Organic Acid Market Size, Share & Industry Analysis, By Type (Acetic Acid, Citric Acid, Lactic Acid and Others), By Application (Industrial, Food & Beverage, Pharmaceutical and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

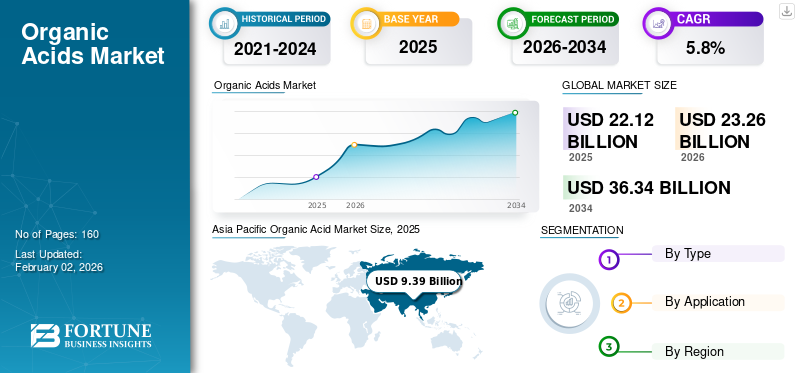

The global organic acid market size was valued at USD 22.12 billion in 2025. The market is projected to grow from USD 23.26 billion in 2026 to USD 36.34 billion by 2034, exhibiting a CAGR of 5.8% during the forecast period. Asia Pacific dominated the global market with a market share of 42.45% in 2025.

Organic acids are carbon-based acids (typically carboxylic acids) that function as acidulants, preservatives, chelating agents, pH regulators and platform chemicals across food and beverages, animal nutrition, pharmaceuticals, personal care and industrial applications. Commercial production is split between fermentation routes (e.g., citric acid, lactic acid, gluconic acid) and petrochemical synthesis routes (e.g., acetic acid), depending on the specific molecule and required end-use purity. The market includes commodity-volume acids (used primarily as ingredients and process aids) as well as higher-value, high-purity grades serving pharma, nutraceutical and specialty industrial segments.

The market growth is driven by rising consumption of processed foods and beverages, increasing adoption of feed acidifiers and preservatives in animal production and a broad shift toward bio-based intermediates for low-carbon materials and chemicals. In parallel, regulatory tightening on emissions and indoor air quality, as well as brand commitments to sustainability, are influencing both product choice and supplier qualification, prompting producers to adopt cleaner production methods, utilize renewable feedstocks and establish traceable supply chains.

Furthermore, the market is comprised of several major players including Celanese Corporation, BASF SE, LyondellBasell Industries, Cargill, Incorporated and Corbion N.V. A broad portfolio, innovative product launches and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

Organic Acid Market Key Takeaways

- 2025 Market Size: USD 22.12 billion

- 2026 Market Size: USD 23.26 billion

- 2034 Forecast Market Size: USD 36.34 billion

- CAGR: 5.8% from 2026–2034

- Asia Pacific dominated the organic acid market with a 42.45% share in 2025.

- The acetic acid segment held the largest market share, accounting for 68.2% in 2025.

- The industrial segment accounted for the leading application share, holding 36.9% of the market in 2025.

Asia Pacific

Asia Pacific led the market in 2025 with a value of USD 9.39 billion and a 42.45% market share.

North America

North America is projected to reach USD 3.95 billion in 2026, supported by strong food, beverage, and industrial demand.

Europe

Europe is expected to reach USD 5.37 billion in 2026, growing at a CAGR of 5.8% during the forecast period.

U.S.

The organic acid market was valued at USD 3.30 billion in 2025, driven by food processing and industrial applications.

Japan

Demand is supported by the country's established food processing industry and growing preference for sustainable bio-based materials.

Read More

ORGANIC ACID MARKET TRENDS

Bio-Based Fermentation Scale-Up and Low-Carbon Production Pathways are Significant Market Trends

Bio-based fermentation is gaining traction as producers and downstream users prioritize renewable inputs, supply security and lower lifecycle emissions. In the food and beverage industry manufacturers are increasingly specifying fermentation-derived acidulants and preservatives that aligns with clean-label claims and meet the requirements for traceability. In parallel, the demand for lactic acid is supported by the growth of Polylactic Acid (PLA) and other bio-based materials. In contrast, citric acid continues to experience a steady demand from beverages, confectionery and household and personal care formulations. On the petrochemical side, acetic acid producers are investing in process efficiency and reducing carbon intensity to maintain competitiveness as customers’ demand lower-carbon molecules.

