Food Packaging Market Size, Share & Industry Analysis, By Material (Glass, Metal, Paper & Paperboard, Plastics {Non-biodegradable, Biodegradable}, & Wood), By Product Type (Rigid, Semi-rigid, & Flexible), By Packaging Type (Bags & Pouches, Films & Wraps, Stick Packs & Sachets, Bottles & Jars, Boxes & Cartons, Cans, Trays, & Clamshells), By Application (Fruits & Vegetables, Bakery & Confectionery, Dairy Products, Meat, Poultry & Seafood, Sauces, Dressings, & Condiments), By End-user (Quick & Full Service Restaurants, Cafe & Kiosks, & Chain Restaurants), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

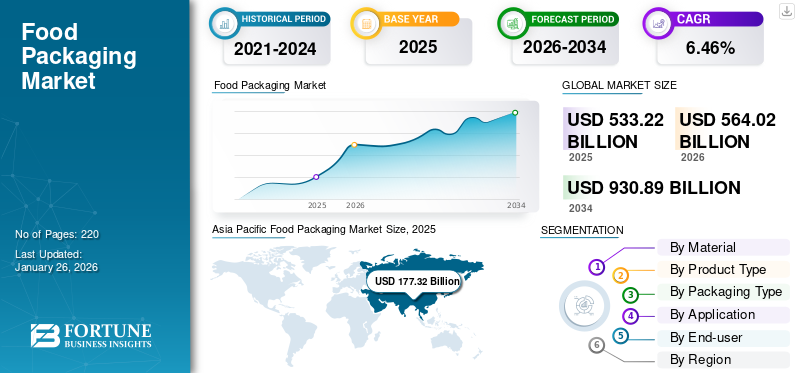

The global food packaging market size was valued at USD 533.22 billion in 2025 and is projected to grow from USD 564.02 billion in 2026 to USD 930.89 billion by 2034, exhibiting a CAGR of 6.46% during the forecast period. Asia Pacific dominated the food packaging market with a market share of 33.25% in 2025.

Food packaging plays a crucial role in preserving the quality, safety, and shelf life of food products. It serves multiple functions, including protection from contamination, facilitation of transportation, and communication of essential information to consumers. The market encompasses a wide range of materials and technologies designed to meet the diverse needs of the food industry.

- As per the Adelaide Now, An Australian shopper discovered a confusing detail on a pack of Woolworths Honey Macadamia nuts labeled 'Australian Made,' but with a note stating 'Product of Australia (Sorted in China).' This sparked frustration and confusion among consumers regarding food packaging labels.

Rising consumer preference and demand for packaged products due to the shift in consumption habits and changing lifestyles are the key factors driving the growth of the global market. The protection, convenience, and portability features the packaging offers also bolster global market growth. In addition, the graphics and varied forms of the food packaging convey information regarding product quality, nutrition, and many others. The rising efforts by major manufacturers to provide such helpful packaging and increasing usage of intelligent packaging techniques foster the industry globally.

Download Free sample to learn more about this report.

FOOD PACKAGING MARKET KEY TAKEAWAYS

Market Size & Forecast:

- 2025 Market Size: USD 533.22 billion

- 2026 Market Size: USD 564.02 billion

- 2034 Forecast Market Size: USD 930.89 billion

- CAGR: 6.46% from 2026–2034

Market Share:

- Asia Pacific led with 33.25% share in 2025, rising from USD 177.32 billion in 2025 to USD 189.31 billion in 2026.

- By material, plastics dominated due to flexibility and cost-effectiveness, while paper & board gain traction for recyclability.

- By product type, flexible packaging led, supported by innovation and lightweight benefits.

- Bakery & confectionery held the largest application share (38.82% in 2026).

Key Country Highlights:

- China: Major consumer driven by frozen food demand and retail growth.

- India: Retail sector boom expected to reach USD 2 trillion by 2032 fuels packaging needs.

- U.S.: Strong demand for healthier packaged foods drives growth.

- Europe: Rising processed food demand boosts packaging adoption.

- Brazil: Growth fueled by canned food and MAP packaging.

