Crude Oil Market Size, Share & Industry Analysis, By Type (Light Crude Oil, Medium Crude Oil, and Heavy Crude Oil), By End Use (Transportation Fuels, Petrochemicals, Industrial Use, and Power Generation), and Regional Forecast, 2026-2034

Crude Oil Market Size and Future Outlook

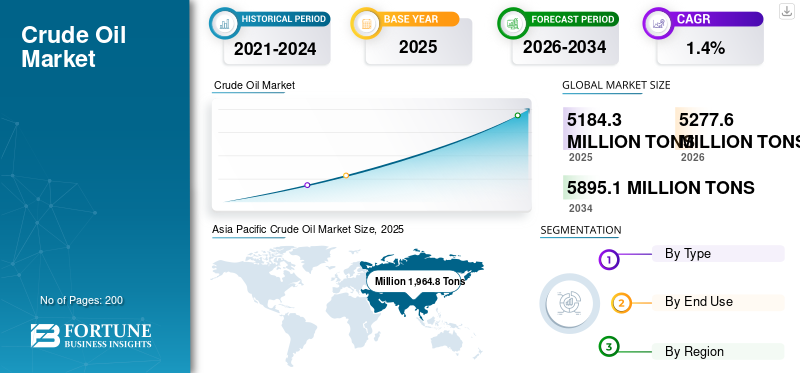

The crude oil market size was valued at 5,184.3 million tons in 2025. The market is projected to grow from 5,277.6 million tons in 2026 to 5,895.1 million tons by 2034, exhibiting a CAGR of 1.4% during the forecast period. Asia Pacific dominated the crude oil market with a market share of 37.9% in 2025.

Crude oil is a naturally occurring liquid mixture of hydrocarbons found in underground rock formations and extracted through drilling. It is unrefined petroleum in its raw form and may vary widely in color, density, sulfur content, and chemical composition depending on the source field. It contains a combination of paraffins, naphthenes, aromatics, sulfur compounds, nitrogen compounds, trace metals, and other impurities. After extraction, it is processed in refineries to produce fuels and petrochemical feedstocks, including gasoline, diesel, jet fuel, LPG, naphtha, lubricants, asphalt, and other industrial materials. Crude oil is commonly classified as light, medium, or heavy, and as sweet or sour, based on its density and sulfur level, as these characteristics influence refining complexity, product yield, and commercial value.

The market growth is driven by rising production levels, reserves, geopolitical developments, the Organization of the Petroleum Exporting Countries (OPEC+) policy decisions, refinery demand, inventory movements, and global economic activity. It is also influenced by benchmark crude streams such as Brent, WTI, and Dubai/Oman, which serve as pricing references for physical trade.

Furthermore, the competitive landscape is led by national oil companies and integrated international majors with strong reserve access, upstream scale, refining linkages, and trading capabilities. aramco, Exxon Mobil Corporation, Chevron Corporation, Shell, and bp p.l.c. remain among the most influential participants due to their resource positions, offshore and unconventional exposure, capital discipline, and ability to balance upstream production with downstream optionality.

Download Free sample to learn more about this report.

Crude Oil Market Key Takeaways

- 2025 Market Size: 5,184.3 million tons

- 2026 Market Size: 5,277.6 million tons

- 2034 Forecast Market Size: 5,895.1 million tons

- CAGR: 1.4% from 2026-2034

- Asia Pacific dominated the crude oil market with a 37.9% share in 2025.

- The light crude oil segment accounted for the largest share of 42.6% in 2025.

- The transportation fuels segment held the leading share of 52.2% in 2025.

Asia Pacific

Asia Pacific maintained its leading position with a market volume of 1,964.8 million tons in 2025.

North America

North America remained a significant market, reaching 1,187.2 million tons in 2025.

Europe

Europe reached 969.5 million tons in 2025 and is projected to grow at a CAGR of 1.2% during the forecast period.

U.S.

The crude oil market is estimated to reach 995.8 million tons in 2026.

Japan

The market is estimated to reach 220.2 million tons in 2026, accounting for around 1.4% of global volume.

