Pilot Training Market Size, Share & Industry Analysis, By Aircraft Type (Airplane (Airbus 320 (Flight Training, Simulator Training, Ground Training, Recurrent Training), Boeing 737 (Flight Training, Simulator Training, Ground Training, Recurrent Training), & Others) and Helicopter), By License Type (Commercial, Private, & Airline Transport Pilot License), By Training Program (Commercial Pilot Training Program, & Cadet Pilot Training Program), By Training Mode (Flight Training, Simulator Training, Ground Training, and Recurrent Training), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

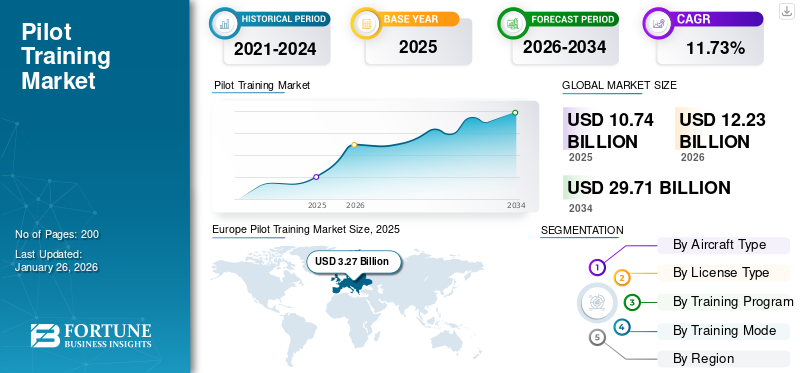

The global pilot training market size was valued at USD 10.74 billion in 2025. The market is projected to grow from USD 12.23 billion in 2026 to USD 29.71 billion by 2034, exhibiting a CAGR of 11.73% during the forecast period. Europe dominated the pilot training market with a market share of 30.41% in 2025.

Pilot training refers to the process of acquiring the necessary knowledge, skills, and experience to operate and control an aircraft safely and efficiently. It is a comprehensive training program that encompasses theoretical instruction, practical flight training, and simulator-based exercises. Flight schools provide various types of training such as ground training, simulator training, flight training, and recurrent training.

Aviation authorities conduct exams for pilots to evaluate their knowledge, skills, and decision-making capabilities. By meeting the necessary flight hour requirements, pilots become eligible to obtain licenses such as Private Pilot License (PPL), Commercial Pilot License (CPL), or Airline Transport Pilot License (ATPL) and other types of licenses. The increasing shortage of pilots is anticipated to drive market growth during the forecast period.

Download Free sample to learn more about this report.

Pilot Training Market Key Takeaways

- 2025 Market Size: USD 10.74 billion

- 2026 Market Size: USD 12.23 billion

- 2034 Forecast Market Size: USD 29.71 billion

- CAGR: 11.73% from 2026–2034

- Europe dominated the market with a 30.41% share in 2025.

- The Airplane segment is projected to account for 89.87% of the market in 2026.

- The Commercial Pilot License (CPL) segment is expected to hold 48.17% of the market in 2026.

Asia Pacific

Asia Pacific recorded USD 3.21 billion in 2025 and is expected to grow to USD 3.75 billion in 2026.

North America

North America reached USD 2.21 billion in 2025 and is projected to grow to USD 2.48 billion in 2026.

Europe

Europe generated USD 3.27 billion in 2025 and is projected to reach USD 3.63 billion in 2026.

U.S.

U.S. market is projected to reach USD 2.07 billion by 2026.

Japan

Japan market is projected to reach USD 0.34 billion by 2026.

Read More

Pilot Training Market Trends

Mixed Reality (MR) Emerges as a Dominant Trend, Garnering Market Attention

Mixed reality combines elements of both Virtual Reality (VR) and Augmented Reality (AR) to create a blended environment that seamlessly integrates digital and physical elements. It augments the pilot's comprehension of the situation by superimposing critical essential data onto their field of vision and furnishes economical training alternatives, thereby diminishing the necessity for actual flight hours, and mitigating hazards. Moreover, the modifiable and versatile attribute of these technologies enable them to accommodate diverse aircraft models and setups. For instance, in November 2022, CAE unveiled its latest innovation in flight training called the CAE 700MXR Flight Simulator.

