Ceramic Matrix Composites Market Size, Share & Industry Analysis, By Matrix Type (Silicon Carbide, Oxide, Carbon, and Others), By Application (Aerospace & Defense, Energy & Power, Automotive, and Others), and Regional Forecast, 2026-2034

Ceramic Matrix Composites Market Size and Future Outlook

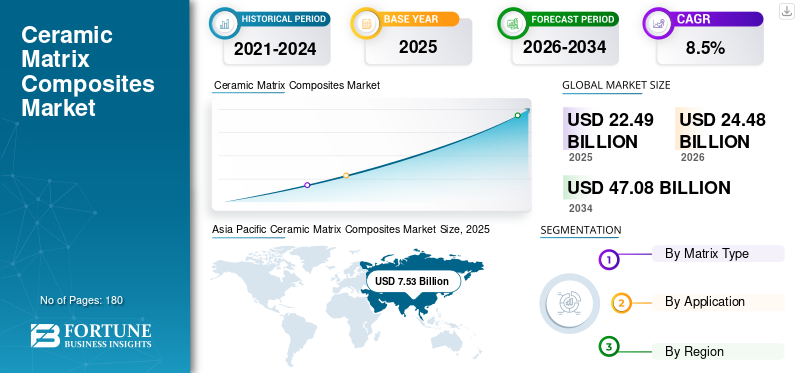

The global ceramic matrix composites market size was valued at USD 22.49 billion in 2025. The market is projected to grow from USD 24.48 billion in 2026 to USD 47.08 billion by 2034, exhibiting a CAGR of 8.5% during the forecast period. Asia Pacific dominated the ceramic matrix composites market with a market share of 36.06% in 2025.

Ceramic Matrix Composites (CMCs) are advanced materials composed of ceramic fibers bonded to a ceramic matrix. They are valued for their ability to withstand very high temperatures, their light weight, and their resistance to wear and oxidation. Demand is mainly driven by the aerospace and defense sectors, especially for jet engine and hot-section parts, where lower weight and greater heat tolerance enhance fuel efficiency and part life. Smaller but growing demand also comes from industrial equipment used in high-temperature environments. Overall, the market grows through targeted OEM programs and the gradual replacement of metal alloys in extreme conditions, rather than through rapid, broad-based volume expansion.

The market is dominated by a small group of vertically integrated, technology-driven manufacturers with specialized fiber and composite processing capabilities and long qualification histories with OEMs. Major players such as Rolls-Royce, CoorsTek Inc., KYOCERA Corporation, Axiom Materials, and Ultramet focus on high-temperature component manufacturing, tight quality control, and certified supply chains, resulting in a moderately consolidated market characterized by program-led demand, high switching costs, long approval cycles, and capacity that is tightly managed around aerospace and defense platforms.

Download Free sample to learn more about this report.

Ceramic Matrix Composites MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 22.49 billion

- 2026 Market Size: USD 24.48 billion

- 2034 Forecast Market Size: USD 47.08 billion

- CAGR: 8.5% from 2026–2034

- Asia Pacific dominated the ceramic matrix composites market with a 36.06% share in 2025.

- The oxide providers segment is expected to account for 20.2% of the market in 2025.

- The aerospace & defense segment held the largest market share in 2025.

North American

North America recorded a market value of USD 7.61 billion in 2025, supported by strong aerospace and defense demand.

Europe

Europe reached USD 4.72 billion in 2025, driven by established aerospace programs and advanced manufacturing.

Asia Pacific

Asia Pacific led the market with USD 8.11 billion in 2025 and is projected to reach USD 8.84 billion in 2026.

U.S.

The market was valued at USD 6.65 billion in 2025, driven by aerospace and defense applications.

Japan

Demand is supported by expanding aerospace manufacturing and increasing adoption of advanced high-temperature materials.

Read More

CERAMIC MATRIX COMPOSITES MARKET TRENDS:

Scale-Up of SiC Fibers and Protective Coatings Is Reshaping the Market

A notable trend in the market is the effort to scale up Silicon Carbide (SiC) fiber supply and to improve Environmental Barrier Coatings (EBCs) that protect CMC parts in hot, corrosive engine conditions. This shift is happening as these two elements strongly influence CMC cost, quality consistency, and lifetime performance. From a business perspective, companies are investing in more scalable fiber production and more durable coating systems to produce CMC components more reliably and use them in more demanding engine environments, thereby supporting the ceramic matrix composites market growth.

