Ventilators Market Size, Share & Covid-19 Impact Analysis, By Type (Adult, and Paediatric & Neonatal), By Interface (Invasive, and Non-invasive), By End User (Hospitals, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Ventilators Market Overview

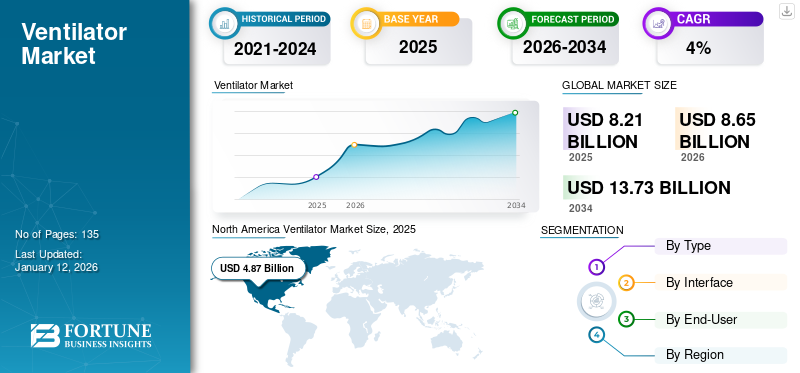

The global ventilators market size was valued at USD 8.21 billion in 2025. The market is projected to grow from USD 8.65 billion in 2026 to USD 13.73 billion by 2034, exhibiting a CAGR of 5.94% during the forecast period (2026-2034). North America dominated the ventilators market with a market share of 59.38% in 2025.

According to the Society of Critical Care Medicine, more than 5 million patients are admitted to the ICU each year in the United States. An estimated 40.0%- 50.0% of these ICU admissions require mechanical ventilation. The Rising number of ICU admissions, due to the prevalence of chronic respiratory diseases, is leading to an increase in demand for critical care equipment such as incubators, patient monitoring systems, and others.

A ventilator is a machine that provides mechanical or artificial ventilation to a patient who is unable to breathe or can breathe partially. There are various modes of ventilation, however, ventilation is primarily termed as invasive, and non-invasive. Non-invasive ventilation modes offer distinct features, however severe and emergency conditions often demand invasive ventilation, owing to clinically proven benefits over non-invasive ventilation. Key market players are investing heavily in R&D with an aim to develop and introduce technologically advanced critical care equipment. For instance, in November 2019, Nihon Kohden launched the NKV-550 Series System, offering a full suite of applications necessary in a critical care setting for neonates and adults.

Global Ventilators Market Overview

Market Size:

- 2025: USD 8.21 billion

- 2026: USD 8.65 billion

- 2034: USD 13.73 billion

- CAGR: 5.94% (2026–2034)

Regional Dominance:

- North America led in 2025 with a 59.38% market share

Key Growth Drivers:

- Increasing prevalence of respiratory diseases, including COVID-19

- Advancements in ventilator technology

- Rising geriatric population susceptible to respiratory ailments

- Growing demand for homecare ventilators

- Government investments in healthcare infrastructure

Trends:

- Shift towards non-invasive ventilation modes

- Integration of AI and improved connectivity in ventilators

- Development of portable and home-use ventilators

Challenges/Restraints:

- Complications associated with ventilator use, such as ventilator-associated pneumonia

- High costs and maintenance of advanced ventilator systems

- Stringent regulatory approvals and compliance requirements

Segment Insights:

- Type: Adult ventilators dominate; pediatric & neonatal segments are growing

- Interface: Invasive ventilators held a dominant share in 2019

- End-User: Hospitals are the primary consumers; specialty clinics are growing

Ventilators Management Amid the COVID-19 Pandemic

With the outbreak of COVID-19, there is an increased demand for advanced medical devices such as critical care equipment to treat infected patients. Intensive care unit equipment, such as patient monitors, incubators, etc., is experiencing an increase in demand from countries worldwide, and is focusing on catering to the unmet needs during the global pandemic. Koninklijke Philips N.V., a leading medical device manufacturer, registered a significant increase in order intake in Q1 2020, for its sleep and respiratory care devices offerings which were primarily driven by the rise in demand for ventilators. Additionally, the rising prevalence of COVID-19, has led to a significant increase in the number of ICU admissions globally, subsequently increasing the need for critical care equipment. According to the World Health Organization (WHO), as of May 18, 2020, around 4.7 million patients are suffering from COVID-19 globally. According to another report published by Imperial College London, an estimated 30.0% of hospitalized patients suffering from COVID-19 are at a higher probability of requiring mechanical ventilation.

