Passive Fire Protection Market Size, Share & Industry Analysis, By Product (Cementitious Materials, Intumescent Coatings, Fireproofing Cladding, and Others), By End-use Industry (Oil & Gas, Infrastructure & Construction, Industrial, Transportation, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

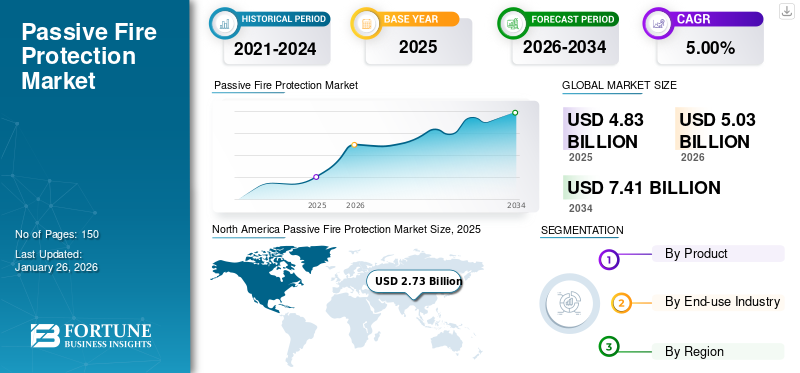

The global passive fire protection market size was USD 4.83 billion in 2025 and is projected to grow from USD 5.03 billion in 2026 to USD 7.41 billion by 2034 at a CAGR of 5.00% during the forecast period (2026-2034). North America dominated the passive fire protection market with a market share of 56.50% in 2025. Moreover, the passive fire protection market in the U.S. is projected to grow significantly, reaching an estimated value of USD 2,956.3 million by 2032, driven by the stringent fire safety regulations and the increasing infrastructure development in the U.S.

Increasing oil & gas company investments in exploration and production, as well as technological developments, are projected to drive this market during the forecast period. As. the oil & gas sector demand passive fire prevention coatings in equipment protection and other offshore and onshore applications. Furthermore, the increase in demand from end-use sectors such as building & construction, and transportation is anticipated to propel the market.

COVID-19 had a significant influence on the building sector in early 2020. The majority of building projects came to a standstill, with no additional updates provided. However, the impact on the building sector differed in different parts of the world. At the same time, the construction sector in the U.S. has witnessed mass layoffs. Construction activity in southern Europe dropped by 60-70 percent.

Download Free sample to learn more about this report.

Passive Fire Protection Market Trends

Increasing Usage of Lithium-ion Batteries for Electric Vehicles is a Prominent Trend

Electric vehicles (EVs) are becoming immensely popular across the world. This is primarily due to air quality and environmental restrictions, as well as customer demand and less expensive rechargeable energy storage devices. Furthermore, major advancements have made many storage devices, particularly those in the lithium-ion family, suitable for vehicle use. As more LIB-powered road vehicles become operational across the world, their role in traffic incidents is expected to increase. For individuals engaged in or reacting to accidents in conventionally fuelled cars, the onboard energy storage system is a dangerous element.

While the dangers associated with conventional cars are well-defined and well accepted in society, LIB-powered road vehicles will require more time and education to attain this level of comfort. When it comes to EVs, there's a chance that the LIB will re-ignite after being damaged for an extended period of time or after being extinguished. This issue affects not just firemen but also people who work with damaged EVs in towing, workshops, scrapyards, or recycling. The global demand for lithium-ion battery-powered road cars continues to rise.

- North America witnessed a passive fire protection market growth from USD 2.73 Billion in 2025 to USD 2.84 Billion in 2026.

As more of them are put into service across the world, their participation in traffic accidents and fires is expected to increase. This can harm the lithium-ion battery, posing a risk to occupants, rescuers, and anyone working on the scene of the accident. The transition to new and varied modes of transportation and infrastructure, however, brings with it new hazards. As a result, it's critical to have a fundamental understanding of these vehicles, as their use in traffic incidents is anticipated to rise. Electric and hybrid vehicle fires, according to the National Fire Protection Association (NFPA), require more water and take longer to extinguish than traditional automobile fires.

Additional reinforcements to battery packs might be added to minimize possible infiltration during specific impact circumstances. Passive and active protection are two methods used to solve the problem. These approaches pertain to increasing the structure's physical strength or using inflatable structures to distribute the load during a crash occurrence, respectively. They were able to minimize the quantity of infiltration by 26 percent with active protection and 58 percent with passive protection utilizing these approaches. The FAA (Federal Aviation Administration) in the U.S. has reported 121 events (including plane crashes) in the last ten years. For electric vehicle battery compartments, 3M offers Sikagard fire protective coating. The Sikagard treatment provides the greatest degree of fire protection, giving a solution for the automobile sector to provide efficient and safe batteries.

