Silicones Market Size, Share & Industry Analysis, By Product Type (Elastomers, Fluids, Resins, Emulsions, and Others), By End-Use Industry (Building & Construction, Automotive, Electronics, Personal Care, Industrial Manufacturing, and Others), and Regional Forecast, 2026-2034

Silicone Market Size & Future Outlook

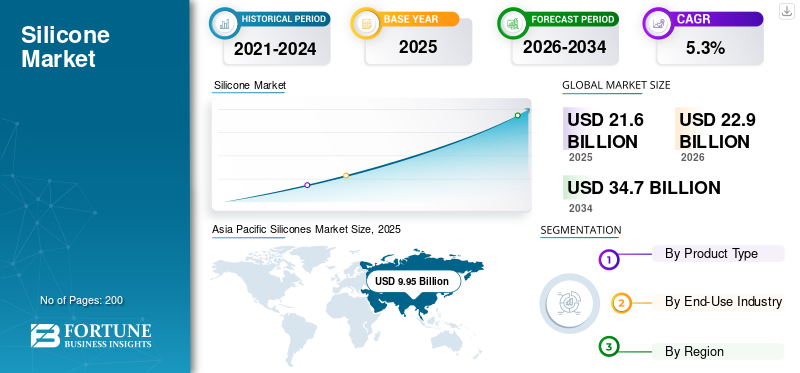

The global silicones market size was valued at USD 21.6 billion in 2025 and is projected to grow from USD 22.9 billion in 2026 to USD 34.7 billion by 2034, exhibiting a CAGR of 5.3% during the forecast period. Asia Pacific dominated the silicones market with a market share of 46.06% in 2025.

The silicones market is experiencing consistent expansion supported by its broad utilization across construction materials, electrical and electronics components, automotive assemblies, healthcare products, personal care formulations, and various industrial applications. Silicones are valued for their durability, flexibility, temperature resistance, and long service life, making them suitable for demanding operating environments. Their ability to maintain performance under extreme heat, cold, moisture, and UV exposure enhances product reliability across end-use sectors. Growing infrastructure activities, rising demand for high-performance consumer goods, and increasing focus on sustainable and energy-efficient solutions are driving the market growth.

Key player participants such as Dow, Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Elkem ASA, and Hoshine Silicon Industry Co., Ltd. strengthen their presence in the silicones market through advanced manufacturing capabilities, integrated value chains, and consistent product performance to meet diverse requirements across industrial, electronics, building and construction, and specialty applications.

Download Free sample to learn more about this report.

SILICONES MARKET Key Takeaways

- 2025 Market Size: USD 21.6 billion

- 2026 Market Size: USD 22.9 billion

- 2034 Forecast Market Size: USD 34.7 billion

- CAGR: 5.3% from 2026–2034

- Asia Pacific dominated the silicones market with a 46.06% share in 2025.

- The fluids segment is projected to expand at a CAGR of 4.6% during the forecast period.

- The automotive segment is expected to grow at a CAGR of 5.7% over the forecast period.

Asia Pacific

Asia Pacific led the global market in 2025 with a valuation of USD 9.95 billion and is expected to maintain its leadership position in 2026, reaching USD 10.63 billion.

North America

North America remained a key regional market, reaching a valuation of USD 4.35 billion in 2025, supported by strong industrial and automotive demand.

Europe

Europe recorded a market value of USD 5.80 billion in 2025 and is expected to witness steady growth driven by expanding manufacturing activities.

U.S.

The U.S. market was valued at USD 3.90 billion in 2025 and accounted for approximately 89.6% of North American revenues, reflecting its strong regional presence.

Japan

Japan continues to be an important market in Asia Pacific, supported by demand from automotive, electronics, and advanced manufacturing industries.

Read More

SILICONES MARKET TRENDS

Rising Demand for High-Performance and Durable Materials Offers a New Market Trend

A key trend in the silicones industry is the growing demand for momentive performance materials that offer durability, flexibility, and long-term stability across diverse applications. End users are increasingly prioritizing materials that can withstand extreme temperatures, moisture, UV exposure, and mechanical stress while maintaining consistent performance. This shift is accelerating the adoption of silicone-based solutions in construction, electronics, automotive, healthcare, and industrial manufacturing sectors. As performance expectations continue to rise, manufacturers are investing in product innovation, formulation improvements, and application-specific solutions to address evolving industry standards and sustainability goals.

