Cyber Insurance Market Size, Share & Industry Trends Analysis, By Insurance Type (Standalone and Tailored), By Coverage Type (First-party and Liability Coverage), By Enterprise Size (SMEs and Large Enterprise), By End-user (Healthcare, Retail, BFSI, IT & Telecom, Manufacturing, and Others), and Regional Forecast, 2026-2034

Cyber Insurance Industry Overview

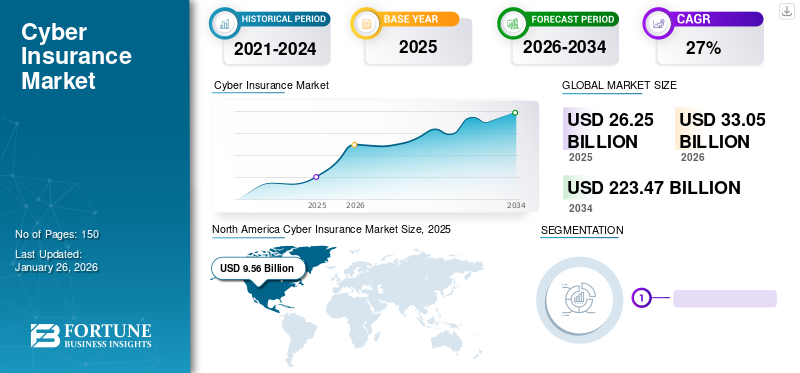

The global cyber insurance market size was valued at USD 26.25 billion in 2025 and is projected to grow from USD 33.05 billion in 2026 to USD 223.47 billion by 2034, exhibiting a CAGR of 27% during the forecast period. North America dominated the global market with a share of 36.4% in 2025. The cyber insurance industry growth is fueled by increasing cyber threats, regulatory compliance requirements, growing digital transformation, and heightened risk awareness.

The usage of cyber insurance solutions helps businesses reduce the risk of cyber threats, such as data breaches and cyberattacks. These solutions protect organizations from the costs of Internet-based attacks that affect information governance, IT infrastructure, and information policies. This attack is often not covered by traditional insurance products or commercial liability policies. The growing cybersecurity risks and data breach activities are enabling businesses to implement cyber insurance policies. Nowadays, small and medium enterprises are also being targeted by cyber attackers. This factor is projected to boost the adoption of new cyber insurance products by small businesses.

The COVID-19 pandemic accelerated the digitalization of business operations and obligated individuals and businesses to embrace remote working. With employees working from home, enterprise Virtual Private Network (VPN) servers have become necessary for organizations. Owing to this, cybercriminals across the globe saw opportunities to capitalize on the crisis. The pandemic period recorded a rise in mail spam, ransomware attacks, and phishing attacks as hackers were using this crisis as bait to imitate brands, thereby misleading employees.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

Latest Cyber Insurance Industry Trends

Market Expansion to be Impelled by Rising Adoption of Crypto Insurance Services

Crypto ownership has been growing daily across the globe. With increasing crypto ownership, crypto threats are rising at an accelerated pace. Highly unstable cryptocurrency serves as the target of multimillion-dollar hacks, leading to investors losing millions and the sector shedding billions. For instance, in March 2022, hackers stole cryptocurrency worth almost USD 540 million from the blockchain project Ronin. This was recorded to be one of the largest cryptocurrency heists on record.

To tackle these crypto-threats, companies have been investing in insurance policies to help them counter these threats. Furthermore, a survey from Goldman Sachs showcases that 11% of the U.S. insurance companies have either shown interest in a current investment or are planning to invest in cryptocurrencies. Insurers expect to broaden and strengthen their return on this investment in the coming years.

Thus, the rising number of crypto threats and the number of insurance companies investing in crypto insurance are expected to positively influence the market growth over the forecast period.

