segment to Account for the Largest Share in the Market

In terms of printing technology, the market is segmented into direct thermal, thermal transfer, laser, inkjet, and others. The logistics and retail industries generally utilize direct thermal printing technology due to its cheap printing capabilities. Direct thermal printers can be as small as a mobile device, making them easy to carry and print labels as and when required. Furthermore, it is cheaper due to the usage of single-colored ink, which increases the margin potential for the logistics service provider. Thus, the direct thermal segment is projected to account for the largest share in this market.

On the flip side, laser printing is to gain considerable market share during the forecast period with pharmaceuticals & personal care products manufacturers utilizing such advanced printing technology to produce colorful and attractive labels to catch the attention of the consumers. Large-scale printing using advanced techniques such as laser printing technology leads to affordable pricing for the labels, thus attracting manufacturers from the food & beverage and personal care product industries.

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Food & Beverage Segment to Account for Significant Share in the Linerless Labels Market

Based on application, the market is segmented into food & beverage, pharmaceutical & personal care, retail, logistics, and others. The food & beverage segment is expected to hold the largest share in the global market, both on the basis of value and volume, on account of the required labels to differentiate the products from the other competitors in the industry. Furthermore, the demand for clean label products has further increased the demand for labels with prolific information about the contents of the products, which is expected to provide growth opportunities for the market.

- The retail segment is expected to hold a 16.9% share in 2019.

Besides food & beverage, the logistics segment is expected to showcase significant growth in the market owing to the increasing spending capacity of the consumers which has resulted in an increase in the shopping of customers via e-commerce platforms.

By Component Analysis

Facestock is Set to be the Largest Segment in this Market

Based on components, the market is segmented into facestock, adhesive, and release coating. The facestock segment accounts for about 4/5th of the label by weight and is necessary for the manufacture of labels. It thus, accounts for the largest stake in this market. With companies seeking labels with high resistance to chemicals and superior sustainability, various materials for facestock are being introduced into the market such as vellum paper, metalized paper, and sugarcane paper. This factor is expected to further drive the growth of the market.

Release coating, on the other hand, is the component that differentiates the linerfree labels from traditional labels as it serves the purpose of a release liner. According to a study by Ravenwood Packaging, about 616 KT of label release liner end up in the landfill annually, which can be replaced by release coating in linerless labels, thus showing immense growth potential for release coating in the linerfree labels market. Furthermore, label companies are researching on developing release coatings which can meet specifications provided by the food products manufacturers, resulting in further adoption of the backingless labels in the industry.

REGIONAL LINERLESS LABELS MARKET ANALYSIS

Asia Pacific Linerless Labels Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

In 2019, the Asia Pacific market was valued at USD 892.5 million, accounting for 38.3% of the global linerless labels market, making it the dominant region in this sector. Asia Pacific is the largest region in the market owing to the fast growth of e-commerce in the region. Furthermore, the fast-moving consumer goods (FMCG) manufacturers in the region are seeking to build their position via brand growth, leading to the significant growth of packaging products, including linerless labels.

North America

The growth of the retail sector in the U.S. will govern the market in North America. As the region is expected to recover from the global pandemic of COVID-19 during the forecast period, the demand for personal care and retail goods is expected to increase. On the other hand, the market in Europe will be driven by the growth of the pharmaceutical industry in the region, which is expected to grow to counter further reoccurrence of such pandemics.

Latin America, Middle East & Africa

The market in Latin America will be defined by beverage manufacturers' adoption of liner-free labels. The market in the Middle East and Africa will follow the growth of the region's logistics sector, which is growing owing to the large shipping industry present in the region.

KEY INDUSTRY PLAYERS

Key Market Players Aiming for Market Share with Acquisition and Mergers of Smaller Companies

The competitive landscape of the market depicts a semi-consolidated market with the top 10 companies accounting for the majority of the share. Key players in the market have invested a considerable amount of resources in the research and development of linerless labels and their components. Development of unusual shapes for labels, research on superior adhesives, and development of novel release coatings are other few activities carried out by the market stakeholders.

Furthermore, key market players have adopted strategies of capacity expansion and acquisitions of smaller enterprises to improve their offering portfolio and services. This trend is projected to impact the global market during the forecast period positively.

LIST OF KEY COMPANIES PROFILED IN THE LINERLESS LABELS MARKET:

- Coveris

- Avery Dennison Corporation

- Ravenwood Packaging

- Innovia Films

- Constantania Flexibles

- Lexit Group AS

- RR Donnelley & Sons Company

- Gipako UAB

- Hub Labels

- Cenveo Corporation

- Reflex Labels Ltd.

- Skanem AS

- NAStar Inc.

- 3M

- Optimum Group

- SATO Europe GmbH

- Tereoka Seiko Co., Ltd.

- L&N Label Company

- Proprint Group

- DuraFast Label Company

- Bizerba Australia

- Bostik

- Dykam A.C.A. Ltd.

- Weber Packaging Solutions

- Other Key Players

KEY INDUSTRY DEVELOPMENTS:

- January 2020 – Bostik introduced a new adhesive for these labels. The new adhesive helps in enhancing the label production line efficiencies along with providing a sustainable packaging solution for quick-service restaurant (QSR) applications.

- August 2019 – Lexit Group entered into linerless labels manufacturing with the addition of a new coating machine Coater Com500F manufactured by Ravenwood Packaging. The new production capabilities will help the company to cater to the market demand in Europe, especially in Scandinavia.

REPORT COVERAGE

The linerless labels market report provides a detailed analysis of the market and focuses on key aspects such as leading companies, components, and leading applications of the linerless labels.

Besides this, the report offers insights into the market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Report Scope & Segmentation

Request for Customization to gain extensive market insights.

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Adhesion Type

|

|

By Printing Technologies

|

|

|

By Application

|

|

|

By Component

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global linerless labels market was valued at USD 2.12 billion in 2025 and is projected to reach USD 3.4 billion by 2034, growing at a CAGR of 5.4% during the forecast period. This growth is driven by rising demand in food packaging, e-commerce logistics, and sustainable labeling practices.

The market is primarily driven by the increasing demand for eco-friendly labeling solutions, especially in the food & beverage and logistics sectors. The absence of release liners reduces waste and improves efficiency, aligning with sustainability goals across industries.

Growing at a CAGR of 5.4%, the Market will exhibit steady growth in the forecast period (2026-2034).

Asia Pacific held the largest market share at 38.3% in 2019, led by rapid growth in e-commerce, food manufacturing, and retail sectors. Countries like China, India, and Japan are key contributors to regional dominance.

Linerless labels are widely used in food & beverage, logistics, pharmaceuticals, retail, and personal care industries. Their versatility and eco-friendliness make them a preferred choice for brands focusing on sustainable packaging.

One notable trend is the development of linerless labels with novel adhesives and release coatings for specialty applications, such as frozen foods and microwaveable items. Companies are also exploring repositionable labels for improved reuse and sustainability.

Direct thermal printing is the dominant technology due to its cost-effectiveness and portability. However, laser and inkjet printing are gaining traction in premium labeling applications like pharmaceuticals and cosmetics.

The main restraint is the limitation in label shape flexibility. Since linerless labels are roll-based, creating non-rectangular shapes is technically challenging, which may limit their use in customized or premium packaging designs.

Key players include Coveris, Avery Dennison, Ravenwood Packaging, Innovia Films, and RR Donnelley & Sons Company. These companies are investing in R&D, acquisitions, and sustainable innovations to strengthen their market positions.

- 2021-2034

- 2025

- 2021-2024

- 280

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us