This cutting-edge simulator is specifically designed for the emerging eVTOL market and promises to transform flight training in intricate urban environments. The CAE 700MXR features a compact mini-motion platform and immersive 360⁰ field of view visuals, providing an incredibly realistic and physics-based simulation experience that caters to single-pilot operations. With its advanced capabilities, this simulator is set to revolutionize the way pilots are trained for complex urban settings. Moreover, pivotal market trends encompass strategic alliances and cooperative ventures, advancements in product offerings, and ongoing innovations.

- Europe witnessed pilot training market growth from USD 2.58 Billion in 2023 to USD 2.92 Billion in 2024.

Download Free sample to learn more about this report.

Pilot Training Market Growth Factors

Emergence of New Airlines across the World Will Catalyze the Market Growth

The growth of new airlines across the globe is driving the growth of the market. The civil aviation industry is experiencing the emergence of several new airlines, particularly in emerging markets and regions with growing economic activity. For instance, in March 2023, Saudi Arabia revealed its plan to establish a new national airline called Riyadh Air, with the objective of transforming the city of Riyadh into a prominent global aviation hub, competing against other major regional players such as Dubai and Doha. Riyadh Air has set a target to commence operations to over 100 international destinations by 2030.

As more and more airlines emerge, there is an increasing need for pilots to manage their flight operations. The establishment of new airlines is coupled with increased air travel demand, expanding tourism sectors, and favorable government policies promoting aviation. As economies grow and disposable incomes increase, more people are opting for air transportation for business and leisure purposes. This has created a need for additional airline services which leads to the establishment of new carriers to meet the growing demand.

Pilot Shortage Propels Aviation Market Growth Prospects

A prevalent challenge encountered by numerous airlines and aviation enterprises globally is scarcity of pilots in the industry. The insufficiency is primarily due to the aging and subsequent retirement of a substantial number of pilots, coupled with inadequate recruitment initiatives annually. For instance, in June 2022, a report issued by the Regional Airline Association, a business association based in the U.S. representing seventeen regional airlines across North America, highlighted that the escalating dearth of pilots poses a significant jeopardy to the viability air services within small communities.

The report also highlighted that nearly half of the existing pool of qualified pilots are approaching the obligatory retirement age thus posing a substantial menace to the aviation sectors sustainability. Different groups such as airlines, government authorities, and aviation training organizations are taking action to tackle the shortage of pilots and avoid the collapse of air services in small communities. They are implementing plans to attract and train new pilots, enhancing strategies to keep existing pilots, and working together with educational institutions to create thorough training programs.

RESTRAINING FACTORS

Complex Regulatory Environments and High Training Costs May Impede Industry Growth

The complex regulatory environments in different countries and regions around the world create obstacles for flight training organizations. Aviation authorities impose strict regulations and certification requirements to ensure safety and standardization in flight training. Additionally, high training costs also act as a restraint for the industry. The expenses associated with training, including aircraft rental, fuel, instructor fees, simulator sessions, and licensing fees, can be significant.

These costs make training a considerable investment for individuals and can limit access to training programs for those who cannot afford it. For instance, according to the International Civil Aviation Organization (ICAO), the cost of obtaining a commercial pilot license can range from USD 70,000 to 150,000 depending on the location and training program. This financial burden can deter potential candidates from pursuing a career in aviation.

Pilot Training Market Segmentation Analysis

By Aircraft Type Analysis

Airplane Segment Dominates due to Increasing Demand of Pilots from Airlines Owing to Fleet Expansion

By aircraft type, The Airplane segment is projected to dominate the market with a share of 89.87% in 2026 and the market is segmented into airplane and helicopter. Airplane segment refers to flight training specific to aircraft of the fixed wing category. This segment includes training for different airplane models such as Airbus A320, Boeing 737, and others.

The helicopter segment focuses on flight training for rotary wing aircraft. It covers specific skills and knowledge required for piloting helicopters, which include flight training, simulator training, ground training, and recurrent training. The advancement and modernization of helicopters is estimated to enhance the pilot training market growth.

By License Type Analysis

Massive Retirement of Pilots in Forecast Period to Bolster Commercial Pilot License

By license type, The Commercial Pilot License segment is projected to dominate the market with a share of 48.17% in 2026 and the market is divided into Commercial Pilot License (CPL), Private Pilot License (PPL), Airline Transport Pilot License (ATPL), and others. CPL refers to the training programs and requirements for obtaining a commercial pilot license. This license allows pilots to operate aircraft for commercial purposes, such as flying for airlines or conducting charter flights. This segment leads the market and is projected to register fastest growth due to the increasing commercial air travel.