In recent years, there has been a rise in the frequency of claims for cyber insurance, which creates a volatile risk environment that results in continuous premium hikes for policyholders. However, the market experienced profitability in 2022 and allowed for conditions to ease during 2023. Still, numerous insureds notice coverage restrictions and scrutiny from underwriters regarding cybersecurity practices and exclusions for certain losses. Artificial intelligence (AI) exposures, data collection concerns, Business Email Compromise (BEC) risks, and ransomware threats are a few key trends to be observed during the forecast period.

Cyber Insurance Industry Growth Factors

Increasing Cyberattacks and Data Breaches among Enterprises to Drive Market Growth

Cyberattacks and data breaches are increasing worldwide among all sizes of enterprises. According to Forbes, the percentage of ransomware attacks that hit organizations jumped to 66% in 2021, with a 29% year-over-year growth. These rising cyberattacks impacted the organizations’ operating ability, which is expected to boost the market growth.

Moreover, according to the latest U.K. government survey in 2023, 32% of businesses and 24% of charities were hit by cyber breaches and cyber attacks in the past year. This is higher for 69% of large companies and 59% of medium businesses. Among such cyber breaches and attacks, the U.K. government estimates that a business of small and medium size suffered a loss of USD 1,384, while a large size business incurred a loss of USD 6,240.

Industries, including BFSI, healthcare, education, and retail are being targeted by hackers and threat actors owing to the large volume of stored customer data. Also, growing digitalization, internet banking, mobile banking, online shopping, digital payment, and electronic medical records will increase the risks of data breaches in these industries.

Cyber insurance offers companies comprehensive coverage and helps minimize the post-cyberattack impact. Thus, increasing cybercrime will surge the demand for various policies.

RESTRAINING FACTORS

High Premium Cost to Hamper Market Growth

Cyber insurance benefits many industries with protection against cybercrimes and threats, resulting in increasing demand for insurance policies. However, the market faces challenges with the high premium cost of an insurance policy. The hike in the price of policies by insurance companies is hampering their continuation and renewal. Premium rates are increasing by 30%, and companies, including American International Group Inc., are reducing coverage limits as the costs soar.

Small & Medium Enterprises (SMEs) with limited funds hesitate to invest in security insurance due to this factor. Thus, high cost is expected to hinder the market growth.

Cyber Insurance Industry Segmentation

By Insurance Type Analysis

Maximum Coverage through Standalone Insurance Type to Boost Market Growth

Based on insurance type, the market is categorized into standalone and tailored.

The standalone segment is likely to gain the maximum market share of 58.55% in 2026 owing to its comprehensive cover policy. A standalone type of insurance protects an organization from lawsuits filed for breaches of security or privacy that allege a failure to protect sensitive information. Moreover, standalone policies cover a range of asset risks, including business interruption, data loss/destruction, and funds transfer loss.

The tailored segment is anticipated to record the highest CAGR during the forecast period owing to the availability of various customized solutions. Tailored insurance is gaining popularity among sectors, such as BFSI, healthcare, IT, and telecom due to its coverage of possible industry risks.

By Coverage Type Analysis

Increasing Cyber Crime to Surge First-party Coverage Demand

Based on coverage type, the market is categorized into first-party and liability coverage.

The first-party coverage segment is expected to lead the market with a share of 54.01% in 2026. First-party insurance covers cases where victims are directly involved in the incident. It provides financial assistance to businesses to mitigate the effect of data breaches and cyberattacks. The increasing online theft, hacking activities, extortion, and data destruction are likely to fuel the first-party segment growth.

The liability/third-party coverage segment is expected to record the highest CAGR during the forecast period. Liability insurance is in high demand as it has become an integral part of risk management programs. Liability coverage is tailored to businesses' specific needs, with benefits, such as loss coverage from business interruption, data breach coverage, forensic assistance in defending against cyber extortion, and coverage beyond typical liability policies.

Thus, firms dealing with clients' confidential data are significantly adopting third-party coverages.

By Enterprise Size Analysis

High-Volume Data Generation to Boost Insurance Investment of Large Enterprises

The market is segmented into Small & Medium Enterprises (SMEs) and large enterprises based on enterprise size.

