Oil and Gas Market Size, Share & Industry Analysis, By Value Chain (Upstream, Midstream, and Downstream), By Product Type (Crude Oil, Natural Gas, Liquefied Natural Gas, Natural Gas Liquids, and Refined Petroleum Products), By Application (Transportation Fuels, Power Generation, Industrial Energy, Residential and Commercial Heating, and Petrochemicals and Specialty Products), and Regional Forecast, 2026-2034

Oil and Gas Market Future Outlook

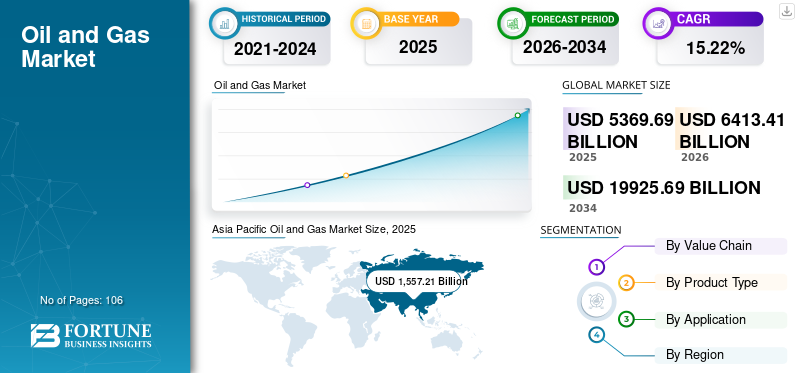

The global oil and gas market size was valued at USD 5369.69 billion in 2025. The market is projected to grow from USD 6413.41 billion in 2026 to USD 19925.69 billion by 2034, exhibiting a CAGR of 15.22% during the forecast period. Asia Pacific dominated the global oil and gas market with a market share of 35.67% in 2025.

Sustained worldwide energy demand, notably from developing nations where urbanization, industrialization, and population expansion continue to increase fuel and electricity consumption, is the main factor behind the expansion of the oil and gas industry. Oil and natural gas continue to be essential to transportation, electricity production, and heavy industries, even as renewable energy grows, since there are still few scalable and dependable options available in the near to medium future. While LNG trade is developing to improve energy security in import-dependent areas, the demand for natural gas is increasing sharply as it is widely used as a transition fuel to replace coal. Companies in the market are increasingly entering into long-term agreements and strategic partnerships to secure supply, stabilize pricing, and reduce operational risks in a volatile energy environment. The oil and gas supply chain market is driven by digitalization, automation, and the adoption of advanced supply chain management solutions. Oil production in the market is driven by upstream capital investments, favorable crude oil prices, and expanding production capacities.

Schlumberger, Saudi Aramco, and BP plc are key participants in the global market, supported by their extensive operational scale and integrated value chain presence. The market, from a business and financial standpoint, is influenced by global energy demand, regulatory policies, and capital expenditure cycles.

In December 2025, Schlumberger signed a five-year agreement with Aramco to deliver stimulation services for Saudi Arabia's unconventional gas fields. The agreement is part of a multi-billion-dollar deal supporting one of the largest unconventional gas development initiatives in the world. Despite a 2.08% revenue headwind over the previous 12 months, the energy services giant, with a market value of USD 57.26 billion and a P/E ratio of 14.9, continues to win major contracts.

Download Free sample to learn more about this report.

Oil and Gas Market Key Takeaways

- 2025 Market Size: USD 5,369.69 Billion

- 2026 Market Size: USD 6,413.41 Billion

- 2034 Forecast Market Size: USD 19,925.69 Billion

- CAGR: 15.22% from 2026–2034

- Asia Pacific dominated the oil and gas market with a 35.67% share in 2025.

- The upstream segment is projected to account for a 44.79% share in 2026.

- The transportation fuels segment is expected to hold a 40.93% share in 2026.

Asia Pacific

Asia Pacific generated USD 1,892.02 billion in 2025, accounting for 35.67% of the global market.

North America

North America reached USD 1,293.14 billion in 2025, representing a 24.21% market share.

Europe

Europe recorded USD 990.86 billion in 2025, contributing 18.33% of global revenue.

U.S.

The market is projected to reach USD 1,250.53 billion by 2026, supported by strong shale production and LNG exports.

Japan

The oil and gas market is projected to reach USD 216.68 billion by 2026.

