Alternative Protein Market Size, Share & Industry Analysis, By Source (Plant-Based [Soy Protein, Pea Protein, and Others], Microbial & Fermentation, Cell Culture, Insect-Based, and Others), By Type (Isolates, Concentrates, Hydrolysates, and Protein Blends), By Form (Dry and Liquid), By Application (Meat Alternatives, Dairy Alternatives, Bakery & Confectionery, Snacks & Bars, Beverages, RTE Meals, Dietary Supplements, Sports Nutrition, Animal Feed, and Others), and Regional Forecast, 2026–2034

(Offer valid till 15th Jul 2026)

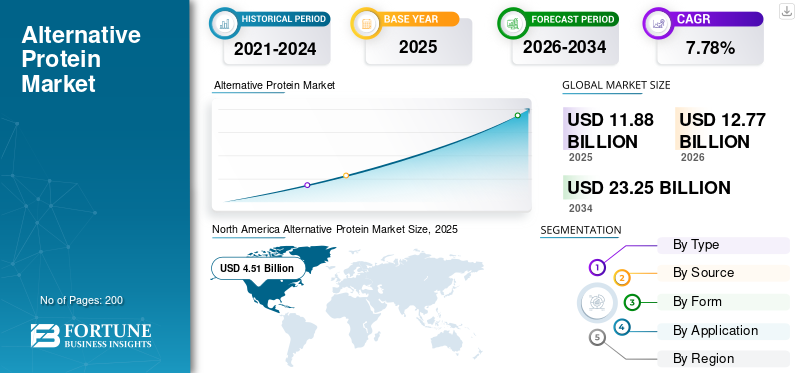

Alternative Protein Market Size and Future Opportunities

The global alternative protein market size was valued at USD 11.88 billion in 2025 and is projected to grow from USD 12.77 billion in 2026 to USD 23.25 billion by 2034, exhibiting a CAGR of 7.78% during the forecast period. North America dominated the global alternative protein market with a market share of 37.96% in 2025. Industry growth is driven by rising demand for sustainable food systems, evolving consumer dietary preferences, and advancements in food technology and protein innovation.

Alternative proteins include plant-based, microbial & fermentation-derived, cell-cultured, and insect protein, developed as substitutes for conventional animal protein sources. These proteins are increasingly incorporated into meat and dairy alternatives, functional foods, beverages, bakery products, sports nutrition, dietary supplements, and animal feed. Market expansion is driven by sustainability food concerns, rising flexitarian and vegan adoption, protein security challenges, and innovation in food production and technology, alongside increasing institutional and government support for sustainable protein systems.

The global alternative protein industry remains moderately fragmented, with strong participation from multinational food companies, ingredient manufacturers, and specialized protein technology firms. Leading players such as Beyond Meat, Inc., Impossible Foods Inc., Cargill, Incorporated, Archer-Daniels-Midland Company (ADM), and Nestlé S.A. continue to focus on taste and texture parity, cost reduction, clean-label positioning, and expansion into emerging markets.

The alternative protein market is transitioning from a niche innovation segment into a structurally significant component of the global food and agriculture ecosystem. Increasing pressure on traditional protein supply chains, combined with environmental sustainability concerns, is accelerating the shift toward diversified protein sources. As a result, the alternative protein market size continues to expand across both developed and emerging economies.

Consumer behavior plays a central role in shaping alternative protein market growth. Dietary preferences are gradually shifting toward plant-based and functional nutrition, supported by rising awareness of health, sustainability, and ethical sourcing considerations. This shift is particularly evident among urban populations and younger demographics, influencing product development strategies across the food industry.

Technological advancements are also redefining the alternative protein industry. Innovations in plant protein extraction, fermentation processes, and cell-based cultivation are improving product quality, scalability, and cost efficiency. These developments enable manufacturers to replicate taste, texture, and nutritional profiles more closely aligned with conventional protein sources.

Key structural forces shaping alternative protein market trends include:

- Increasing demand for sustainable and resource-efficient food production

- Rapid innovation in fermentation and cell culture technologies

- Expansion of plant-based protein applications across food categories

- Growing investment from institutional investors and food technology companies

Download Free sample to learn more about this report.

