Wood Pellets Market Size, Share & Industry Analysis, By Feedstock (Forest Waste, Agricultural Waste, and Others), By Application (Heating, Combined Heat & Power (CHP), and Power Generation), By End-user (Residential, Commercial, and Industrial), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

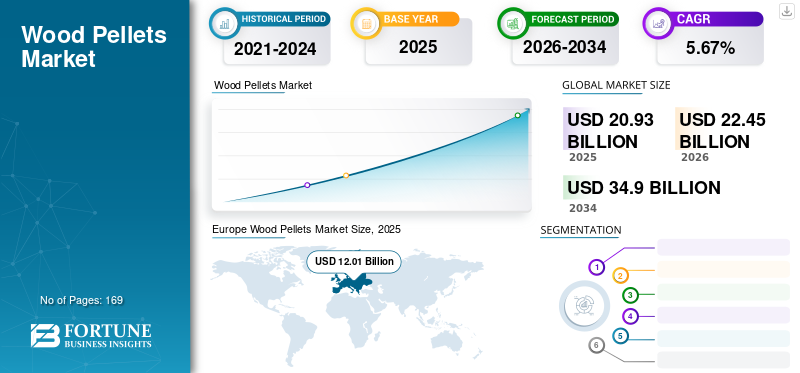

The global wood pellets market size was valued at USD 20.93 billion in 2025 and is projected to grow from USD 22.45 billion in 2026 to USD 34.90 billion by 2034, growing at a CAGR of 5.67% from 2026 to 2034. Europe dominated the market with a share of 57.42% in 2025. The market is driven by increasing renewable energy demand, strict carbon regulations, government incentives & continuous technological innovations. Cost-effectiveness & widespread adoption across residential, industrial & power sectors further bolster market expansion.

Pellets were originally produced as an alternative to oil, particularly for heating, due to their high fuel density and quality. Various factors, such as resource availability, geographical characteristics, climate, and other economic factors, influence market growth. These market elements are intertwined with the intervention of various national and regional policies, weaving a complex trading web. The steady and rapid growth of the market is driven by various factors related to different market segments (industrial pellet for co‐firing, industrial pellet for CHP and district heating, and pellet for residential heating); however, the markets are still quite dependent on different extents on the availability of direct or indirect support measures.

Download Free sample to learn more about this report.

Global Wood Pellets Market Overview

Market Size:

- 2025 Value: USD 20.93 billion

- 2026 Value: USD 22.45 billion

- 2034 Forecast Value: USD 34.90 billion, with a CAGR of 5.67% during 2026–2034

Market Share:

- Regional Leader: Europe, which commanded a dominant 91.76% share of the global wood pellets market in 2023

- Fastest‑Growing Region: While Europe leads now, North America (particularly the U.S.) is projected for strong growth, nearing USD 976.98 million by 2032 thanks to renewable energy mandates

- End‑User Leader: The industrial segment holds the leading share globally, thanks to widespread use in power generation, CHP, district heating, and co‑firing applications

Industry Trends:

- Massive European dominance: Europe’s share stood at around 57.42% in 2025, making it the principal consumer and producer of wood pellets globally

- COVID‑era boost: Demand exceeded expectations during the pandemic as biomass energy policies accelerated uptake across multiple regions

- Feedstock shift toward forest waste: Wood pellets are predominantly produced from forestry residues, which remain the largest and most reliable feedstock segment

- Industrial applications dominate: Usage is increasingly focused on large-scale power and CHP facilities that require high fuel density and low emissions

Driving Factors:

- Rising fuel prices: Increases in oil, coal, and gas prices are prompting a shift toward cost-competitive wood pellet fuel options

- Sustainability mandates and policy support: Strong regulatory frameworks in Europe and North America favor biomass under renewable energy targets and carbon reduction goals

- Abundant and low-cost feedstock: Forestry residues (e.g. sawmill byproducts) provide a reliable, low-cost supply base for pellet production