Read More

CRUDE OIL MARKET TRENDS

Supply Discipline and Non-OPEC Growth are Significant Market Trends

One of the most visible market trend is the increasing divergence between tightly managed OPEC+ supply and resilient non-OPEC growth from the U.S., Canada, Brazil, and Guyana. The market is no longer expanding through a uniform global production cycle. However, market balances are increasingly shaped by a combination of voluntary producer restraint in the Middle East and selective project-led growth in deepwater and unconventional basins. This has made the market more segmented by basin economics, project cycle time, and export flexibility.

At the same time, demand growth is becoming less transportation-centric than in earlier cycles. Jet fuel recovery, refinery runs, and petrochemical feedstocks remain supportive, but official outlooks increasingly highlight petrochemical demand, emerging-market industrialization, and evolving product mix as the main areas sustaining long-term oil use. As a result, the market is being influenced not only by headline production volumes, but also by crude quality compatibility, refinery configuration, trade-route diversification, and the strategic role of spare capacity.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Transportation Fuels, Petrochemical Feedstock, and Energy Security Priorities Drives Market Growth

The primary driver for crude oil market growth is the need for transportation fuels across road freight, aviation, marine bunkers, and mobility systems that remain difficult to replace at scale in the near term. Even where transport electrification is progressing, heavy-duty, aviation, and international logistics still require large hydrocarbon input streams. This preserves a substantial structural role for crude oil in refinery systems and in global trade balances.

An additional layer of support comes from petrochemical feedstocks, strategic stock policies, and energy-security considerations. Many importing countries continue to emphasize supply diversification and reserve buffers, while producer countries maintain long-cycle investment programs to protect export revenues and fiscal stability. This combination sustains crude production capacity even when price conditions fluctuate.

MARKET RESTRAINTS

Producer Restraint, Capital Discipline, and Transition Pressures Restricts Market Expansion

OPEC+ management of supply, voluntary cuts, and quota-linked policy adjustments can constrain immediate volume expansion even in periods of stronger demand. This is especially relevant when inventories are elevated or when exporters prioritize price stability over aggressive production growth.

The market also faces investment friction due to energy-transition policies, greater financing selectivity, and more rigorous environmental scrutiny. New oil projects often require long lead times, complex permitting, and larger commercial justification. As a result, not every reserve base translates into near-term marketable supply, especially in higher-cost or carbon-intensive regions.

MARKET OPPORTUNITIES

Deepwater, Unconventional, and Recovery-Optimization Pathways Are Expanding Recoverable Supply

One of the strongest opportunities lies in highly productive basins where infrastructure, geology, and execution capabilities continue to unlock incremental barrels. The Permian Basin, Canadian Oil Sands debottlenecking, Brazil’s pre-salt developments, Guyana’s offshore growth, and selective Middle Eastern capacity additions all illustrate how targeted upstream investment can add supply without relying on broad-based expansion globally.

There is also a notable opportunity in enhanced recovery, digital field optimization, and efficiency-led brownfield expansion. Producers that can improve recovery factors, lower lifting costs, and better match crude quality to refinery demand captures higher market share even in a slower-growth global environment. These advantages are particularly important in mature basins where value creation depends more on optimization than on frontier exploration alone.

MARKET CHALLENGES

Geopolitical Risk, Price Volatility, and Long Project Cycles Can Hamper Market Growth

The market remains exposed to geopolitical disruptions, sanctions, shipping constraints, and sudden changes in policy or security conditions. As crude oil flows are globally traded and benchmark-sensitive, even localized disruptions can quickly alter supply expectations, freight economics, and regional price differentials. This makes volume planning and revenue visibility more difficult for both exporters and refiners.

Another challenge is that many crude projects still require complex infrastructure and multi-year investment cycles. Offshore developments, oil sands projects, and capacity expansions often involve higher capital intensity and longer payback horizons than short-cycle production. Combined with volatile benchmark prices, this raises execution risk and can slow the translation of resource potential into market.

Segmentation Analysis

By Type

Light Crude Oil Segment Dominates Due to Growing Preference for Lighter Barrels by Refiners

Based on type, the market is segmented into light crude oil, medium crude oil, and heavy crude oil.