MARKET DYNAMICS

Market Drivers

Rising Demand for Convenience Food to Aid Market Growth

Convenience food is ready-to-eat and majorly used due to its easy portability, long shelf life. These items include snacks, frozen food, finger food, candy, and beverages. These products usually require less preparation and are served hot in ready-to-eat containers. Rising demand for ready-to-eat snacks due to a sedentary lifestyle is expected to fuel demand for convenience food. Rising per capita disposable income and an increasing working population also enhances market growth.

- According to Real Simple, Costco is subject to a recall of 79,200 pounds of Kirkland Signature Sweet Cream Butter. According to the U.S. Food & Drug Administration (FDA), packages of salted and unsalted butter are missing the required allergy statement “Contains Milk” on the packaging. However, the report says the ingredient list does include cream.

Nowadays, due to the fast-moving lifestyle of consumers, there has been an increasing demand for fast food items. This high demand has caused convenience food makers to develop products with better nutritional value and less harmful effects on the body. Henceforth, such a rise in demand for convenience food contributes to the need for significant packaging.

Increasing Demand for Edible Packaging Bolsters Market Growth

Rising concerns about packaging waste and its environmental impact boost the demand for edible packaging. In the past decade, traditional food packaging materials created tons of packaging waste and increased landfills. The recycling rate of the same was too low.

- According to the Organization for Economic Co-operation and Development (OECD), plastic pollution is growing relentlessly as waste management and recycling is falling short. Only 9% of plastic waste is recycled globally, while 22% is mismanaged. Such factors enhance the need for edible packaging and contribute to the industry's growth.

Edible packaging highly utilizes renewable & biodegradable materials to offer consumers a significant substitute for conventional plastic food packaging. A new form of edible packaging developed from milk protein, casein, is used around food products. As per the survey, these casein films keep the food fresh and less exposed to oxygen. They offer better storage, enhance shelf life and safety, and eliminate the waste cycle—such a rise in demand for edible packaging cushions the global food packaging market growth.

Market Restraints

Rapid Changing Technologies and Rising Cost of Raw Materials to Impede Market Growth

Plastic is one of the primary raw materials used for food packaging. The plastic packaging is made from synthetic polymers, such as polypropylene and polyethylene, manufactured from natural resources. The fluctuating price of these raw materials affects the packaging industry. Moreover, regulations developed by the government and associations over resource conservation are surging the price of these raw materials, which in turn is restraining the market growth. Raw material availability does not support technological advancements, hindering technological improvement in packaging solutions. Henceforth, the rapidly changing technologies also hinder market growth. High raw materials costs are causing inaccessibility to many new packaging technologies, and companies depend on traditional packaging, further affecting the economy and environment equally.

Market Opportunities

Digital Printing Offers Eye-Catching Visuals and Cost-effective Solutions Creates Opportunities

The snack food industry is shifting toward flexible packaging, with digital printing being the future for creating flexible packaging. Flexible packaging that is printed digitally presents a great chance to enhance brand recognition and boost sales.

When more snack options are introduced in flexible packaging, it is important to consider certain factors to ensure your packaging stands out. A well-designed look is widely known to enhance brand visibility and increase perceived worth. However, excellent design cannot succeed by itself — it requires printing in a manner that fully enhances the design. Digital printing enables the use of eye-catching visuals, vibrant hues, and a complete range of design options, such as pictures and promotional details, nutritional facts, and the history of the brand. Digital printing enables brands to make adjustments to their designs at the last minute. Finally, digital printing proves to be a more cost-effective option. Digital printing is great for creating short and medium-run length projects at competitive prices, two attributes that typically do not align in the field.

- A statistic showed The U.S. printing industry was valued at USD 77.7 billion in 2021. It is estimated that there are around 46,200 printing businesses in the U.S.

Market Challenges

Finding Sustainable Solutions that Maintain Functionality is a Significant Challenge

The industry faces pressure to address issues related to plastic waste and its environmental impact. Developing sustainable packaging solutions that do not compromise functionality is a significant challenge.

Due to the global focus on sustainability, the industry is being urged to decrease its environmental footprint. Conventional plastics are commonly used in food packaging, but their impact on pollution and landfill waste is receiving a lot of public attention. The difficulty is in discovering appropriate options that do not sacrifice functionality or safety. Numerous food companies are opting for biodegradable materials and recyclable packaging choices. New developments, such as bioplastics, produced from sustainable sources, show potential but frequently encounter challenges related to expense and effectiveness.

