Geosynthetic Clay Liner Market Size, Share & Industry Analysis, By Application (Landfill, Containment & Wastewater Treatment, Roadways & Civil Construction, Energy, and Others), and Regional Forecast, 2026-2034

Geosynthetic Clay Liner Market Size and Future Outlook

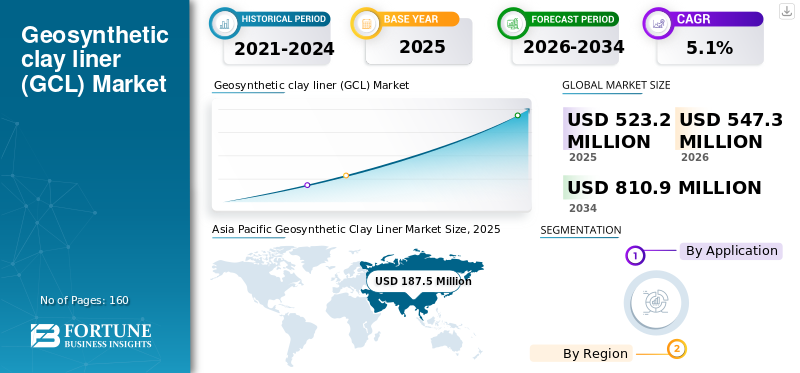

The global geosynthetic clay liner market size was valued at USD 523.2 million in 2025. The market is projected to grow from USD 547.3 million in 2026 to USD 810.9 million by 2034, exhibiting a CAGR of 5.1% during the forecast period. Asia Pacific dominated the geosynthetic clay liner market with a market share of 35.83% in 2025.

Geosynthetic clay liners are factory-manufactured hydraulic barriers, typically comprising a layer of sodium bentonite encapsulated between geotextiles (often needle-punched/stitched) and, in some designs, bonded to a geomembrane or film. When hydrated, the bentonite swells to form a very low-permeability layer, offering self-sealing around minor penetrations and overlapping self-sealing characteristics in many constructions.

The market growth is driven by tighter containment performance expectations for municipal and industrial waste facilities, greater use of engineered liners in water and wastewater infrastructure, and increasing deployment in mining and energy containment, where chemical compatibility and slope stability are key. At the same time, project timing, permitting cycles, and freight sensitivity can create year-to-year demand variability, particularly for civil works and energy projects.

Furthermore, the market comprises several major players, including Solmax, Minerals Technologies Inc., Naue GmbH & Co. KG, HUESKER, Terrafix, and Geosynthetics Inc. A broad portfolio, innovative product launches, and substantial expansion of their geographic presence have supported these companies' dominance in the global market.

Download Free sample to learn more about this report.

GEOSYNTHETIC CLAY LINER MARKET TRENDS

Specification Tightening, Chemical Compatibility Engineering, and Infrastructure Programs are the Significant Market Trends

GCL procurement is becoming increasingly specification-driven as owners and design engineers tighten acceptable limits on hydraulic performance, peel strength, internal and interface shear resistance, and manufacturing quality control. Standardized specification and test-method frameworks (e.g., Geosynthetic Institute specifications and guides) support more consistent qualification, acceptance testing, and documentation across suppliers.

In parallel, more aggressive leachates in industrial waste, mining, and Coal-Combustion Residual (CCR) applications are driving increased use of polymer-modified bentonite and chemically resilient GCL constructions. For water and wastewater, the emphasis is on long-lasting barrier performance, robust installation, and predictable overlap behavior under field hydration.

- For instance, regulatory and quality assurance guidance for GCL use in landfill and environmental liner designs continues to be published and updated by U.S. state environmental agencies and the U.S. EPA, reinforcing design/QC expectations and documenting typical GCL construction types.

