Coal Market Size, Share & Industry Analysis, By Application (Power Generation, Steel Production, Cement, and Others), and Regional Forecast, 2026-2034

COAL MARKET SIZE AND FUTURE OUTLOOK

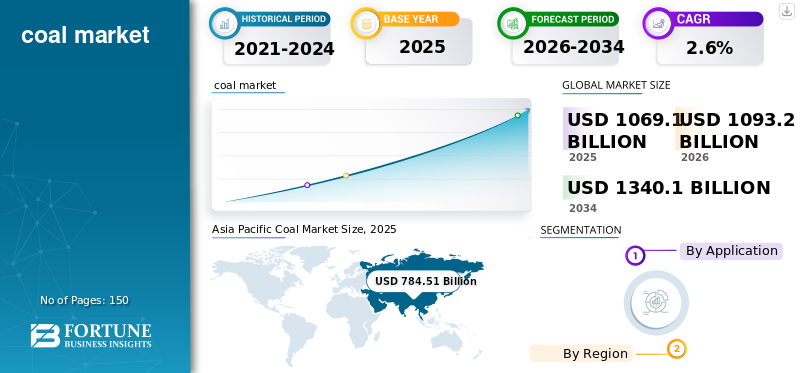

The global coal market size was valued at USD 1,069.1 billion in 2025. The market is projected to grow from USD 1,093.2 billion in 2026 to USD 1,340.1 billion by 2034 at a CAGR of 2.6% during the forecast period. Asia Pacific dominated the coal market with a market share of 69.86% in 2025.

The global coal market remains a structurally significant part of the world’s energy and industrial system, despite accelerating decarbonization efforts. Coal continues to play a central role in electricity generation, particularly in emerging economies where power demand growth and grid reliability needs remain high. At the same time, metallurgical coal remains an essential feedstock for blast furnace-based steelmaking, which continues to account for the majority of global primary steel production.

Market dynamics are increasingly shaped by diverging regional trajectories. While coal consumption is declining structurally in Europe and North America due to plant retirements and tightening emissions regulations, demand remains resilient across the Asia Pacific region, led by China and India. As a result, the market is entering a transitional phase in which coal is simultaneously a declining fuel in mature economies and a critical baseload and industrial input in developing regions, creating a complex global outlook.

China Shenhua Energy Co., Ltd., Coal India Limited, China Coal Energy Co., Ltd., BHP Group, Glencore plc, and Peabody Energy Corporation are the key players operating in the market.

Download Free sample to learn more about this report.

Coal Market Key Takeaways

- 2025 Market Size: USD 1,069.1 billion

- 2026 Market Size: USD 1,093.2 billion

- 2034 Forecast Market Size: USD 1,340.1 billion

- CAGR: 2.6% from 2026–2034

- Asia Pacific dominated the coal market with a 69.86% share in 2025.

- The Power Generation segment accounted for the largest market share.

- The Steel Production segment held a significant share of the global market.

Asia Pacific

Rising electricity demand and industrial expansion continue to support coal consumption.

North America

Coal demand declines gradually amid renewable adoption and power plant retirements.

Europe

Carbon pricing and coal phase-out policies continue to reduce regional consumption.

U.S.

U.S. Market reached USD 91.2 billion in 2025, accounting for 8.5% of global sales.

Japan

Stable demand from power generation and steel manufacturing supports coal consumption.

Read More

COAL MARKET TRENDS

Increasing Divergence Between Asian Markets Boosts Industry Growth

One of the most important trends shaping the coal market is the widening divergence between consumption patterns in Asia Pacific and those in OECD economies. China and India continue to account for the majority of global coal use, while Europe and North America are rapidly reducing their reliance on coal through plant retirements and renewable expansion. This geographic concentration is reshaping coal trade dynamics, pricing benchmarks, and capital investment priorities.

At the same time, coal supply chains are adapting to this structural shift. Exporters are increasingly focused on serving Asian buyers, while domestic production declines in several Western markets. The IEA notes that coal demand growth is flattening, reinforcing Asia’s dominant role in determining market stability and seaborne trade flows.

MARKET DYNAMICS

MARKET DRIVERS

Rising Electricity Demand and Baseload Power Requirements in Emerging Economies Fuel Industry Expansion

Coal continues to be a major pillar of energy security in countries where electricity demand is expanding faster than renewable capacity additions and grid infrastructure upgrades. In large developing markets, coal-fired generation remains one of the few scalable sources of dispatchable baseload power capable of supporting industrial growth, urbanization, and rising household consumption. This dynamic is particularly evident in Asia-Pacific, where coal remains deeply embedded in national power systems due to domestic resource availability, established logistics, and cost competitiveness relative to imported gas.