- According to the U.S. Department of Energy’s National Energy Technology Laboratory (NETL), DOE is funding a project with a total award value of USD 1,002,188 (DOE share USD 799,674) to develop SiC fiber/SiC ceramic matrix composites for hydrogen turbine hot-section applications at 2,700°F, reflecting active government-backed work to scale and improve next-gen CMC systems.

MARKET DYNAMICS

MARKET DRIVERS:

Rising Adoption of Lightweight, High-Temperature Materials in Aerospace Sustains Demand

Ceramic matrix composites demand is primarily driven by the increasing need for lightweight materials that can operate reliably at extreme temperatures in aerospace and defense applications. Jet engines and aircraft systems are steadily shifting toward higher efficiency and hotter operating conditions, where CMCs provide clear advantages over metal alloys by reducing weight while maintaining strength and oxidation resistance. This adoption creates a direct demand-side pull for CMC components in engine hot sections, exhaust parts, and thermal protection applications, as every new engine platform win or component conversion to CMC translates into sustained, long-cycle consumption tied to production rates and aftermarket replacements.

- According to the U.S. Federal Aviation Administration (FAA)’s 2025–2045 Aerospace Forecast, U.S. carrier domestic passenger traffic is projected to grow by an average of 2.4% per year over the next 20 years, supporting sustained aircraft and engine activity that underpins demand for advanced high-temperature materials such as CMCs.

Download Free sample to learn more about this report.

MARKET RESTRAINTS:

High Dependence on Aerospace and Defense Program Cycles Restraints Market Growth

Ceramic matrix composites' demand is constrained by their heavy reliance on aerospace and defense platforms, where procurement and production rates can fluctuate with airline profitability, aircraft order timing, engine program delays, or shifts in defense budgets. Any slowdown in aircraft deliveries or deferral of engine ramp-ups can quickly reduce near-term demand for CMC components, since volumes are concentrated in a limited set of qualified applications. Unlike conventional engineering materials, which have broader end-use diversification, CMC consumption is tightly linked to a small number of OEM-approved programs and long production cycles, making demand more exposed to program timing changes and macroeconomic uncertainty.

- According to the U.S. Department of Transportation’s Bureau of Transportation Statistics (BTS), U.S. and foreign airlines serving the U.S. carried 398 million systemwide scheduled-service passengers in 2020, down 62% from 2019, demonstrating how quickly airline cycles can drop and disrupt aerospace-linked demand.

MARKET OPPORTUNITIES:

Industrial Gas Turbines and High-Temperature Equipment Are Creating Growth Opportunities

The material demand is poised to benefit as industrial users increasingly seek materials that can operate reliably at extreme temperatures, improving uptime and reducing maintenance frequency. In industrial gas turbines and other high-temperature equipment, CMCs can withstand higher operating temperatures and exhibit greater resistance to oxidation and thermal fatigue than many metal alloys. As power and industrial operators focus more on efficiency and lifecycle performance, adoption of CMC components in these non-aerospace systems can create incremental, structurally attractive demand beyond the core aircraft engine market.

- According to the U.S. Energy Information Administration (EIA), U.S. natural gas-fired power plants generated 1,767 billion kWh of electricity in 2024, presenting the large operating base of gas-turbine-linked generation where higher-efficiency hot-section materials (such as CMCs) can create incremental adoption opportunities.

MARKET CHALLENGES:

Complex Manufacturing and Strict Qualification Requirements Make CMC Supply Hard to Scale

CMC producers face a significant challenge due to complex manufacturing and stringent aerospace quality standards, which make costs and delivery timelines hard to predict. Steps such as fiber layup, densification/infiltration, protective coating application, and precision machining require tight process control, and even minor defects can lead to rework or scrap. In addition, OEM approval and inspection requirements are lengthy, so suppliers cannot quickly change materials, processes, or sources to improve cost or capacity. This combination limits how fast supply can scale, keeps unit costs high, and increases the risk of delays as CMC use expands into more engine components.

- According to NASA’s Glenn Research Center (through NASA Technical Reports Server), NASA has developed SiC/SiC ceramic matrix composites for turbine engine applications at 2,700°F, highlighting the demanding performance targets that drive long testing and qualification cycles for CMC components.

