Cold Insulation Market Size, Share & Industry Analysis, By Material Type (Polyurethane Foam, Fiberglass, Polystyrene Foam, Phenolic Foam, and Others), By Application (HVAC, Refrigeration, Oil & Gas, Chemicals, and Others), and Regional Forecast, 2026-2034

Cold Insulation Market Overview

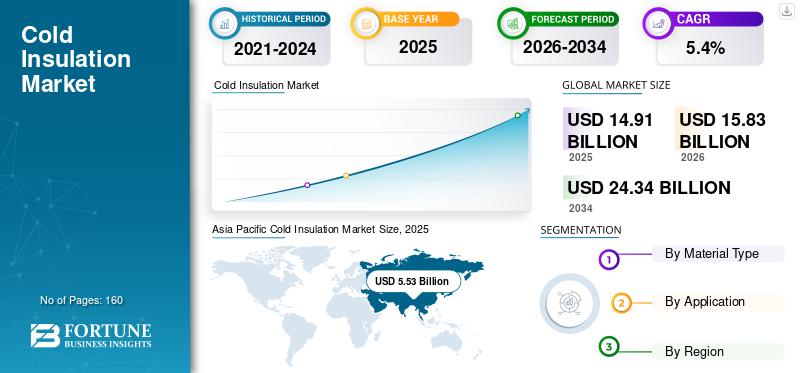

The global cold insulation market size was valued at USD 14.91 billion in 2025. The market is projected to grow from USD 15.83 billion in 2026 to USD 24.34 billion by 2034, exhibiting a CAGR of 5.4% during the forecast period. Asia Pacific dominated the cold insulation market with a market share of 37.09% in 2025.

Cold insulation refers to insulation systems used to limit heat gain and prevent condensation on equipment and infrastructure operating below ambient temperature, such as chilled-water lines, refrigeration piping, and cold rooms, and cryogenic assets in LNG and industrial gas value chains. Cold insulation materials include rigid foams (PU and phenolic boards, EPS/XPS), fibrous products (glass wool), and specialized solutions used where vapor control, dimensional stability, and safety requirements are critical. Performance is determined by thermal conductivity, water vapor diffusion resistance, mechanical strength, long-term dimensional stability, and compliance with fire and application-specific standards.

Market growth is driven by rising energy-efficiency expectations across building services (HVAC chilled-water networks), ongoing expansion of the cold chain for food and pharmaceuticals, and sustained industrial investment in chemicals and process refrigeration. In parallel, growth in LNG liquefaction, regasification, and cryogenic storage is driving demand for higher-specification cold-insulation solutions for pipes, tanks, and equipment. At the same time, specification scrutiny around fire performance, vapor control, and installation quality continues to shape product selection and system design.

Furthermore, the market comprises several major players, including Kingspan, Johns Manville, Saint–Gobain, Dow, and CertainTeed. Broad product portfolios spanning HVAC, refrigeration, and industrial cold applications, alongside regional manufacturing and distribution footprints, support these companies’ competitive positioning in the global market.

Download Free sample to learn more about this report.

COLD INSULATION MARKET TRENDS

Building-Efficiency Policy, Cold-Chain Buildout, and Cryogenic Project Cycles are Significant Market Trends

Cold insulation demand is increasingly shaped by energy-efficiency and decarbonization pathways that prioritize reducing heating and cooling loads and improving system performance. High-performing building envelopes and well-insulated chilled-water networks are increasingly positioned as durable, long-lifetime efficiency measures, reinforcing demand for reliable insulation systems and vapor-control detailing. In parallel, growth in refrigerated warehousing and temperature-controlled logistics is raising demand for insulated panels, pipe insulation, and condensation-control solutions across food and pharmaceutical chains.

Alongside building-driven demand, industrial and LNG/cryogenic project cycles are influencing product mix. Cryogenic assets tend to require higher-performance insulation solutions and more robust vapor and moisture management, increasing the importance of engineered system designs and qualified installation. Manufacturers are also investing in product compliance documentation and system-level guidance to support specification and reduce performance gaps caused by installation variability.

