Luxury Vinyl Plank Market Size, Share & Industry Analysis, By Product Type (Rigid and Flexible), By End-Use Industry (Residential, Commercial, and Industrial) And Regional Forecast, 2026-2034

Luxury Vinyl Plank Market Size and Future Outlook

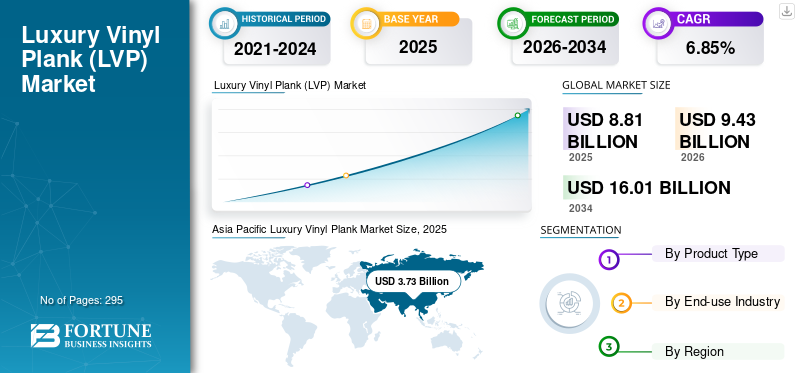

The global luxury vinyl plank market size was valued at USD 8.81 billion in 2025. The market is projected to grow from USD 9.43 billion in 2026 to USD 16.01 billion by 2034, exhibiting a CAGR of 6.85% during the forecast period. Asia Pacific dominated the luxury vinyl plank market with a market share of 42.34% in 2025.

Luxury Vinyl Plank (LVP) is a luxury vinyl flooring product made in plank form (boards) and engineered to replicate hardwood visuals (grain/texture) using a multi-layer construction. Luxury vinyl plank demand is driven mainly by its ability to deliver a realistic wood look in moisture-prone, high-use areas such as kitchens, basements, laundry rooms, and rental homes, where hardwood and many laminates can struggle with durability or warranty performance.

Furthermore, many key industry players, including Mohawk Industries, Shaw Industries, Tarkett SA, Forbo Holdings, and Gerflor Group operating in the market, are focusing on developing innovative products to meet the rising demand.

Download Free sample to learn more about this report.

Luxury Vinyl Plank Market KEY TAKEAWAYS

- 2025 Market Size: USD 8.81 billion

- 2026 Market Size: USD 9.43 billion

- 2034 Forecast Market Size: USD 16.01 billion

- CAGR: 6.85% from 2026–2034

- Asia Pacific dominated the luxury vinyl plank market with a 42.34% share in 2025.

- The Rigid segment captured the largest share in 2025 through strength, waterproofing, and versatility.

- Rising home renovation projects and DIY flooring systems fueled Residential segment growth in 2025.

Asia Pacific

The market was valued at USD 3.73 billion in 2025 and remains the largest and fastest-growing region.

North America

The market maintained a significant position in 2025, supported by strong home renovation activity.

Europe

The market is projected to reach USD 2.04 billion in 2026, growing at a 5.71% CAGR, driven by renovation-led demand.

U.S.

The market is projected to reach USD 2.22 billion in 2026, supported by a large remodeling market.

Japan

The market is projected to reach USD 0.41 billion in 2026.

Read More

Shift Toward Flexible Glue Down Planks is the Latest Market Trend

In commercial interiors of retail, hospitality, healthcare, and education, specifiers prioritize dimensional stability under heat and rolling loads, seam integrity, and serviceability. Glue-down flex LVT is installed as a fully bonded system, which helps reduce movement, minimizes gapping, and performs well with heavy traffic, carts, and frequent cleaning. It also supports selective replacement: a damaged plank/tile can often be swapped without disturbing a floating floor assembly, which is important for keeping downtime low.

In the value tier, flex LVT can be more cost-effective as it often uses simpler constructions and avoids some rigid-core cost adders (thicker cores, attached pads, premium locking systems). For contractors, it can also be more predictable on challenging footprints where flatness can be achieved during prep.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Exceptional Properties of Luxury Vinyl Plank To Boost The Market Growth

Luxury vinyl plank demand is propelled by a clear bundled advantage: wood aesthetics, moisture tolerance, easy installation, and low upkeep, aligned with renovation-led buying cycles.