Download Free sample to learn more about this report.

- According to Springer Nature research, silicone elastomers are recognized for their high thermal stability, durability, and suitability for demanding environments such as electronics, automotive, and other high-performance applications, due to the strength of their siloxane backbone and resistance to degradation under thermal stress.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Construction and Infrastructure Activities Drive Market Growth

The global silicones market growth is strongly supported by rising construction and infrastructure development across residential, commercial, and industrial sectors. The product is widely used in sealants, adhesives, coatings, and insulation materials due to its durability, weather resistance, and long service life. Their ability to withstand extreme temperatures, moisture, and UV exposure makes them suitable for glazing, structural bonding, and protective applications in modern buildings. In addition, flexibility, ease of application, and compatibility with various substrates enable manufacturers and contractors to enhance building performance, energy efficiency, and long-term maintenance outcomes.

- According to the American Chemistry Council’s Silicon Environmental, Health and Safety Center, building and construction is one of the primary end-use sectors for silicon worldwide, where silicone products such as sealants and coatings are used to protect, strengthen, preserve, and improve the performance of structures, highlighting their key role in modern construction applications.

MARKET RESTRAINTS

Fluctuations in Key Raw Material Prices Restrain Market Stability

The market faces challenges due to fluctuations in the prices of key raw materials, particularly silicon metal and energy inputs required for production. Since silicone manufacturing is energy-intensive and dependent on upstream silicon supply, variations in raw material costs can directly impact production expenses and profit margins. Sudden price swings may create uncertainty for manufacturers and downstream users, affecting long-term procurement planning and contract pricing.

- According to the U.S. Geological Survey (USGS) Mineral Commodity Summaries – Silicon, average U.S. spot market prices for 75%-grade ferrosilicon and silicon metal declined by approximately 50% in 2023 compared with 2022 levels, reflecting significant price volatility in upstream silicon materials.

MARKET OPPORTUNITIES

Growing Adoption in Renewable Energy and Electric Mobility Creates New Opportunities

The market presents strong growth opportunities driven by increasing adoption in renewable energy systems and electric mobility solutions. The products are widely used in solar modules, wind energy components, battery assemblies, and electric vehicle electronics due to their thermal stability, electrical insulation properties, and long-term durability. As global investments in clean energy infrastructure and electrified transportation continue to rise, demand for materials that enhance safety, efficiency, and performance is expanding.

- According to the International Energy Agency (IEA), global electric car sales surpassed 14 million units in 2023, reflecting strong growth in electric mobility. This expansion supports the rising demand for silicone materials used in battery insulation and electronic protection systems.

MARKET CHALLENGES

Environmental Regulations and Sustainability Pressures Create Market Challenges

The market faces challenges related to evolving environmental regulations and increasing sustainability expectations across end-use industries. Regulatory scrutiny on chemical production processes, emissions, and waste management can raise compliance costs and require continuous process optimization. Variations in regional regulations and environmental standards may also affect production planning, product approvals, and cross-border trade, creating additional challenges for consistent global market expansion.

- According to the European Chemicals Agency (ECHA), cyclic siloxanes D4, D5, and D6 are manufactured and used in large volumes in the EU but have been identified as Substances of Very High Concern (SVHC) and are subject to REACH restrictions due to environmental persistence and potential risks.

Segmentation Analysis

By Product Type

Durability, Flexibility, and Wide Industrial Acceptance Support the Dominance of the Silicone Elastomers Segment

Based on product type, the market is segmented into elastomers, fluids, resins, emulsions, and others.

Elastomers hold the largest silicones market share due to their exceptional flexibility, durability, and broad acceptance across multiple end-use industries. These materials provide excellent resistance to extreme temperatures, moisture, UV exposure, and mechanical stress, making them suitable for construction sealants, automotive components, electrical insulation, healthcare products, and industrial applications. Their ability to maintain elasticity over long periods enhances product reliability and service life.

According to Medical Design Briefs, silicone elastomers are widely selected in medical device manufacturing due to their established biocompatibility, durability, chemical inertness, and versatile processing characteristics, including high consistency rubber (HCR) and liquid silicone rubber (LSR) for scalable production.

The fluids segment is expected to grow at a CAGR of 4.6% over the forecast period.