ALTERNATIVE PROTEIN MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 11.88 Billion

- 2026 Market Size: USD 12.77 Billion

- 2034 Forecast Market Size: USD 23.25 Billion

- CAGR: 7.78% from 2026–2034

- North America dominated the alternative protein market with a 37.96% share in 2025.

- The plant-based segment led the market with a value of USD 8.90 billion in 2025.

- Protein isolates dominated the market with a value of USD 4.81 billion in 2025.

North America

North America reached USD 4.51 billion in 2025 and led the market.

Europe

Europe accounted for USD 3.26 billion in 2025, supported by strong plant-based adoption.

Asia Pacific

Asia Pacific was valued at USD 3.02 billion in 2025 and is the fastest-growing region.

U.S.

The market reached USD 3.85 billion in 2025, driven by food technology innovation.

Japan

Growth is supported by advanced food technology and sustainable nutrition trends.

Read More

Alternative Protein Market Trends

Rising Shift Toward Sustainable and Environment-Friendly Protein Sources to Shape Industry Growth

Global food systems are under increasing pressure to reduce greenhouse gas emissions and resource intensity. Alternative proteins require significantly lower land, water, and feed inputs compared to livestock-based proteins. According to the Food and Agriculture Organization, lifecycle assessments, plant-based protein production emits up to 90% fewer greenhouse gases than conventional beef production, while using substantially less freshwater and arable land. This sustainability advantage continues to accelerate adoption across both developed and developing economies.

The alternative protein market is evolving through a series of technological and consumer-driven trends that are reshaping the global food landscape. One of the most significant alternative protein market trends involves the diversification of protein sources beyond traditional plant-based formulations.

Fermentation-based proteins are gaining increasing attention. Precision fermentation enables the production of functional proteins with specific nutritional and sensory attributes. This technology supports the development of alternative dairy and specialty ingredients with improved performance characteristics.

Another notable trend is the advancement of cell culture technologies. Cultivated protein production aims to replicate conventional meat at the cellular level, offering potential improvements in sustainability and supply chain efficiency.

Key trends shaping the alternative protein market include:

- Expansion of fermentation-based and microbial protein solutions

- Increasing development of cell-cultured protein technologies

- Innovation in plant-based protein formulations and textures

- Growth of hybrid products combining multiple protein sources

- Sustainable and Environment-Friendly Protein

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Growing Global Protein Demand to Support Market Expansion

Growing global protein requirements, combined with mounting food security pressures, are key structural drivers that will accelerate global alternative protein market demand over the next decade. These forces are pushing policymakers, investors, and food companies to treat alternative proteins as a strategic tool to secure affordable, sustainable protein supplies. Alternative proteins provide scalable, resource-efficient solutions, positioning them as a critical component of future food security strategies.

- According to the Food and Agriculture Organization of the United Nations (FAO), projections estimate global protein demand to increase by over 50% by 2050, creating significant supply and sustainability challenges.

The alternative protein market is driven by structural shifts in global food demand and increasing pressure on conventional protein supply chains. Population growth and rising protein consumption are intensifying demand for scalable and resource-efficient protein sources, accelerating alternative protein market growth.

Sustainability concerns represent a primary driver. Traditional livestock production requires significant land, water, and energy resources, while contributing to greenhouse gas emissions. Alternative protein solutions offer comparatively lower environmental impact, aligning with corporate sustainability targets and regulatory expectations.

Changing consumer preferences also support market expansion. Health-conscious consumers increasingly seek protein sources perceived as cleaner, plant-based, or functionally beneficial. This shift is particularly pronounced among younger demographics, influencing product innovation and market positioning.

Key drivers shaping the alternative protein market include:

- Increasing demand for sustainable food production systems

- Rising consumer preference for plant-based and functional nutrition

- Expansion of global protein consumption across urban populations

- Strong investment in food technology and innovation ecosystems

Market Restraints

Cost Competitiveness and Processing Complexity to Restrain Market Growth

Despite progress, many alternative protein products remain more expensive than conventional animal proteins, primarily due to processing costs, fermentation infrastructure, and scale limitations. While prices are declining, especially for plant-based proteins, affordability remains a key barrier in price-sensitive markets.