The large enterprises segment is likely to lead the market with share of 53.98% in 2026 owing to high-volume data generation. This increases cybercrimes and incidents of massive data breach. Large enterprises invest extensively in risk management solutions to ensure the safety of client and company data.

The SMEs segment is also expected to witness significant growth during the forecast period. SMEs are the new target of hackers. Therefore, small businesses are keen on investing in cybersecurity insurance solutions.

By End-user Analysis

To know how our report can help streamline your business, Speak to Analyst

Mandate Protection of Vital Customer Data to Surge Insurance Demand in BFSI Sector

Based on end-user, the market is categorized into healthcare, retail, BFSI, IT & telecom, manufacturing, and others.

The BFSI segment is likely to hold the largest share during the forecast period. Consumers' inclination toward digitalization, mobile applications, and internet banking is anticipated to increase cyber risks. Due to vast data generation in the financial sector, it becomes an easy target for hackers. This is likely to surge the demand for cybersecurity insurance in the BFSI industry, thereby propelling the segment’s growth. The retail segment will account for 23.87% market share in 2026.

The healthcare industry is projected to register the highest CAGR during the forecast period. The adoption of insurance policies in the healthcare industry is on the rise due to increase in data breaches in this sector. The healthcare sector reported around 4,419 data breaches involving more than 500 records between 2009 and 2021.

REGIONAL INSIGHTS

Geographically, the market is divided into five key regions - North America, South America, Europe, the Middle East & Africa, and Asia Pacific. They are further categorized into countries.

North America Cyber Insurance Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America accounted for USD 9.56 billion in 2025, representing 36.40% of the global market share, and is projected to reach USD 11.98 billion in 2026. The regional growth is driven by increasing cyberattacks and high risk of data loss. The US market holds the maximum share in the region owing to the country's strong government regulation and strict policy in ensuring cybersecurity. Also, the growth is due to the presence of dominant solutions providers. The U.S. market is projected to reach USD 6.31 billion by 2026. North America dominated the market with a valuation of USD 9.56 billion in 2025 and USD 11.98 billion in 2026. The U.S. market is projected to reach USD 6.31 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

Asia Pacific

In 2025, Asia Pacific held 24.60% of the global market, reaching a valuation of USD 6.46 billion, and is projected to grow to USD 8.36 billion in 2026. Asia Pacific is expected to witness significant growth during the forecast period owing to increasing ransom attacks and risks in the region. In 2021, countries with the highest increase in cyberattacks in Asia Pacific are Japan, Singapore, Indonesia, and Malaysia, with increases of 40%, 30%, 25%, and 22% respectively. Moreover, governments, including Japan, India, South Korea, and China are investing in insurance to lessen the impact of cybercrimes. The Japan market is projected to reach USD 2.03 billion by 2026, the China market is projected to reach USD 2.2 billion by 2026, and the India market is projected to reach USD 1.52 billion by 2026.

As per a report by Cyber Risk Management, insurance demand in Asia Pacific for cybersecurity increased by 87%.

Cyber insurance solutions are gaining traction in Asia Pacific due to rapidly growing connectivity. The accelerating digital transformation exposes an organization and makes it vulnerable to cyber exploitation.

Europe

The Europe market was valued at USD 6.21 billion in 2025, capturing 23.70% of global revenue, and is estimated to reach USD 7.83 billion in 2026. Europe is poised to gain a prominent market share during the forecast period. The regional market’s growth is attributed to the changing insurance regulatory rules that increase the demand for these insurance services. According to research by Wavestone, Marsh, and law firm CMS, insurance claims are more than the number of policies across Europe, as digitalization among organizations remains vulnerable to malicious cyberattacks. The UK market is projected to reach USD 1.22 billion by 2026, while the Germany market is projected to reach USD 1.25 billion by 2026.

South America

The South America market accounted for USD 1.9 billion in 2025, representing 7.20% of the global industry, and is expected to reach USD 2.3 billion in 2026. South America is likely to gain steady growth during the forecast period. The demand for cyber policies is increasing in South America as the region has witnessed a surge in Distributed Denial of Services (DDoS) attacks under one gigabyte per second (Gbps). This will create opportunities for insurance providers to expand their regional product offerings and customer base.