Read More

MARKET DRIVERS

Increasing Demand for Transportation Fuels to Propel Market Growth

The primary driver of the oil and gas market growth is the increasing demand for transportation fuels. Petroleum-based fuels, such as gasoline, diesel, jet fuel, and bunker fuel, continue to be widely used in marine shipping, aviation, road transportation, and logistics, as few viable large-scale alternatives exist. Increased fuel use is being driven by rising vehicle ownership, the growth of international trade, and the expansion of air travel, especially in developing nations.

In September 2025, Woodside Energy Trading Singapore Pte Ltd (Woodside) and PETRONAS LNG Ltd (PLL), a division of Petroliam Nasional Berhad (PETRONAS), have reached a fully defined sale and purchase agreement (SPA) for the delivery of 1 million tonnes per annum (Mtpa) of liquefied natural gas (LNG) to Malaysia for 15 years, beginning in 2028.

This significant event signals the successful transformation of the non-binding Heads of Agreement (HOA) signed in June 2025 into a binding agreement, reaffirming both firms' shared goal of enhancing collaboration across the LNG value chain. This agreement will enhance long-term LNG trade partnerships that support transportation fuel demand (marine and power).

MARKET RESTRAINTS

High Capital Investment Requirements to Restrain Market Growth

The need for significant capital expenditures is hampering the expansion of the oil and gas industry. Significant initial expenditures and extended payback times are necessary for exploration, drilling, offshore development, LNG liquefaction, pipeline installation, and refinery expansion. Businesses are exposed to financial risk through these capital-intensive initiatives, especially when volatility in natural gas and crude oil prices is high. Additionally, project costs are increased by rising expenditures for environmental compliance, the introduction of cutting-edge technology, and infrastructure expansion.

MARKET OPPORTUNITIES

Technological Advancements in Exploration and Production to Create Lucrative Growth Opportunities

The oil and gas industry is experiencing significant growth potential due to technological advancements in exploration and production. Technological advances, such as sophisticated seismic imaging, horizontal and directional drilling, digital oilfields, reservoir modeling using artificial intelligence, and enhanced oil recovery techniques, have significantly increased the success rate of discovery and hydrocarbon recovery.

In June 2025, Halliburton and Chevron U.S.A. Inc., a division of Chevron Corporation, collaborated to develop a novel method enabling feedback-driven, closed-loop completions in Colorado. This intelligent fracturing method uses subsurface feedback and automated stage execution to maximize energy delivered to the wellbore without requiring human intervention. The capacity improves the prior implementation of autonomous hydraulic fracturing technology.

OIL AND GAS MARKET TRENDS

Growing Adoption of Natural Gas and LNG to Drive Market Growth

The increased usage of natural gas and LNG significantly fuels the expansion of the oil and gas sector. Due to its lower carbon emissions compared to oil and coal, natural gas is increasingly being chosen as a transition fuel, making it a vital component of power generation, industrial heating, and urban energy supply. Concurrently, the growth of LNG infrastructure and long-term supply contracts is facilitating cross-border gas trade, which is enhancing energy security for import-dependent areas.

In July 2024, to advance its strategic gas expansion, Saudi Arabia's Aramco awarded three packages of contracts totaling over USD 25 billion. The second phase of the Jafurah unconventional gas field's development is linked to 16 contracts worth USD 12.4 billion, including the construction of gas compression facilities and related pipelines, and the extension of the Jafurah Gas Plant (including the construction of gas processing trains, utilities, sulfur, and export facilities). The project will also include building the new Riyas Natural Gas Liquids (NGL) fractionation facilities in Jubail to treat NGL from Jafurah.

MARKET CHALLENGES

Energy Transition and Decarbonization Pressure to Hamper Market Growth

Decarbonization pressures and energy transitions are constraining market expansion. The transition to renewable energy, electric cars, and alternative fuels is being hastened by increasingly stringent climate rules, net-zero goals, and carbon-reduction pledges governments are enacting across major economies. These steps are expected to lower long-term demand projections for oil and gas, particularly in the transportation and electricity production industries.

Download Free sample to learn more about this report.

Segmentation Analysis

By Value Chain

Rising Investments in Exploration and Production Operations Boosted Upstream Segment Growth

Based on the value chain, the market is classified into upstream, midstream, and downstream.

The upstream segment is projected to dominate the market with a share of 44.79% in 2026. The market is dominated by the upstream sector, driven by significant investments in exploration and production, rising demand for crude oil and natural gas, and ongoing development of both conventional and unconventional resources.