- For instance, the revised EU Energy Performance of Buildings Directive (EU/2024/1275, EPBD) entered into force on 28 May 2024. It must be transposed by 29 May 2026, supporting multi-year renovation activity and insulation demand.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Energy-Efficient Cooling Infrastructure, Cold-Chain Expansion, and LNG/Cryogenic Buildout are Driving Market Growth

HVAC and refrigeration systems are core demand centers for cold insulation, as condensation control and heat-gain reduction directly affect operating efficiency and reliability. In commercial buildings and district cooling, well-insulated chilled-water networks help stabilize temperatures and reduce cooling loads. In cold rooms, warehouses, and refrigerated processing, insulation performance supports temperature stability and reduces energy costs, which is especially important as operators face tighter performance expectations and higher electricity prices.

Beyond building services, chemicals, and oil and gas applications, cold insulation is used to maintain process temperatures, protect equipment, and manage moisture. LNG infrastructure, in particular, is insulation-intensive, and a wave of new LNG export capacity additions through the late 2020s is expected to support incremental demand for higher-specification cold-insulation systems in pipes and tanks. These drivers collectively sustain volume growth and, in higher-performance niches, support value growth through product mix.

- For instance, the IEA notes that efficient building design integrating high-performing envelopes is the most effective way to reduce buildings' thermal needs, reinforcing insulation as a key efficiency lever.

MARKET RESTRAINTS

Fire-Safety Scrutiny, Vapor-Control Complexity, and Project-to-Project Specification Variability Can Restrict Market Expansion

Cold insulation systems must manage both thermal performance and moisture ingress. In practice, failures are often linked to vapor barrier discontinuities, water ingress, and workmanship issues that can cause localized condensation, corrosion under insulation, or performance loss. This raises the importance of detailing, jacketing selection, and installer skill, and can slow adoption in cost-sensitive projects where long-term performance is undervalued.

In parallel, fire-performance scrutiny and code complexity can increase qualification costs for certain foam products and assemblies, especially in building applications. In industrial settings, procurement often emphasizes reliability and lifecycle risk reduction, which can constrain substitution and slow adoption of new materials unless backed by strong field evidence and compliance documentation. Leading suppliers increasingly provide compliance cards, system documentation, and installation guidance to support certification and reduce specification friction.

MARKET OPPORTUNITIES

Cold-Chain Modernization, District Cooling Growth, and Cryogenic Infrastructure Investments are Creating Lucrative Growth Opportunities

Growth in temperature-controlled food and pharmaceutical logistics continues to expand the installed base of refrigerated buildings and industrial refrigeration networks. This creates recurring demand for insulation in new cold storage construction, retrofits, and expansions, including insulated panels, pipe insulation, and accessories that improve vapor tightness and reduce leakage-related losses.

District cooling expansion and industrial electrification trends can increase chilled-water distribution and process-cooling needs, thereby supporting incremental insulation demand. Cryogenic investments in LNG and industrial gases can further expand high-value niches where advanced materials and engineered system designs reduce installation complexity and improve reliability. This is expected to boost the cold insulation market growth in the coming years.

- For example, the IEA’s LNG capacity tracker highlights a major wave of LNG export capacity additions through 2030, which can raise demand for cryogenic insulation in terminals and associated infrastructure.

MARKET CHALLENGES

System-Level Performance Assurance, Installation Quality Control, and Long-Term Moisture Management Can Hamper Market Growth

A central challenge in cold insulation is that realized performance depends heavily on system integrity, especially vapor control. Even high-performance materials can underperform if joints, penetrations, and terminations are not sealed consistently, or if jacketing is damaged during operations. This makes quality assurance, contractor capability, and periodic maintenance important determinants of lifecycle outcomes.

Cold insulation projects are often delivered through fragmented contracting ecosystems, and the required workmanship varies by application (HVAC vs industrial cryogenic). Maintaining consistent installation quality across geographies, training installers, and aligning documentation with local codes can be difficult, particularly for projects that prioritize the lowest upfront cost.

- For instance, the IEA’s Energy Efficiency analysis emphasizes accelerating retrofits to reduce heating and cooling energy demand, implying higher scrutiny of installed performance and verification.

Segmentation Analysis

By Material Type

Polyurethane Foam Segment Led Market Due to Its Widespread Use in Cold Rooms

Based on material type, the market is segmented into polyurethane foam, fiberglass, polystyrene foam, phenolic foam, and others.