The primary growth driver for the market is its ability to deliver a hardwood-style aesthetic with superior functional performance, enabling broader adoption across both residential and light commercial interiors. The product’s value proposition is anchored in moisture tolerance, durability, and low maintenance, directly addressing the performance gaps of traditional wood and several laminate offerings, particularly in spill-prone or high-traffic areas.

Demand is further amplified by the ongoing shift toward rigid-core constructions (SPC/WPC) and click-lock installation systems. These formats reduce installation complexity and time, offer improved dimensional stability, and are better suited to common renovation conditions such as uneven subfloors and fast turnaround requirements.

MARKET RESTRAINTS

Rising Price Competition and Complaiance Pressures to Hapmer Market Growth

One of the biggest constraints is intensifying competition that drives commoditization: as more manufacturers, importers, and private-label brands enter the category, many products appear similar to consumers, so purchase decisions often shift to price per square foot rather than brand value. This creates margin pressure through persistent discounting, contractor rebates, and promotional activity. At the same time, retailers and distributors raise channel costs through display requirements, marketing fees, shelf-placement competition, and tougher commercial terms.

When capacity expands faster than demand or imports rise, suppliers may reduce prices to keep inventories moving, pulling down average selling prices and making it harder for premium brands to justify higher price points. At the same time, manufacturers face increasing compliance and reputational risk tied to indoor air quality expectations; meeting low-emission standards, maintaining certifications, and reformulating materials can raise costs and introduce product-transition challenges, and any negative publicity about chemical safety can damage category trust.

MARKET OPPORTUNITIES

Evolving Customer Preferences And Expanding Commercial Construction May Create Lucrative Growth Opportunities

The LVP market presents strong growth opportunities driven by evolving consumer preferences, construction trends, and product innovation. One major opportunity lies in the growing demand for waterproof and low-maintenance flooring products, particularly in residential remodeling. As homeowners increasingly renovate kitchens, bathrooms, and basements, LVP’s moisture resistance and durability position it as a practical alternative to hardwood and laminate. The expanding home improvement and DIY segment further supports luxury vinyl plank market growth, as click-lock luxury vinyl plank systems are installer-friendly and reduce labor costs.

Another significant opportunity exists in the commercial construction sector, including hospitality, healthcare, retail, education, and office spaces. These segments require durable, cost-effective flooring with aesthetic appeal and easy maintenance. The product’s ability to mimic natural wood or stone while offering superior wear resistance and acoustic properties makes it attractive for high-traffic environments. Growth in multi-family housing and rental properties also supports demand, as property owners prioritize cost efficiency and durability.

MARKET CHALLENGES

Ensuring Consistent Quality And Performance Across Project Sites Pose A Critical Challenge To Market Growth

The LVP market faces several practical challenges that can slow growth and compress profitability. Cost volatility in PVC resin, additives, and freight can whipsaw margins and complicate annual pricing, while tariffs or import restrictions can raise landed costs and create supply uncertainty.

Moreover, performance consistency is a persistent challenge: moisture, subfloor flatness, temperature swings, and heavy rolling loads can cause gapping, telegraphing, or joint failure, leading to callbacks and warranty claims that erode brand trust.

Segmentation Analysis

By Product Type

Rigid Segment To Dominate Segmental Growth owing to Wider Application Versatility

Based on product type, the market is segmented into rigid and flexible.

The rigid segment accounted for the largest luxury vinyl plank market share in 2025 due to better dimensional stability, greater impact/indent resistance, and broader application versatility. Rigid products generally provide a more “solid underfoot” feel and offer improved sound reduction. Rigid-core lines are favoured as they reduce callbacks related to subfloor issues and support waterproof positioning, a strong consumer purchase trigger.

Flexible luxury vinyl plank remains relevant due to its lower cost, thinner profile, and suitability for spaces where height/transition constraints matter. It can be more flexible in certain layouts and is often used in budget residential upgrades, rental housing, and price-sensitive renovation jobs.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Residential Segment To Lead Market Due To High Product Demand

Based on the end-use industry, the market is segmented into residential, commercial, and industrial.