The downstream segment is the second-largest segment in the market, driven by strong demand for refined petroleum products, including gasoline, diesel, jet fuel, and petrochemicals, across various transportation, industrial, and consumer applications.

By Product Type

Extensive Use of Crude Oil in Transportation Fuels and Petrochemical Feedstocks Boosts Segment Growth

In terms of product type, the market is categorized into crude oil, natural gas, liquefied natural gas, natural gas liquids, and refined petroleum products.

The curde oil segment is expected to lead the market, contributing 31.89% globally in 2026. Due to its widespread use as a primary energy source and as a vital feedstock for transportation fuels, petrochemicals, and industrial goods, as well as its well-established global production, refining, and distribution infrastructure, crude oil is the dominant segment.

Natural gas is the second-largest segment of the market, driven by its widespread adoption as a cleaner transition fuel, strong demand across power generation, industry, and residential applications, and the rapid expansion of LNG infrastructure, which enables global trade and energy security.

By Application

To know how our report can help streamline your business, Speak to Analyst

Rising Demand for Mobility Propels Transportation Fuels Segment Growth

In terms of application, the market is categorized into transportation fuels, power generation, industrial energy, residential and commercial heating, and petrochemicals and specialty products.

The transportation fuels segment will account for 40.93% market share in 2026. Due to the ongoing reliance of the road transport, aviation, marine, and logistics sectors on petroleum-based fuels, which are scarce and lack large-scale alternatives, and the increasing global demand for mobility, the market is dominated by the transportation fuels segment.

Industrial energy is the second-largest segment of the market. Due to the significant dependence of manufacturing, refining, petrochemicals, cement, steel, and other energy-intensive industries on oil and natural gas for continuous, high-intensity energy needs, the industrial energy sector dominates the market.

Oil and Gas Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Oil and Gas Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed approximately USD 1892.02 Billion to the global market in 2025, accounting for 35.67% share, and is expected to reach USD 2287.69 Billion in 2026. The Asia Pacific market is growing due to rapid industrialization, rising energy demand driven by population growth and urbanization, expansion of the transportation and petrochemical sectors, and increasing investments in refining, LNG imports, and domestic exploration. In 2025, the Chinese market is estimated to reach USD 662.15 billion. Increasing energy demand from industrial development and urbanization, rising transportation fuel consumption, rapid expansion of the petrochemical sector, and government backing for natural gas and LNG to enhance energy security and lower emissions are all contributing to the growth of China's market. The Japan market is projected to reach USD 216.68 billion by 2026, the China market is projected to reach USD 826.57 billion by 2026, and the India market is projected to reach USD 560 billion by 2026.

For instance, in December 2025, Petronas LNG entered into a liquefied natural gas supply arrangement with the Singapore trading division of China National Offshore Oil Corporation (CNOOC). The subsidiary of the Malaysian state giant Petronas stated that it has signed a Sale & Purchase Agreement (SPA) with CNOOC Gas & Power Singapore Trading & Marketing for the delivery of one million tons of LNG annually.

North America

In 2025, North America held 24.21% of the global market share, reaching a valuation of USD 1293.14 Billion, and is projected to grow to USD 1552.61 Billion in 2026. The U.S. market is experiencing growth due to strong shale production, rising demand for natural gas and LNG exports, increased investments in energy security, and technological advancements that have improved drilling efficiency and reduced production costs. Backed by these factors, countries including the U.S. market is projected to reach USD 1250.53 billion by 2026, and Canada is expected to record USD 259.23 billion in 2025.

Europe

The market in Europe reached USD 990.86 Billion in 2025, representing 18.33% of total market revenue, and is projected to reach USD 1175.65 Billion in 2026. In the region, Germany market is projected to reach USD 219.81 billion by 2026. Due to increased investments in import infrastructure and supply diversification, continued reliance on refined fuels for transportation and industry, and rising demand for natural gas and LNG to improve energy security, the European market is expanding. The UK market is projected to reach USD 140.63 billion by 2026

Latin America

In 2025, Latin America generated USD 400.49 Billion, contributing 6.94% to global market revenue, and is projected to grow to USD 445.0 Billion in 2026. The Latin America market is growing due to expanding upstream investments in offshore and unconventional resources, rising domestic energy demand, increased refining capacity, and government initiatives to boost production and reduce fuel imports.