- Cultivated meat, one of the more technologically advanced segments, remains expensive at a small scale. GFI Good Food Institute estimates that production cost could reach USD 2.92 per pound under optimized scenarios by 2030. While this would narrow the price gap, it may still fall short of fully matching conventional meat pricing without further innovation and large-scale commercialization.

Despite strong growth potential, the alternative protein market faces several structural constraints that influence scalability and adoption. Cost competitiveness remains a primary challenge. Many alternative protein products, particularly those based on advanced fermentation and cell culture technologies, remain more expensive than conventional protein sources.

Production scalability also presents limitations. Manufacturing processes for emerging protein technologies often require specialized infrastructure and significant capital investment. Achieving large-scale production while maintaining consistent quality remains a critical industry challenge.

Consumer perception continues to influence market adoption. While plant-based proteins are widely accepted, newer categories such as cultured and insect-based proteins face varying levels of consumer skepticism. Taste, texture, and familiarity also affect purchasing decisions.

Key constraints affecting alternative protein market growth include:

• Higher production costs compared with traditional protein sources

• Limited scalability of advanced production technologies

• Consumer acceptance challenges for novel protein categories

• Regulatory uncertainties across different geographic markets

Market Opportunities

Advancements in Precision Fermentation to Unlock New Growth Avenues

Advances in precision fermentation and microbial protein production are unlocking functional use cases that closely mimic animal proteins. These technologies enable the production of animal-identical proteins (e.g., whey analogs, egg proteins) with targeted amino acid profiles and texture properties suitable for diverse food formulations. The Good Food Institute’s investment data indicates increasing venture capital deployment into fermentation startups, with billions raised annually to scale production and improve cost competitiveness.

- For instance, in April 2025, a South Korea-based food-tech company INTAKE raised USD 9.2 million in a Series C round to scale yeast-based precision fermentation proteins for meat, dairy, egg, and seafood alternatives.

The alternative protein market presents substantial opportunities as global food systems adapt to changing consumption patterns and sustainability requirements. One of the most significant opportunities lies in expanding alternative protein penetration across emerging markets.

Rapid urbanization and rising income levels in developing economies are increasing demand for diversified protein sources. Alternative proteins offer scalable solutions that can support long-term food security and supply chain resilience.

Another key opportunity involves product innovation and formulation improvements. Enhancing taste, texture, and nutritional profiles remains critical for increasing consumer acceptance and expanding market share.

Key opportunities supporting alternative protein market growth include:

- Expansion of alternative protein products in emerging economies

- Development of next-generation fermentation and cell culture technologies

- Increasing use of alternative proteins across diverse food applications

- Growing investment in sustainable food production systems

SEGMENTATION ANALYSIS

By Source

Plant-Based Protein Segment Dominates While Microbial & Fermentation Emerges as Fastest-Growing

On the basis of source, the market is segmented into plant-based, microbial & fermentation, cell culture, insect-based, and others.

Plant-Based

The plant-based segment dominated the global alternative protein market, valued at USD 8.90 billion in 2025, driven by wide availability, regulatory familiarity, cost efficiency, and extensive use in meat, dairy, bakery, and beverage alternatives. Soy and pea proteins remain the most commercially scalable sources.

Plant-based proteins represent the largest and most commercially mature segment within the alternative protein market. Soy protein and pea protein dominate due to established supply chains, functional versatility, and cost efficiency. These proteins are widely used across meat alternatives, dairy substitutes, and processed food applications.

Soy protein continues to hold a significant share due to its complete amino acid profile and well-developed processing infrastructure. Pea protein is gaining traction as manufacturers seek allergen-friendly and non-genetically modified alternatives. Other plant sources, including rice, wheat, and chickpea proteins, contribute to product diversification.

Microbial & Fermentation

Microbial and fermentation-based proteins represent a rapidly advancing segment of the alternative protein market. Precision fermentation enables the production of functional proteins, enzymes, and bioactive compounds with high efficiency.

Fermentation technologies offer advantages in scalability and consistency. Production processes are less dependent on agricultural inputs, reducing exposure to climate variability and supply chain disruptions.