By End-Use Industry

Expanding Infrastructure Development and Demand for Durable Materials Drive Building & Construction Segment Dominance

In terms of end-use industry, the market is categorized into building & construction, automotive, electronics, personal care, industrial manufacturing, and others.

To know how our report can help streamline your business, Speak to Analyst

The building & construction segment holds the largest share of the market, supported by increasing infrastructure development and the need for durable, long-lasting materials. This product is extensively used in sealants, adhesives, waterproofing systems, glazing, and protective coatings due to its ability to withstand extreme weather conditions, temperature variations, and prolonged environmental exposure. Their flexibility and strong adhesion to diverse substrates enhance structural integrity and energy efficiency in residential, commercial, and industrial buildings.

- According to the American Chemistry Council’s Silicon Environmental, Health and Safety Center (SEHSC), silicon is widely used in building and construction applications such as sealants, adhesives, coatings, and insulation materials due to its durability, flexibility, and resistance to weathering. This highlights the strong role of construction activities in driving silicone demand.

The automotive segment is expected to grow at a CAGR of 5.7% over the forecast period.

Silicones Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific held the dominant position in the market in 2025, valued at USD 9.95 billion, and is expected to maintain its leading role in 2026, reaching USD 10.63 billion. The region’s leadership is supported by rapid infrastructure development, strong construction activity, expanding automotive production, and growing electronics manufacturing capacity. Increasing investments in renewable energy, electric mobility, and industrial modernization further contribute to regional demand.

Asia Pacific Silicones Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

China Silicones Market

Based on Asia Pacific’s strong contribution and China’s extensive industrial base, the China market was valued at USD 4.47 billion in 2025, accounting for approximately 44.9% of regional revenues during the forecast period. Strong construction activity, large-scale electronics production, and significant solar and electric vehicle manufacturing drive silicone consumption. China benefits from integrated supply chains, substantial silicones production capacity, and continued investments in advanced manufacturing technologies, supporting steady domestic demand.

To know how our report can help streamline your business, Speak to Analyst

India Silicones Market

The Indian market in 2025 was valued at USD 0.78 billion. Demand is supported by expanding urban infrastructure projects, growth in residential and commercial construction, and rising automotive and electronics manufacturing. Government initiatives focused on domestic manufacturing, infrastructure modernization, and renewable energy expansion are contributing to increasing adoption of silicone-based materials across industrial and construction applications.

North America

North America remains a significant regional market and reached a valuation of USD 4.35 billion in 2025. Demand is supported by strong construction activity, advanced automotive manufacturing, expanding renewable energy installations, and steady growth in electronics production. The region benefits from a mature industrial base, well-established regulatory standards, and leading silicone manufacturers with advanced production capabilities.

U.S. Silicones Market

The U.S. market in 2025 reached a valuation of USD 3.90 billion, accounting for approximately 89.6% of regional revenues. Demand is driven by large-scale infrastructure projects, growth in residential and commercial construction, and increasing adoption of silicone materials in automotive, aerospace, and clean energy applications. The country benefits from integrated supply chains, strong research and development capabilities, and the presence of major global silicone producers that support continuous product innovation and industrial expansion.

Europe

Europe is expected to record steady growth in the market and reached a valuation of USD 5.80 billion in 2025. The region is supported by advanced automotive engineering, established construction standards, and strong demand for high-performance materials in industrial and energy applications. Increasing focus on sustainable construction, electric mobility, and renewable energy systems further strengthens silicon consumption. Strict regulatory frameworks and an emphasis on product quality also encourage the adoption of durable, environmentally compliant silicone solutions across multiple sectors.

Germany Silicones Market

Germany’s market reached a valuation of USD 1.18 billion in 2025, accounting for approximately 20.4% of regional demand. Growth is supported by a strong automotive manufacturing base, advanced industrial machinery production, and expanding renewable energy installations. The country’s emphasis on engineering excellence, energy-efficient buildings, and electric vehicle development drives steady demand for silicone-based materials in structural, insulation, and electronic applications.

Italy Silicones Market

The Italian market in 2025 was valued at USD 0.85 billion, representing roughly 14.6% of regional revenues. Demand is driven by ongoing residential and commercial construction activity, growth in specialty manufacturing, and increasing adoption of durable sealants and coatings. Continued modernization of infrastructure and steady development in industrial production contribute to consistent silicone consumption across building and technical applications.