The global COVID-19 pandemic was unprecedented and staggering, with wood pellets experiencing higher-than-anticipated demand across all regions compared to pre-pandemic levels. The strategies are drafted to empower companies to continue operations effectively with fiscal benefits. Accordingly, the revival of industry verticals is set to unveil new possibilities for integrating reliable virtual power plant solutions to maximize efficiency and mitigate operational risks. The outbreak of the COVID-19 pandemic impacted the sustainable energy industry significantly across the globe. As a result of the current scenario, various pellet manufacturers worldwide had to limit their operation and services in several locations, as countries were stringently implementing lockdown measures to deal with the pandemic.

Download Free sample to learn more about this report.

Wood Pellets Market Trends

Rapid Demand for Electricity to Increase the Demand for the Product

Rapid population growth, the flourishing industrial sector, and the rapid expansion of infrastructure have led to a significant increase in the demand for electricity. As electricity demand increases, regions around the world are increasing their electricity generation capacity by expanding the capacity of existing plants or installing new plants. Due to stringent government policy regarding CO2 emissions, industry players are more prone to use renewable energy sources to generate electricity, especially bioenergy, solar energy, and wind power.

In the race to tackle climate change, minimize GHG emissions, and fulfil the Kyoto Protocol agreements, wood pellets draw significant attention worldwide as an innovative strategy. As per the U.K. Environment Agency, minimizing greenhouse gas emissions from biomass energy generation, pellets made from wood can reduce carbon emissions relative to coal between 74% and 90%.

According to the World Energy & Climate Statistics – Yearbook 2022, global power consumption will increase by 5.5% in 2021. China, the largest electricity consumer with 31% of global consumption, triggered the COVID-19 recovery. European countries, including Germany, France, and Italy, have shown a strong increase in consumption, and consumption in Asian countries, including South Korea, Indonesia, and India, rose by 5% during 2021.

Wood Pellets Market Growth Factors

Increasing Primary Fuel Prices to Drive the Market

Wood pellets are made from by-products of forests, such as agricultural waste and sawdust. It is becoming increasingly popular around the world due to rising primary fuel prices. There is high product demand as biomass fuel is increasing rapidly worldwide due to the high demand for industrial and commercial purposes. In addition, the easy availability of pellets as a fuel raw material and the low production costs have led to higher consumption in the industrial sector.

Europe holds the largest market share, and many European key players are converting their coal to biomass power plants. Furthermore, governments across Europe are choosing wood types of pellets and other renewable energy to meet their renewable energy commitments by using biomass to generate electricity. For instance, the Drax Group has started converting its units from coal to wood fuel as the U.K. government imposes tough limits on CO2 emissions to help fight climate change. The U.K. also announced its plan to completely phase out coal-fired power generation by 2025 completely, and under the E.U., biomass is legally classified as a CO2-neutral energy source. Due to insufficient domestic production of pellets in Europe, several countries are largely dependent on imports. According to the Global Agricultural Information Network (GAIN), Europe imported around 5.4 million tons of market value worth USD 924 million in 2021.

Moreover, according to USDA (U.S. Department of Agriculture) Foreign Agricultural Services, the U.S. exported 1.01 million metric tons of wood pellets in December 2023, and the total export for 2023 was 9.54 million metric tons. The U.S. exported these wood pellets to over 16 countries, the U.K. being the top destination, which exported 653,970 metric tons, followed by Japan at 130,830 metric tons and Denmark at 126,693 metric tons. The total annual exports reached USD 1.75 billion compared to USD 1.56 billion in 2022.

