Water Heater Market Size, Share & Industry Analysis, By Technology (Storage (Tank) Water Heaters, Tankless / Instantaneous Water Heaters, Heat Pump Water Heaters, Solar Thermal Water Heaters, and Others) By Capacity (Below 30 L, 30 L - 100 L, 100 L - 250 L, 250 L - 400 L, and Above 400 L), By Energy Source (Electricity, Natural Gas & LPG, Solar Thermal, and Others) By Application (Residential {Single-Family Homes, Multi-Family / Apartments}, Commercial {Hospitality, Healthcare, Education, Food Service and Others} and Industrial) and Regional Forecast, 2026-2034

Water Heater Market Size and Future Outlook

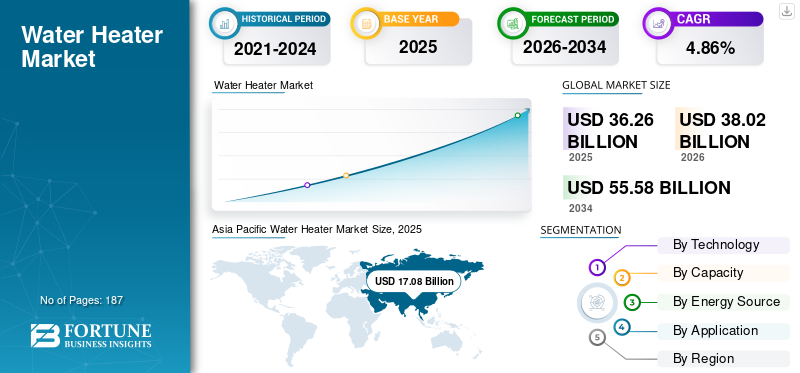

The global water heater market size was valued at USD 36.26 billion in 2025. The market is projected to grow from USD 38.02 billion in 2026 to USD 55.58 billion by 2034, with a CAGR of 4.86% over the forecast period. Asia Pacific dominated the water heater market with a market share of 47.05% in 2025.

Water heaters are appliances designed to heat and store or deliver hot water for residential, commercial, and industrial applications. They supply hot water for everyday uses such as bathing, cleaning, cooking, and space conditioning, using energy sources including electricity, natural gas, Liquefied Petroleum Gas (LPG), solar energy, or heat pump–based systems.

Demand growth in the market is supported by residential construction and renovation activity, replacement cycles in developed markets, and improving living standards and urbanization in emerging economies. A primary structural driver is the ongoing shift toward higher-efficiency and lower-emission technologies, particularly heat pump water heaters and advanced condensing gas units, accelerated by tightening building energy codes, appliance efficiency standards, and decarbonization policies. Electrification trends, rising electricity price volatility, and the integration of smart controls are further influencing adoption, enabling features such as load shifting under time-of-use tariffs, demand response participation, and improved energy management in connected homes. In parallel, product innovation is targeting reduced standby losses, faster heating performance, compact designs for space-constrained installations, and lower total installed cost through simplified installation and modular system designs.

The competitive landscape includes diversified HVAC and water heating OEMs, regional specialists, and fuel- or utility-linked distribution ecosystems, with prominent players such as A. O. Smith, Rheem, Ariston Group, Rinnai, Bosch, and Bradford White competing across premium and mass-market tiers. Competitive strategies increasingly focus on efficiency-led product portfolios, regulatory compliance readiness, channel strength (plumbing contractors, retail, and wholesale distribution), and localized manufacturing to manage costs and respond to regional standards. As the market transitions toward electrified and smart water heating, differentiation is increasingly driven by product reliability, warranty, service networks, compatibility with connected ecosystems, and the ability to meet evolving efficiency and emissions requirements across residential and commercial applications.

Download Free sample to learn more about this report.