MARKET DYNAMICS

MARKET DRIVERS

Regulated Containment Requirements and Construction Efficiency Benefits to Drive the Market Growth

Landfill liners and caps remain a primary demand center in many regions as regulatory frameworks require low-permeability barrier systems and construction quality assurance for municipal and industrial waste facilities. Compared with compacted clay liners, GCLs provide a factory-controlled hydraulic barrier that can reduce on-site borrow material needs, enable faster installation, and deliver repeatable thickness and quality when installed under appropriate QA/QC controls.

Beyond landfills, ongoing investment in water and wastewater containment (ponds, lagoons, reservoirs, and basins), industrial secondary containment, and civil infrastructure waterproofing supports steady demand. In mining and energy containment, the ability to select chemically compatible GCL variants and reinforced constructions for steep slopes supports adoption in higher-risk environments.

- For instance, EPA guidance documents municipal solid waste landfill applications of GCLs and positions them as an accepted barrier technology when they meet performance standards.

MARKET RESTRAINTS

Permitting, Freight Sensitivity, and Project Cyclicality Can Restrict Market Expansion

GCL delivered economics are highly sensitive to freight and regional supply footprints. For many projects, supplier selection is driven by delivered cost, lead times, and the ability to meet project-specific roll sizes and QA documentation rather than ex-works pricing. In regions with limited local production, import dependence can increase cost volatility and extend procurement cycles.

Demand-side cyclicality is an additional restraint. Large landfill expansion schedules, municipal procurement timing, and the capital cycle of mining and energy projects can create short-term swings in annual demand. Where permitting or community opposition delays new waste facilities, the pace of liner deployment may slow, even when long-term waste-management needs remain structural.

- For instance, state-level design and construction quality assurance guidance emphasizes documentation, testing, and field practices, which can increase compliance workload for projects and suppliers.

MARKET OPPORTUNITIES

Water Infrastructure Programs, Mining Containment Upgrades, and Higher-Performance GCL Constructions to Create Lucrative Growth Opportunities

Public investment in water and wastewater infrastructure supports long-duration demand for dependable barrier systems in basins, reservoirs, and stormwater facilities. In many projects, GCLs are adopted for schedule compression and predictable performance where suitable subgrade preparation and protection layers are feasible.

On the industrial side, the growth of tailings management upgrades, CCR storage improvements, and stricter chemical compatibility requirements is increasing interest in polymer-modified bentonite GCLs and geomembrane-backed composite designs. Suppliers that pair products with chemical compatibility guidance, testing support, and installation training are well-positioned to capture these opportunities. This drives geosynthetic clay liner market growth.

- For example, CETCO markets polymer-modified GCL families designed for chemically aggressive leachates in mining and waste storage applications, reflecting the market shift toward compatibility-engineered products.

MARKET CHALLENGES

Installation Robustness, Slope Stability, and Long-Term Performance Assurance Can Hamper Market Growth

While GCLs offer construction advantages, long-term performance depends on correct design detailing and installation quality. Key challenges include managing hydration control during installation, ensuring adequate confining stress and cover layers, and maintaining overlap integrity at seams and penetrations under field conditions.

In steep-slope and interface-sensitive applications, maintaining stability requires appropriate reinforcement, interface friction management, and design checks. For chemically aggressive environments, demonstrating compatibility and maintaining barrier performance over time adds testing and documentation requirements, increasing project complexity.

Download Free sample to learn more about this report.

Segmentation Analysis

By Application

To know how our report can help streamline your business, Speak to Analyst

The Landfill Segment Dominates the Market Due to the Extensive Use of the Product

By application, the market is categorized into landfill, containment & wastewater treatment, roadways & civil construction, energy, and other sectors.