ATPL refers to training programs tailored for pilots who are aiming to obtain an airline transport pilot license. This license is the highest level of pilot certification and allows pilots to operate as captains or first officers in commercial airlines. Due to growing demand for passenger and cargo transport the segmented is projected to grow during the projected period.

By Training Mode Analysis

Flight Training Segment Leads Due to Stringent Regulations to Complete Mandatory Flight Hours

By training mode, The Flight Training segment is projected to dominate the market with a share of 44.22% in 2026 and the market is segmented into flight training, simulator training, ground training, and recurrent training. Flight training includes hands-on experience in operating an aircraft. Pilots learn maneuvers, takeoffs, landings, navigation, communication, and emergency procedures under the guidance of certified instructors. This segment dominates the market in the base year due to stringent regulations to complete the mandatory flight hours.

- The ground training segment is expected to hold a 15% share in 2024.

Recurrent training refers to a regularly scheduled training program that is required to maintain pilot proficiency and helps pilots to refresh their type-specific knowledge, ensuring that they keep their qualifications up-to-date and handle the aircraft they are licensed on with maintaining the safety standards. This segment is expected to be the fastest growing segment due to the rising demand of skilled pilots globally.

To know how our report can help streamline your business, Speak to Analyst

Owing to Increased Demand for Commercial Pilots all Around the Globe, Commercial Pilot Training Program Dominates the Market

By training program,The Commercial Pilot Training Program segment is projected to dominate the market with a share of 53.20% in 2026 and the market is trifurcated into commercial pilot training program, cadet pilot training program, and others. Commercial pilot training program is a special educational program designed to provide pilots with the necessary knowledge to obtain a commercial pilot license. This segment is the dominating and is expected to register significant growth due to the increasing demand for commercial pilots.

The others segment refers to training programs that are necessary for actively recruited pilots to improve and enhance their skills. This segment is estimated to be the fastest growing during forecast due to growing demand for rising demand for skilled pilots.

REGIONAL ANALYSIS

Regionally, the market is segmented into Asia Pacific, Europe, North America, the Middle East, and the Rest of the World.

Europe

Europe Pilot Training Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Europe market accounted for USD 3.27 billion in 2025, representing 30.41% of the global industry, and is expected to reach USD 3.63 billion in 2026. This growth is attributed to expansion of commercial airlines and the launch of new routes and destinations. For instance, in October 2022, the European Union (EU) and the Association of Southeast Asian Nations (ASEAN) entered into a new open skies agreement, aiming to enhance and expand airline connections between the two regions. This agreement stands out as it encompasses not just two countries but rather two blocs of countries, with the EU consisting of 27 members and ASEAN consisting of 10 members. The UK market is projected to reach USD 0.76 billion by 2026, and the Germany market is projected to reach USD 0.36 billion by 2026.

Asia Pacific

Asia Pacific recorded a market size of USD 3.21 billion in 2025, capturing 29.84% of the global market share, and is projected to reach USD 3.75 billion in 2026. The region’s growth is owed to its increasing air traffic and expansion of airline fleets to meet increasing passenger demand. For instance, February 2023, Air India and Boeing have jointly announced a significant agreement, wherein the airline, owned by the Tata Group, will acquire a total of 220 aircraft from Boeing. The order comprises 190 B737 MAX, 20 B787, and 10 B777X aircraft, with a combined value of USD 34 billion at the list price. The Japan market is projected to reach USD 0.34 billion by 2026, the China market is projected to reach USD 0.61 billion by 2026, and the India market is projected to reach USD 0.54 billion by 2026.

North America

In 2025, North America generated USD 2.21 billion, contributing 20.53% to global market revenue, and is projected to grow to USD 2.48 billion in 2026. The growth in this region is owed to rising demand for pilot in the aviation industry due to increasing retirement. Furthermore, multi pilot license, economical training, focus on security and threat mitigation are the other factors that contributed to the growth in the U.S. The U.S. market is projected to reach USD 2.07 billion by 2026.