Applications include alternative dairy proteins, specialty ingredients, and protein isolates for functional food products. This segment is attracting significant investment due to its potential to deliver high-performance protein solutions.

However, commercialization challenges remain, including production costs and infrastructure requirements. As technologies mature, fermentation-based proteins are expected to capture an increasing alternative protein market share.

Cell Culture

The cell culture segment is projected to grow at the fastest CAGR of 11.68% during the forecast period. Cell culture-based proteins represent one of the most technologically advanced segments within the alternative protein industry. These proteins are produced by cultivating animal cells in controlled environments, aiming to replicate conventional meat products at the cellular level.

This segment offers potential benefits in terms of sustainability and supply chain control. However, it remains in early commercialization stages, with scalability and regulatory approval representing key challenges.

Investment in research and development continues to support technological progress. As production costs decline and regulatory pathways become clearer, cell culture proteins may play a more significant role in future alternative protein market growth.

Insect-Based

Insect-based proteins represent a niche but growing segment within the alternative protein market. These proteins offer high nutritional value and efficient resource utilization, requiring less land and water compared with traditional livestock.

Adoption remains regionally concentrated, with higher acceptance in certain markets. Applications include animal feed, protein powders, and specialty food products.

To know how our report can help streamline your business, Speak to Analyst

By Type

Isolates Segment Lead the Market due to their High Protein Concentration

Based on type, the market is segmented into isolates, concentrates, hydrolysates, and protein blends.

Isolates

Protein isolates led the global alternative protein market share with a valuation of USD 4.81 billion in 2025, owing to their high protein concentration, neutral flavor profiles, and suitability for premium food and nutrition applications. Protein isolates represent a high-purity segment within the alternative protein market. These products contain a concentrated protein content, making them suitable for applications requiring precise nutritional formulations.

Isolates are widely used in sports nutrition, dietary supplements, and specialized food products. Their functional properties enable manufacturers to control texture and consistency effectively. Demand for isolates is driven by increasing consumer interest in high-protein diets and functional nutrition.

Concentrates

Protein concentrates contain moderate protein levels and are commonly used in mainstream food applications. These products offer a balance between cost and functionality, making them suitable for large-scale food manufacturing. Concentrates are widely used in bakery products, snacks, and meat alternatives. Their versatility supports broad adoption across the food industry.

Hydrolysates

Hydrolysates are partially broken-down proteins designed for improved digestibility and absorption. These products are often used in specialized nutrition applications, including infant formula and medical nutrition. The hydrolysis process enhances functional properties, making these proteins suitable for targeted dietary requirements.

Protein Blends

Protein blends are expected to register the fastest CAGR of 9.71%, driven by manufacturers combining multiple protein sources to improve amino acid balance, texture, and sensory appeal. Protein blends combine multiple protein sources to achieve desired nutritional and functional characteristics. Manufacturers use blends to optimize amino acid profiles, improve texture, and enhance product performance. Blending strategies are increasingly used to differentiate products and address consumer preferences.

By Form

Dry Segment Dominated due to Longer Shelf Life

On the basis of form, the market is segmented into dry and liquid.

Dry

The dry segment accounted for USD 9.56 billion in 2025, benefiting from longer shelf life, ease of storage, and wide application across food processing and supplements. Dry forms dominate the alternative protein market due to ease of storage, transportation, and formulation flexibility. Powders and granules are widely used in food manufacturing and dietary supplements.

Dry proteins offer extended shelf life and compatibility with various processing methods. These advantages support large-scale production and distribution.

Liquid

The liquid segment is projected to grow at a CAGR of 9.56%, driven by increasing use in RTD beverages, dairy alternatives, and liquid nutrition products. Liquid protein forms are used in ready-to-drink beverages, dairy alternatives, and certain industrial applications. These products offer convenience and ease of integration into liquid-based formulations.

However, liquid forms require more stringent storage and transportation conditions. Shelf life considerations and logistical challenges may limit widespread adoption compared with dry formats.

By Application

Meat Alternatives Segment Led, Driven by Strong Retail Penetration

By application, the market is fragmented into meat alternatives, dairy alternatives, bakery & confectionery, snacks & bars, beverages, RTE Meals, dietary supplements, sports nutrition, animal feed, and others.