Middle East & Africa

The Middle East & Africa region captured 14.85% of the global market in 2025, generating USD 793.19 Billion in revenue, and is projected to reach USD 952.46 Billion in 2026. The Middle East & Africa market is growing due to abundant hydrocarbon reserves, increasing investments in upstream capacity expansion, rising regional energy demand, and strong export demand for crude oil, natural gas, and LNG.

COMPETITIVE LANDSCAPE

Key Industry Players

Vendors are Actively Discovering New Oil and Gas Resources Through Increased Exploration Activities

Through increased exploration activities, advanced seismic surveys, and the adoption of innovative drilling technologies, oil and gas companies are actively discovering and developing new resources to expand reserves and meet growing global energy demand. Oil companies in the oil and gas market are driven by demand growth and competitive pressures.

In December 2025, Equinor discovered two new gas and condensate deposits in the Sleipner region of the North Sea. Through existing infrastructure, these may be developed for the European market and represent Equinor's greatest discoveries so far this year.

The two wells, Lofn and Langemann, in production license 1140, are situated between the Gudrun and Eirik fields. According to early estimates, the reservoirs may hold between 5 and 18 million standard cubic meters of recoverable oil equivalents, or between 30 and 110 million barrels.

LIST OF KEY OIL AND GAS COMPANIES PROFILED

- Saudi Aramco (Saudi Arabia)

- Chevron Corporation (U.S.)

- Shell plc (U.K.)

- Sinopec Group (China)

- Petrobras (Brazil)

- Eni S.p.A (Italy)

- Gazprom (Russia)

- Repsol S.A. (Spain)

- Woodside Energy (Australia)

- Rosneft Oil Company (Russia)

- TotalEnergies SE (France)

- Equinor ASA (Norway)

- BP Plc (U.K.)

- Occidental Petroleum (U.S.)

- Oil and Natural Gas Corporation (India)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Chevron Cyprus, a division of the U.S.-based oil giant Chevron, and its partners BG Cyprus (Shell) and NewMed Energy decided to proceed with a front-end engineering design (FEED) study for an offshore gas field reservoir in Block 12, which is situated in the Eastern Basin of the Mediterranean Sea.

- December 2025: Serbia prolonged its gas agreement with Russian Gazprom until March 31, 2026. The nation has been anticipating the signing of a longer-term agreement since May of this year, but thus far, it has only been able to guarantee supplies via consecutive three-month extensions. The US sanctions on the Serbian oil business NIS, in which Gazprom has a majority ownership, make energy cooperation "complicated." The situation may also be impacted by the possibility of EU legislation aimed at prohibiting Russian gas.

- November 2025: Repsol SA is exploring a reverse merger of its upstream division with potential partners, including the American energy company APA Corp., according to sources familiar with the matter. The Spanish oil and gas company has held preliminary talks with APA, formerly known as Apache Corp., regarding a potential transaction.

- April 2025: in a major move in the Kingdom's ongoing efforts to increase its energy output and diversify its reserves, Aramco announced the discovery of 14 new oil and natural gas locations throughout the Eastern Province and the vast Empty Quarter desert. The discoveries include six oil fields, two independent gas fields, four natural gas reservoirs, and two more oil reservoirs. The state-owned oil behemoth stated that the new fields will boost the production of both crude oil and natural gas.

- April 2025: Sinopec cautiously resumed buying Russian oil after a short pause last month. The decision follows a risk assessment in light of US sanctions imposed on several Russian entities. Unipec, the trading arm of Sinopec, has recently acquired May-loading cargoes of ESPO Blend crude from Russia’s Far East. The company had previously refrained from purchasing March and April-loading shipments amid tightening restrictions.

- February 2025: Oil and Natural Gas Corporation Limited (ONGC) and BP signed an agreement to explore potential areas for cooperation and collaboration across the energy sector, both in India and globally, with a focus on oil and gas exploration and production, as well as trading and expansion into other energy vectors.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 15.22% from 2026-2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Value Chain

By Product Type

By Application

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5369.69 billion in 2025 and is projected to reach USD 19925.69 billion by 2034.

In 2025, the market value in Asia Pacific stood at USD 1892.02 billion.

The market is expected to exhibit a CAGR of 15.22% during the forecast period (2026-2034).

The transportation fuels segment led the market in terms of application.

Increasing demand for transportation fuels to propel market growth.

BP plc., Chevron Corporation, and Shell are among the prominent players in the market.

Asia Pacific dominated the global oil and gas market with a market share of 35.67% in 2025.

Growing adoption of natural gas and LNG to drive market growth.

- 2021-2034

- 2025

- 2021-2024

- 106

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us