- For example, integrated PLA projects that include lactic acid fermentation capacity are being developed to strengthen backward integration and improve supply reliability for biopolymer value chains.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Food and Beverage Acidulants and Shelf-Life Solutions Drives the Market Growth

Organic acids, such as citric, lactic, acetic and malic acids, are widely used to control pH, enhance flavor balance and improve microbiological stability in beverages, dairy products, confectionery, sauces, and processed foods. As the penetration of packaged food and modern retail expands, brand owners are increasingly optimizing formulations for consistent sensory performance and longer distribution cycles, thereby supporting steady demand for food-grade acidulants and preservatives. At the same time, clean-label positioning is reinforcing the shift toward recognizable ingredients and fermentation-derived acids that can replace or reduce certain synthetic additives. These factors collectively contribute to the organic acid market growth.

- For instance, beverage formulators routinely combine citric acid with citrate salts to stabilize acidity while improving taste and buffering performance in carbonated and still drinks.

MARKET RESTRAINTS

Volatility in Feedstock and Energy Costs can Compress Margins and Restrict Market Expansion

A significant portion of organic acid production relies on agricultural feedstocks (e.g., corn, sugar, molasses) and energy-intensive downstream processing. As a result, producers face exposure to crop-price swings, weather-driven supply disruptions, logistics costs and energy price volatility. These factors can lead to rapid changes in conversion economics, particularly for commodity-grade acids sold under contract structures that lag behind spot raw material movements. For petrochemical routes, acetic acid economics are sensitive to methanol and energy pricing, while compliance and maintenance costs can rise as plants invest in emissions controls and reliability.

- For example, sharp movements in corn or sugar prices can raise fermentation input costs, leading to price increases for citric and lactic acid and tighter availability for downstream formulators.

MARKET OPPORTUNITIES

Premiumization into High-Purity and Specialized Grades to Create Lucrative Growth Opportunities

Tightening quality requirements in pharmaceuticals, nutraceuticals, medical nutrition and high-performance industrial applications is encouraging demand for higher-purity organic acids and tailored derivatives (e.g., controlled impurity profiles, low heavy metal content, and application-specific salt forms). Producers that can offer validated quality systems, documentation support, and consistent global supply can capture pricing premiums and longer-term contracts. In addition, sustainability goals are accelerating the adoption of bio-based and low-carbon grades, creating differentiation opportunities beyond commodity price competition.

- For example, pharma and nutraceutical customers increasingly require documented traceability and tighter impurity controls for citric acid and lactate salts used as excipients and buffering agents.

MARKET CHALLENGES

Substitution and Intense Price Competition in Commodity Grades to Hamper Market Growth

In several end uses, organic acids compete with inorganic acids, alternative preservatives and functional additives that can deliver similar performance at lower cost or with easier formulation handling. Commodity-grade segments also face persistent price pressure from capacity expansions, export flows and aggressive competition among large-scale producers. This can narrow margins and delay returns on new fermentation or acetyl-chain investments, particularly when demand growth slows or end-use sectors experience cyclical downs.

- For instance, in some industrial cleaning and descaling applications, inorganic acids may displace organic acids when customers prioritize upfront cost over biodegradability and handling benefits.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Acetic Acid Segment Leads Market Due to Growing Consumption of Flexible Packaging

Based on type, the market is segmented into acetic acid, citric acid, lactic acid and others.

The acetic acid segment accounted for the largest organic acid market share in 2025. The segment's growth is driven by expanding consumption of flexible packaging, water-based paints, and engineered wood adhesives, where VAM derivatives are widely used. In many regions, capacity additions and process efficiency upgrades also improve supply reliability and cost competitiveness, reinforcing adoption across large-volume industrial value chains. Furthermore, the segment is set to hold a 68.2% share in 2025.

The growth of the citric acid segment is driven by its multifunctionality as an acidulant, chelating agent, preservative, and flavor enhancer, making it a staple in beverages, processed foods and household/personal care formulations. Demand is strengthening as manufacturers prioritize “clean-label” ingredients and replace some synthetic additives with naturally derived alternatives. Citric Acid is projected to grow at a CAGR of 5.6% during the study period.

