Caps & Closures Market Size, Share & Industry Analysis, By Material (Plastic, Metal, and Others), By Product Type (Tethered Caps, Push/Pull Caps, Screw Caps, and Others), By End Use Industry (Food & Beverages, Pharmaceutical, Consumer Goods, Personal Care & Cosmetics, and Others), and Regional Forecasts, 2026-2034

Last Updated: May 18, 2026

| Format: PDF

| Report ID:

FBI102542

Thank you for your interest in the

"United States Medical Devices Market!"

To receive a sample report, please provide the following details:

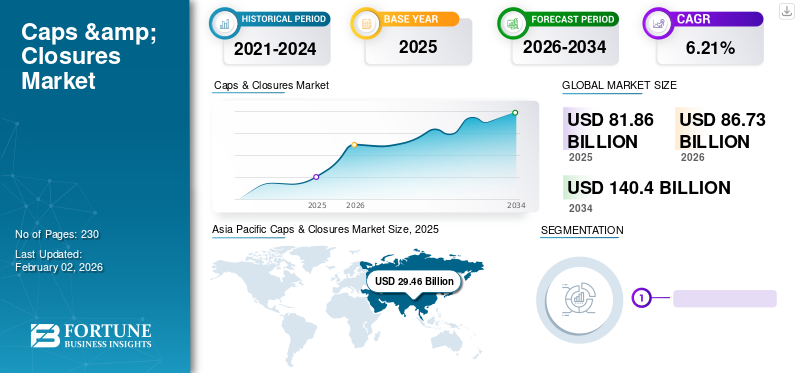

The caps & closures market size was valued at USD 81.86 billion in 2025 and is projected to grow from USD 86.73 billion in 2026 to USD 140.40 billion by 2034, exhibiting a CAGR of 6.21% during the forecast period. Asia Pacific dominated the caps & closures market with a market share of 35.99% in 2025. Moreover, the caps & closures market in the U.S. is projected to grow significantly, reaching an estimated value of USD 17.91 billion by 2032, driven by the properties such as lightweight and durability offered by manufacturers.

Caps & closures are the components that are used to seal and secure containers such as bottles, jars, and tubes. They are designed to provide a tight and secure seal to protect the contents of the container from air, moisture, and other contaminants. Caps & closures come in a wide range of shapes and sizes. Depending upon requirements and applications, they can be made from plastic, metal, rubber, cork, or other materials. They are an essential packaging component for many industries, including food & beverage, pharmaceutical, cosmetics, and household products. Caps & closures improve the product's shelf life, helping brands maintain product quality and value in the marketplace. The global market is driven by the increasing demand for convenience packaging solutions and sustainable packaging options. Plastic caps and closures are the most commonly used type due to their ease of use, durability, and cost-effectiveness. The rising sustainability trend will offer lucrative opportunities for the growth of the market over the forecast period.

The market was negatively affected by the COVID-19 pandemic. The demand for caps & closures decreased due to the closure of retail stores. The end-use industries, such as food & beverage and personal care witnessed a reduction in sales. However, the increasing demand for innovative and creative packaging solutions after the ease of lockdowns is creating lucrative opportunities for the market.

Asia Pacific dominated the caps & closures market with a 35.99% share in 2025, driven by rising demand for convenient, lightweight, and sustainable packaging solutions across food & beverage and personal care industries in China, India, and Southeast Asia.

By material, plastic held the largest market share in 2023, owing to its affordability, chemical resistance, and adaptability across various closure types and end-use industries.

Key Country Highlights:

United States: The caps & closures market in the U.S. is projected to reach USD 17.91 billion by 2032, driven by growing demand for lightweight and durable packaging components in food, beverages, and healthcare sectors.

China: Rapid industrial growth and expansion in the beverage, personal care, and pharmaceutical sectors support high consumption of plastic caps and screw closures.

India: Accelerated urbanization and demand for packaged food products are increasing the need for customizable and cost-effective closures.

Germany: Strong regulatory focus on sustainable materials and increased use of recyclable closures in cosmetics and consumer goods contribute to market expansion.

Brazil: Growing beverage consumption and rising investments in modern packaging formats are boosting cap and closure usage.

GCC Countries: Personal care and food industries are key demand drivers for advanced cap types like tethered and screw closures due to increasing hygiene awareness and regional manufacturing expansion.