Even as renewables expand rapidly, coal plants frequently provide critical grid stability during periods of intermittency, supporting peak demand and balancing supply fluctuations. The IEA continues to highlight that coal demand remains structurally high in emerging Asia, where power-sector requirements and industrial electrification needs sustain consumption levels. As a result, coal demand is expected to remain resilient in the near term, especially in markets prioritizing affordability and reliability alongside long-term energy transition goals.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Stricter Air Pollution Standards to Restrict Market Development

A major restraint on the global coal market growth is the tightening policy environment surrounding emissions reduction, particularly in Europe and North America. Governments in these regions are implementing coal phase-out strategies, carbon pricing mechanisms, and stricter air pollution standards, making coal-fired generation increasingly uneconomic compared with renewables and gas. As a result, structural coal demand decline is underway in mature markets, supported by regulatory pressure and investor-driven decarbonization commitments.

In addition, financial institutions and multilateral development banks have significantly reduced funding for new coal projects, limiting capacity additions outside a small number of emerging economies. The Energy Institute’s Statistical Review shows that coal demand is increasingly concentrated in Asia, reflecting a sharp contraction in OECD markets. Over time, this structural restraint is expected to reduce seaborne thermal coal trade growth and accelerate oversupply risks in export-dependent regions.

MARKET OPPORTUNITIES

Emerging Economies with Expanding Infrastructure Boost Market Growth

Despite long-term decarbonization ambitions, metallurgical coal remains a critical opportunity segment within the coal market due to its essential role in blast furnace-based steel production. Primary steelmaking still relies heavily on coke as both a fuel and reducing agent, and large-scale substitution through hydrogen-based routes will require significant time, infrastructure investment, and cost competitiveness. This creates a durable medium-term demand base for high-quality coking coal.

Emerging economies with expanding infrastructure and manufacturing sectors continue to drive steel demand, reinforcing metallurgical coal trade flows. While alternative technologies such as electric arc furnaces are growing, they depend on scrap availability and power costs, limiting their ability to fully displace blast furnace production globally. As a result, metallurgical coal represents a more structurally resilient component of the coal market compared with thermal coal, especially in industrializing regions.

MARKET CHALLENGES

Price Volatility and Uncertainty in Long-Term Investment Signals Hinder Industry Expansion

A key challenge facing the coal market is heightened price volatility driven by geopolitical disruptions, shifting trade policies, and uncertain long-term demand signals. Coal prices have experienced sharp swings in recent years due to supply shocks, export restrictions, and changing procurement strategies among major importers. This volatility creates risk for both producers and consumers, complicating contract structures and investment planning.

In parallel, the global energy transition introduces significant uncertainty around the long-term role of coal, discouraging sustained capital investment in new mining capacity or infrastructure. While demand remains high today, expectations of future decline in many regions can constrain supply responsiveness, leading to cyclical tightness and price spikes. World Bank commodity price data continues to highlight coal’s sensitivity to broader global energy market conditions, reinforcing the persistent volatility challenge for market participants.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade policies and geopolitics influence the global coal market primarily through seaborne trade flows, energy security strategies, and supply-side export restrictions. Coal remains one of the most geopolitically sensitive commodities, as major importers such as China, India, Japan, and parts of Europe rely on international supply chains for thermal and metallurgical coal. Export controls, sanctions, freight disruptions, and shifting bilateral trade relationships can materially affect benchmark pricing and availability.

On the other side, geopolitical uncertainty has encouraged import diversification and domestic production prioritization, particularly in Asia. Several countries are increasingly emphasizing long-term supply contracts, strategic stockpiling, and regional sourcing to reduce exposure to global price volatility. As a result, the coal trade is becoming more fragmented, with supply security and reliability gaining importance alongside cost competitiveness in utility and steel-sector procurement decisions.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D activity in the coal market is increasingly focused on technologies that reduce emissions intensity, improve combustion efficiency, and enhance coal utilization in industrial systems. Key developments include upgrades to ultra-supercritical power plants, advanced particulate and sulfur control systems, and digital monitoring tools that optimize fuel burn rates and reduce operational losses in coal-fired generation.

These innovations aim to improve coke efficiency and lower blast furnace carbon intensity through higher-quality coal blending, alternative injectants, and process optimization. While coal mining itself is mature, producers are also investing in automation, methane management, and productivity-enhancing extraction technologies to remain competitive amid tightening environmental and financial constraints.

SEGMENTATION ANALYSIS

By Application

Power Generation Lead Due to Coal’s Continued Role as a Scalable Baseload Fuel

Based on application, the market is segmented into power generation, steel production, cement, and others.

The power generation segment dominates the global coal market due to coal’s continued role as a scalable baseload fuel in emerging economies. In Asia Pacific, coal-fired power remains central to grid stability and industrial electrification, particularly where renewable intermittency and limited gas infrastructure constrain alternatives. The segment continues to represent the largest share of global coal consumption despite a structural decline in OECD markets.

The steel production segment holds a significant share, driven by metallurgical (coking) coal demand in blast furnace-based steelmaking. Primary steel production remains heavily dependent on coke as a reducing agent, making metallurgical coal one of the most structurally resilient coal applications over the medium term, especially in infrastructure-led economies.

The cement segment accounts for a smaller but stable share, as coal remains an important kiln fuel in many developing markets. However, substitution by waste-derived fuels and biomass in mature regions is gradually limiting coal intensity in cement manufacturing.