The lactic acid segment is projected to experience significant growth during the forecast period. The segment's growth is driven by growing demand from food-grade applications (acidity control, preservation, fermentation support) and bio-based materials, especially Polylactic Acid (PLA). As brands and regulators push for lower-carbon, renewable and compostable packaging, lactic acid consumption can rise with PLA capacity growth and broader adoption in disposable foodservice items and films.

By Application

To know how our report can help streamline your business, Speak to Analyst

The Industrial Segment Dominates the Market Due to Extensive Use of Product

In terms of application, the market is categorized into industrial, food and beverage, pharmaceutical, and other sectors.

The industrial segment accounted for the largest share in 2025 due to expansion of packaging, coatings, and adhesive value chains (notably for acetic-acid-linked derivatives), as well as higher maintenance and efficiency needs in process industries. A growing focus on safer, more biodegradable chemistries and stricter discharge norms can further shift users toward optimized organic-acid formulations over harsher inorganic alternatives. Furthermore, the segment is set to hold a 36.9% share in 2025.

The food & beverage segment is expected to experience favorable growth over the projected period. The growth of this segment is driven by rising packaged-food consumption, urbanization and the expansion of cold chains, which increases the need for shelf-life and taste consistency. Clean-label preferences also support citric and lactic acids as they are widely recognized ingredients that help reduce reliance on some synthetic preservatives. The segment is expected to grow at a CAGR of 5.6% over the forecast period.

The pharmaceutical segment is witnessing favorable growth throughout the forecast period, driven by increase in consumption of pharmacopeial-grade acids, and growth in generics, OTC products, syrups, effervescents and topical formulations. Expanding healthcare access and manufacturing capacity in emerging markets further support volumes. Stricter quality, traceability and impurity control requirements also favor reliable suppliers, often increasing the value per ton through higher-grade specifications.

Organic Acid Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Organic Acid Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 9.39 billion, and is expected to maintain the leading share in 2026, with USD 9.91 billion. The region serves as a major hub for both production and consumption of fermentation-derived organic acids, supported by large-scale manufacturing clusters, growing demand for processed food and expanding animal nutrition markets. India and Southeast Asia contribute to demand growth through beverages, packaged foods, and livestock sector modernization. Regional investment in bio-based chemicals and materials also supports demand for lactic acid and its derivatives.

China Organic Acid Market

In 2025, the China market reached USD 3.16 billion. China remains a key producer of citric acid and other fermentation products, benefiting from scale, integrated upstream feedstocks, and export-oriented supply chains. It is a central node in the global fermentation-based organic acid supply chain, boasting a large installed capacity in citric acid and supporting capabilities across food ingredients, feed additives, and industrial intermediates. Domestic demand is driven by beverages, convenience foods and animal nutrition, while exports supply global ingredient sector. Environmental compliance and energy efficiency upgrades are increasingly shaping plant operating costs and competitive positioning.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is also a significant contributor to the market, estimated to reach USD 3.95 billion by 2026, driven by the packaged food and beverage manufacturing sector, industrial acetyl-chain consumption, and the large animal nutrition market. The region also benefits from bio-based innovation ecosystems that support lactic acid derivatives and PLA value chains, alongside a robust regulatory framework for food additives and pharmaceutical excipients. Investment priorities include supply reliability, sustainability credentials and domestic manufacturing footprints for strategic ingredients.

U.S. Organic Acid Market

In 2025, the U.S. market reached USD 3.30 billion. The market is driven by large food and beverage manufacturing capacity, animal nutrition demand and industrial consumption in coatings, adhesives and chemical intermediates. Bio-based material initiatives and sustainability-driven procurement are also relevant for lactic acid and derivative chains.

Europe

Europe is expected to experience significant growth in the coming years. During the forecast period, the European region is projected to record a growth rate of 5.8% and reach the valuation of USD 5.37 billion in 2026. The region's growth is driven by stringent food safety, chemical regulation and sustainability requirements, which support demand for traceable, low-emission organic acids. Consumption is supported by food and beverage acidulants, feed hygiene applications and industrial processing uses, while innovation efforts emphasize circular feedstocks, process efficiency, and decarbonization. Import dependence for some acids and competition with alternative additives can influence pricing dynamics.

U.K. Organic Acid Market

The U.K. market in 2025 was valued at USD 0.66 billion, representing approximately 5.0% of the global market revenue.