Another major obstacle is the complicated process of recycling food packaging. Food remnants can make recyclable items unrecyclable, making it harder to boost recycling rates. As a result, the sector must carefully manage the fine line between sustainability and feasibility, guaranteeing that new materials can efficiently preserve food while also being eco-friendly.

Download Free sample to learn more about this report.

FOOD PACKAGING MARKET TRENDS

Packaging Innovation in the Food Industry will Emerge as a Key Trend

The rising innovations in packaging hold a potential opportunity for market growth. Packaging is vital in preserving food quality, ensuring food safety, and increasing shelf-life. Plastic packages are very useful in achieving innovative product solutions. Among various plastic packaging kinds, plastic cling film is a widely used plastic packaging today. The shift toward eco-friendly packages and advanced innovations in cling film packaging also shape the growth of the market. The innovation comprises an extensive range of packaging options: intelligent packaging, active packaging, nanocomposites, edible/biodegradable packaging, and different types of packaging design. Asia Pacific witnessed a food packaging market growth from USD 156.57 billion in 2023 to USD 166.61 billion in 2024.

- According to the Food & Agriculture Organization of the United Nations, innovations and technological advancements in the food sector are rapidly evolving in the food safety arena. These technologies in food production, processing & packaging offer better tools for enhancing traceability, sensing contaminants in food, and inspecting outbreaks. It has subsequently generated the demand for packaging innovations, further booming as a critical trend for market growth.

IMPACT OF COVID-19

As the food industry was kept under essential services by all governments, the impact of COVID-19 pandemic on the global market is lower than other manufacturing industries. Flexible packaging companies serving the sectors, such as packaged foods, performed well during the pandemic. Changing consumer demand patterns, government measures, and stockpiling fuel the demand for packaged food. Due to the increased food safety crisis during the pandemic, many consumers in developing economies, such as India, have shifted their preference from unpacked food to packed food. Also, the rise in e-commerce retail during the outbreak aided the growth of domestic packaged food sales and flexible packaging for packaged foods.

SEGMENTATION ANALYSIS

By Material

Significant Properties Offered by Plastics Boost Segment's Growth

Based on material, the market is segmented into glass, metal, paper & paperboard, plastics, and wood. The Plastics segment dominated the market accounting for 46.84% market share in 2026. The plastic used in packaging is the most feasible material as it is flexible, lightweight, and cost-effective, does not cause splintering, and protects food from damage. Most of the plastic resins used in packaging are recyclable. Flexible & rigid plastic packaging offers opportunities to innovate. For instance, Modified Atmosphere Packaging (MAP) helps conserve food freshness, increasing the product's shelf life by slowing bacterial growth. Increasing consumption of beverages has led to a rise in plastic demand, which may favor segment growth.

- As per the Plastic Soup Foundation, The amount of plastic produced worldwide each year has exploded within the span of one human lifetime: from 2 million tons in 1950 to over 390 million tons in 2021. By far, the most plastic, 44%, is used for packaging material. In second and third place are the construction and automotive industries, respectively.

Paper & paperboard is the second dominating segment in the market. Paper and paperboard materials are more frequently chosen for food packaging because of their recyclability and environmental benefits. Often utilized for dry food items, takeout boxes, and baked goods, these materials are valued for their environmental friendliness and affordability.

By Product Type

Flexible Packaging Commands Dominance with Innovation and Technological Advancements

Based on product type, the market is segmented into rigid, semi-rigid, and flexible. The flexible product type segment is projected to dominate the market with a share of 52.01% in 2026 and is estimated to witness massive development over the forecast period. It is attaining high demand due to increasing technological advancements and innovative solutions for product packaging needs. Flexible packaging uses significantly less material than rigid containers and requires less energy when forming packaging products. Rising demand for packaging to ensure nutrient and flavor fortification will accelerate segment growth.

- According to the Flexible Packaging Association, Flexible Packaging is the second largest packaging segment in the U.S., garnering about 21% of the USD 180.3 billion U.S. packaging market. The largest market for flexible packaging is food (retail and institutional), accounting for about 50% of shipments.

Rigid product type is the second dominating segment in the market. Rigid packaging ensures strength and outstanding safeguarding, making it ideal for maintaining food freshness and avoiding contamination. Its structural durability is perfect for items needing extended shelf lives, such as canned items, drinks, and sauces.