Currently, there is a massive gap between the availability of ventilators and its demand in various nations worldwide. The global pandemic has exposed the frailties of healthcare systems worldwide, and the sudden increase in ICU admissions has once again highlighted the lack of healthcare resources, including medical professionals and critical care equipment, in various countries. According to the article published by NCBI, currently, there are an estimated 62,000 fully-featured mechanical ventilators installed in the U.S.

This is supported by a Strategic National Stockpile (SNS), and around 98,000 non-full-featured ventilators in the country. This takes the total tally of devices capable of providing ventilation to around 200,000 in the U.S. However, according to the various statistics if the COVID-19 virus continues to spread as projected in the U.S., in 2020, around 4.8 million patients would require hospitalization. Additionally, 1.9 million COVID-19 patients would require ICU admissions, and 960,000 would progressively require mechanical ventilation in the U.S. These numbers of patients would be highly challenging for the country to manage, given the substantially lower number of available devices. This has further led to the rising demand for home care restorative devices such as ventilators and others.

The rising prevalence of COVID-19 globally has visibly exposed the lack of various critical care equipment in hospitals and other healthcare settings. This has led the government authorities to scramble and prepare contingency plans to increase the number of available devices per 100,000 people. This has subsequently led to a rapid growth in demand in 2020.

Ventilators Market Trends

Download Free sample to learn more about this report.

Market Players Focusing on Ramping up Production citing the Supply-Demand Gap

The current demand for critical care equipment is very high due to the rising number of patients requiring urgent care. The existing healthcare infrastructure present worldwide is unable to meet the increasing demands and hence require upgrading. Most of the healthcare facilities are focusing on improving the healthcare infrastructure and are investing massively on the same. Majority of the key market players are focusing on expanding their current production capacities, realizing the exponential demand for these devices due to the outbreak of the COVID-19 pandemic.

For instance, in March 2020, Medtronic, a leading medical device manufacturer, increased its production by 40.0%. Also, in March 2020, Koninklijke Philips N.V., targeted to increase its production capacity by 4 times, to meet the rising demand. Getinge AB launched a second ramp-up to its production capacity from 10,000 in 2019 to 26,000 ventilators in 2020, an increase in size by 160.0% compared to 2019. Significant demand for new devices from various countries is projected to aid in the expansion of the market during 2025-2032.

DRIVING FACTORS

Increasing Number of ICU Admissions is Augmenting Demand for Critical Care Equipment

The burden of respiratory diseases is rising globally, owing to numerous factors such as smoking, obesity, and lifestyle changes. According to the Regents of the University of California, in the United States, approximately 4 million ICU admissions are registered each year. In Germany, around 2.1 million patients are admitted in ICU each year, out of which an estimated 42.0% patients require mechanical ventilation.

The increasing demand for critical care equipment, due to the increasing number of ICU admissions in emerging and developed countries, is one of the major factors anticipated to drive the growth of the market. Additionally, the impact of COVID-19, the number of ICU admissions had an additional impact and the need of critical care equipment. According to the Centers for Disease Control and Prevention, as of March 2020, 53.0% of the total COVID-19 cases reported, were admitted in the ICU. The rise in the number of ICU admissions due to COVID-19 is another major factor driving the market.

Introduction of Technologically Advanced Products to Drive the Ventilators Market

Robust research and development on cardiovascular interventions and the introduction of novel devices will boost the market during the forecast period of 2025-2032. Key market players are investing in developing cheaper and new mechanical ventilators. For instance, in May 2020, NASA received an emergency approval from the U.S. Food and Drug Administration (FDA), for the VITAL system for the treatment of patients suffering from COVID-19.

Additionally, in January 2020, Drägerwerk AG launched new ICU ventilators named new Evita V600 and V800. This new product launch will help to support daily clinical tasks in the ICU thereby, spurring the industry growth. In August 2017, Hamilton Medical launched HAMILTON-C6 new generation of high-end ventilators. Introduction of technologically advanced devices by key market players is increasing the demand, thereby promoting growth.

RESTRAINING FACTORS

Complications Associated with Ventilator will Challenge Growth

Despite the rising ICU admissions and increasing demand for critical care equipment, certain factors are challenging this market. They cause complications such as bronchopleural fistula, pneumothorax and nosocomial pneumonia and similar complications that result in a decrease in cardiac output, gastric problems and renal impairment, or alkalosis. According to a study published by the American Society of Microbiology, 80.0% of nosocomial pneumonias are associated with mechanical ventilation and are termed ventilator-associated pneumonia (VAP). Around 250,000 and 300,000 such cases are reported each year in the United States. This is one of the major factors causing hindrance to the growth of the market.