The polyurethane foam segment accounted for the largest cold insulation market share in 2025. The segment’s growth is driven by widespread use in cold rooms and insulated panels, as well as strong adoption in chilled-water pipe insulation, where closed-cell structures help manage vapor ingress. PU-based systems also benefit from established converting capacity and strong contractor familiarity, supporting consistent specification in refrigeration and HVAC applications. Furthermore, the segment held a 36.6% share in 2025.

The fiberglass segment is projected to grow at a 5.3% CAGR during the study period, supported by its broad use in HVAC and industrial insulation, where faced systems and jacketing solutions provide vapor control.

The polystyrene foam segment is projected to grow significantly in the coming years. The segment’s growth is driven by rising demand in cold storage floors, selected building envelope elements, and cost-sensitive applications where compressive strength and moisture resistance are valued.

By Application

To know how our report can help streamline your business, Speak to Analyst

HVAC Segment Dominated Market Due to Extensive Use of Products

By application, the market is categorized into HVAC, refrigeration, oil & gas, chemicals, and others.

The HVAC segment accounted for the largest share in 2025. The segment's growth is driven by demand for condensation control and energy efficiency in chilled-water distribution lines, air-handling systems, and commercial building services. Flexible elastomeric foams and faced fibrous systems are widely used across HVAC systems, as moisture management and installation practicality are critical. Furthermore, the segment is set to hold a 30.0% share in 2025.

The refrigeration segment is also expected to grow at a CAGR of 5.4% over the forecast period. The segment's demand is driven by growth in cold storage warehouses, food processing, and temperature-controlled logistics for pharmaceuticals. Insulation demand is closely linked to new cold room construction, retrofits, and expansions, with PU insulated panels and associated accessories playing a structural role in maintaining stable internal temperatures.

The oil & gas segment is anticipated to grow at a moderate pace during the forecast period. The growth is supported by LNG and cryogenic infrastructure buildout, which is insulation-intensive and often uses higher-specification solutions.

Cold Insulation Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Cold Insulation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 5.53 billion, and is expected to maintain its leading share in 2026, valued at USD 5.93 billion. The region benefits from construction intensity, expansion of cold storage and food logistics networks, and growing demand for chilled-water and industrial refrigeration insulation in urban infrastructure. China remains the largest consumption base, while India and Southeast Asia continue to increase demand linked to housing, commercial development, and cold-chain expansion.

China Cold Insulation Market

In 2025, the China market reached USD 2.00 billion. China’s demand is supported by large-scale cold-chain infrastructure, industrial refrigeration systems, and extensive HVAC infrastructure in commercial and public buildings.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is also a significant contributor to the market, with the market estimated to reach USD 3.21 billion by 2026. The market’s growth is driven by a large installed base of commercial buildings and industrial refrigeration, as well as continued investment in cold-chain infrastructure. The region’s demand is linked to retrofit activity, energy-code adoption across states and provinces, and ongoing HVAC system upgrades in commercial facilities.

U.S. Cold Insulation Market

In 2025, the U.S. market reached USD 2.59 billion. The U.S. dominates regional consumption due to its large cold storage footprint, extensive HVAC installed base, and significant industrial demand across chemicals and LNG-linked infrastructure.

Europe

Europe is expected to experience significant growth in the coming years. During the forecast period, the European region is projected to grow at a 4.9% rate, reaching a valuation of USD 3.09 billion in 2026. The region’s market is supported by renovation activity, established insulation standards, and policy-driven efficiency targets that prioritize reduced heating and cooling loads. Mature manufacturing and distribution networks, along with a strong focus on system-level compliance and documentation, support adoption across HVAC and industrial applications.

U.K. Cold Insulation Market

The U.K. market in 2025 reached USD 0.52 billion, representing approximately 4.4% of global market revenue.

Germany Cold Insulation Market

Germany’s market reached approximately USD 0.57 billion in 2025, equivalent to around 5.8% of global sales.

Latin America

Latin America is experiencing steady growth. The Latin America market in 2026 is expected to reach a valuation of USD 1.76 billion. The demand is driven by expanding cold-chain needs, gradual adoption of insulation in commercial buildings, and industrial refrigeration in food processing. Demand is concentrated in building services and cold storage facilities, with variability by country depending on construction cycles and availability of insulation supply.