Water Heater Market Trends

Grid-Interactive / Demand-Response Ready Water Heaters Are Becoming a Core Differentiator

Grid-interactive (demand-response-ready) water heaters are becoming a key product differentiator as utilities increasingly treat electric storage and heat pump water heaters as dispatchable, flexible load, effectively functioning as thermal batteries. By heating water during low-cost or high-renewable periods and reducing consumption during peak demand, these systems enhance grid stability without affecting customer comfort. This shift is reflected in market specifications, with the Consortium for Energy Efficiency (CEE) referencing AHRI 1430 and requiring automated demand-response capability across all tiers starting January 2026. At the regulatory level, Washington State mandates that electric storage water heaters manufactured on or after January 1, 2023, include a modular demand-response communications port compliant with ANSI/CTA-2045-A. Program initiatives, such as TECH Clean California's HPWH load-shifting pilot, further reinforce grid-interactive adoption. At the same time, mainstream media increasingly describes water heaters as grid-supporting "thermal batteries," highlighting growing consumer and policy awareness.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Building Electrification, Efficiency Regulation, and Incentives Are Structurally Shifting Demand Toward High-Efficiency Water Heating

Building electrification, efficiency regulation, and incentives are structurally shifting demand toward high-efficiency water heating. Water heating is increasingly being pulled into building-decarbonization roadmaps, driving the market away from conventional gas and electric resistance units toward heat pump water heaters (HPWHs) and hybrid technologies. For example, new U.S. DOE efficiency standards are projected to require that most electric storage water heaters use heat pump technology by 2029, delivering about USD 7.6 billion in annual household energy savings and significantly reducing carbon emissions compared with current products.

Moreover, the replacement demand remains a durable baseline driver: water heaters are "must-have" household infrastructure with predictable failure/replacement cycles, and efficiency increasingly shapes purchase decisions as electricity and gas price volatility makes operating cost more salient. The growth in residential construction, renovation activity, and the electrification of household loads is further increasing the need for system upgrades, such as panel enhancements and heat-pump–ready retrofits, creating a pull-through effect for higher-value water-heating solutions.

Market Restraints

Upfront Installed Cost, Retrofit Friction, and Customer Decision Complexity Hampers the Market Growth

Despite strong operating economics in many regions, the biggest adoption limiter, particularly for HPWHs, is still the installed cost and retrofit complexity. Many homes face practical constraints, such as limited space, noise/ventilation considerations, condensate drainage needs, or electrical panel capacity, which raise "soft costs" and extend installation timelines relative to like-for-like tank replacements. These frictions are amplified in price-sensitive customer segments and rental housing, where split incentives (landlord pays capex, tenant benefits from lower bills) can suppress upgrades.

In addition, customer decision-making is often constrained by the "failure replacement" dynamic: when a water heater fails, the buyer prioritizes speed and availability, which favors widely stocked, familiar conventional units over higher-efficiency models that may require additional site work. This dynamic can blunt the near-term impact of incentives unless programs are paired with installer enablement, stocking strategies, and streamlined point-of-sale rebate redemption.

Market Opportunities

Grid-Interactive Water Heaters as Thermal Batteries Creates Growth Opportunities

A major opportunity is emerging from the positioning of water heaters, especially electric tank systems and HPWHs, as grid-flexible thermal batteries. Utilities are increasingly using connectivity standards to shift water-heating load away from peak hours without sacrificing customer comfort. Ecosystems built around CTA-2045/EcoPort enable utilities to send load curtailment or load-up signals, while device logic protects hot-water availability, reducing program risk and improving customer acceptance.

This creates whitespace for manufacturers and platform providers to differentiate through software, controls, telemetry, and "program-ready" product lines, similar to how VPP-readiness is reshaping distributed energy assets. For customers, utility demand-response payments, bill credits, or time-based optimization can improve payback; for grid operators, aggregated flexible water heating can support peak management and renewable integration. Related R&D and deployment efforts also point to more advanced control strategies (e.g., optimized load shifting and thermal storage use cases) becoming commercialized over time. These efforts drive the water heater market growth.

Market Challenges

Policy Uncertainty, Regional Electrification Pathways, and Standards Evolution Create Uneven Demand and Product Transition Risk

While long-term fundamentals are supported by efficiency and decarbonization goals, near-term demand can be disrupted by shifting policy design, changing test methods, and evolving minimum standards. Europe's ongoing work to revise water heater Eco-design and labelling rules illustrates how updates can reshape product portfolios and compliance requirements—benefiting leaders but creating transition costs for laggards.