By Packaging Type

Bags & Pouches Segment Seizes Market Share, Driven by Versatility and Printing Advancements

Based on packaging type, the market is segmented into bags & pouches, films & wraps, stick packs & sachets, bottles & jars, boxes & cartons, cans, trays, clamshells, and others. The bags and pouches segment will account for 25.9% market share in 2026 and is projected to grow exponentially over the forthcoming years. Pouches are lightweight and offer excellent product integrity. They are easy to reseal and carry, which increases their demand in the food industry. In addition, the modern flexographic printing methods employed in bags & pouches contribute to the segment growth.

- According to the Paper Bag Organization, Europe is the world leader in recycling paper. The paper recycling rate in Europe was 73.9% in 2020. Fifty-six million tons of paper were recycled in that year – which is equal to 1.8 tons of paper every second. Fibers are reused on average 3.8 times in Europe and paper bags are part of this loop.

Films and wraps is the second dominating segment in the market. Films & wraps are adaptable packaging options utilized for snacks and pet food. Their lightweight and adjustable design renders them very adaptable and simple to carry, boosting their attractiveness in the market.

By Application

Bakery & Confectionery Segment Sustains Market Leadership, Fueled by Diverse Product Applications

Based on application, the market is segmented into fruits & vegetables, bakery & confectionery, dairy products, meat, poultry & seafood, sauces, dressings, and condiments, and others. Among these applications, the bakery & confectionery segment is expected to remain dominant market share of 38.82% in 2026 during the forecast period. This segment finds prominent use in bakery & confectionery items, including chewing gums, croissants, savory pastries, candies, toffees, and chocolates. Increasing the consumption of these food products will lead to market growth. In addition, the demand for gluten-free substitutes has widely increased, contributing to the food packaging market share.

Fruits & vegetables is the second dominating segment in the market. This category necessitates packaging that guarantees product safety, freshness, and prolonged shelf life because of the perishable characteristics of products. Improvements in cold chain logistics and developments in eco-friendly packaging materials additionally enhance growth.

To know how our report can help streamline your business, Speak to Analyst

By End-user

Chain Restaurants Lead Market, Fueled by Convenience and Health Trends

Based on end-user, the market is segmented into quick service restaurants, café & kiosks, full service restaurants, chain restaurants, and others. The chain restaurants segment holds the largest share of the global market. The rising consumer focus on more convenient methods of food consumption is the primary factor enhancing the segment's growth. In addition, the augmenting demand for healthy food and creative presentation also contribute to the growth of the chain restaurant segment.

- As per the National Restaurant Association, Eating and drinking places will directly contribute USD 1.4T in output (or sales) to the U.S. economy in 2024 dollars. Adding in these additional impacts, the industry will make a total contribution of USD 3.5T in output to the U.S. economy in 2024, or 15.6% of real GDP, with 22.9M employees and USD 1.1T in total labor income.

The full service restaurants hold the second largest share of the market. Full-service eateries utilize food containers to safeguard their meals and prolong their freshness. The packaging materials utilized by full-service restaurants need to be sturdy and temperature-regulated to accommodate the requirements of online ordering and delivery.

FOOD PACKAGING MARKET REGIONAL OUTLOOK

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Food Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific Leads Global Market, Driven by Retail Growth and Increasing Frozen Food Demand

The market in Asia Pacific reached USD 177.32 billion in 2025, representing 33.25% of total market revenue, and is expected to reach USD 189.31 billion in 2026. Asia Pacific accounted for the largest global market share and is expected to continue its dominance over the forecast period. The rising urban population levels and retail infrastructure development are expected to support the growing need for packed goods in China, Japan, and India. Due to various manufacturers and increasing demand for frozen food, China is a significant packaging consumer in Asia. Further, consumer spending on packaged food and improving lifestyles may fuel regional product demand. The Japan market is valued at USD 25.29 billion by 2026, the China market is valued at USD 64.57 billion by 2026, and the India market is valued at USD 57.04 billion by 2026.

- According to the India Brand Equity Foundation, the Indian retail industry has emerged as one of the most dynamic and fast-paced industries due to the entry of several new players. It accounts for over 10% of the country’s Gross Domestic Product (GDP) and around 8% of employment. India is the world’s fifth-largest global destination in the retail space and ranked 63 in the World Bank’s Doing Business 2023. The retail sector in India is expected to reach a whopping USD 2 trillion in value by 2032, according to a recent analysis by the Boston Consulting Group (BCG).