Caps & Closures MarketTrends

Utilization of Biodegradable or Recyclable Plastics and Growing Sustainability Trend

The rising concerns regarding environmental hazards have led to an increasing focus on sustainable and eco-friendly packaging solutions. The market is positively influenced by a growing focus on sustainability, with manufacturers exploring eco-friendly materials and designs to align with consumer preferences. Bio-degradable caps and closures, for example, are made from materials that break down naturally in the environment, such as plant-based plastics or biodegradable polymers. They can be composted or recycled after use, reducing their effect on the environment. On the other hand, recyclable caps and closures are made from recyclable materials such as aluminum or PET plastics. They can be recycled with other household or industrial waste. Overall, sustainable caps and closures offer a range of benefits, including reduced environmental impact, improved brand image, and increased customer loyalty. As sustainability continues to be a key driver in this market, manufacturers are investing in sustainable materials and developing new solutions to meet the growing demand for sustainable packaging. Asia Pacific witnessed a growth from USD 22.44 billion in 2022 to USD 25.95 billion in 2023.

Surge in Demand for Packaged Food & Beverages with Growing Urbanization Drives Market Growth

Rising demand for caps and closures is closely linked with growing urbanization. Urban consumers are inclined more towards convenient and on-the-go packaging solutions for food or beverage products. Caps and closures play a key role in providing convenience, ensuring the products are easy to open and close, and can be consumed without spillage. Caps and closures offer an airtight seal, preventing the entry of bacteria and keeping the product fresh for a longer time. They address the growing concern about safety and hygiene associated with food & beverage products by preventing spoilage. With a focus on food safety and hygiene, and an increasing demand for packaged goods, the caps & closures market is expected to experience robust growth. Manufacturers also offer various customization alternatives more suitable for the product, which helps retain their customers, thus boosting their market globally.

Properties such as Lightweight and Durability to Increase Demand Boosting Market Growth

Lightweight caps and closures offer a range of benefits to consumers and manufacturers, which has led to increased demand and adoption in the market. Plastic closures offer manufacturers a versatile solution suitable for various industries. Their ease of use, lightweight nature, customizability, and compatibility with diverse product types contribute to their widespread adoption. They use fewer resources and generate less waste making them eco-friendlier than conventional caps and closures. This is particularly important for companies looking to reduce their carbon footprint and minimize their environmental impact. In addition to the environmental concerns, lightweight caps and closures are more cost-effective than traditional options. They use fewer materials and are less expensive to produce and transport, which can significantly reduce manufacturers' costs and is thus anticipated to drive this market in the upcoming years.

RESTRAINING FACTORS

Availability of Alternative Packaging Solutions to Hinder Market Growth

Flexible packaging alternatives like pouches, blisters, and others offer several benefits such as flexibility, lightweight, and cost-effectiveness that might be more attractive to some consumers. These flexible packaging solutions can provide unique branding, such as shaped pouches and blisters with custom graphics helping brands stand out and improve brand recognition. Rigid packaging solutions cost more to produce and transport than flexible packaging solutions. The time-and-effort-consuming process of designing customized products compared to alternative packaging solutions is the key factor that hampers the growth of the global market.

Caps & Closures Market Segmentation Analysis

By Material Analysis

Plastic Dominates Owing to the Varied Features Offered by the Material

Based on the material, the market is segmented into plastic, metal, and others. Plastic by material holds the highest share of the global market contributing 62.97% globally in 2026. Plastic caps and closures are typically less expensive than other materials such as glass, wood, or rubber. Due to their chemical stability, plastic caps and closures are perfect for storing chemicals. Plastic caps and closures can be customized with various shapes, colors, and designs.

By Product Type Analysis

Screw Caps Dominate Owing to the Convenient Packaging & Protection Offered

Based on the product type, the market share is broken down into tethered caps, push/pull caps, screw caps, and others. The tethered caps segment will account for 40.89% market share in 2026. Screw caps is the dominating segment. The significant factor driving the segment's growth is the convenience, child-resistant, and high sealing capability the screw caps offer. Screw caps can be used for various products and container types, including bottles, jars, and tubes. This versatility makes them popular for manufacturers who produce multiple products with different packaging needs.