Integration of Passive Fire Protection with Energy-efficient Building Designs is a Growing Trend

There is a global emphasis on constructing buildings that are environmentally friendly and energy-efficient. Passive fire protection solutions, such as fire-resistant materials and compartmentalization systems, can be integrated seamlessly into sustainable designs without compromising energy efficiency. Using fire-resistant materials with high thermal insulation properties can improve a building’s thermal performance reducing the need for heating or cooling and consequently lowering energy consumption.

Many building codes and regulations require adherence to fire safety standards and compliance with energy efficiency requirements. Integrating passive fire protection measures with energy-efficient building designs helps developers and architects meet these dual regulatory demands more effectively. The trend of integrating passive fire protection with energy-efficient building designs underscores the importance of holistic approaches to building safety and sustainability in modern construction practices.

Download Free sample to learn more about this report.

Passive Fire Protection Market Growth Factors

Rising Demand for Development of Fire Safe Infrastructure to Drive Growth

Globally, the demand for better fire safety has been increasing as people become more aware of the problems caused by poor fire safety standards. Numerous people all over the world witnessed the catastrophic event that occurred in August 2020 at the harbor of Beirut, Lebanon’s capital. The aftermath of the disaster revealed that a nearby fire was responsible for triggering the explosion of 2750 tons of ammonium nitrate, which was one of the greatest non-nuclear explosions in human history. This catastrophe, and many more like it, might have been easily prevented if fire safety standards had been better. According to the National Fire Protection Association, about 1.3 million fires occur in the U.S. each year, resulting in an annual loss of close to USD 15 billion.

Today, many governments and industrial organizations recognize the seriousness of the issue. As a result, they are adopting stricter fire safety regulations in an effort to prevent and mitigate losses from such disasters in the future. For example, the Royal Institution of Chartered Surveyors (RICS), which is a professional organization dedicated to promoting and enforcing the highest international standards in land, real estate, construction, and infrastructure appraisal, management, and development, has introduced its revised International Fire Safety Standards Common Principles (IFSS-CP) in October 2020 to meet the evolving demands of the construction industry. Many European countries already have strict regulations and standards in place for fire safety in residential buildings.

Passive fire protection is expected to play a critical part in all of these improved and already existing safety standards and fire safety strategies. This protection is integrated into a building's structure to protect people's lives and mitigate the financial impact due to damaged infrastructure. The materials used to construct the building provide this protection, or it can be added later to improve the building's fire resistance as the construction industry expands in many parts of the world due to increased demand from the residential and commercial sectors. Also, the market is projected to benefit and expand during the forecast period. Rising demand to upgrade fire safety standards for residential and industrial constructions owing to people’s improved purchasing power and standard of living is expected to drive passive fire protection market growth.

Increasing Demand for Fire-safe Data Storage Facilities to Propel Market Growth

Expanding Information Technology (IT), IT-enabled Services (ITES), and telecom industries all over the world have seen a major expansion in recent years and are expected to grow further during the forecast period. These industries are expected to generate significant demand for fire-safe infrastructure owing to the fact that they face a greater degree of fire hazard risk in comparison to conventional office complexes. The cost of recovery from a fire hazard that takes place within such industries can be enormous, not only in terms of human casualties but also the irreversible damage to the infrastructure which is utilized to store massive amounts of data and information.

In the future, major corporations such as Google, Amazon, and Facebook are also likely to invest substantially in creating fire-resistant infrastructure for their data storage operations. For example, Google said in March 2024 that it would invest USD 7 billion in office space and data centers in the U.S. this year, on top of the previous year's USD 10 billion expenditures. Rising heavy investments from IT, ITES, and telecom develop data storage facilities that are fire safe, owing to its relevance in company operations, is expected to drive growth of the market.

RESTRAINING FACTORS

Time-consuming Application of PFP Coatings to Restrict Market Growth

Epoxy passive fire protection coatings are meant to reduce the rate of steel temperature rise, therefore preventing or delaying the collapse of the structure. The oil & gas industry has relied on epoxy PFP coatings that require extra mesh reinforcing. Reinforcement mesh must have been placed appropriately in line with the product's certification to avoid any danger of failure when exposed to spread of fire. Project delays are common with complex mesh reinforced systems. Installation takes a long time and requires a lot of effort. Mesh installation entails following certain certification requirements, such as measuring overlap and installing depth inside the system.