Middle East & Africa

The Middle East & Africa region is gradually expanding, driven by project-led construction in GCC markets, industrial facilities, and growing cold-chain needs. Harsh climatic conditions, high cooling demand, and LNG/industrial gas infrastructure reinforce the value proposition of high-quality cold insulation systems.

GCC Cold Insulation Market

GCC reached USD 0.98 billion in 2025, accounting for approximately 4.6% of global revenues. GCC demand is supported by large-scale commercial construction, industrial projects, and cryogenic and LNG-linked infrastructure where cold insulation intensity is high.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies are Expanding Deposits, Processing Footprints, and Specialty Grades to Maintain Their Positions in Market

The market includes global insulation manufacturers, specialist mechanical insulation suppliers, and advanced materials companies serving industrial cold and cryogenic applications. Competition is shaped by thermal performance, vapor-control detailing, compliance and certifications, supply reliability, and the ability to deliver system solutions (materials, accessories, and installation guidance). Leading companies differentiate through performance-validated product ranges, engineered system designs for complex assets, and contractor support that improves installation quality and reduces lifecycle risks. Some key market players include Kingspan, Johns Manville, Saint–Gobain, Dow, and CertainTeed.

LIST OF KEY COLD INSULATION COMPANIES PROFILED

- Armacell (Luxembourg)

- Kingspan (Ireland)

- Johns Manville (U.S.)

- Saint-Gobain (France)

- K-FLEX (Italy)

- Aspen Aerogels (U.S.)

- Knauf Insulation (U.K.)

- DOW (U.S.)

- Huntsman (U.S.)

- CertainTeed (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Armacell inaugurated a new aerogel insulation manufacturing facility in Pune, India, to produce ArmaGel XGH/XGC for global supply and stated that its available aerogel blanket capacity doubles, signaling a major capacity expansion for cryogenic and dual-temperature insulation used in energy and industrial systems.

- April 2025: Armacell launched ArmaGel XGC, highlighting ASTM C1728 compliance and suitability down to -196°C, and noted additional production commencing at its new India facility, signaling portfolio upgrades and supply-chain resilience to meet cryogenic and dual-temperature cold insulation demand.

- September 2024: Armacell announced it would open a new aerogel plant in India and launched the next-generation ArmaGel XG platform (ASTM C1728-compliant), including plans to add ~1 million m²/year of capacity by mid-2025, signaling accelerated investment to scale aerogel insulation supply for industrial and energy end uses.

- June 2024: Armacell acquired the engineering business of E&M Industries (Australia), an insulation fabrication/jacketing player, signaling a move toward higher-value solution selling and deeper reach into industrial cold/technical insulation projects in Asia Pacific.

- October 2022: Armacell acquired Austroflex (Austria), a specialist in flexible pre-insulated pipe systems (district heating/cooling and technical installations), expanding its signaling portfolio for pre-insulated pipe solutions relevant to cooling networks and low-temperature distribution.

- July 2022: Aspen Aerogels announced plans to construct an advanced manufacturing facility in Statesboro, Georgia, to significantly expand aerogel capacity, signaling longer-term scaling of high-performance aerogel insulation supply for energy/industrial applications (including cold/cryogenic use cases for aerogel blankets).

- July 2022: Armacell acquired IZOLIR (Serbia), a manufacturer of pre-insulated pipes, signaling entry into and scale-up in the fast-growing pre-insulated pipe segment, supporting energy-efficient thermal distribution in pipelines and installations.

- June 2021: ROCKWOOL began commercial production at its West Virginia factory (industrial/commercial insulation), signaling incremental North American supply capacity that can support broader technical insulation availability for industrial and building-services applications where condensation control and thermal performance are critical.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.4% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Material Type, Application, and Region |

| By Material Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 14.91 billion in 2025 and is projected to reach USD 24.34 billion by 2034.

Recording a CAGR of 5.4%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The HVAC application segment led the market in 2025.

Asia Pacific held the highest market share in 2025.

Kingspan, Johns Manville, Saint–Gobain, Dow, and CertainTeed are some of the prominent players in the market.

The growth driver is the rapid expansion of cold-chain and refrigeration infrastructure.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us