By End Use Industry Analysis

To know how our report can help streamline your business, Speak to Analyst

Food & Beverages Leads the Market Share Due to the Widespread Usage of Caps & Closures in the Food Industry

On the basis of the end-use industry, the market share is divided into food & beverages, pharmaceutical, consumer goods, personal care & cosmetics, and others. Food & beverages are the dominating segments. Changing lifestyle trends and increasing demand for processed food contribute to the growth. The use of customized packaging on beverages packaging products containing wine, alcohol, water, soda, and many others is increasing rapidly. The increasing inclination towards such beverages aids the segment's growth. Caps and closures improve brand awareness and sales for food and beverages, thus leading to the segment's rapid growth.

The food & beverages segment is expected to hold a 33.52% share in 2026.

REGIONAL INSIGHTS

Asia Pacific Caps & Closures Market Size, 2025 (USD Billion)

The market is analyzed for manufacturers across North America, Asia Pacific, Europe, the Middle East and Africa, and Latin America. Asia Pacific is the dominating region of the market. The increasing population and number of SMEs for customized packaging enhance the market growth of Asia Pacific. The surge in demand from the cosmetic industry boosts regional market growth in Europe. The rapid shift in consumer lifestyles and rising disposable income that has increased demand for carbonated drinks, alcoholic beverages, and many others fosters growth in the European region.

Asia Pacific

Asia Pacific dominated the market with a valuation of USD 29.46 billion in 2025 and is projected to reach USD 31.5 billion in 2026, underpinned by its large population base and rapidly expanding manufacturing ecosystem. The region benefits from a growing number of small and medium-sized enterprises focused on customized and cost-efficient packaging solutions, which enhances overall market penetration. Regulatory frameworks vary widely across countries but are increasingly aligning with global standards for food safety and packaging quality, supporting long-term market formalization. Demand growth is driven by urbanization, rising consumption of packaged foods and beverages, and expanding personal care and pharmaceutical sectors, positioning Asia Pacific as both a high-volume production hub and a major consumption market. The Japan market is projected to reach USD 6.22 billion by 2026, the China market is projected to reach USD 10.26 billion by 2026, and the India market is projected to reach USD 7.88 billion by 2026.

North America

The North America region captured 19.83% of the global market in 2025, generating USD 16.24 billion in revenue, and is projected to reach USD 17.11 billion in 2026. North America represents a mature and technologically advanced caps & closures market, accounting for a substantial share of global demand. The region’s strong market position is supported by the presence of leading manufacturers, a well-established processed food and beverage industry, and a robust healthcare packaging ecosystem. Regulatory oversight is stringent, with a strong emphasis on food contact safety, tamper evidence, recyclability, and compliance with sustainability mandates, which continues to drive material innovation and lightweighting initiatives. Demand trends are shaped by convenience packaging, extended shelf-life requirements, and steady consumption of packaged foods, pharmaceuticals, and ready-to-drink beverages. The U.S. remains the dominant country in the region, holding the largest share of the global caps & closures market, supported by continuous product innovation and high-value packaging applications. The U.S. market is projected to reach USD 13.61 billion by 2026.

Europe

Europe maintained a strong presence in the global market, reaching USD 23.35 billion in 2025, accounting for 28.52% share, and is expected to reach USD 24.77 billion in 2026. Europe holds a significant position in the global caps & closures market, characterized by high regulatory rigor and strong adoption of sustainable packaging solutions. The regulatory landscape is defined by comprehensive environmental directives, circular economy targets, and recycling content requirements, prompting manufacturers to invest in mono-material designs and eco-friendly closure systems. Market demand is strongly influenced by the cosmetic and personal care industries, where premium packaging aesthetics and functional performance are critical. Additionally, the region’s evolving consumer lifestyles and rising disposable incomes have increased consumption of carbonated drinks, alcoholic beverages, and other packaged beverages, further supporting market growth across both rigid and specialty closure formats. The UK market is projected to reach USD 4.11 billion by 2026, while the Germany market is projected to reach USD 7.2 billion by 2026.

Latin America

The Latin America market generated USD 8.29 billion in 2025, representing 10.12% of the global market landscape, and is expected to reach USD 8.65 billion in 2026. Latin America represents a steadily growing caps & closures market, supported by the gradual expansion of the food and beverage industry across the region. Regulatory requirements are evolving, with increasing attention to packaging safety and quality standards, although enforcement remains less uniform compared to developed regions. Market demand is primarily volume-driven, with growing consumption of bottled beverages, dairy products, and processed foods contributing to consistent uptake of plastic and metal closures. While pricing sensitivity remains a key factor, manufacturers are increasingly focusing on functional improvements and cost-optimized designs to address regional demand patterns.