Rest of the World

The Rest of the World market was valued at USD 0.63 billion in 2025, capturing 5.83% of global revenue, and is estimated to reach USD 0.71 billion in 2026. The Middle East market is expected to grow significantly during the forecast period. The Middle East & Africa market generated USD 1.44 billion in 2025, representing 13.39% of the global market landscape, and is expected to reach USD 1.67 billion in 2026. The growth is attributed to the increase in air traffic due to tourism. Furthermore, increasing orders for new aircraft also catalyzes the market growth. The rest of the world is expected to observe steady market growth throughout the projected duration. This Latin America and Africa aviation industry is expected to boost the market’s growth.

KEY INDUSTRY PLAYERS

Aviation Industry Leaders Prioritize M&A, Emerging Markets, UAV Training, and Innovation

The global market is highly fragmented with key players such as CAE Inc., BAA Training, ATP Flight School, FlightSafety International Inc., Lufthansa Aviation Training GmbH, and others. Prominent entities prioritize emerging markets, mergers & acquisitions, technological progress, UAV simulators and product innovation as focal strategies to augment their market presence. For instance, in August 2022, a 15-year partnership agreement was signed between CAE and the Qantas Group to establish and manage a brand-new flight training center in Sydney, Australia. The CAE Sydney Training Centre, spanning over 7,000 square meters, is scheduled to commence operations in early 2024. As part of the agreement, CAE will introduce a state-of-the-art A320 full flight simulator and acquire the Qantas Group's B787, A330, and B737NG full-flight simulators, along with their corresponding integrated procedures trainers, to be utilized at the new facility.

List of Top Pilot Training Companies:

- CAE Inc. (Canada)

- BAA Training (Lithuania)

- ATP Flight School (U.S.)

- FlightSafety International Inc. (U.S.)

- Lufthansa Aviation Training GmbH (Germany)

- L3Harris Technologies Inc. (U.S.)

- Pan AM Flight Academy (U.S.)

- Airbus Flight Academy (U.S.)

- Thrust Flight (U.S.)

- Indra Sistemas S.A. (Spain)

KEY INDUSTRY DEVELOPMENTS:

- March 2023 - Airways Aviation, a UAE-based flight training provider collaborated with Asia Pacific Flight Training Academy Limited (APFT), which is headquartered in India to provide prospective Indian students and airline cadets access to an innovative pilot pathway program.

- February 2023 - Gen24 Flybiz, an India-based emerging flight training company, has signed a contract with Avion for the procurement of eight Airbus A320 aircraft simulators after the acquisition of Avion Group and Avion Simulators. The establishment of their new training center with two Avion A320 simulators set to be transported to India and certified by the Indian civil aviation authority, DGCA.

- February 2023 - L3Harris Technologies got selected by All Nippon Airways Co. Ltd., Japan’s largest airlines to train its next generation pilots. The first batch is set to begin in March 2023, and will be trained on various single and multi-engine aircraft.

- February 2023 - RMIT- Royal Melbourne Institute of Technology, in Australia launched their RMIT Aviation academy with a fleet of about 24 aircraft to support growing demand for flight training and global aviation workforce training. RMIT University has been training aerospace engineers and pilots for over 80 years across flight training sites at regional Victoria (Bendigo) and Point Cook.

- July 2022 - Embry Riddle Aeronautical University (ERAU) introduced Virtual Reality (VR) in its flight training program, resulting in a 30% reduction in training time. The VR allows the students to practice with less or no anxiety and confidence, decreasing the distraction encountered in flight training's initial stage.

REPORT COVERAGE

The market research report provides a detailed market analysis. It comprises all major aspects such as R&D capabilities and optimization of the operating services. Moreover, the report offers insights into market forecast, market trends, regional analysis, porter’s five forces analysis, competitive landscape of various companies profiled with market competition, and primarily highlights key industry developments. In addition to the above-mentioned factors, it mainly focuses on several factors that have contributed to the global market growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.73% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Aircraft Type

|

|

By License Type

|

|

|

By Training Program

|

|

|

By Training Mode

|

|

|

By Geography

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 10.74 billion in 2025.

The market is likely to grow at a CAGR of 11.73% over the forecast period (2026-2034).

The flight training segment is expected to lead the market due to rising demand for high skilled pilots from the aviation industry.

The market size in Europe stood at USD 3.27 billion in 2025.

Emergence of new airlines globally and shortage of pilots in aviation industry are expected to drive the market.

Some of the top players in the market are CAE Inc., BAA Training, ATP Flight School, FlightSafety International Inc., Lufthansa Aviation Training GmbH, and others.

The U.S. dominated the market in 2025.

Complex regulatory environments and high training costs are expected to hamper the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us