Ductile Iron Pipe Market Size, Share & Industry Analysis, By Application (Sewerage & Wastewater Systems, Irrigation & Agriculture, Fire Protection Networks, Industrial Utilities, and Others), and Regional Forecast, 2026-2034

Ductile Iron Pipe Market Size and Future Outlook

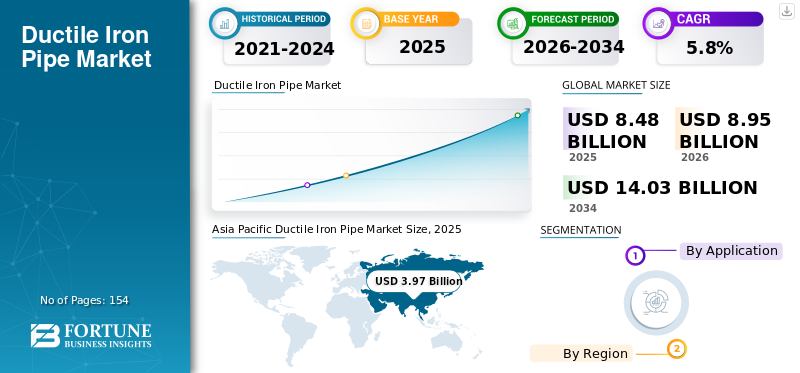

The global ductile iron pipe market size was valued at USD 8.48 billion in 2025. The market is projected to grow from USD 8.95 billion in 2026 to USD 14.03 billion by 2034 at a CAGR of 5.8% during the forecast period. Asia Pacific dominated the global ductile iron pipe market with a market share of 46.81% in 2025.

Ductile Iron Pipe (DIP) is a critical infrastructure material used primarily for pressurized water transmission, sewerage & wastewater systems, irrigation networks, fire protection systems, and industrial utility pipelines. It combines the mechanical strength of cast iron with enhanced ductility, making it suitable for high-pressure, buried pipeline applications requiring long service life and structural reliability. Major consumption pathways include municipal water supply networks, sewerage and wastewater force mains, irrigation and agricultural conveyance, fire protection networks, and industrial utilities, where durability and load-bearing performance are critical.

Asia Pacific represents the largest regional demand base, while sewerage & wastewater systems and water supply infrastructure together account for the dominant share of global consumption. They are primarlity used in urban water infrastructure expansion, aging pipeline replacement cycles, and large-scale public works programs, which are most concentrated in Asia and increasingly active across emerging economies. Duktus, CNBM International, Xinxing Ductile Iron Pipes, U.S. Pipe, and McWane Inc. are the key players operating in the market.

Download Free sample to learn more about this report.

Ductile Iron Pipe Market KEY TAKEAWAYS

- 2025 Market Size: USD 8.48 Billion

- 2026 Market Size: USD 8.95 Billion

- 2034 Forecast Market Size: USD 14.03 Billion

- CAGR: 5.8% from 2026–2034

- Asia Pacific dominated the ductile iron pipe market with a 46.81% share in 2025.

- The sewerage & wastewater systems segment accounted for the largest market share in 2025.

- The irrigation & agriculture segment held a significant share in 2025.

Asia Pacific

Asia Pacific dominated the market in 2025, driven by rapid urbanization and large-scale water infrastructure projects.

North America

North America is witnessing steady growth, supported by aging water infrastructure replacement and asset management programs.

Europe

Europe is growing steadily, driven by infrastructure modernization and stringent environmental regulations.

U.S.

The U.S. market reached USD 1.07 billion in 2025, supported by strong demand for water distribution and high-pressure pipeline applications.

Japan

Japan is witnessing stable demand, supported by investments in resilient water infrastructure and pipeline modernization.