Assuring that the mesh is applied in accordance with the system design presents ongoing challenges, particularly when dealing with complicated structures. Maintenance and repair are time-consuming, costly, and difficult. The oil & gas industry's challenge has been to develop an epoxy PFP that eliminates the need for extra mesh reinforcement in hydrocarbon pool and jet fire situations. Mesh adds inherent hazards connected with improper complicated reinforcement installation. Some passive fire protection coatings are more difficult and time-consuming to apply than other coating types.

Passive Fire Protection Market Segmentation Analysis

By Product Analysis

Cementitious Materials Segment to Dominate the Market owing to its Rising Use in Construction Industry

Based on the product, the market is classified into cementitious materials, intumescent coatings, fireproofing cladding, and others.

The cementitious materials segment held the major passive fire protection market share of 42.15% in 2026 and is expected to maintain its dominance during the forecast period. A cementitious material can be put on steel elements in the construction of a structure to protect them. This material is made up of cement or gypsum, which, when wet, produces a tough, fire-resistant surface. To preserve the underlying material, cementitious sprays are sprayed in numerous layers. It produces a barrier that slows the pace of heat transmission in the case of a fire once it's done. Cementitious material is still one of the most cost-effective options for fireproofing buildings.

Intumescent coatings are expected to expand at a rapid pace during the forecast period. Epoxy intumescent coatings are the most prevalent kind of PFP utilized in modern, high-risk sectors such as oil & gas and petrochemical facilities. Because the oil & gas industry involves operations such as exploration, production, storage, and transportation of extremely flammable liquids and gases, intumescent passive fire protection is an excellent choice for shielding structural steel from the intense heat generated by hydrocarbon fires.

Fireproofing cladding includes boards that are commonly used to defend structures from fire. They're utilized in situations where the protective system is visible and in situations where it's hidden. They provide the specifier a neat, boxed appearance and have the added benefit of being a dry transaction with minimal influence on other activities.

By End-use Industry Analysis

To know how our report can help streamline your business, Speak to Analyst

Oil & Gas Segment Accounted for Major Market Share due to Product Adoption in Structural Steel Protection

By end-use industry, the market segments include oil & gas, infrastructure & construction, industrial, transportation, and others.

Oil & gas industries employ intumescent coatings to safeguard their onshore and offshore steel buildings against fire, which necessitates solutions that can resist temperatures of 1,100°C and more. The Oil & gas segments maqrket with a share of 34.39% in 2026. They are also utilized to protect structural steel against moisture and chemical exposures, as well as fires caused by pools and jets. In the oil and gas sector, PFP coatings are becoming increasingly essential. When exposed to high temperatures, the coatings expand to produce an insulating layer of carbon char on industrial oil and gas facilities. This allows the steel to keep its load-bearing capability for up to four hours longer during a fire, allowing occupants more time to get out of the structure.

- The infrastructure & construction segment is expected to hold a 27.7% share in 2023.

Passive fire protection is an important element of fire safety, which is a key factor in designing a secure structure. The cumulative impact of the different measures that are designed and implemented in a structure is referred to as passive fire prevention. Because fire safety is so important, most countries have enacted legislative laws on fire-safe buildings. This ensures that a complete fire strategy is addressed throughout the construction of a structure, safeguarding people's lives and assisting in the quantification of damages in the event of a fire.

REGIONAL INSIGHTS

North America

North America Passive Fire Protection Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America contributed approximately USD 2.73 billion to the global market in 2025, accounting for 56.50% share, and is expected to reach USD 2.84 billion in 2026, owing to the increasing and driving demand for multifamily housing activities and rising consumer awareness about fire safety. The rising buying power of consumers, as well as the government's and regulatory agencies' increased emphasis on improving the fire safety standard. This factor is expected to boost demand for the market during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

Asia Pacific

The Asia Pacific region captured 9.70% of the global market in 2025, generating USD 0.47 billion in revenue, and is projected to reach USD 0.48 billion in 2026. In Asia Pacific, the growing demand for the product from industries such as construction, industrial, and warehousing, notably in China and India, is expected to drive the market. The rising demand for fire-safe infrastructures, such as commercial and residential buildings, and the surging consumer awareness are projected to fuel demand for the market.