The others segment includes industrial boilers, chemicals, brick manufacturing, and residual residential heating uses. This segment is declining slowly in several regions due to electrification and clean fuel adoption, but remains relevant in parts of Asia and Africa.

To know how our report can help streamline your business, Speak to Analyst

COAL MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific Coal Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia Pacific accounted for the leading coal market share in 2025. Growth is driven by electricity demand growth, industrial expansion, and continued reliance on coal for power generation in China and India. The region remains the center of global coal consumption, with China alone representing more than half of global demand. Despite gradual policy tightening, coal remains structurally embedded in Asia’s power and steel systems.

China Coal Market

China’s market is one of the largest worldwide, with 2025 revenue at USD 536.1 billion, representing roughly 50.1% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America’s coal market is largely replacement- and decline-driven, shaped by coal plant retirements, renewable penetration, and regulatory constraints. The U.S. remains the dominant coal consumer in the region, but demand continues to contract structurally due to power-sector transition trends.

U.S. Coal Market

In 2025, the U.S. represents USD 91.2 billion market in the region, driven primarily by strong demand from the industrial sectors, and accounts for roughly 8.5% of global market sales.

Europe

Europe’s market is characterized by accelerated phase-out policies, carbon pricing pressure, and declining coal-fired generation. While countries such as Germany and Poland still maintain coal consumption, the region overall is in structural decline, with demand increasingly concentrated in a few industrial and legacy power applications.

Germany Coal Market

The Germany market in 2025 reached around USD 24.6 billion, representing roughly 2.3% of global market revenues.

Turkey Coal Market

Turkey market in 2025 reached around USD 13.8 billion, representing roughly 1.3% of global market revenues.

Latin America

Latin America represents a smaller but stable coal market, with demand concentrated in industrial applications and limited coal-based power generation. Brazil and Mexico contribute modest shares, while Colombia remains more significant as an exporter than a consumer.

Brazil Coal Market

Brazil market in 2025 reached around USD 6.3 billion, representing roughly 0.6% of global market revenues.

Middle East & Africa

Demand in the Middle East & Africa is influenced by South Africa’s coal-dependent power system and selective growth pockets linked to industrialization and energy security needs. GCC countries remain minor coal consumers, but regional imports are increasing in niche industrial and power applications.

GCC Coal Market

The GCC market in 2025 stood at USD 5.7 billion, representing roughly 0.5% of global market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Focus on Sustainability to Reduce Environmental Footprint

Major investments are underway in the market as manufacturers respond to rising sustainability expectations and higher performance requirements across end-use industries. Leading producers, such as China Shenhua Energy Co., Ltd., Coal India Limited, China Coal Energy Co., Ltd., BHP Group, Glencore plc, Peabody Energy Corporation, are directing capital toward process optimization, product quality enhancement, and environmentally aligned manufacturing practices. Innovation efforts are increasingly focused on enhancing purity consistency, reducing the environmental footprint, and developing grades suitable for advanced products.

LIST OF KEY COAL COMPANIES PROFILED IN THE REPORT:

- China Shenhua Energy Co., Ltd. (China)

- Coal India Limited (India)

- China Coal Energy Co., Ltd. (China)

- BHP Group (Australia)

- Glencore plc (Switzerland)

- Peabody Energy Corporation (U.S.)

- Adaro Energy Indonesia (Indonesia)

- PT Bumi Resources Tbk (Indonesia)

- Sasol Limited (South Africa)

- Exxaro Resources (South Africa)

KEY INDUSTRY DEVELOPMENTS:

- April 2024 - Coal India announced plans to scale production beyond 1 billion tons annually through new mine commissioning and brownfield expansions. The move supports India’s energy security strategy, as coal continues to account for the majority of the country’s electricity generation. Capacity expansion is also aimed at reducing import dependency, particularly for thermal coal.

- October 2023 - BHP Group reaffirmed the strategic importance of its Queensland metallurgical coal assets. The company continues optimizing high-margin steelmaking coal production to align with long-term infrastructure-driven steel demand in Asia. This reflects a shift toward premium met coal exposure rather than thermal coal dependence.

- August 2023 - Glencore confirmed the acquisition of Teck Resources’ steelmaking coal business, significantly strengthening its position in the global market. The acquisition enhances long-life reserves and export capacity, particularly into Asian steel markets. It also consolidates Glencore’s role as a leading diversified commodities supplier.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies and applications. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors contributing to market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTES | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion), Volume (Million Ton) |

| Growth Rate | CAGR of 2.6% from 2026 to 2034 |

| Segmentation |

By Application

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 1,069.1 billion in 2025 and is projected to reach USD 1,340.1 billion by 2034.

Recording a CAGR of 2.6%, the market is slated to exhibit steady growth during the forecast period (2026-2034).

The power generation segment led the market by application in 2025.

Asia Pacific held the highest market share in 2025.

Rising electricity demand and baseload power requirements in emerging economies are key factors driving market growth.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us