Titanium Dioxide Market Size, Share & Industry Analysis, By Grade (Anatase and Rutile), By Process (Sulphate and Chloride), By Application (Paints & Coatings, Plastic, Inks, Paper & Pulp, Food & Beverages, Cosmetics, Pharmaceuticals, and Others), and Regional Forecast, 2026-2034

TITANIUM DIOXIDE MARKET SIZE AND FUTURE OUTLOOK

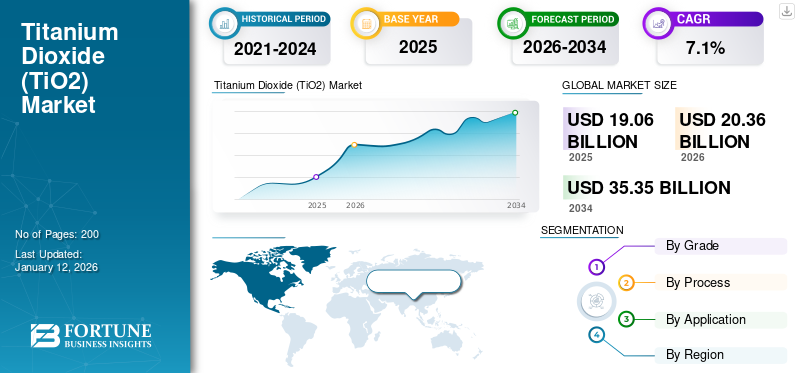

The global titanium dioxide market size was valued at USD 19.06 billion in 2025 and is projected to grow from USD 20.36 billion in 2026 to USD 35.35 billion by 2034 at a CAGR of 7.1% during the forecast period (2026-2034). Asia Pacific dominated the global titanium dioxide market with a market share of 47.00% in 2025.

Titanium Dioxide (TiO₂) is a white, powdered compound widely recognized for its exceptional brightness and opacity. It is used across diverse industrial and consumer applications, including paints and coatings, cosmetics, plastics, paper, textiles, and food colorants. In the construction and automotive sectors, TiO₂ serves as a vital pigment in paints and coatings used for roofing, flooring, automotive finishes, and printing inks. Rapid urbanization and growing construction activities in developing regions, fueled by population growth, have significantly increased TiO₂ demand in these applications. Additionally, the expanding use of plastics and rubber in consumer goods further supports market growth. The COVID-19 pandemic has also driven higher demand for plastic-based medical equipment such as gloves, IV bags, and respiratory devices, where TiO₂ is used as a pigment.

Major market players include Tronox Holdings plc, The Chemours Company, Argex Titanium Inc., and Evonik Industries.

Download Free sample to learn more about this report.

TITANIUM DIOXIDE MARKET TRENDS

High Demand for Titanium Dioxide in Various Applications to Lead Market

The growing adoption of Titanium Dioxide (TiO₂) pigments across multiple applications, including paints and coatings, rubber, textiles, and printing inks, is significantly driving market growth. In printing inks, technological advancements have expanded TiO₂ usage in lamination, metal decorative inks, and screen printing, opening new avenues for development. The increasing production of lightweight vehicles to enhance fuel efficiency is also boosting TiO₂ demand, as the compound is widely used to coat plastic auto components such as bumpers and interior or exterior parts. TiO₂’s excellent properties such as scratch resistance, chemical stability, and durability further enhance its use in plastics, textiles, rubber, and cosmetics for coloring fabrics and coating products. Moreover, the COVID-19 pandemic has amplified TiO₂ demand, particularly due to its role in manufacturing essential medical equipment.

Expanding Infrastructure and Urbanization in Emerging Economies Creates New Growth Opportunities

Rapid urbanization and infrastructure expansion in emerging economies are fueling strong demand for titanium dioxide (TiO₂). As cities grow and modern housing, transport, and commercial projects rise, TiO₂ is increasingly used in coatings and plastics for its brightness, durability, and weather resistance. According to UN DESA, India, China, and Nigeria will together account for 35% of global urban population growth by 2050, driving massive demand for construction and protective materials. Government initiatives such as India’s Smart Cities Mission are also promoting sustainable and energy-efficient urban development, boosting TiO₂ consumption. Companies aligning their strategies with these trends and focusing on high-performance, eco-friendly TiO₂ solutions stand to gain significantly from long-term growth in the construction and infrastructure sectors across developing regions.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Lightweight Vehicles in Automotive and Construction Industries to Drive Growth

The increasing demand for lightweight vehicles, supported by technological advancements in the automotive industry, is significantly driving the titanium dioxide market growth. Stricter emission regulations have accelerated the shift toward fuel-efficient vehicles, further boosting TiO₂ consumption in automotive coatings and components. Additionally, expanding construction activities, driven by rising consumer living standards and large-scale government infrastructure initiatives, are fueling demand for TiO₂-based materials. Beyond these sectors, growing production in consumer goods, appliances, and electronics is also contributing to market expansion, as TiO₂ continues to be valued for its brightness, durability, and versatility across diverse industrial applications.