Europe

In 2025, the Europe market stood at USD 1.08 billion, representing 22.30% of global demand, and is projected to grow to USD 1.13 billion in 2026. In Europe, the market is expected to rise as people become more aware of fire safety and the U.K. government implements more legislation, such as the Health and Safety Executive (HSE) business plan. Furthermore, the market is projected to be aided by increased standardization and inspection in industrial facilities, as well as harsh regulatory penalties for failing to comply with the requirements.

- In U. S., the infrastructure & construction segment is estimated to hold a 29.3% market share in 2023.

Middle East & Africa

In 2025, Middle East & Africa generated USD 0.4 billion, contributing 8.20% to global market revenue, and is projected to grow to USD 0.41 billion in 2026. The Middle East & Africa is expected to expand at a steady pace due to increasing government expenditure on port improvements and higher investments in transportation infrastructure. Demand for passive fire prevention solutions is likely to be driven by exploration operations in the region.

Latin America

Latin America recorded a market size of USD 0.16 billion in 2025, capturing 3.30% of the global market share, and is projected to reach USD 0.16 billion in 2026.

KEY INDUSTRY PLAYERS

Strategic Planning Adopted by Companies to Strengthen Their Market Share

To gain a competitive edge, manufacturers are increasingly seeking to distinguish and develop their products. Manufacturers are concentrating on other important product aspects, such as product simplicity of use and product operational life extension. Product portfolio expansions, distribution network expansion, and product development are common strategies used by market players. For example, 3M sells its goods through a variety of distribution channels, including direct to users, wholesalers, retailers, distributors, and dealers in a variety of trades. The key major players in the market are 3M, Akzo Nobel N.V., Bostik, Sika AG, Jotun, and Hempel A/S.

List of Top Passive Fire Protection Companies:

- Akzo Nobel N.V. (Netherlands)

- Bostik (France)

- Sika AG (Switzerland)

- Jotun (Norway)

- 3M (U.S.)

- Hempel A/S (Denmark)

- The Sherwin-Williams Company (U.S.)

- PPG Industries, Inc. (U.S.)

- TÄBY BRANDSKYDDSTEKNIK AB (Sweden)

- CPG EUROPE (England)

- Advanced Insulation Limited (U.K.)

- Polyseam Ltd (U.K.)

- Muehlhan AG (Germany)

- ALTRAD (France)

- Nullifire (U.K.)

- ROCKWOOL International A/S (Denmark)

KEY INDUSTRY DEVELOPMENTS

- December 2023 – Hempel A/S launched an intumescent coating estimation software, HEET Dynamic. The software has been designed to estimate intumescent coating on steel selections and assists engineers and estimators in quick and easy calculations of volume and thickness.

- October 2020 – CharCoat Passive Fire Protection Inc., a company specialized in electrical fire protection and insulation coatings, announced the completion of another successful test for its CharCoat CC Electrical Cable Coating.

- September 2020 – CIN introduced two new fire-resistance products for steel buildings. Long fire resistance periods distinguish C-THERM S110 and C-THERM S111 FD, which safeguard structures for up to 150 minutes. The two new intumescents in CIN's new generation line are solvent-based coatings that, when heated, form a foam with extremely low thermal conductivity, providing exceptional insulating characteristics.

REPORT COVERAGE

The global passive fire protection market research report provides a detailed analysis of the market and focuses on crucial aspects such as leading companies, and products. Also, it offers insights into market trends and highlights vital industry developments. In addition to the factors mentioned above, the report encompasses various factors contributing to the market's growth rate in recent years. It further includes historical data & forecasts revenue growth at global, regional, and country levels, and analyzes the industry's latest market dynamics and growth opportunities.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 5.00% during 2026-2034 |

|

Segmentation |

By Product

|

|

By End-use Industry

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 4.83 billion in 2025 and is expected to reach USD 5.03 billion by 2034.

In 2025, the North American market size stood at USD 2.73 billion.

Registering a CAGR of 5.00%, the market will exhibit steady growth during the forecast period (2026-2034).

The oil & gas segment is the leading end-use industry in the market.

The increasing demand from end-use sectors such as oil & gas, building & construction, and transportation is anticipated to propel the market.

3M, Akzo Nobel N.V., Bostik, Sika AG, Jotun, and Hempel A/S are major players in the global market.

North America dominated the passive fire protection market with a market share of 56.50% in 2025.

The increasing oil & gas company investments in exploration and production, as well as technological developments, are projected to drive the market.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us