Supportive Government Policies and Initiatives to Propel the Growth of the Market

Recently, due to rapid industrialization, CO2 emissions have increased significantly, which led to climate change. The growing global population, thriving industrial sector, and expansion of infrastructure have led to an enormous increase in the demand for electricity. Governments around the world are striving to reduce the effect of climate change by increasing the uptake of renewable technologies. Governments are offering various global tax incentive programs such as State sales tax exemption, state income tax credit, corporate income tax deduction, and local property tax exemption to encourage renewable adoption. Many federal incentives are also available to corporations, nonprofits, and community projects. These include a modified Accelerated Cost Recovery Scheme (MACRS), tax incentives for subsidies, and business tax incentives. Government support and regulations, including subsidy programs and business tax incentives that provide tax benefits and investment grants, play a key role in promoting the global market. Various government programs, such as the Renewable Heat Incentive (RHI), have generated significant interest in the U.K. pellet market. Such programs are expected to drive the market in the long term.

In 2024, the U.K. government proposed extending the existing subsidies on wood pellets electricity generation. The government is backing new financial support for the old subsidy of around USD 760 million, extending from 2027 to 2030. It will financially support companies that generate electricity from wood pellets, including Britain’s largest power station, Drax in North Yorkshire.

RESTRAINING FACTORS

Fulfilling Certification Criteria May Act as an Impeding Factor for Market Growth

Government certification helps assure customers that the wood pellets come from sustainably achieved forests, proving it to be a valuable tool. Increasing the certification measures for export to European countries and other countries where numerous directives mandate the production of renewable energy is a key constraint on the wood pellets market growth.

Program for the Endorsement of Forest Certification (PEFC), The Sustainable Forestry Initiative (SFI), the Forest Stewardship Council (FSC), and the American Tree Farm System are some of the largest forest certification standards organizations and systems in the world. FSC and SFI are recognized in the U.S., while FSC and PEFC have excellent reputations in Europe. The latter requires the protection of water, wildlife, visual quality, special sites, and other essential resources.

In the industry, pellet producers are worried about sustainability certification. This is to show their customers and governments that pellets used for electricity are sustainably produced. In the heating sector, third-party quality certifications are becoming increasingly important to give consumers peace of mind that the pellets they buy are performing optimally in stoves and boilers.

For instance, norms laid down by the Forest Stewardship Council and Sustainable Forestry Initiative, a certification organization in North America, restrict the market growth in the U.S. Presently, the U.S. owns hectares of forest land, which is more than 300 million. Though, major U.S. standards count only 19% of U.S. commercial forestland.

Wood Pellets Market Segmentation Analysis

By Feedstock Analysis

Forest Waste Segment Holds the Dominant Market Share Due to its Convenience

On the basis of feedstock, the market is split into agricultural waste, forest waste, and others. Forest waste is expected to hold the dominant market share of 92.63% in 2026. as pellets are mainly made from the by-products of conventional forest operations, which include finished wood products and sawmills. Several key players, such as Drax Group and Eviva, own private forests for pellet production. In the U.S., about 85% of forest land is owned by private families and small landowners. The majority of these landowners accomplish their land as a working forest or forest that is carefully managed to provide a sustainable supply of forest products to numerous industries.

The agricultural waste segment is anticipated to rise significantly in the market during the study period. According to Global Bioenergy Statistics, energy production from agricultural residues could account for about 3%-14% of the world's total energy supply.

By Application Analysis

Power Generation Segment Holds the Dominant Market Share Due to the Growing Shift toward Biomass Utilization

Based on application, the market is segmented into heating, Combined Heat & Power (CHP), and power generation.

The power generation segment holds the dominant market share 51.66% in 2026 globally as governments worldwide attempt to switch to biomass power generation. The demand is expected to increase due to urbanization, industrialization, and population growth. Furthermore, biomass gasifiers are in increasing demand as rural electrification enables decentralized power generation.

Releases from the chimney from the use of wood energy to generate electricity and heat are marked as carbon neutral by regulators and policymakers globally. This will have a positive impact on market growth in all regions. Wood pellets are considered to be better than coal or fossil fuels for the environment that old power plants use to generate electricity. According to the U.K. Environment Agency, substituting biomass for coal has reduced CO2 emissions.

Combined heat and power generation is expected to grow significantly over the forecast period. Biomass CHP is currently qualified for both heat and electricity promotion. This makes them a potentially attractive investment option in areas with a continuous and sustained need for heat, provided the electricity generated can be used on-site or fed into the grid.