Residential segment accounted for the dominant market share in 2025, driven by the exceptional properties of luxury vinyl plank, such as water resistance, scratch/dent tolerance, easy cleaning, and cost effectiveness. Demand is amplified by remodeling and replacement cycles, especially in kitchens, living areas, bedrooms, basements, and increasingly bathrooms, where consumers want “upgrade looks” without high maintenance. The rise of DIY-friendly click-lock systems and faster installation also supports residential growth by lowering labor dependency.

Commercial is the second largest segment expected to grow at a CAGR of 6.6% during the forecast period, driven by high footfall and performance requirements, as well as the need for cost-efficient refurbishment with minimal downtime. Sectors such as retail, hospitality (hotels), offices, education, and healthcare clinics prefer LVP due to its balance of durability, design flexibility, and easier maintenance compared to carpet (stains, hygiene) or hardwood (wear and refinishing). Commercial buyers also value acoustic underlayment options, slip resistance, and modular replacement.

Luxury Vinyl Plank Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Luxury Vinyl Plank Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific reached a valuation of USD 3.73 billion in 2025. It is the fastest-growing and largest market opportunity zone, driven by urbanization, rising middle-class housing demand, and expanding organized retail in flooring. Large-scale residential construction, growing hospitality and retail spaces, and increasing preference for modern interior finishes support product adoption. The region also benefits from manufacturing ecosystems and improving distribution, though price sensitivity and fragmented installer networks influence product positioning.

Japan Luxury Vinyl Plank Market

The Japanese market in 2026 is estimated at around USD 0.41 billion, accounting for roughly 4.4% of global revenues. Japan’s market is driven by renovation and refurbishment, with buyers prioritizing cleanability, moisture tolerance, and quiet/comfort performance in compact urban homes and high-traffic commercial spaces.

China Luxury Vinyl Plank Market

Chinese market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 1.23 billion, representing roughly 13.1% of global sales. China’s market is shaped by a renovation-first demand structure, strong domestic manufacturing depth, and tight price competition, with growth opportunities concentrated in urban households, multi-family upgrades, and selective commercial refurbishment.

India Luxury Vinyl Plank Market

The Indian market in 2026 is estimated at around USD 0.39 billion, accounting for roughly 10.06% of global revenues. India is an emerging, fast-adopting LVP market, with demand primarily tied to urban housing upgrades, organized retail expansion, and commercial fit-outs. Unlike mature markets where replacement dominates, India’s demand is a mix of new interior finishing (especially in apartments) and renovation/retrofit in top cities.

To know how our report can help streamline your business, Speak to Analyst

North America

North America held a significant share in 2025, valued at around USD 0.31 billion. The region remains prominent due to a strong culture of home renovation and replacement flooring, wide penetration of big-box retail and specialty flooring stores, and high acceptance of rigid-core waterproof formats. Demand is supported by single-family remodeling, multi-family upgrades, and commercial refurbishment, while competition is intense, with frequent price promotions and a strong private-label presence.

U.S. Luxury Vinyl Plank Market

The U.S. market can be analytically approximated at around USD 2.22 billion in 2026. The U.S. is one of the most developed and competitive markets, anchored by a large replacement/remodeling base, strong distribution reach, and high consumer acceptance of waterproof rigid-core products. Demand is closely tied to home improvement cycles: even when housing transactions slow, many homeowners choose to renovate rather than move, supporting steady flooring replacement volumes, especially for kitchens, living areas, basements, and multi-family unit turns.

Europe

Europe is projected to grow at 5.71% over the coming years and reach a valuation of USD 2.04 billion by 2026. The regional market growth is driven by renovation-led demand, especially in Western Europe, where luxury vinyl plank benefits from the shift away from carpet and some traditional laminate toward easy-clean, moisture-resistant surfaces. Growth is also supported by multi-family refurbishment and institutional projects, though it is more regulated, with a stronger emphasis on product emissions, sustainability, and compliance certifications, which influence the product mix and cost structures.

U.K. Luxury Vinyl Plank Market

The U.K. market in 2026 is estimated at around USD 0.30 billion, representing roughly 3.2% of global revenues.