North America

North America is the Second-dominating Region, Driven by U.S. Consumer Demand for Healthier Packaged Foods

The North America market was valued at USD 151.12 billion in 2025, capturing 28.34% of global revenue, and is estimated to reach USD 160.49 billion in 2026. North America is the second-dominating region. The U.S. is one of the major consumers of packaged foods, which will aid the demand for food packaging. Rising awareness of a healthy lifestyle has influenced consumers to shift to a higher quality of packaged food, driving product demand. The U.S. market is valued at USD 130.56 billion by 2026.

- As per the American Farm Bureau Federation, in 2023, USD 174.9 billion worth of American agricultural products were exported globally. Many Americans celebrate holidays with food, spending a total of nearly USD 14 billion each year. About 20% of U.S. farm products by value are exported each year.

Europe

Growing Demand for Processed Food Enhances Europe’s Market Growth

In 2025, Europe held 24.80% of the global market, reaching a valuation of USD 132.25 billion, and is expected to reach USD 139.21 billion in 2026. Europe held a significant share and is anticipated to witness substantial growth in the market owing to increasing demand from the food & beverage industry. Increasing demand for packaging and processed food and changing consumer lifestyles, mainly in Germany, the U.K., and Italy, will bolster regional growth. The UK market is valued at USD 25.31 billion by 2026, while the Germany market is valued at USD 37.67 billion by 2026.

- According to FoodDrinkEurope, in 2020, the EU food and drink industry generated a turnover of USD 1139.18 billion and a value-added of USD 234.65 billion. With USD 41.49 billion invested in 2020, the food and drink industry is the manufacturing sector with the highest capital spending.

Latin America

Brazil Drives Latin America's Market Growth, Fueled by Canned Food Demand

Latin America maintained a strong presence in the global market, reaching USD 40.84 billion in 2025, accounting for 7.66% share, and is expected to reach USD 42.35 billion in 2026. Mexico and Brazil are the major countries in Latin America that will support market growth. Growth in the region is mainly attributable to the growing demand for canned food. Some novel packaging tools, such as Modified Atmosphere Packaging (MAP), increase as consumers demand greater transparency and minimal processing. Such features enhance the industry in the region.

- In November 2024, the food packaging industry in Latin America is undergoing significant changes as new regulations come into effect, driving a shift toward more sustainable and transparent practices. These regulations, particularly Mexico, Chile, Argentina, Colombia, and Brazil, are reshaping how food products are packaged and labeled, pushing businesses to adapt to a growing focus on public health and environmental sustainability. In Mexico, for instance, the Norma Oficial Mexicana NOM-051 has significantly impacted consumer habits, resulting in a 25% reduction in the consumption of products bearing these warning labels.

Middle East & Africa

Middle East & Africa will Witness Growth Due to Rising Demand for Dairy, Meat, Poultry, Seafood, and Convenience Foods

In 2025, the Middle East & Africa market stood at USD 31.69 billion, representing 5.94% of global demand, and is projected to grow to USD 32.65 billion in 2026. The Middle East & Africa is expected to observe substantial growth in the market owing to increasing demand for dairy products, meat, poultry, and seafood applications. The surge in Western food culture and food service in the region indicates the increasing product demand that will lead to market growth. Burgeoning demand for convenience food with rising consumer purchasing power shall foster regional growth during the forecast period.

- In September 2024, Japan earmarked the Middle East as its next major emerging market for exports with the establishment of a specialized export platform in the UAE, banking on the rising interest in Japanese food in the region. Japan has been on a quest to increase its food export market since 2020 when the Ministry of Agriculture, Forestry and Fisheries MAFF announced the establishment of the specialized Export and International Bureau to accelerate progress toward its goal of USD 13.7 billion by 2025 and USD 34.2 billion by 2030.

IMPACT OF TRADE PROTECTIONISM ON THE FOOD PACKAGING INDUSTRY

Trade protectionism, characterized by tariffs and import restrictions, can significantly impact the industry. For example, tariffs on raw materials can increase production costs, which may be passed on to consumers. Additionally, export restrictions can disrupt supply chains, leading to shortages and delays. The World Bank has analyzed the effects of such policies on global food markets, emphasizing the need for cooperative trade practices to ensure food security.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Market Participants to Witness Significant Growth Opportunities with New Product Launches

The global market is highly fragmented and competitive. A few significant players are dominating the market by offering innovative packaging solutions in the packaging industry. These major market players constantly focus on expanding their customer base across regions by innovating their existing wide range of products.