By End-user Analysis

To know how our report can help streamline your business, Speak to Analyst

Industrial Segment to Hold the Dominant Market Share to Meet the Global Carbon Emission Goal

Based on end-users, the market is segmented into residential, commercial, and industrial.

The industrial segment is expected to hold the dominant market share of 59.73% in 2026. due to the international drive to minimize CO2 emissions, majorly from the industrial sector. Wood pellets are becoming an increasingly attractive fuel for power generation, according to new research from N.H. Agricultural Experiment Station at the University of New Hampshire, the use of pellets reduces GHG emissions by more than 50% compared to fossil fuels and natural gas. For instance, the Drax power station was originally envisioned as a large coal power station to add capacity to the national grid. Still, currently, it has become the largest power station in the U.K. and Western Europe, which has six boilers, four of which burn biomass to minimize carbon emission.

The residential segment is expected to grow at a stagnant rate during the forecast period as pellets are becoming popular among household users due to their characteristics, such as eco-friendliness, cleaning, and sustainability. These are used not only for home cooking and heating but also as horse bedding and cat litter.

The commercial segment is expected to grow considerably during the forecast period as pellets are environment-friendly compared to gas, oil, and electricity alternatives. Currently, the most commonly used fuels for commercial greenhouses are fossil fuels, resulting in higher heating costs and a significant environmental impact.

REGIONAL INSIGHTS

On the basis of geography, the global market is analyzed across North America, Asia Pacific, Europe, and the rest of the world.

Europe

The market in Europe reached USD 12.01 billion in 2025, representing 57.42% of total market revenue, and is projected to reach USD 12.74 billion in 2026. As per the European Pellet Council, Europe remained the world’s largest consumer of industrial pellets. Great Britain was the largest user of pellet-based energy, using more than 8 million tons. In Belgium, the U.K., and the Netherlands, the domestic use of pellets is small, and large power plants dominate the market. The governments of these countries have chosen to meet their renewable energy commitments by using sustainable biomass to generate electricity. Since these countries do not have adequate domestic production of pellets, they are largely dependent on imports.

Europe Wood Pellets Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia Pacific contributed approximately USD 7.66 billion to the global market in 2025, accounting for 36.62% share, and is expected to reach USD 8.39 billion in 2026. The Asia Pacific market is projected to grow the most during the forecast period. The Japan market is valued at USD 1.68 billion by 2026, the China market is valued at USD 5.16 billion by 2026, and the India market is valued at USD 5.16 billion by 2026. South Korea, China, and Japan are the largest consumers of pellets. South Korea imports its pellets mainly from Malaysia and Vietnam, while Japan mainly sources them from Canada.

North America

In 2025, North America held 5.17% of the global market share, reaching a valuation of USD 1.08 billion, and is projected to grow to USD 1.14 billion in 2026. Moreover, the North American region holds a significant market share. The U.S. market is valued at USD 0.77 billion by 2026, supported by the presence of over 24 million acres of lowland hardwood forests, accounting for 65% of the North American region. Additionally, the U.S. Southeast has emerged as a major supplier and net exporter of pellets, and the industry continues to thrive on abundant timber resources. The wood pellets market in the U.S. is projected to grow significantly, reaching an estimated value of USD 976.98 million by 2032, driven by federal and state renewable energy mandates and efforts to reduce GHG emissions.

Rest of the World

The Rest of the World market accounted for USD 0.17 billion in 2025, representing 0.80% of the global industry, and is expected to reach USD 0.18 billion in 2026.

List of Key Companies in Wood Pellets Market

Key Participants are Concentrating on Enhancing their Product Capacities

The market is highly fragmented, with numerous players. Each of the present companies in the market has a strong foothold in their base country and region. Drax Group plc, Enviva, LP, and Rentech Inc. are the leading major players with a strong presence across different countries. The success of their operational plants will help them acquire contracts and have a considerable market share in the coming years.