There is also a technology-transition challenge across regions with different electrification readiness: places with constrained electrical infrastructure, high electricity prices, or colder climates may experience slower HPWH penetration (or continued reliance on gas), creating a fragmented market where manufacturers must manage multiple platforms (gas, electric tank, HPWH, hybrid) simultaneously. Moreover, workforce capacity (installer training), consumer awareness, and supply-chain readiness (components, refrigerants, controls) can become bottlenecks as markets try to scale higher-efficiency systems quickly.

Segmentation Analysis

By Technology

Low Replacement Complexity and Strong Contractor Distribution Drives Storage (Tank) Water Heaters Segment Growth

Based on technology, the market is segmented into storage (tank) water heaters, tankless/instantaneous water heaters, heat pump water heaters, solar thermal water heaters, and others.

Storage (tank) water heaters remains the largest segment globally, as it is the lowest-friction replacement option in most homes and small commercial sites, offers straightforward installation, and spans a broad price range across capacities. This segment is also supported by widespread contractor familiarity and deep retail distribution, especially in replacement-driven markets where "like-for-like" swap-outs dominate demand.

The heat pump water heaters segment is the fastest-growing in many electrification-led markets, supported by tightening efficiency standards, utility rebate programs, and whole-home decarbonization initiatives. HPWHs deliver materially lower energy consumption versus conventional electric resistance storage, making them increasingly attractive where electricity prices are high or incentives reduce upfront cost. The heat pump water heaters segment is expected to grow at a CAGR of 8.90% during the forecast period.

By Capacity

Balanced Capacity, Mass-Market Fit, and Strong Replacement Demand Drives 30-100 L Segment Growth

Based on capacity, the market is segmented into below 30 L, 30–100 L, 100–250 L, 250–400 L, and above 400 L.

The 30-100 L segment dominated with the largest water heater market share. It fits the needs of typical households across apartments and single-family homes, balances purchase price with adequate hot water availability, and dominates replacement cycles in many regions. This capacity band aligns well with mass-market retail SKUs and contractor-driven replacements, making it the most liquid and widely available category.

The 250 L–400 L capacity segment falls in the mid-to-large storage category, positioned between mainstream residential systems and heavy-duty commercial/industrial units. This segment is primarily driven by high-occupancy residential properties, small- to mid-sized commercial facilities, and institutional applications that require higher hot water availability and faster recovery than standard household units. The 250 L – 400 L segment is expected to grow at a CAGR of 5.62% during the forecast period.

By Energy Source

Grid Accessibility and Shift Toward High-Efficiency Electric Systems Drives Electricity Segment Growth

Based on energy source, the market is segmented into electricity, natural gas & LPG, solar thermal, and others.

The electricity segment accounted for the largest share globally due to broad grid availability, ease of installation, and strong presence in emerging markets where piped gas infrastructure is limited. Growth is increasingly driven by the transition to high-efficiency electric platforms, including heat pump water heaters and smart-controlled systems, which can reduce operating costs and support grid-responsive demand.

Solar thermal segment benefits from high solar resources and from institutional/hospitality use cases where hot water is a consistent daily load. Others include niche fuels and localized solutions that are limited in scale but relevant in specific geographies or infrastructure conditions. The solar thermal segment is expected to grow at a CAGR of 7.78% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Residential Segment Dominated the Market Driven by Rising Household Comfort Standards

Based on application, the market is segmented into residential {single-family homes, multi-family/apartments}, commercial {hospitality, healthcare, education, food service, and others}, and industrial.

Residential segment accounts for the largest share globally, driven by the scale of the housing stock and the frequency of replacement cycles. Single-family homes typically drive higher-capacity purchases and premium technology adoption (tankless and heat pump). At the same time, multi-family/apartments favor standardized, energy-efficient systems and contractor-led replacement programs, supporting consistent baseline demand.