Major players in the industry include Mondi Group, Amcor plc, Berry Global Inc., Stora Enso, Constantia Flexibles, and others. Numerous other companies operating in the market are focused on market scenarios and delivering advanced packaging solutions.

List of Key Food Packaging Companies Profiled:

- Mondi Group (Austria)

- Amcor plc (Switzerland)

- Berry Global Inc. (U.S.)

- Stora Enso (Finland)

- Constantia Flexibles (Austria)

- Plastipak (U.S.)

- Tetra Pak International S.A. (Switzerland)

- DS Smith (U.K.)

- Crown Holdings, Inc. (U.S.)

- ExxonMobil Chemical (U.S.)

- Coveris Group (U.K.)

- International Paper Company (U.S.)

- Smurfit Kappa Group (Ireland)

- Graphic Packaging International, LLC (U.S.)

- WestRock Company (U.S.)

- Sonoco Products Company (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- September 2024: Pakka, a producer of compostable packaging options, introduced a new line of flexible compostable packaging products. The innovative product line has been created to meet the rising need for flexible packaging in the food and beverage industry with compostable options and to help promote a cleaner environment.

- June 2024: Crocco and Versalis collaborated to create food packaging film utilizing recycled post-consumer plastics. By using Versalis' Balance product, this packaging upholds crucial food safety and performance standards. The partnership emphasizes the significance of varied raw materials and supply chain collaborations in promoting circular economy objectives.

- June 2024: Saica Group and Mondelēz collaborated to introduce a new paper-based solution aimed at multipack items for the confectionery, biscuits, and chocolate sectors, intended to be recyclable within the paper waste stream. By 2025, the firm intends to cut the use of virgin plastic in rigid plastic packaging by a minimum of 25% and in all plastic packaging by 5%.

- January 2024: Mars China launched a Snickers bar that includes dark chocolate cereal and comes in mono-material flexible packaging. This innovative product provides a low-sugar and low-Glycemic Index (GI) alternative, with individual packaging made from mono PP material aligned with the 'Designed For Recycling' principle, which allows for easy recycling in designated streams.

- December 2023: Melodea unveiled MelOx NGen, a high-performance barrier solution aimed at enhancing the recyclability of plastic food packaging and more. The innovative barrier aims to preserve food freshness while sustainably minimizing plastic waste. MelOx NGen is a waterborne, plant-derived coating intended to coat the inner surfaces of packaging, such as films, pouches, bags, lidding, and blister packs for CPG products, and it will be launched worldwide.

INVESTMENT ANALYSIS AND OPPORTUNITIES

In August 2024, The chairman and MD of ITC, Sanjiv Puri, revealed plans for an investment of approximately USD 200 million in the medium term, emphasizing confidence in the Indian narrative. The varied conglomerate plans to invest in the FMCG sector, along with the paperboard and packaging industry. The remainder will be utilized for farming and additional enterprises. Puri stated that 30-35% will go toward investments in paperboards and packaging sectors over the next five years. He mentioned that the location in Bhadrachalam is saturated, and the team might consider a greenfield site for a paperboard plant.

REPORT COVERAGE

The market research report provides a detailed market analysis. The market overview also focuses on key aspects, such as top key players, competitive landscape, product types, market segments, Porter’s five forces analysis, and leading segments of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market intelligence and growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope and Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.46% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material

|

|

By Product Type

|

|

|

By Packaging Type

|

|

|

By Application

|

|

|

By End-user

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market is valued at USD 533.22 billion in 2025.

The market is likely to grow at a CAGR of 6.46% over the forecast period (2026-2034).

The plastic material segment is expected to lead the market in the forecast period.

The market size of Asia Pacific stood at USD 189.31 billion in 2026.

The key market drivers are increasing consumption of beauty products to bolster market growth.

Some of the top players in the market are Huhtamaki, AptarGroup, Inc., Berry Global Group Inc., BIG SKY PACKAGING, Gerresheimer, and others.

The global market size is expected to reach USD 930.89 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us