Read More

DUCTILE IRON PIPE MARKET MARKET TRENDS

Shift Toward Long-Life Pipeline Solutions in Municipal Infrastructure

A key trend in the market is the increasing preference for long-life pipeline systems in municipal water and wastewater infrastructure. Utilities are moving away from short-term, cost-minimized material choices and more toward pipeline solutions that offer higher structural integrity, longer service life, and reduced failure rates. Ductile iron pipes are increasingly being specifically in trunk mains, transmission pipelines, and critical pressure zones where failure risk carries high economic and social costs.

This trend is reshaping procurement behavior. Instead of focusing solely on upfront material costs, municipalities and public authorities are incorporating life-cycle cost analysis, asset management frameworks, and resilience criteria into quotation specifications. As a result, ductile iron pipes maintain a strong position even against lighter polymer alternatives, particularly in high-load urban environments, deep-burial installations, and even in the areas with unstable soil conditions.

MARKET DYNAMICS

MARKET DRIVERS

Expansion and Rehabilitation of Sewerage & Wastewater Infrastructure to Drive Market Growth

Sewerage and wastewater systems represent the largest and most structurally stable demand driver for ductile iron pipes. Rapid urban population growth, tightening environmental regulations, and increased wastewater treatment capacity requirements are pushing governments to expand and modernize sewer networks. Ductile iron pipes are widely used in wastewater force mains, rising mains, and deep sewer installations, where pressure resistance and mechanical strength are essential.

In both developed and emerging economies, the replacement of aging concrete, asbestos-cement, and legacy cast-iron pipelines further reinforces demand. Sewer systems often operate under corrosive conditions and external loads, making ductile iron with appropriate linings and coatings a preferred solution. This leads to a long-term demand foundation that is less sensitive to short-term economic cycles than discretionary infrastructure spending.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

High Initial Material Cost Compared with Polymer Alternatives to Hinder Market Growth

One of the primary restraints for the ductile iron pipe market growth is its higher upfront material cost compared with PVC, HDPE, and other plastic pipe alternatives. In cost-sensitive projects—particularly in smaller-diameter applications or low-pressure rural networks procurement authorities may prioritize lower initial expenditure over long-term durability, limiting ductile iron adoption.

Additionally, ductile iron pipes are heavier and require more robust handling and installation logistics, which can increase transportation and installation costs in remote or logistically constrained regions. These factors can restrain their penetration in applications where mechanical performance requirements are less stringent, even though life-cycle economics may favor ductile iron in the long run.

MARKET OPPORTUNITIES

Water Security, Climate Resilience, and Flood-Resistant Infrastructure Investment to Pose as Growth Opportunity

Global emphasis on water security and climate-resilient infrastructure projects presents a significant opportunity for increasing the demand for ductile iron pipes. Increasing incidents of flooding, ground movement, and extreme weather events are forcing utilities to adopt pipeline materials that can withstand external stresses without catastrophic failure. Ductile iron’s flexibility, joint integrity, and load-bearing capacity position it favorably in resilience-focused infrastructure planning.

Government-funded programs targeting leakage reduction, non-revenue water control, and system hardening further enhance opportunity. In regions prone to seismic activity, heavy traffic loads, or aggressive soils, ductile iron pipes are often specified over lighter materials, enabling manufacturers to tap into higher-value project opportunities even if total installed length growth remains moderate.

MARKET CHALLENGES

Competition from Alternative Materials and Specification Substitution to Hamper Product Demand

The market faces sustained competition from PVC, HDPE, and steel pipes, particularly in regions where polymer pipelines are aggressively promoted for cost or ease of installation. Advances in plastic pipe technology, such as improved pressure ratings and joint systems, continue to challenge the demand of ductile iron in certain segments.

Specification substitution remains a challenge, especially in markets with fragmented standards or limited engineering oversight. Where procurement decisions prioritize short-term budgets over lifecycle performance, ductile iron may lose share despite its technical advantages. Maintaining specification relevance requires ongoing engagement with utilities, engineers, and regulators.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade policies and geopolitics influence the market primarily through raw material costs, cross-border project pipelines, and regional manufacturing strategies. Tariffs on iron and steel inputs, localization requirements, and public procurement preferences can alter cost competitiveness and supply chain configuration.