The light crude oil segment accounted for the largest crude oil market share in 2025. The segment’s growth is driven by the scale of the U.S. tight oil and North Sea production, and many refiners' preference for lighter barrels with easier processing characteristics. Light grades benefit from strong export flexibility, favorable refinery yields for transport fuels, and lower complexity requirements in some refining systems. Furthermore, the segment accounted for a 42.6% share in 2025.

The medium crude oil segment remains highly significant as most of the Middle Eastern supply base is concentrated in medium-grade streams that anchor international benchmark trade and long-haul exports to Asia.

Heavy crude oil also holds a significant share, supported by Canada, South America, and select Middle Eastern systems, but its growth is more closely tied to complex refining capacity and discount-driven trade flows. The segment is projected to grow at a 1.2% CAGR during the study period.

By End Use

To know how our report can help streamline your business, Speak to Analyst

Transportation Fuels Segment Dominates Due to Extensive Use of Product in Diesel, Gasoline and Jet Fuel

By end use, the market is categorized into transportation fuels, petrochemicals, industrial use, and power generation.

The transportation fuels segment accounted for the largest share in 2025, as crude oil remains the primary upstream input for gasoline, diesel, jet fuel, and marine fuels. Despite the gradual rise of electrification in passenger mobility, liquid fuels still dominate freight, aviation, and large parts of emerging-market transport systems. Furthermore, the segment achieved a 52.2% share in 2025.

The petrochemicals segment is also expected to grow favorably over the projected period. The segment’s demand is supported by continued naphtha, LPG, and other hydrocarbon feedstock demand in plastics, intermediates, and industrial chemicals.

Power generation remains the smallest segment globally, while industrial use retains a visible role through fuel oils, process energy, and feedstock-linked industrial applications in regions where oil continues to support industrial and backup energy systems. The segment is expected to grow at a CAGR of 1.4% over the forecast period.

Crude Oil Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Crude Oil Market Size, 2025 (Million Tons)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2024, valued at 1,919.3 million tons, and also maintained its leading share in 2025, valued at 1,964.8 million tons. The region is smaller on a production basis than on a consumption basis, but it remains strategically important as it combines sizeable domestic output in China and India with the world’s largest refining and demand base.

China Crude Oil Market

China remains the region’s largest domestic production center. In 2026, the Chinese market is estimated at around 1,115.8 million tons. The growth is reinforced by national energy-security priorities, continued upstream investment, and the country’s central role in both refining and petrochemical demand.

To know how our report can help streamline your business, Speak to Analyst

Japan Crude Oil Market

The Japan market in 2026 is estimated at around 220.2 million tons, accounting for roughly 1.4% of global volume.

India Crude Oil Market

The India market in 2026 is estimated at around 375.0 million tons, accounting for roughly 1.6% of global volume.

North America

North America is also a significant contributor to the market and reached 1,187.2 million tons by 2025. The market’s growth is driven by project flexibility, basin productivity, and established pipeline, refining, and export infrastructure, although it remains sensitive to benchmark spreads, drilling economics, and capital discipline.

U.S. Crude Oil Market

In 2026, the U.S. market is estimated to reach 995.8 million tons. The country’s position is underpinned by tight oil growth in the Permian, export flexibility, and the ability to respond relatively quickly to market signals.

Europe

Europe is expected to experience significant growth in the coming years. During the forecast period, the European region is projected to grow at a CAGR of 1.2% and reached a valuation of 969.5 million tons in 2025. The regional position is anchored by Germany and the U.K., while most of the wider regional market remains mature and structurally exposed to the decline of legacy basins, decarbonization pressures, and import dependence.

U.K. Crude Oil Market

The U.K. market in 2026 is estimated at around 178.2 million tons, representing approximately 0.5% of global market volume.

Germany Crude Oil Market

Germany’s market is projected to reach approximately 281.9 million tons in 2026, accounting for about 1.9% of global sales.

South America

South America is experiencing steady growth. The South America market in 2025 reached a valuation of 321.4 million tons. Brazil supports the region through pre-salt expansion, while Mexico, Guyana, Argentina, Colombia, Ecuador, and others contribute to a broader and increasingly diversified regional supply base.