The industrial segment accounted for the fastest-growing share owing to increasing demand for reliable hot water across manufacturing, processing, and facility operations where consistent temperature control and high uptime are critical. Industries such as food processing, chemicals, pharmaceuticals, textiles, and metal treatment require continuous hot water supply for cleaning, processing, sterilization, and operational safety, which drives demand for durable and higher-capacity water heating systems. The industrial segment is expected to grow at a CAGR of 5.08% during the forecast period.

Water Heater Market Regional Outlook

By geography, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Water Heater Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the market with a valuation of USD 17.08 billion in 2025, accounting for ~47.11% of global revenues. The region benefits from rapid urbanization, ongoing additions to the housing stock, and expanding access to reliable hot-water systems across emerging markets. Growth is also shaped by a widening product mix, from affordable electric storage systems to instantaneous and heat pump water heaters, along with rising appliance standards and premiumization in higher-income markets.

China Water Heater Market

China’s market was estimated at USD 7.06 billion in 2025 and is set to reach USD 7.40 billion in 2026, supported by a very large installed base, continued demand for residential upgrades, and expansion of the technology mix (including higher-efficiency systems). Replacement cycles plus ongoing product premiumization help sustain market scale.

India Water Heater Market

Indian market was estimated at USD 3.92 billion in 2025 and is expected to reach USD 4.21 billion in 2026, reflecting expanding urban middle-class adoption, improving household penetration of water heaters, and strong demand in multi-family housing. The growth is largely volume-led, with gradual shifts toward higher-capacity, more efficient models in urban markets.

Japan Water Heater Market

The Japanese market was estimated at USD 2.00 billion in 2025 and is likely to reach USD 2.08 billion in 2026, supported by a mature replacement market and continued preference for high-efficiency, high-reliability systems. Replacement-driven demand and premium product adoption remain key stabilizers.

North America

North America was valued at USD 6.97 billion in 2025, accounting for approximately 19.23% of the market. Demand is anchored by a large replacement-driven installed base, strict expectations for reliability and hot-water availability, and steady new housing + retrofit activity. The region is also experiencing a gradual mix shift toward higher-efficiency electric options (including heat pump water heaters), driven by rising efficiency standards, utility rebate programs, and electrification of residential end uses. In commercial buildings, replacement cycles, energy-cost optimization, and compliance upgrades continue to support recurring demand.

U.S. Water Heater Market

The U.S. market was estimated at USD 6.13 billion in 2025 and is set to reach USD 6.40 billion in 2026, supported by the world's largest installed base of residential systems and a highly structured replacement channel (plumbers/contractors, retail, and OEM networks). Growth is increasingly shaped by efficiency upgrades (notably heat pump water heaters in suitable climates and applications), the ongoing shift toward connected/controlled water heating in some utility programs, and steady demand from multifamily and light commercial refurbishments.

Europe

Europe accounted for USD 7.56 billion in 2025, accounting for ~20.84% of global revenues. Electrification policies drive growth, tighten building energy performance regulations, and sustain a push toward efficient technologies (especially heat pump water heaters) across residential and commercial stock. High retail energy price sensitivity in many countries also supports payback-driven upgrades, while the region's mature installer ecosystem accelerates the adoption of replacements and retrofits.

Germany Water Heater Market

Germany’s market was estimated at USD 1.54 billion in 2025 and is set to reach USD 1.63 billion in 2026, supported by strong retrofit intensity, high acceptance of heat-pump-led solutions, and continued investments in building energy efficiency. Replacement demand remains steady, but incremental growth is increasingly tied to high-efficiency electrified upgrades and compliance-led refurbishments.

U.K. Water Heater Market

The U.K. market was valued at USD 1.18 billion in 2025 and is likely to reach USD 1.22 billion in 2026, supported by housing refurbishment cycles, efficiency upgrades, and growing demand in electrification, where system-level heating transitions are underway. Replacement demand remains the backbone, with incremental growth tied to policy-driven improvements and the improving availability of high-efficiency solutions.

Latin America

Latin America accounted for USD 2.89 billion in 2025, representing ~7.96% of the global market. Demand is supported by steady residential replacement, selective new housing activity, and growth in electric water-heating penetration across several markets. Energy affordability and installation simplicity often favor electric solutions, while solar thermal remains a niche but gradually expanding segment in suitable climates.