SEGMENTATION

By Type Analysis

To know how our report can help streamline your business, Speak to Analyst

Adult Segment to Grow at Faster Pace during Forecast Period

Based on indication, the market is segmented into adult and pediatric & neonatal. In the U.K., the number of ICU admission is increasing by 2.5% annually. Higher demand for ventilation support in the elderly population being admitted to the ICU, is one of the major factors driving the growth of the adult segment. Moreover, the increasing number of preterm births is propelling the demand for the pediatric ventilators and will help this segment grow at a significant CAGR. The adult segment led the market accounting for 61.01% market share in 2026.

By Interface Analysis

Invasive Segment Held Dominant Share in 2024

Based on interface, the ventilators market is segmented into invasive and non-invasive. The invasive segment held dominating share of 88.84% in 2026. The dominance is attributable to the increase in the demand from ICU’s due to the increasing number of patients admitted to the ICU department. In the U.S., around 5 million patients are admitted to ICU each year out which around 45.0% require mechanical ventilation.

The demand for invasive ventilators owing to clinical and operational benefits offered over non-invasive devices, is further fuelled by the current pandemic. There has been a surge in the number of patients suffering from covid-19, being admitted to the ICU and requiring mechanical ventilation. (This addition of the statement above was simple.) For instance, according to an article published by The Lancet in February 2020, out of 710 COVID-19 patients in Wuhan China, 52 patients were admitted to the intensive care unit.

By End User Analysis

Higher Adoption by Hospitals has led to the Dominance of the Segment in 2024

An increasing number of ICU admissions in hospitals is one of the major elements leading to the rise in demand. Increasing prevalence of respiratory diseases and COVID-19 is also one of the additional factors anticipated to propel the growth of the hospital segments with a share of 56.29% in 2026 . Additionally, the rising number of hospitals in the emerging countries is likely to increase the demand for the ICU equipment, hence driving the segmental growth. For instance, in September 2019, Aster DM Healthcare, a medical service provider in India and the GCC, announced its plans to open two new hospitals in Bengaluru, India.

The Specialty Clinics segment is anticipated to grow at a significant CAGR during the forecast period due to the rising number of well-equipped specialty clinics in developed and developing countries. An influx of private players in the hospitals and healthcare industry in various countries has changed the face of specialty clinics. These clinics have diversified their service offerings and are more focused on offering critical care and emergency services as well. This has led to a gradual rise in demand from these settings.

REGIONAL INSIGHTS

North America Ventilator Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The ventilators market size in North America stood at USD 4.87 billion in 2025 and is expected to hold a major ventilators market share due to the increasing number of patients admitted to the ICU each year. For instance, according to the Society of Critical Care Medicine, around 5 million patients are admitted to the ICU each year in the U.S. Also, the country has among the highest number of critical care beds per capita, at around 34.7 per 100,000 population. According to the United States Department of Health & Human Services (HHS), there are only 20.5 ICU beds per 100,000 population, equipped with a ventilator. The U.S. market is projected to reach USD 4.74 billion by 2026.

Additionally, the rising prevalence of COVID-19 in the U.S. has led to an increase in the number of patients admitted to the ICU and the number of patients requiring mechanical ventilation. The increasing number of ICU admissions is anticipated to drive the demand for critical care equipment, including these, and hence, the growth of the market in the region.

Europe

Europe is anticipated to account for the second-highest share in the market due to increasing ICU admissions in the region. For instance, in U.K and Germany, out of the total hospital admissions in these countries, statistics revealed that 6.7% and 9.0% of patients were admitted in the ICU department in 2018. Statistics also suggested that, out of the total ICU admissions in the U.K., around 67.0% of admissions required ventilation. The increasing rate of ICU admissions in Europe and the need for mechanical ventilation support are some of the major factors anticipated to increase the demand for these devices in the region. The UK market is projected to reach USD 0.1 billion by 2026, while the Germany market is projected to reach USD 0.53 billion by 2026.

Asia Pacific

For instance, the annual growth rate of ICU admissions in Europe is 5.0%- 6.0%. Asia Pacific is expected to grow at a significant CAGR during the forecast period.

Increasing number of ICU admissions coupled with patients requiring respiratory support, especially in India and China, are some of the major factors anticipated to drive the market growth in the Asia Pacific. The Japan market is projected to reach USD 0.32 billion by 2026, the China market is projected to reach USD 0.51 billion by 2026, and the India market is projected to reach USD 0.29 billion by 2026. The current outbreak of COVID-19 has led local manufacturers and new startups to develop devices at a low cost. In addition, governments' initiatives to boost the production and non-healthcare sector companies are collaborating with healthcare companies to expand the production of these ventilators are among the additional factors boosting the market growth in Asia Pacific.

Latin America, and Middle East & Africa is anticipated to grow at a slower pace during the forecast period.