Middle East & Africa

Middle East & Africa recorded a market size of USD 4.54 billion in 2025, capturing 5.54% of the global market share, and is projected to reach USD 4.7 billion in 2026. The Middle East & Africa caps & closures market is projected to grow at a moderate pace, reflecting a developing but improving packaging landscape. Regulatory structures differ significantly across countries, with gradual progress toward standardized food safety and packaging regulations, particularly in Gulf Cooperation Council economies. Market demand is being supported by rising consumption of personal care and cosmetics products, alongside growing packaged food and beverage penetration in urban centers. Although overall market volumes remain lower than in other regions, increasing brand presence and improving retail infrastructure are expected to sustain incremental demand for reliable and visually differentiated closure solutions.

List of Key Companies in Caps & Closures Market

Leading Players Bound to Witness Robust Growth Opportunities

The global market is highly competitive and fragmented. The few large firms who dominate the market in terms of market share provide cutting-edge packaging for the packaging sector. These dominant market businesses never stop concentrating on growing their regional consumer bases, innovating, and raising market revenue.

BERICAP Holding GmbH, Guala Closures S.p.A, Closure Systems International, Inc., Amcor Plc, Silgan Holdings Inc., Aptar Group, and others are significant market participants. Delivering cutting-edge packaging solutions is the primary goal of a large number of additional industry participants.

July 2022 - Guala Closures, a global leading producer of closures for spirits, wines, beverages and oil bottles acquired Labrenta. The acquisition took place to strengthen Guala Closure's presence in the luxury segment.

January 2023 - Aptar Pharma, part of AptarGroup, Inc., launched APF Futurity™, its first metal-free and highly recyclable, multidose nasal spray pump developed to deliver nasal saline and other comparable over-the-counter (OTC) formulations.

March 2023 - UNITED CAPS Launched 23 H-PAK, a new cap for carton packaging. The company's latest innovation 23 H-PAK is tethered to outstanding value and performance instead of expensive line changes.

February 2023 - BerryGlobal launched fully accredited child-resistant PET bottle combination for the pharmaceutical syrup market. The new Berry Healthcare bundle features seven ranges of 28mm neck PET bottles in sizes from 20ml to 1,000ml and a variety of designs, with eight accompanying closures that incorporate tamper-evident and child-resistant features.

October2021 - Silgan Holdings has acquired Easytech Closures S.p.A. which manufactures and sells easy-open and sanitary metal ends used with metal containers primarily for food applications in Europe.

REPORT COVERAGE

An Infographic Representation of Caps & Closures Market

The report provides detailed market analysis and focuses on key aspects such as leading companies, competition landscape, marketing strategy, product/service types, porters five forces analysis, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the above factors, the report encompasses several factors that contributed to the market's growth in recent years.

REPORT SCOPE AND SEGMENTATION

ATTRIBUTE

DETAILS

Study Period

2021-2034

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2034

Historical Period

2021-2024

Growth Rate

CAGR of 6.21% from 2026-2034

Unit

Value (USD Billion) & Volume (Billion Units)

Segmentation

By Material

Plastic

Metal

Others

By Product Type

Tethered Caps

Push/Pull Caps

Screw Caps

Others

By End-use Industry

Food & Beverages

Pharmaceutical

Consumer Goods

Personal Care & Cosmetics

Others

By Region

North America (By Material, By Product Type, By End Use Industry, and Country)

U.S. (By Product Type)

Canada (By Product Type)

Europe (By Material, By Product Type, By End Use Industry, and Country)

Germany (By Product Type)

France (By Product Type)

U.K. (By Product Type)

Italy (By Product Type)

Spain (By Product Type)

Russia (By Product Type)

Rest of Europe (By Product Type)

Asia Pacific (By Material, By Product Type, By End Use Industry, and Country)

China (By Product Type)

India (By Product Type)

Japan (By Product Type)

Australia (By Product Type)

Southeast Asia (By Product Type)

Rest of Asia Pacific (By Product Type)

Latin America (By Material, By Product Type, By End Use Industry, and Country)

Brazil (By Product Type)

Mexico (By Product Type)

Rest of Latin America (By Product Type)

Middle East & Africa (By Material, By Product Type, By End Use Industry, and Country)

GCC (By Product Type)

South Africa (By Product Type)

Rest of the Middle East & Africa (By Product Type)

View Full Infographic

View Full Infographic