Germany Luxury Vinyl Plank Market

Germany’s market is projected to reach approximately USD 0.40 billion in 2026, equivalent to around 4.3% of global sales.

Latin America and the Middle East & Africa

Latin America is a growth-oriented market, supported by residential construction recovery, remodeling activity, and commercial projects in urban centers. Luxury vinyl plank flooring is gaining traction among consumers seeking affordable “premium-look” flooring, but adoption can be constrained by import dependence, currency volatility, and distribution gaps outside major cities.

The Latin America market is set to reach a valuation of USD 0.43 billion in 2026.

Middle East & Africa shows steady potential, driven by hospitality, retail malls, and large infrastructure-linked real estate projects, particularly in GCC markets, as well as emerging residential demand in selected African economies. However, growth is shaped by project-based purchasing, high climate exposure (heat), and reliance on imports, making quality specs, availability, and logistics critical.

The Middle East & Africa is set to reach USD 0.22 billion in 2026.

GCC Luxury Vinyl Plank Market

The GCC market is projected to reach around USD 0.06 billion in 2026, representing roughly 3.49% of global revenues. The GCC market is project-led and refurbishment-heavy, with demand concentrated in Saudi Arabia and the UAE, followed by Qatar, Kuwait, Oman, and Bahrain.

COMPETITIVE LANDSCAPE

Key Industry Players

Premiumization and Innovation To Propel Market Progress

The luxury vinyl plank market is moderately concentrated at the top, with a few large, vertically integrated flooring groups, but highly fragmented in the long tail containing regional brands, private labels, and OEM/ODM suppliers. Competition is shaped by brand pull, channel control, and specification performance. Top brands and larger groups compete by upgrading rigid-core (SPC/WPC), improving locking systems, scratch resistance, acoustics, and realism (embossing/printing). Mohawk Industries, Shaw Industries, Tarkett SA, Forbo Holdings, and Gerflor Group are the largest players in the market.

Other notable players in the global market include Mannington Mills, LG Hausys Ltd, James Halstead Plc, Interface Inc. and others.

LIST OF KEY LUXURY VINYL PLANK COMPANIES PROFILED

- Mohawk Industries (U.S.)

- Shaw Industries Group, Inc. (U.S.)

- Tarkett S.A. (France)

- Interface, Inc. (U.S.)

- Gerflor Group (France)

- Forbo Holding AG – Forbo Flooring Systems (Switzerland)

- Mannington Mills, Inc. (U.S.)

- Karndean Designflooring (U.K.)

- Amtico International Ltd. (U.K.)

- LG Hausys, Ltd. (South Korea)

- James Halstead plc (U.K.)

- IVC Group (Belgium)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Interface, Inc., a global flooring solutions provider recognized for its sustainability leadership, introduced two new global collections: Dressed Lines carpet tile and Lasting Impressions Luxury Vinyl Tile (LVT). Both launches reflect the company’s design-driven approach, combining contemporary aesthetics with reinterpretations of classic styles through advanced patterns, construction techniques, and manufacturing innovations to deliver a cohesive design experience.

- October 2024: Shaw Industries Group, Inc. strengthened its U.S. resilient flooring manufacturing footprint through a USD 90 million investment in Plant RP in Ringgold, Georgia, which produces SPC and LVT flooring. This expansion phase is expected to more than double the plant’s resilient flooring output by 2026.

REPORT COVERAGE

The global market analysis includes a comprehensive study of the market size and forecast across all market segments covered in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers, and acquisitions, and key industry developments, as well as their prevalence by key regions. The global market research report also provides a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.85% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, End-Use Industry, and Region |

| By Product Type |

|

| By End-use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 8.81 billion in 2025 and is projected to reach USD 16.01 billion by 2034.

In 2025, the market value in the Asia Pacific stood at USD 3.73 billion.

The market is expected to grow at a CAGR of 6.85% over the forecast period.

By product type, the rigid segment led the market in 2025.

The rising demand for vinyl flooring solutions due to its expectional properties are the key factors driving the market.

Mohawk Industries, Shaw Industries, Tarkett SA, Forbo Holdings, and Gerflor Group are the major players in the global market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 295

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us