On the demand side, geopolitical uncertainty encourages regionalization of infrastructure supply chains, favoring domestic or regionally based pipe manufacturers. This supports local production investment but can reduce export-driven growth opportunities. Long-term infrastructure contracts increasingly emphasize supply security and local manufacturing presence over lowest-cost global sourcing.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D activities in the market is increasingly focused on advanced linings, coatings, and joint technologies that extend service life and improve corrosion resistance. Developments such as enhanced cement mortar linings, zinc-aluminum coatings, polyethylene sleeving, and restrained joint systems are designed to improve performance in aggressive soils and high-pressure applications.

Manufacturers are also investing in process optimization, casting consistency, and digital quality control, enabling tighter dimensional tolerances and reduced defect rates. These innovations support higher-specification compliance and allow suppliers to compete more effectively in premium municipal and industrial projects.

SEGMENTATION ANALYSIS

By Application

To know how our report can help streamline your business, Speak to Analyst

Sewerage & Wastewater Systems Lead Due to Requirement in High Structural and Pressurized Wastewater Conveyance Systems

Based on application, the market is segmented into sewerage & wastewater systems, irrigation & agriculture, fire protection networks, industrial utilities, and others.

The sewerage & wastewater systems segment dominates the market due to the extensive use of ductile iron pipes in force mains and pressurized wastewater conveyance systems. These systems demand materials capable of withstanding internal pressure, corrosive environments, and external loads, making ductile iron a preferred choice. The segment is projected to grow at a 6.4% CAGR through the forecast period, driven by energy efficiency mandates.

The irrigation & agriculture segment holds a noteworthy share. In agriculture, pipes handle variable pressures, sediment-laden water, and exposure to fertilizers without cracking. Their longevity minimizes replacement costs in large-scale networks for drip and sprinkler systems, enhancing water efficiency amid climate variability. Segment’s growth is tied to precision farming and government subsidies in arid regions like India, promoting sustainable crop yields.

Fire networks require reliable, high-pressure performance with zero failure risk during emergencies. Ductile iron's impact resistance and joint integrity ensure rapid water delivery, meeting stringent NFPA standards for municipal hydrants and sprinklers. Adoption rises with urban fire safety upgrades and insurance incentives for durable infrastructure.

Industrial utilities register positive growth. Utilities in power plants, chemical facilities, and mining operations convey abrasive slurries, cooling water, and process fluids under extreme conditions. The material's abrasion resistance and thermal stability support high-velocity flows, reducing downtime in continuous operations. Segment’s expansion is linked to industrial electrification and green hydrogen projects needing robust piping.

The other segment includes oil/gas transport, hydropower & dams, and mining slurries, where specialized fittings handle thermal cycling and harsh chemistries are required. Ductile iron provides cost-effective scalability for niche, high-stress uses beyond standard water systems. Trends favor it in emerging applications like desalination outflows, driven by customization options.

DUCTILE IRON PIPE MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Ductile Iron Pipe Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for the leading ductile iron pipe market share in 2025. Growth is driven by rapid urbanization, large-scale water and sanitation programs, and extensive investment in irrigation infrastructure. China and India dominate the regional demand due to massive need for municipal pipeline networks and ongoing replacement cycles.

China Ductile Iron Pipe Market

China’s market is one of the largest globally, with 2025 revenue value at USD 1.80 billion, representing roughly 21.2% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America’s demand is largely replacement-driven, supported by aging water and sewer infrastructure and asset management programs.

U.S. Ductile Iron Pipe Market

In 2025, the U.S. represented USD 1.07 billion market in North America, driven primarily by strong demand from the industrial sectors. The U.S. accounts for roughly 12.6% of global market sales. The U.S. accounts for the majority of regional demand, with ductile iron favored for critical mains and high-pressure applications.

Europe

Europe’s market is shaped by stringent engineering standards and lifecycle-focused procurement. Replacement of aging infrastructure and strong regulatory oversight sustain steady demand, particularly in Germany, France, and U.K. Increasing demand for sustainability and strict environmental regulations boost adoption in water management, driving market demand.