Germany Organic Acid Market

Germany’s market reached USD 1.08 billion in 2025, equivalent to around 6.3% of global sales.

Latin America

Latin America is experiencing steady growth. The Latin America market in 2026 is expected to reach a valuation of USD 2.36 billion, driven by the expansion of food and beverage industries, animal production, and export-oriented agribusiness value chains. The availability of agricultural feedstocks can support fermentation-based economics in select countries, while imports remain important for certain specialty acids. Currency and logistics volatility can influence procurement strategies.

The Middle East & Africa

The Middle East & Africa region is gradually expanding, driven by the growth of food processing, increasing beverage demand, and rising animal nutrition needs, with a significant share of supply being imported. Local chemical production supports certain industrial acid chains, while large infrastructure and consumer sector investments can increase demand for industrial, cleaning and processing applications.

GCC Organic Acid Market

GCC reached a value of USD 0.41 billion by 2025, accounting for approximately 2.0% of global Organic Acid revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players are Adopting Business Expansion Strategies to Maintain Their Positions in Market

Key players compete on scale, cost position (including feedstock and utilities), fermentation and purification expertise, regulatory and quality systems (for food, pharma, and feed), and the ability to offer a consistent global supply. Some of the key market players include Celanese Corporation, BASF SE, LyondellBasell Industries, Cargill, Incorporated, and Corbion N.V. Portfolio breadth across acids and derivatives, application support and sustainability credentials (including renewable inputs, carbon intensity, and traceability) are increasingly influencing supplier selection, particularly among multinational food, beverage and consumer goods customers.

LIST OF KEY ORGANIC ACID COMPANIES PROFILED

- Celanese Corporation (U.S.)

- BASF SE (Germany)

- LyondellBasell Industries (U.S.)

- Cargill, Incorporated (U.S.)

- Corbion N.V. (Netherlands)

- NatureWorks LLC (U.S.)

- Jungbunzlauer Suisse AG (Switzerland)

- ADM (Archer Daniels Midland Company)

- TTCA Co., Ltd. (China)

- Weifang Ensign Industry Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- April 2025: thyssenkrupp Uhde (Uhde Inventa-Fischer) and Praj Industries announced a strategic partnership to offer an end-to-end PLA technology package (upstream-to-downstream), explicitly tied to producing different grades of lactic acid as part of integrated biorefineries.

- November 2024: INEOS and GNFC signed an MoU to build a 600,000 tpa acetic acid plant in India, signalling new regional capacity creation and a push toward more localized acetyl supply chains.

- October 2024: Praj Industries inaugurated its biopolymers demonstration facility (India), showcasing integrated capability that includes lactic acid and lactide sections supporting scale-up validation and future commercialization pathways.

- March 2024: Celanese initiated a major acetic acid capacity expansion at Clear Lake (reported at ~1.3 million tons), thereby directly increasing global supply headroom for acetyl/organic-acid-linked downstream applications.

- December 2023: Corbion announced mechanical completion of its new “circular” lactic acid plant in Rayong, Thailand, positioning the market for a lower-footprint lactic acid supply as commissioning moved toward completion in early 2024.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.8% from 2026-2034 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Type, Application, and Region |

|

By Type |

· Acetic Acid · Citric Acid · Lactic Acid · Others |

|

By Application |

· Industrial · Food & Beverage · Pharmaceutical · Others |

|

By Geography |

· North America (By Type, Application, and Country) o U.S. (By Application) o Canada (By Application) · Europe (By Type, Application, and Country) o Germany (By Application) o France (By Application) o Italy (By Application) o U.K. (By Application) o Rest of Europe (By Application) · Asia Pacific (By Type, Application, and Country) o China (By Application) o Japan (By Application) o India (By Application) o South Korea (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Type, Application, and Country) o Brazil (By Application) o Mexico (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Type, Application, and Country) o GCC (By Application) o South Africa (By Application) o Rest of the Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 22.12 Billion in 2025 and is projected to reach USD 36.34 Billion by 2034.

Recording a CAGR of 5.8%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The industrial application segment led in 2025.

Asia Pacific held the highest market share in 2025.

Celanese Corporation, BASF SE, LyondellBasell Industries, Cargill, Incorporated, and Corbion N.V. are some of the prominent players in the market.

The rising demand for bio-based, fermentation-derived acids drives the market growht.

The wider use of products as acidulants/preservatives and pH regulators in packaged food & beverages favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 160

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us