Latin America, the Middle East, and Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in the market during the forecast period. The Latin America market reached a valuation of USD 0.96 billion in 2025, supported by expanding construction activities, growth in automotive assembly operations, and increasing demand for durable sealants and coatings across major economies. Rising infrastructure investments and gradual industrial development continue to support the adoption of materials across residential and commercial projects. The Middle East & Africa market was valued at USD 0.49 billion in 2025, driven by large-scale infrastructure projects, expansion in energy and utilities sectors, and growing use of high-performance materials in construction and industrial applications.

Brazil Silicones Market

The Brazilian market in 2025 was valued at USD 0.53 billion, accounting for approximately 55.1% of Latin America revenues. Demand is driven by expanding residential and commercial construction, growth in automotive production, and increasing use of durable sealants and adhesives in infrastructure and industrial applications. Ongoing investments in energy, transportation, and urban development projects continue to support steady silicone consumption in the country.

COMPETITIVE LANDSCAPE

Key Industry Players

High Capital Intensity and Strategic Asset Management Shape Competition in the Market

The market for silicones remains moderately consolidated and technologically intensive, as large-scale production requires advanced chemical processing capabilities, integrated supply chains, and strict compliance with environmental and safety regulations, particularly in construction, automotive, electronics, and healthcare industries. High capital investment in manufacturing facilities, quality control systems, product testing, and regulatory approvals, along with long qualification cycles in performance-critical sectors, can create barriers for new entrants.

Leading companies such as Dow, Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Elkem ASA, and Hoshine Silicon Industry Co., Ltd. primarily focus on advancing formulation technologies, strengthening global distribution networks, and improving product consistency and performance to maintain a competitive advantage rather than relying solely on aggressive capacity expansion.

LIST OF KEY SILICONES COMPANIES PROFILED:

- Dow (U.S.)

- Wacker Chemie AG (Germany)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- Elkem ASA (Norway)

- Evonik Industries AG (Germany)

- Hoshine Silicon Industry Co., Ltd. (China)

- DONGYUE GROUP (China)

- Henkel AG & Co. KGaA (Germany)

- CHT Germany GmbH (Germany)

- Siltech Corporation (Canada)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Henkel AG & Co. KGaA entered a joint venture with Wetherby Laroc to accelerate growth in high-performance building and façade systems, reinforcing Henkel’s construction sealants/adhesives positioning where silicone technologies are widely used.

- December 2025: Wacker Chemie AG and its JV partner SICO Performance Material opened a new application development center for organofunctional silanes in Jining, China, strengthening upstream specialty inputs that support silicone/silane-based formulations for adhesives, coatings, and advanced manufacturing.

- October 2025: Siltech Corporation highlighted the launch of Silmer Sustain-H, a bio-based silicone elastomer gel designed to enhance sensorial performance and formulation versatility in personal care applications.

- September 2025: Dow launched DOWSIL EG-4175 Silicone Gel, a new silicone gel product designed for higher-voltage power electronics used in EVs and renewable energy technologies.

- March 2025: Dow reported completion/start-up of its Silicone Expansion Project in Zhangjiagang (China), supporting higher silicone supply capability for electronics and other fast-growing end uses.

- May 2024: Shin-Etsu Chemical Co., Ltd. announced construction of a new silicone products plant in Zhejiang (China) (via a new entity), aimed at expanding capacity and higher-function silicone emulsions.

REPORT COVERAGE

The global market analysis provides an in-depth study of the market size and forecast for all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.3% from 2026-2034 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Product Type, End-Use Industry, and Region |

|

By Product Type |

|

|

By End-Use Industry |

|

|

By Region |

North America (By Product Type, End-Use Industry, and Country)

Europe (By Product Type, End-Use Industry, and Country)

Asia Pacific (By Product Type, End-Use Industry, and Country)

Latin America (By Product Type, End-Use Industry, and Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 21.6 billion in 2025 and is projected to reach USD 34.7 billion by 2034.

Recording a CAGR of 5.3%, the market is slated to exhibit steady growth during the forecast period.

The building & construction end-use industry segment led in 2025.

Asia Pacific held the highest market share in 2025.

Rising demand for durable silicone sealants and adhesives, supported by expanding construction activity and growing use in automotive and electronics, is the key factor driving the silicones market growth.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us