Meat Alternatives

Meat alternatives dominated the market with USD 4.26 billion in 2025, supported by strong retail penetration, demand for plant-based protein, foodservice adoption, and product offerings innovation. Meat alternatives represent the largest application segment within the alternative protein market. These products aim to replicate the taste, texture, and nutritional profile of conventional meat.

Continuous innovation in formulation and processing technologies supports product development. Consumer demand for plant-based meat substitutes drives significant market growth.

Dairy Alternatives

Dairy alternatives represent another major application area. Products such as plant-based milk, yogurt, and cheese continue gaining consumer acceptance. Fermentation-based proteins are also contributing to this segment by enabling the production of functional dairy proteins without animal inputs.

Bakery & Confectionery

Alternative proteins are increasingly used in bakery and confectionery products to enhance nutritional profiles. Protein-enriched snacks and baked goods cater to health-conscious consumers.

Snacks & Bars

Protein bars and snacks represent a rapidly growing segment. Consumers seek convenient, high-protein options for on-the-go consumption. Manufacturers use alternative proteins to develop functional snack products with improved nutritional value.

Beverages

The beverages segment is projected to grow at the fastest CAGR of 11.06%, driven by demand for protein-enriched functional drinks, plant-based milks, and sports beverages. Protein-enriched beverages are gaining popularity across health and wellness segments. Alternative proteins are used in smoothies, ready-to-drink shakes, and functional drinks.

Regional Insights

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America Alternative Protein Market Analysis

North America Alternative Protein Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America was valued at USD 4.51 billion in 2025 and is projected to grow at a CAGR of 6.37%. The region benefits from high consumer awareness, strong vegan and flexitarian adoption, and advanced food innovation ecosystems. North America leads the alternative protein market due to strong consumer adoption and advanced food technology ecosystems.

Established plant-based brands and increasing investment in fermentation and cell culture technologies support innovation. Retail and food service integration enhances accessibility. High awareness of sustainability and health trends continues to drive alternative protein market growth across the region’s mature consumer base.

U.S. Alternative Protein Market

The U.S. accounted for approximately USD 3.85 billion in 2025, driven by strong retail penetration, institutional adoption, and investment in fermentation-based protein technologies. The United States dominates the North American alternative protein market, supported by robust innovation and strong venture capital investment in food technology.

Major food manufacturers actively expand plant-based and fermentation-derived product portfolios. Consumer demand for sustainable and functional nutrition drives market expansion. Established distribution networks and strong retail presence contribute to increasing alternative protein market share across diverse product categories.

Europe Alternative Protein Market Analysis

Europe accounted for USD 3.26 billion in 2025, expanding at a CAGR of 7.01%. Regulatory support for sustainable food systems and high plant-based adoption underpin market growth. Europe represents a significant alternative protein market driven by regulatory support for sustainable food systems and strong consumer awareness. Countries across the region actively promote plant-based diets and food innovation. The presence of established food manufacturers and research institutions supports product development. Growing demand for environmentally sustainable nutrition continues to strengthen alternative protein market growth across Europe.

Germany Alternative Protein Market

Germany was valued at USD 0.73 billion in 2025, supported by robust vegan food consumption and strong retail infrastructure. Germany plays a central role in the European alternative protein market due to its strong food processing industry and innovation capabilities. Consumers show increasing preference for plant-based and sustainable products. Food manufacturers invest in product development and supply chain expansion. Government support for sustainable agriculture and food technologies further contributes to Germany’s growing alternative protein market share.

United Kingdom Alternative Protein Market

The United Kingdom alternative protein market benefits from strong consumer awareness and a dynamic food innovation ecosystem. Retailers and food service providers increasingly incorporate alternative protein products into their offerings. Demand for plant-based and functional nutrition continues to rise. Investment in food technology startups and research initiatives supports innovation and expansion of the alternative protein market across the United Kingdom.