The landfill segment accounted for the largest geosynthetic clay liner market share in 2025. The segment's growth is driven by the need for engineered bottom liners and final cover systems that meet regulatory performance requirements and provide reliable long-life hydraulic barriers. Geosynthetic clay liners are utilized in base liners, caps, and side slopes of landfills. Environmental protection regulations require the use of liners at municipal, industrial, and hazardous waste sites. The growth of urban areas increases solid waste production, which in turn supports the ongoing construction of landfills. Rehabilitation of older landfill sites also creates a demand for replacements. The high swelling capacity and self-sealing properties of GCLs make them ideal for landfill applications. This segment continues to be the main source of revenue for manufacturers worldwide. Furthermore, the segment held a 38.6% share in 2025.

The containment & wastewater treatment segment is also expected to grow favorably over the projected period. The segment's demand is supported by increasing investments in municipal and industrial water infrastructure. Geosynthetic clay liners are commonly utilized in wastewater treatment plants to prevent seepage and safeguard groundwater resources. Strict environmental regulations require the use of impermeable liners in sludge ponds, lagoons, and treatment basins. Industrial wastewater facilities depend on GCLs to manage chemically aggressive effluents. Key performance requirements include long-term durability and low hydraulic conductivity. The segment is expected to grow at a CAGR of 4.8% over the forecast period.

The roadways & civil construction segment's growth is driven by large-scale infrastructure development. GCLs are utilized for moisture control, slope stabilization, and seepage prevention in highways, tunnels, and embankments.

The energy segment's growth is supported by mining, oil & gas, and renewable energy projects. GCLs are extensively used in tailings storage facilities, evaporation ponds, and containment areas.

Geosynthetic Clay Liner Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Geosynthetic Clay Liner Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 187.5 million, and is expected to maintain its leading share in 2026, valued at USD 197.3 million. The market's growth is driven by rapid urbanization and infrastructure expansion. Large-scale landfill construction and wastewater treatment projects fuel demand. Emerging economies contribute significantly to volume growth. Government investments in environmental protection accelerate adoption. Industrial expansion increases demand for containment systems. Manufacturing scalability improves product affordability. Civil construction projects expand liner applications beyond waste management. Infrastructure modernization remains a key growth driver. Urban population growth increases environmental pressure. Asia Pacific is the fastest-expanding regional market with strong long-term growth prospects.

China Geosynthetic Clay Liner Market

In 2025, the China market reached USD 79.3 million. China’s market demand is driven by massive infrastructure development and urbanization. Rapid industrial growth increases waste generation and the need for containment. Government regulations increasingly enforce environmental protection standards.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is also a significant contributor to the market, with the market estimated to reach USD 113.7 million by 2026. Strict environmental regulations and advanced waste containment standards drive the market’s growth. The region benefits from a well-established landfill and hazardous waste management infrastructure. The U.S. market dominates regional demand due to continuous landfill modernization and remediation projects. Federal and state regulations mandate high-performance liner systems for environmental protection. Transportation infrastructure expansion contributes to steady demand for civil construction.

U.S. Geosynthetic Clay Liner Market

In 2025, the U.S. market reached a valuation of USD 102.6 million. In the U.S., year-to-year demand is anchored in landfill liners and closures, with additional pull from industrial and water containment and selected energy and mining uses.

Europe

Europe is expected to experience significant growth over the coming years. During the forecast period, the European region is projected to grow at a 5.1% rate and reach a valuation of USD 132.0 million in 2026. The regional market is driven by strong environmental protection frameworks and infrastructure renewal initiatives. EU regulations strictly enforce the use of advanced liner systems in landfills and wastewater treatment facilities. Western Europe accounts for the majority of regional demand due to higher regulatory compliance requirements. Sustainable construction and circular economy initiatives support long-term adoption.

U.K. Geosynthetic Clay Liner Market

The U.K. market in 2025 was estimated at around USD 16.2 million, representing approximately 4.5% of global market revenue.

Germany Geosynthetic Clay Liner Market

Germany’s market reached around USD 24.6 million in 2025, equivalent to around 5.6% of global sales.

Latin America

Latin America is experiencing steady growth. The Latin America market in 2026 is expected to reach a valuation of USD 39.2 million. The region is driven by landfill modernization, industrial containment, and selective mining-related applications. Country-level variability is high, depending on local regulations, project pipelines, and access to qualified materials.