Germany Ductile Iron Pipe Market

The Germany market in 2025 valued at around USD 0.48 billion, representing roughly 5.7% of global market revenues.

U.K. Ductile Iron Pipe Market

The U.K. market in 2025 was valued around USD 0.20 billion, representing roughly 2.4% of global market revenues.

Latin America

Latin America represents a moderate but growing market, driven by urban water access expansion and sewerage upgrades, particularly in Brazil and Mexico. Urbanization in these countries fuels incresing investments in water infrastructure and water distribution. In addition, the demand emerges from housing and industrial investments, though a smaller share reflects developing infrastructure.

Middle East & Africa

Demand in this region is influenced by water security, desalination-linked transmission pipelines, and irrigation projects, with the Gulf countries and South Africa acting as key demand centers. The growth stems from GCC wastewater investments and scarcity solutions, with expansions such as China's plant in Egypt. South Africa and the UAE lead via population-driven projects.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Prominent Market Players are Investing in Developing Enhanced Products for High Performance

The market for ductile iron pipe is underway for major investments as manufacturers respond to rising sustainability expectations and higher performance requirements across end-use industries. Leading producers, such as Duktus, CNBM International, Xinxing Ductile Iron Pipes, U.S. Pipe, and McWane Inc. are directing their capital investment toward process optimization, product quality enhancement, and environmentally aligned manufacturing practices. Innovation efforts are increasingly focused on enhancing purity consistency, reducing the environmental footprint, and developing grades suitable for advanced products.

LIST OF KEY DUCTILE IRON PIPE PLAYERS PROFILED IN THE REPORT

- Duktus (Switzerland)

- CNBM International (China)

- Xinxing Ductile Iron Pipes (China)

- S. Pipe (U.S.)

- McWane Inc. (U.S.)

- Kubota Corporation (Japan)

- Saint-Gobain (France)

- AMNS India (India)

- Electrosteel Castings Ltd. (India)

- Tata Metaliks Ltd. (India)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Electrosteel Castings Ltd. expanded ductile iron pipe capacity to around 1 million tonnes by late 2025 through brownfield upgrades, driven by export growth to Africa, the Middle East, and other regions despite domestic slowdowns.

- July 2023: McWane Inc. expanded its U.S. manufacturing capabilities, primarily through ductile iron utility pole facilities adjacent to existing pipe operations, indirectly supporting municipal infrastructure demands. While not exclusively for pipe replacement projects, these investments enhanced overall production versatility for waterworks products amid rising utility needs.

REPORT COVERAGE

The report provides a detailed analysis of the ductile iron pipe market. It focuses on key aspects, such as leading companies and application. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors contributing to the market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion), Volume (Kiloton) |

|

Growth Rate |

CAGR of 5.8% from 2026 to 2034 |

|

Segmentation |

By Application and By Region |

|

By Application |

|

|

By Region |

North America (By Application, By Country) o U.S. (By Application) o Canada (By Application) Europe (By Application, By Country) o Germany (By Application) o U.K. (By Application) o France (By Application) o Italy (By Application) o Rest of Europe (By Application) Asia Pacific (By Application, By Country) o China (By Application) o India (By Application) o Japan (By Application) o Rest of Asia Pacific (By Application) Latin America (By Application, By Country) o Mexico (By Application) o Brazil (By Application) o Rest of Latin America (By Application) Middle East & Africa (By Application, By Country) o GCC (By Application) o South Africa (By Application) o Rest of Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 8.48 Billion in 2025 and is projected to reach USD 14.03 Billion by 2034.

Recording a CAGR of 5.8%, the market is slated to exhibit steady growth during the forecast period.

The sewerage & wastewater systems segment led in 2025.

Asia Pacific held the highest market share in 2025.

Expansion and rehabilitation of sewerage & wastewater infrastructure drives market growth.

- 2021-2034

- 2025

- 2021-2024

- 154

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us