Asia-Pacific Alternative Protein Market Analysis

Asia Pacific represented USD 3.02 billion in 2025 and is the fastest-growing region, registering a CAGR of 10.45%. Growth is fueled by urbanization, protein demand, and expanding middle-class consumption. Asia-Pacific represents a rapidly expanding alternative protein market driven by population growth and evolving dietary preferences. Increasing urbanization and rising income levels support demand for diversified protein sources. Governments promote food security and sustainable production methods. Expansion of manufacturing capabilities and growing investment in food technology continue to drive alternative protein market growth across the region.

Japan Alternative Protein Market

Japan’s alternative protein market is supported by advanced food technology and strong consumer interest in functional nutrition. Food manufacturers develop innovative plant-based and fermentation-derived products tailored to local preferences. Government initiatives promoting sustainable food systems further support market expansion. High standards in food quality and safety contribute to Japan’s steady alternative protein market growth.

China Alternative Protein Market

China was valued at USD 1.21 billion in 2025, supported by government-backed food innovation programs and traditional plant-protein consumption. China represents a major growth market for alternative proteins due to its large population and increasing demand for diversified protein sources. Government initiatives supporting food security and sustainability drive adoption. Domestic companies invest in plant-based and fermentation technologies. Expanding consumer awareness and improving distribution networks continue to strengthen China’s alternative protein market share.

India Alternative Protein Market

India reached USD 0.60 billion in 2025, driven by vegetarian dietary patterns, soy protein usage, and growing nutraceutical exports.

Latin America & South America Alternative Protein Market Analysis

South America accounted for USD 0.66 billion in 2025, expanding at a CAGR of 8.15%, driven by the region’s strong agricultural base and increasing investment in plant protein processing. Countries such as Brazil and Argentina benefit from abundant soy, pea, and pulse production, enabling cost-competitive plant-based protein manufacturing.

Latin America’s alternative protein market is developing steadily, supported by increasing awareness of sustainable food consumption and growing demand for plant-based products. Countries in the region begin investing in food technology and production capabilities. Expanding retail distribution and improving supply chains contribute to market growth. Rising consumer interest in health and nutrition supports future alternative protein market expansion.

Middle East & Africa Alternative Protein Market Analysis

The Middle East & Africa reached USD 431.22 billion in 2025, growing at a CAGR of 5.50%, with demand primarily driven by food security strategies, import dependency reduction, and health-focused nutrition initiatives. The Middle East and Africa alternative protein market is emerging as governments focus on food security and sustainable production systems. Adoption remains in early stages, with plant-based products gaining traction. Investment in food technology and infrastructure supports gradual market development. Increasing consumer awareness and urbanization are expected to drive long-term alternative protein market growth.

UAE Alternative Protein Market

The UAE alternative protein market was valued at approximately USD 0.13 billion in 2025 and is projected to grow at a CAGR of 6.88% during 2026-2034, positioning the country as one of the most advanced and high-value markets within the Middle East.

Alternative Protein Industry Competitive Landscape

Key Industry Players

Key Players are Focused on Strategic Partnerships to Gain Competitive Edge

Companies in the alternative protein market control upstream protein processing, downstream branded products, and global distribution networks. The top five players exert influence through scale, proprietary formulations, R&D intensity, and strategic partnerships across foodservice, retail, and ingredient supply chains.

The alternative protein market is characterized by a competitive environment involving global food manufacturers, specialized food technology companies, and emerging startups. Market participants compete across product innovation, scalability, cost efficiency, and distribution capabilities.

Large multinational food companies maintain strong positions due to established supply chains and global distribution networks. These organizations increasingly invest in alternative protein portfolios through internal development and strategic acquisitions. Their ability to scale production and integrate products into existing channels supports market expansion.

Food technology startups play a critical role in driving innovation within the alternative protein industry. These companies focus on developing advanced fermentation processes, cell culture technologies, and novel plant-based formulations. Their agility enables rapid experimentation and product differentiation.

Key competitive strategies observed within the alternative protein market include:

- Investment in research and development for next-generation protein technologies

- Strategic partnerships between food manufacturers and technology firms

- Expansion of production capacity to achieve cost competitiveness

- Diversification of product portfolios across multiple application categories

Key Players in the Alternative Protein Market

|

Rank |

Company Name |

|

1 |

Beyond Meat, Inc. |

|

2 |

Impossible Foods Inc. |

|

3 |

Cargill, Incorporated |

|

4 |

Archer-Daniels-Midland (ADM) |

|

5 |

Nestlé S.A. |

List of Key Alternative Protein Companies Profiled

- Beyond Meat, Inc. (U.S.)