The Middle East & Africa

The Middle East & Africa region is gradually expanding, driven by project-based demand in industrial facilities, water infrastructure, and mining and energy containment. Import dependence in several markets elevates the importance of regional distribution and logistics.

GCC Geosynthetic Clay Liner Market

GCC market reached USD 23.4 million in 2025, accounting for approximately 3.9% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Broadening Manufacturing Footprints, Chemical-Compatibility Offerings, and Installation Support to Maintain Their Positions

The market includes multinational geosynthetics groups, specialty containment-focused manufacturers, and regional converters and distributors. Competition is shaped by manufacturing capacity, product construction options (reinforced, film-backed, composite), quality assurance systems, and the ability to support design teams with test data and installation guidance. Some of the key market players include Solmax, Minerals Technologies Inc., Naue GmbH & Co. KG, HUESKER, Terrafix, and Geosynthetics Inc. Large players increasingly position GCLs as part of integrated geobarrier systems that include geomembranes, drainage, and protection layers.

LIST OF KEY GEOSYNTHETIC CLAY LINER COMPANIES PROFILED

- Solmax (Canada)

- Minerals Technologies Inc. (U.S.)

- Naue GmbH & Co. KG (Germany)

- HUESKER(Germany)

- Terrafix Geosynthetics Inc. (Canada)

- Geofabrics Australasia Pty Ltd. (Australia)

- Global Synthetics (Australia)

- Wall Tag Pte Ltd. (Singapore)

- Shanghai Yingfan Engineering Material Co., Ltd. (China)

- Maharshee Geomembrane (India) Pvt. Ltd. (India)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Solmax launched its Performance Materials platform as the next step in integrating the legacy of TenCate Geosynthetics and Propex under Solmax, signaling deeper organizational consolidation and investment capacity behind its broader geosynthetics portfolio (including containment product families).

- September 2024: Solmax supported a landfill-closure project at the Homer Solid Waste Facility in Alaska, deploying about 226,000 ft² (21,000 m²) of landfill closure area using a geosynthetic clay liner alongside drainage and gas systems, highlighting continued landfill-closure demand.

- September 2023: NAUE completed modifications to its Bentofix production plant, enabling the production of coated and higher bentonite-weight products and improving production efficiency for bentonite mat portfolios.

- June 2021: Solmax completed its acquisition of Propex, expanding its manufacturing footprint and product breadth across geosynthetics, supporting stronger global supply capability for containment solutions that include geosynthetic clay liners alongside other barrier system components.

- November 2020: CETCO (Minerals Technologies) introduced the RESISTEX Universal polymer-modified GCL series (line extension) at GeoAmericas 2020, positioning it to address more aggressive leachates (e.g., calcium chloride, coal ash, high-strength mining leachates) and broaden chemical-compatibility coverage for containment projects.

REPORT COVERAGE

The global market analysis provides an in-depth study of the market size and forecast for all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers, and acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Million) Volume (Mn. Sqr. Mtrs.) |

| Segmentation | By Application and Region |

| By Application |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 523.2 million in 2025 and is projected to reach USD 810.9 million by 2034.

Recording a CAGR of 5.1%, the market is slated to exhibit steady growth during the forecast period.

The landfill application segment led in 2025.

Asia Pacific held the highest market share in 2025.

Solmax, Minerals Technologies Inc., Naue GmbH & Co. KG, HUESKER, Terrafix, and Geosynthetics Inc. are some of the prominent players in the market.

Rising investment in engineered containment for municipal/industrial waste, water & wastewater assets, and environmental protection are the key factors driving the market growth.

The major factors expected to favor product adoption include space and cost efficiency, consistent factory-controlled quality, and construction productivity where projects face tight schedules, variable subgrade conditions, or limited access to suitable natural clay.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us