KEY INDUSTRY PLAYERS

Strong Portfolio of Koninklijke Philips N.V., Hamilton Medical AG, Getinge AB, and Medtronic has propelled these players to a Leading Market Position

Some of the major companies operating in the ventilators market are Koninklijke Philips N.V., Hamilton Medical AG, Getinge AB, and Medtronic. These players accounted for a dominant share of this market in 2019. These companies strongly focus on the development of novel technologically advanced devices. Other key strategies adopted by players in this market include mergers and acquisitions, partnerships, collaborations, and geographical expansions.

Additionally, key market players operating in the market are scaling up production. For instance, Getinge AB, a manufacturer of advanced ventilators for intensive care units, has announced a ramp-up of 160% in the production capacity and a rise from 10,000 in 2019 to 26,000 by the end of 2020.

Other key players include Vyaire Medical, Inc., Becton Dickinson and Company, Drägerwerk AG & Co. KGaA, GE Healthcare, Shenzhen Mindray Bio-Medical Electronics Co., Ltd. and others.

LIST OF KEY COMPANIES PROFILED:

- Koninklijke Philips N.V. (Amsterdam, Netherlands)

- Hamilton Medical AG (Bonaduz , Switzerland)

- Getinge AB (Gothenburg, Sweden)

- Medtronic (Dublin, Ireland)

- Vyaire Medical, Inc. (Illinois, United States)

- Drägerwerk AG & Co. KGaA (Lübeck, Germany)

- GE Healthcare (Illinois, United States)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (Shenzhen, China)

- Others

KEY INDUSTRY DEVELOPMENTS:

- In May 2021, VYAIRE MEDICAL, INC., donated Five Vela ventilators, two CPAP/BIPAP and oxygen concentrators, 100 bellavista ventilators, 500 oxygen concentrators in India with a view to support India in this covid-19 pandemic as well as to strengthen its brand position as a leading brand in India.

- In April 2021, Getinge AB announced the U.S. FDA approval for a number of software for Servo–u and Servo-n ventilators. Also, the company received the U.S. marketing approval of Servo-u MR from U.S. FDA. This helped the company to broaden product line and strengthen its brand name.

- In June 2020, Medtronic announced partnership with Foxconn Industrial Internet, a part of Foxconn Technology Group to initiate the manufacturing Medtronic Puritan Bennett 560 ventilators with a view to cater the increasing demand of ventilators in the covid-19 pandemic.

- In April 2020, Koninklijke Philips N.V., increased its production capacity of hospital ventilators with a view to cater the increasing demand of hospital ventilators during covid pandemic.

- In April 2020, NIHON KOHDEN CORPORATION received the production and marketing approval for NKV-550 series ventilator in Japan to cater the increasing demand for ventilators in Japan market.

- In April 2020, ResMed announced the expansion of AirView, a cloud-based platform for monitoring and managing respiratory care patients in India, to remotely monitor patients.

REPORT COVERAGE

This ventilators market report provides a detailed analysis and focuses on key aspects such as leading companies, types, interface and end-users. Besides this, the market research report offers insights into the market, current trends, and the impact of COVID-19 on respiratory disorders, and highlights the key industry developments. Furthermore, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Type

|

|

By Interface

|

|

|

By End-User

|

|

|

By Geography

|

Frequently Asked Questions

According to Fortune Business Insights, the global ventilator market size was valued at USD 8.65 billion in 2026 and is projected to reach USD 13.73 billion by 2034, growing at a CAGR of 5.94% during the forecast period.

Latest trends include the integration of AI and IoT for smart ventilators, portable and home-care ventilators gaining popularity, and rising adoption of non-invasive ventilation technologies to improve patient comfort and outcomes.

Growing at a CAGR of 5.94%, the market will exhibit steady growth in the forecast period (2026-2034).

The market is segmented into invasive and non-invasive ventilators, with invasive ventilators holding a larger share due to their widespread use in critical care settings.

Key drivers include the rising prevalence of chronic respiratory diseases, the COVID-19 pandemic aftermath increasing demand, technological innovations, and a growing geriatric population requiring respiratory support.

Key players dominating the ventilator market include Medtronic, Philips Healthcare, Drägerwerk AG & Co. KGaA, GE Healthcare, and Hamilton Medical AG, leveraging innovative product launches and strategic partnerships to maintain market leadership.

North America dominated the ventilators market with a market share of 59.38% in 2025.

Future advancements focus on AI-enabled predictive analytics, wireless connectivity, miniaturization, and personalized ventilation settings to enhance patient care and reduce hospital stays.

Market challenges include high cost of advanced ventilators, lack of skilled healthcare professionals to operate complex devices, and regulatory hurdles in some regions.

- 2021-2034

- 2025

- 2021-2024

- 135

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us