Brazil Crude Oil Market

Brazil’s market reached approximately 173.4 million tons in 2026, accounting for about 0.6% of global sales.

The Middle East & Africa

The Middle East & Africa region is expected to experience significant growth. The region continues to lead due to the concentration of low-cost reserves, high reserve-to-production depth, and strong export-oriented capacity across the Gulf. Spare capacity, integrated export infrastructure, and the strategic influence of national oil companies further reinforce the region’s position in global supply balances.

Saudi Arabia Crude Oil Market

Saudi Arabia is expected to reach 288.7 million tons by 2026, accounting for approximately 1.2% of global volume.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Expanding Production Footprints and Specialty Grades to Maintain Their Positions in Market

The global market is concentrated around a mix of national oil companies and large integrated international producers. Competitive advantage is determined by reserve quality, lifting cost, fiscal resilience, midstream and export access, refining integration, and trading strength. Producers that can balance stable upstream output with downstream optionality and strong capital discipline are best positioned to protect margins through volatile cycles.

Aramco, ADNOC, and other Middle Eastern companies maintain influence through low-cost positions in conventional resources and strategic spare capacity. International companies such as Aramco, Exxon Mobil Corporation, Chevron Corporation, Shell, and bp p.l.c. differentiate themselves through offshore execution, depth of unconventional resources, marketing reach, and disciplined portfolio allocation. The next stage of competition is likely to center on capital efficiency, project quality, carbon-management strategy, and the ability to supply the right crude grades to the right refinery systems.

LIST OF KEY CRUDE OIL COMPANIES PROFILED

- Aramco (Saudi Arabia)

- Exxon Mobil Corporation (U.S.)

- Chevron Corporation (U.S.)

- Shell (U.K.)

- bp p.l.c. (U.K.)

- Petrobras (Brazil)

- ADNOC (UAE)

- ConocoPhillips (U.S.)

- Equinor ASA (Norway)

- Vedanta Limited (India)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Eight OPEC+ countries decided to implement a 206,000 barrels per day production adjustment for May 2026, drawn from the 1.65 million barrels per day of additional voluntary cuts announced earlier, showing continued month-by-month calibration of supply to support market stability.

- August 2025: ExxonMobil started production at Yellowtail, Guyana’s fourth offshore development, bringing the country’s total installed capacity to above 900,000 barrels per day and adding a new 250,000 barrels per day deepwater crude project ahead of schedule.

- October 2024: Petrobras started production from the Marechal Duque de Caxias (Mero 3) FPSO in Brazil’s Santos Basin pre-salt, with a capacity of up to 180,000 barrels of oil per day, increasing Mero’s installed capacity to 590,000 barrels per day and supporting Latin American offshore crude growth.

- November 2023: ExxonMobil started production at Payara, Guyana’s third offshore development, lifting total installed capacity in Guyana to about 620,000 barrels per day and adding another large deepwater source of light crude to the global market.

- February 2022: ExxonMobil started production at Liza Phase 2 in Guyana, bringing total installed capacity in the country to more than 340,000 barrels per day, reinforcing Guyana’s emergence as a fast-growing non-OPEC crude supplier.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 1.4% from 2026 to 2034 |

| Unit | Volume (Million Ton) |

| Segmentation | By Type, End Use, and Region |

| By Type |

|

| By End Use |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights estimates that the global market size was 5,184.3 million tons in 2025 and is projected to reach 5,895.1 million tons by 2034.

The market is expected to record a CAGR of 1.4% during the forecast period.

The transportation fuels end-use segment leads the market.

Asia Pacific held the highest share of the market.

Aramco, Exxon Mobil Corporation, Chevron Corporation, Shell, and bp p.l.c. are some of the top players in the market.

The key factor driving market growth is the rising global energy demand, particularly from transportation, industry, and developing economies.

The major factors expected to favor product adoption are the expanding demand for transport fuels, petrochemical feedstock requirements, industrial energy needs, and the continued reliance on crude-derived fuels.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us