Brazil Water Heater Market

Brazil’s market was estimated at USD 0.97 billion in 2025 and is expected to reach USD 0.99 billion in 2026, supported by a large addressable residential base and ongoing upgrades/replacements. Market structure continues to favor practical, mass-market solutions, with gradual premiumization in urban centers.

Middle East & Africa

The Middle East & Africa was valued at USD 1.76 billion in 2025, contributing ~4.86% of global revenues. Growth is supported by ongoing construction in parts of the Gulf, steady replacement demand in urban areas, and gradual electrification and appliance adoption across developing markets. Climate conditions also support niche growth in solar thermal in select countries, though overall penetration remains modest.

GCC Water Heater Market

GCC was estimated at USD 0.70 billion in 2025 and is expected to hit USD 0.74 billion in 2026, supported by construction activity, hospitality/commercial demand, and consistent replacement cycles in residential buildings.

KEY INDUSTRY PLAYERS

Key Players Focus on Electrification, Channel Strength, and Grid Connectivity to Gain Market Advantage

The global water heater market is moderately consolidated, with a mix of diversified HVAC majors, dedicated water heating specialists, and regionally strong manufacturers competing across technology platforms (gas storage, electric storage, tankless, and heat pump water heaters), distribution reach, brand trust, and installer relationships. While thermal efficiency, durability, and safety certifications remain baseline requirements, competition is increasingly shifting toward electrification readiness, Heat Pump Water Heater (HPWH) portfolios, refrigerant transition capability, and grid-interactive connectivity.

The channel strategy is becoming a critical competitive dimension. Manufacturers with strong plumbing contractor loyalty, significant big-box retail penetration, and utility-program alignment are better positioned to capture replacement-driven demand, which accounts for the majority of residential volume. In commercial and multi-family segments, lifecycle economics, system redundancy, cascade control, and hybrid integration (tank + heat pump + tankless) are shaping competitive positioning. As a result, market leadership is increasingly tied to portfolio breadth, regulatory foresight, installer enablement, and grid compatibility.

List of Key Water Heater Companies Profiled

- O. Smith Corporation (U.S.)

- Rheem Manufacturing Company (U.S.)

- Ariston Holding N.V. (Italy)

- Rinnai Corporation (Japan)

- Bradford White Corporation (U.S.)

- Bosch Thermotechnology (Germany)

- Haier Inc. (China)

- Navien (South Korea)

- Ferroli S.p.A. (Italy)

- Noritz Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- October 2025: A. O. Smith expanded its U.S. heat pump water heater production capacity, reinforcing its positioning in high-efficiency electric segments ahead of the 2029 DOE compliance timeline and signaling confidence in HPWH-driven replacement demand.

- August 2025: Rheem accelerated the rollout of CTA-2045–enabled, EcoNet-connected water heaters, emphasizing grid-interactive readiness and utility program compatibility as core differentiators.

- June 2025: Ariston strengthened its European heat pump and hybrid water heating portfolio, aligning product development with evolving EU ecodesign revisions and refrigerant transition requirements.

- April 2025: Rinnai expanded high-efficiency condensing and hybrid tankless offerings in North America, targeting premium residential and light-commercial retrofit applications where space optimization and continuous hot water are key decision drivers.

- February 2025: Bosch Thermotechnology advanced low-GWP refrigerant integration across its heat pump water heating systems in Europe, reflecting intensifying competition around sustainability compliance and lifecycle emissions performance.

REPORT COVERAGE

The report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter's Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.86% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Technology

|

|

By Capacity

|

|

|

By Energy Source

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 36.26 billion in 2025 and is projected to reach USD 55.58 billion by 2034.

The market is likely to grow at a CAGR of 4.86% over the forecast period.

By energy source, the electricity segment led the market.

The Asia Pacific market size stood at USD 17.08 billion in 2025.

Building electrification, efficiency regulation, and incentives are the key factors driving the market.

Top players in the market include A.O. Smith, Rheem Manufacturing Company, Rinnai Corporation, and Bosch Thermotechnology.

- 2021-2034

- 2025

- 2021-2024

- 187

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us