Middle East & Africa

Similarly, the Middle East & Africa is likely to showcase significant growth during the forecast period. Middle East & Africa contributed approximately USD 2.12 billion to the global market in 2025, accounting for 8.10% share, and is expected to reach USD 2.58 billion in 2026. Nations, such as Qatar, Oman, the U.A.E., Bahrain, and others are powerfully moving toward digitization in the security and observation areas, which is projected to propel the regional market growth.

Competitive Landscape

Strategic Collaborations and Partnerships to Boost Market Footprint of Key Players

Key players are trying to expand their operations and increase their global presence through partnerships and collaborations. This enables them to develop their cyber security offerings and customer base. For instance,

- April 2022: Beazley Group and Cytora partnered to streamline insurance for clients and brokers, accelerate profitable growth, and automate risk processing. By implementing the Cytora platform, Beazley will modernize the global underwriting operations, improve straight-through processing, and reduce manual processes.

- July 2022: Spring Insure launched a commercial cyber offering personalized for Small and Medium-sized Enterprises (SMEs). This cyber offering delivers protection against loss from a cyber-attack and provides access to Beazley Cyber services, including risk management and pre-breach services.

List of the Key Cyber Insurance Companies Profiled:

- Travelers Indemnity Company (US.)

- AXA XL (US.)

- Chubb (Switzerland)

- American International Group, Inc. (US.)

- Beazley Group (UK.)

- AXIS Capital Holdings Limited (Bermuda)

- CNA Financial Corporation (US.)

- BCS Financial Corporation (US.)

- The Hanover Insurance, Inc. (US.)

- Zurich Insurance (Switzerland)

LATEST CYBER INSURANCE INDUSTRY DEVELOPMENTS:

- March 2023: Saiber Innovation Technologies entered a partnership with CYMAR Management Ltd., a cyber-insurance specialist, to fulfill the cyber insurance needs of the maritime & logistics sector in the U.A.E. and help protect this sector from cyber-attacks.

- February 2023: Cowbell, a cyber-insurance provider, entered a partnership with Millennial Shift Technologies to deliver Cowbell’s cyber insurance programs named as Cowbell Prime 100 and 250 to access Millennial Shift's e-trading broker platform, mFactor, for better operations.

- July 2022: SBI General introduced the SBI General Cyber VaultEdge insurance plan, an insurance cover that provides protection against financial losses that occur due to cyber risks and attacks.

- October 2022: AXA XL formed an incident response team in the Americas. The Cyber Incident Response team determines commitment to the clients and helps them before, during, and after a cyber-incident.

- July 2022: AXA XL announced cyber insurance roles and regional management appointments in the U.S. These roles will focus on the company's growth strategy and discover innovative methods to address complicated cyber & technology risks.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The research report highlights leading regions across the world to offer a better understanding of the significant trends in the market. Furthermore, it provides insights into the latest industry trends and analyzes technologies deployed at a rapid pace at the global level. The report further highlights some growth-stimulating factors and restraints, helping the reader gain in-depth knowledge about the market.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 27% from 2026 to 2034 |

|

Segmentation |

By Insurance Type

By Coverage Type

By Enterprise Size

By End-user

By Region

|

Frequently Asked Questions

The market is projected to reach USD 223.47 billion by 2034.

In 2025, the market value stood at USD 26.25 billion.

The market is projected to record a CAGR of 27% during the forecast period of 2026-2034.

The BFSI segment is likely to hold the maximum market share during the forecast period.

Increasing cyberattacks and data breaches among enterprises will drive the market growth.

Travelers Indemnity Company, AXA XL, Chubb, American International Group, Inc., Beazley Group, AXIS Capital Holdings Limited, CNA Financial Corporation, BCS Financial Corporation, The Hanover Insurance, Inc., and Zurich Insurance are the top players in the market.

North America is expected to hold the highest market share.

Asia Pacific is expected to register a significant CAGR.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us