Segmentation Analysis

By Matrix Type

High-Temperature Aerospace Demand Drives Dominance of Silicon Carbide Segment

Based on matrix type, the market is segmented into silicon carbide, oxide, carbon, and others.

To know how our report can help streamline your business, Speak to Analyst

The Silicon Carbide (SiC) segment held a dominant ceramic matrix composites market share in 2025. SiC-based CMCs lead consumption as they offer the better combination of high-temperature strength, low density, and oxidation resistance needed in critical aerospace and defense components, especially in engine hot sections and exhaust hardware. Demand for these parts is performance-driven rather than discretionary, since reducing weight and withstanding higher operating temperatures directly supports fuel efficiency and component life. As aircraft engines continue to push higher thermal stability and OEMs expand CMC use in certified platforms, SiC matrix composites remain the most structurally anchored and highest-value matrix type in the market.

The oxide matrix type is expected to register the CAGR of 8.0% over the forecast period, supported by its growing use in industrial high-temperature equipment and aircraft components that prioritize oxidation resistance, durability, and cost-effective manufacturability compared with SiC-based CMCs.

By Application

Aerospace & Defense Segment Dominates Due to Extreme Temperature and Lightweight Engine Requirements

By application, the market is segmented into aerospace & defense, energy & power, automotive, and others.

The aerospace & defense segment accounted for the largest market share in 2025. CMCs deliver a rare combination of high-temperature capability, low weight, and oxidation resistance, which is critical for jet-engine hot-section and exhaust components as well as thermal-protection parts. As aircraft and engine programs continue to prioritize fuel efficiency, higher operating temperatures, and longer component life, CMCs are increasingly specified where metal alloys face performance limits. This creates a performance- and qualification-driven demand base that supports stable consumption of CMC components over long production cycles and aftermarket replacement needs.

- According to the U.S. Department of Defense (DoD) FY 2025 Budget Estimates (Aircraft Procurement, Air Force), the 2025 request for Aircraft Procurement is USD 19.84 billion, highlighting the scale of aerospace procurement that anchors demand for advanced engine and thermal materials such as CMCs.

The energy & power segment is expected to grow at a CAGR of 8.0% over the forecast period.

Ceramic Matrix Composites Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Ceramic Matrix Composites Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant position in 2025, valued at USD 8.11 billion, and is expected to retain its leading role in 2026, reaching USD 8.84 billion. The region’s leadership is driven by its expanding aerospace manufacturing ecosystem, growing aircraft production and maintenance activity, and increasing investments in advanced materials and high-temperature component capabilities across key countries. Robust demand from commercial aviation supply chains, defense modernization programs, and industrial high-temperature applications supports sustained product consumption, particularly as regional OEMs and tier suppliers work to localize critical materials and strengthen certified production capacity.

China Ceramic Matrix Composites Market

Based on Asia Pacific’s significant impact and China’s growing aerospace manufacturing footprint, the China market was valued at USD 2.51 billion in 2025, accounting for approximately 30.91% of global revenues. Demand is supported by rising aero-engine and aircraft component programs, increasing MRO activity, and investments in high-temperature materials and certified supply chains. Early adoption in industrial turbines and thermal equipment also adds incremental CMC consumption.

India Ceramic Matrix Composites Market

The India market in 2025 was estimated at around USD 1.28 billion. Growth is supported by rising aerospace and defense manufacturing, aircraft utilization and MRO needs, and increasing investment in advanced materials. Gradual strengthening of domestic supply chains for composites and ceramics supports incremental CMC demand.

North America

North America remains a significant regional market, with a valuation of USD 7.61 billion in 2025. Demand is anchored by a strong aerospace and defense base, supporting steady consumption of CMC components in jet engine hot sections, exhaust systems, and thermal protection applications. The region benefits from major engine OEMs, mature composite and ceramics manufacturing capabilities, and well-established qualification and aftermarket support networks.

U.S. Ceramic Matrix Composites Market

The U.S. market in 2025 reached a valuation of USD 6.65 billion, representing approximately 87.39% of global revenues. Consumption is driven by aerospace and defense use of CMCs in jet engine hot sections, exhaust components, and thermal protection parts, supported by production and aftermarket demand.