Rising Demand from Paints and Coatings Industry Accelerates Market Growth

The paints and coatings industry is the largest consumer of titanium dioxide (TiO₂), accounting for over half of global demand, and remains a major growth driver for the market. TiO₂’s exceptional opacity, brightness, UV resistance, and durability make it indispensable in architectural, automotive, industrial, and marine coatings. Urbanization and rising construction activities, particularly in Asia Pacific, are fueling demand for decorative and weather-resistant architectural coatings. Meanwhile, growing automotive production and industrial expansion further boost TiO₂ use, as it enhances surface protection and appearance. Sustainability trends are also shaping the market, with increasing adoption of eco-friendly, low-VOC, and energy-efficient coatings where TiO₂ plays a key role. Together, these factors ensure that the paints and coatings sector will continue to underpin strong global demand for titanium dioxide.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Stringent Government Regulations May Hinder Market Growth

The demand for Titanium Dioxide (TiO₂) has risen significantly across various end-use industries due to its excellent pigmenting and performance properties. However, the market faces challenges from the growing availability of alternative materials such as antimony oxide, carbonates, and zinc oxide, which can serve as substitutes in certain applications. Additionally, stringent government regulations focused on minimizing industrial waste and promoting environmental sustainability are limiting TiO₂ production and usage, thereby restraining overall market growth.

MARKET OPPORTUNITIES

Revival of Automotive and Construction Industries Boosts Market Progress

In the post-pandemic period, the rebound of the automotive and construction industries has fueled renewed demand for titanium dioxide (TiO₂), a crucial ingredient in paints, coatings, and plastics. Rapid urbanization and large-scale infrastructure projects are driving the need for durable, weather-resistant, and visually appealing coatings. Simultaneously, the rise in vehicle production and refinishing activities is boosting the product usage in automotive coatings and plastic components. Moreover, growing sustainability trends are expanding TiO₂ applications in self-cleaning surfaces, air purification systems, and solar panels, encouraging innovation in eco-friendly and advanced formulations. With ongoing advancements in nanotechnology further enhancing its performance, TiO₂ producers and suppliers are well positioned to capitalize on significant growth opportunities across these evolving sectors.

MARKET CHALLENGES

Supply Chain Disruptions, Environmental Concerns, and Price Volatility Pose Risks to Market Growth

The titanium dioxide (TiO₂) market faces key challenges such as supply chain disruptions, environmental concerns, and price volatility. Global trade restrictions and geopolitical tensions affecting raw materials such as ilmenite and rutile have raised production costs and limited supply. High energy use and waste generation during TiO₂ processing have led to stricter environmental regulations in regions such as the EU and the U.S., increasing compliance costs. Additionally, the EU’s 2022 ban on TiO₂ in food products and its classification as a potential carcinogen have created regulatory hurdles. To address these issues, major producers are focusing on sustainable mining, recycling, and alternative sourcing to enhance supply stability and meet evolving environmental standards.

TRADE PROTECTIONISM

In November 2024, the European Union implemented definitive anti-dumping duties on titanium dioxide (TiO₂) imports from China, with tariffs ranging from USD 0.28 to 0.83 per kilogram. Effective from January 2025 for a five-year period, the measure aims to safeguard EU producers from a surge in low-priced Chinese imports, which had captured around 22% of the market and negatively impacted the profitability of local manufacturers.

SEGMENTATION ANALYSIS

By Grade

Rutile Segment Dominated the Market Due to Advancements In Chloride-Route Processing

The market is segmented based on grade into anatase and rutile. Rutile will hold the leading share of 8.43% in 2026 worldwide due to its exceptional opacity, UV resistance, and durability. A key driver is the expansion of construction and infrastructure projects across developed and developing economies, where rutile-based paints and coatings provide long-lasting performance and visual appeal. From skyscrapers in Asia to large-scale renovation programs in Europe and North America, demand remains strong. Moreover, advancements in chloride-route processing have increased production efficiency and aligned with global sustainability goals, enhancing rutile’s position in the market. The growing use of rutile in automotive coatings, industrial plastics, and packaging further supports its widespread adoption. With continuous innovation and broad application across industries, rutile remains the primary grade of titanium dioxide, sustaining its leadership role in global demand.

Anatase titanium dioxide continues to expand its presence in diverse applications, particularly in consumer and environmental markets. Its transparency and UV absorption make it highly valued in sunscreens, cosmetics, and skincare products, where health-conscious consumers seek effective protection and appealing formulations. Furthermore, its strong photocatalytic activity is widely applied in water purification, air filtration, and self-cleaning surfaces, technologies that align perfectly with sustainability and innovation trends.

By Process

Sulfate Segment Held the Major Share Due to its Cost Effectiveness Production Process

On the basis of process, the market is segmented into sulfate and chloride.