In 2021, Enviva LP held the largest market share. The company owns and operates plants with a combined production capacity of about 6.2 million metric tons of wood pellets per year in Florida, North Carolina, Virginia, South Carolina, Mississippi, and Georgia. The company is the major supplier of industrial pellets to European countries. Wood Pellet Energy U.K. (LTD), German Pellets Trading GmbH, Snow Timber Pellets, LLC, Lignetics, and the Westervelt Company are the other key players operating in the market.

The competition among top players in the market is very high as they are targeting to expand across regions. The one with unique offerings in technology, portfolio, design, efficiency, and more will capture the maximum end-user attention.

Again, the market is not stagnant; if a company comes up with extra benefits and advancements, other companies will target more innovation. So, there is always hardcore competition among top-notch players.

List of Key Companies Profiled:

- Drax Group PLC (U.K.)

- Enviva, LP (U.S.)

- The Westervelt Company (U.S.)

- Fram Renewable Fuels LLC (U.S.)

- Rentech Inc. (U.S.)

- Wood Pellet Energy U.K. (LTD) (U.K.)

- German Pellets Trading GmbH (Germany)

- Snow Timber Pellets, LLC (U.S.)

- ENERGEX AMERICAN, INC. (U.S.)

- LIGNETICS (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- August 2022 - The Drax Group signed an agreement with Princeton Standard Pellet Corporation (PSPC) to acquire their pellet plant in Princeton, British Columbia, and Canada, which has been in operation since 1995 and can produce 90,000 tonnes of wood pellets per year, mainly from sawmill residues. Once the acquisition is complete, the plant is expected to contribute to the group's strategy to increase pellet production to 8 million tons per year by 2030.

- April 2021 - Drax announced the acquisition of the whole issued share capital of Pinnacle Renewable Inc. Pinnacle would operate as a subsidiary of Drax and remain headquartered in British Columbia. Over 480 Pinnacle employees, including its existing leadership, will be welcomed into the Drax Group.

- July 2020 - Enviva acquired all limited liability interests in Georgia Biomass Holding LLC, a Georgia limited company and indirect owner of a wood pellet manufacturing facility in Waycross, Georgia, for an aggregate consideration of USD 164.0 million in cash, after taking into account certain collateral adjustments. The acquisition of Georgia Biomass was accounted for as a business combination and accounted for using the purchase method.

- June 2020 - Drax Group plc. and Mitsubishi Heavy Industries Group signed an agreement to build new bioenergy with a pilot carbon capture and storage (BECCS) plant. This newly constructed pilot plant will allow Mitsubishi Heavy Industries (MHI) to demonstrate that its BECCS technology can be deployed at scale and help achieve the U.K.'s zero-carbon targets.

- October 2019 - Enviva Partners L.P. constructed a new manufacturing plant in Lucedale, Mississippi, U.S. The company will invest nearly USD 140 million in these new plants. The company has eight manufacturing plants located in the southeastern U.S., which produce more than 3 million metric tons of pellets annually. Construction of these new plants will be completed in 15 to 18 months.

REPORT COVERAGE

The research report provides a detailed regional analysis of the market and focuses on key aspects such as the system's competitive landscape, types, and applications. Besides this, the report offers insights into the wood pellets market analysis and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the market growth opportunities in recent years.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.67% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Feedstock

|

|

By Application

|

|

|

By End-user

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights study shows that the global market was USD 20.93 billion in 2025.

The global market is projected to grow at a CAGR of 5.67% in the forecast period.

The market size of Europe stood at USD 12.01 billion in 2025.

Based on end-user, the industrial segment holds the dominating share in the global market.

The global market size is expected to reach USD 34.90 billion by 2034.

Increasing primary fuel prices are driving the global demand for wood pellets.

The top players in the market are Drax Group plc, Enviva, LP, the Westervelt Company, and Rentech Inc.

- 2021-2034

- 2025

- 2021-2024

- 169

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us