Europe

Europe is projected to record modest growth over the forecast period, with the region valued at USD 4.72 billion in 2025. It is characterized by strong aerospace programs, strict certification requirements, and high manufacturing and energy costs that can pressure production economics. Despite these constraints, continued demand from jet engine and aircraft supply chains, defense modernization, and select industrial high-temperature applications support steady consumption of CMS across key countries.

Germany Ceramic Matrix Composites Market

Germany’s market reached approximately USD 1.05 billion in 2025, equal to around 22.25% of the global market. Demand is supported by strong aerospace and advanced manufacturing capabilities, participation in European aircraft and engine supply chains, and select industrial high-temperature applications that require lightweight, heat-resistant components.

U.K. Ceramic Matrix Composites Market

The U.K. market in 2025 was valued at USD 0.81 billion, accounting for roughly 17.06% of global revenues. Consumption is concentrated in aerospace and defense, especially in aircraft and jet engine supply chains that use high-temperature, lightweight CMC components, with limited high-heat industrial applications.

Latin America, the Middle East, and Africa

Latin America and the Middle East & Africa are expected to witness moderate growth over the forecast period. Latin America reached USD 0.80 billion in 2025, supported by the gradual expansion of aircraft maintenance activity, investments in manufacturing, and the rising use of high-temperature components in energy applications. In the Middle East & Africa, demand is driven by energy and power generation infrastructure projects, gas-turbine service requirements, and early adoption of heat-resistant materials for refining and heavy industry. With few qualified local suppliers, most demand is met through imports, keeping volumes small. The Middle East & Africa market reached a valuation of USD 1.24 billion in 2025.

GCC Ceramic Matrix Composites Market

The GCC market accounted for around USD 0.61 billion in 2025, representing approximately 49.01% of regional revenues. Demand is supported by gas-turbine power generation, refining and petrochemical operations, and growing aviation MRO hubs, driving incremental need for heat-resistant CMC components.

COMPETITIVE LANDSCAPE

Key Industry Players:

Substantial Capital Intensity and Strategic Asset Management Drives Market Competition

The ceramic matrix composites market is relatively consolidated and technology intensive, as complex manufacturing processes, high investment requirements, and strict qualification and certification standards create significant barriers to entry. These factors limit new participation and concentrate supply among a small group of established manufacturers with integrated capabilities and proven process expertise.

Key players such as Rolls-Royce, CoorsTek Inc., KYOCERA Corporation, Axiom Materials, and Ultramet focus primarily on scaling qualified production, improving yield and quality consistency, and strengthening long-term OEM programs rather than pursuing aggressive broad-based capacity expansion. Recent activities across these companies highlight a strategic emphasis on operational discipline, cost competitiveness, and incremental improvements in process and coating to support long-term market positioning.

LIST OF KEY CERAMIC MATRIX COMPOSITES COMPANIES PROFILED:

- Rolls-Royce (U.K.)

- CFCCARBON CO, LTD (China)

- CoorsTek Inc. (U.S.)

- Morgan Advanced Materials plc (U.K.)

- Mitsubishi Chemical Group Corporation (Japan)

- KYOCERA Corporation (Japan)

- Starfire Systems, Inc (SSI) (U.S.)

- Axiom Materials (U.S.)

- Ultramet (U.S.)

- Semicorex Advanced Material Technology Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS:

- September 2025: KYOCERA and Kyoto Fusioneering signed a joint development agreement to co‑create advanced ceramic materials for fusion-energy plants, explicitly including silicon carbide composite materials, strengthening the innovation pipeline for high‑temperature CMC‑class components in extreme environments.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including market shares and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

Attribute |

Details |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.5% from 2026-2034 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Matrix Type, Application, and Region |

|

By Matrix Type |

|

|

By Application |

|

|

By Geography |

North America (By Matrix Type, Application, and Country)

Europe (By Matrix Type, Application, and Country)

Asia Pacific (By Matrix Type, Application, and Country)

Latin America (By Matrix Type, Application, and Country)

Middle East & Africa (By Matrix Type, Application, and Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 22.49 billion in 2025 and is projected to reach USD 47.08 billion by 2034.

Recording a CAGR of 8.5%, the market is slated to exhibit steady growth during the forecast period.

By application, the aerospace & defense segment led the market in 2025.

Asia Pacific held the highest market share in 2025.

Rising adoption of CMCs in aerospace and defense engines to enable higher-temperature operation, weight reduction, and better fuel efficiency are the key factors driving the market growth.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us