- Impossible Foods Inc. (U.S.)

- Archer-Daniels-Midland (ADM) (U.S.)

- Ingredion Incorporated (U.S.)

- Kerry Group (Ireland)

- Nestlé S.A. (Switzerland)

- Cargill, Incorporated (U.S.)

- Roquette Frères (France)

- Tate & Lyle PLC (U.K.)

- Oatly Group AB (Sweden)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Alpine Bio, a molecular farming startup, recently debuted two innovative soy-based proteins: a highly soluble soy protein isolate and an iron-rich lactoferrin produced in soybeans.

- September 2025: Burcon NutraScience Corporation announced the first commercial sales of Puratein C, its high-purity canola protein isolate. Puratein C contains over 90% protein, derived from non-GMO North American canola seeds using a solvent-free process. It offers a complete amino acid profile with all nine essential amino acids and achieves a top PDCAAS score of 1 for digestibility.

- September 2025: Leaft Foods, a New Zealand-based company, announced a strategic partnership with Lacto Japan Co., Ltd., to introduce its innovative Leaf Rubisco Protein to the Japanese market. Rubisco Protein Isolate is extracted directly from green leaves, offering a sustainable, allergen-free alternative to animal proteins such as whey.

- May 2025: Bunge launched a new line of soy protein concentrates, targeting plant-based food manufacturers with clean-taste, neutral-color solutions. The concentrates offer approximately 70% protein and 17% fiber on a dry basis, available in non-GMO and conventional varieties. They come in powdered and textured formats suitable for snacks, baked goods, meat alternatives, and beverages.

- May 2024: Roquette launched NUTRALYS Fava S900M, its first fava bean protein isolate, targeting plant-based meat, dairy alternatives, and baked goods. This ingredient offers over 90% protein content with a clean taste, light color, and strong functional properties such as high gel strength and stability.

REPORT COVERAGE

The global alternative protein market industry report analyzes the market in depth and highlights crucial aspects such as global market trends, supply chain, market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the research report also provides insights into the global alternative protein market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.78% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Source · Plant-Based o Soy Protein o Pea Protein o Others · Microbial & Fermentation · Cell Culture · Insect-Based · Others |

|

|

By Form · Dry · Liquid |

|

|

By Application · Meat Alternatives · Dairy Alternatives · Bakery & Confectionery · Snacks & Bars · Beverages · RTE Meals · Dietary Supplements · Sports Nutritions · Animal Feed · Others |

|

|

By Region · North America (By Type, Source, Form, Application, and Country) • U.S. (By Form) • Canada (By Form) • Mexico (By Form) · Europe (By Type, Source, Form, Application, and Country) • Germany (By Form) • Spain (By Form) • Italy (By Form) • France (By Form) • U.K. (By Form) • Rest of Europe (By Form) · Asia Pacific (By Type, Source, Form, Application, and Country) • China (By Form) • Japan (By Form) • India (By Form) • Australia (By Form) • Rest of Asia Pacific (By Form) · South America (By Type, Source, Form, Application, and Country) • Brazil (By Form) • Argentina (By Form) • Rest of South America (By Form) · Middle East & Africa (By Type, Source, Form, Application, and Country) • South Africa (By Form) • UAE (By Form) • Rest of Middle East & Africa (By Form) |

Frequently Asked Questions

Fortune Business Insights says that the global market was valued at USD 11.88 billion in 2025 and is anticipated to reach USD 23.25 billion by 2034.

At a CAGR of 7.78%, the global market will exhibit steady growth over the forecast period.

By form, the dry segment led the market.

North America held the largest market share in 2025.

Growing global protein demand is the key factor driving market expansion.

Beyond Meat, Inc., Impossible Foods Inc., Cargill, Incorporated, Archer-Daniels-Midland Company (ADM), Nestlé S.A., and others are the leading companies in the market.

The rising shift toward sustainable and climate-efficient protein sources is the key industry trend.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us