In 2024, the sulfate segment accounted for 41.6% of the titanium dioxide market share, driven by its simpler and more cost-effective production process. Rising demand from the automotive and construction sectors has boosted TiO₂ use in paints and coatings, while technological advancements have improved efficiency through low-cost machinery and eco-friendly raw materials.

The chloride segment is projected to witness notable growth during the forecast period, supported by increasing demand for consumer goods. Although limited by high production costs and reliance on high-grade raw materials, ongoing innovations, such as AI-driven reactors that have reduced energy use by 30%, are enhancing process efficiency and sustainability. These advancements are positioning the chloride method for future expansion.

By Application

Paints & Coatings Segment to Dominate the Market Due to Rising Construction Activities

The market is segmented based on application into paints & coatings, plastic, inks, paper & pulp, food & beverages, cosmetics, pharmaceuticals, and others.

The paints & coatings segment is expected to dominate the titanium dioxide (TiO₂) market, accounting for 53.29% of the share in 2026. Strong demand from the automotive sector and expanding construction activities are key growth drivers. TiO₂ is widely used as a pigment in paints and coatings due to its superior properties, including corrosion resistance, high durability, and scratch resistance. These qualities make it essential for enhancing the performance and longevity of coatings in both automotive and construction applications, thereby supporting the continued growth of this segment.

Plastics represent the second-largest application of titanium dioxide, with demand led by packaging and automotive industries. In packaging, TiO₂ enhances opacity, whiteness, and UV stability in films, containers, and flexible packaging materials. Automotive plastics also benefit from TiO₂’s durability, especially in lightweight parts that require weather resistance.

The paper & pulp segment is projected to experience steady growth during the forecast period, with a CAGR of 7.01% from 2025 to 2032. This expansion is driven by the increasing use of titanium dioxide (TiO₂) in applications such as printing inks, decorative papers for magazines, and decorative foils. Rising demand for fillers among paper manufacturers is further supporting segment growth. Additionally, the growing utilization of TiO₂ in coating plastic-based consumer goods is contributing to the segment’s expansion, reflecting its versatility and importance across multiple end-use industries.

Inks rely heavily on titanium dioxide for brightness, opacity, and print consistency. Packaging inks dominate this application, particularly in food, beverage, and consumer goods sectors where clarity and branding are critical. TiO₂ supports high-quality results across flexographic, offset, and digital printing processes. Demand is rising in Asia Pacific and North America due to e-commerce expansion and consumer product branding.

Pharmaceuticals add steady demand for TiO₂ globally. It is widely used in tablet and capsule coatings, where it enhances opacity, improves stability, and ensures consistent product appearance. TiO₂ also supports brand recognition by providing uniform coloring across pharmaceutical products. With rising healthcare needs and the expansion of generic drug production, demand for TiO₂ in pharmaceuticals continues to grow.

Cosmetics represent a dynamic application for TiO₂ globally, where sunscreen demand is high due to strong solar intensity in major countries. Japan and South Korea further boost consumption with advanced skincare and cosmetic products that rely on TiO₂’s transparency and UV absorption. Rising consumer awareness of sun protection and skincare continues to drive steady growth, making cosmetics a highly promising application for TiO₂.

Growing demand for visually consistent, premium-looking packaged foods has surged the titanium dioxide demand. It is used mainly as a white color and opacifier in confectionery coatings, chewing gum, bakery icings, powdered desserts, dairy-style products, sauces, and some drink mixes, giving a bright “clean white” and better color contrast at low doses. Growth is supported by rising processed-food and confectionery consumption and expanding industrial food output.

The others segment for titanium dioxide includes smaller, varied applications such as rubber and elastomer products, adhesives and sealants, manmade fibers and technical textiles, ceramics, glass and enamel finishes, and functional uses in catalysts and photocatalysts for air and water purification, self-cleaning materials, and select electronics or energy systems. Growth in this segment is supported by rising rubber demand from automotive and industrial goods, expanding construction and DIY adhesive markets, higher production of synthetic fibers and performance textiles, steady ceramics and glass consumption linked to infrastructure, and growing adoption of TiO2 based environmental and green building technologies.

To know how our report can help streamline your business, Speak to Analyst

TITANIUM DIOXIDE MARKET REGIONAL OUTLOOK

Asia Pacific

Asia Pacific Titanium Dioxide Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed approximately USD 8.96 billion to the global market in 2025, accounting for 47.00% share, and is expected to reach USD 9.69 billion in 2026. This growth is largely due to the increasing demand for Titanium Dioxide (TiO2) from various end-use industries, including automotive, construction, plastics, and paper. Economic development in India, China, and Japan is driving significant demand from the construction sector, fueled by lifestyle improvements and government infrastructure projects. China is estimated to be worth USD 7.36 billion in 2026. China, in particular, leads the region, owing to the rapid growth of its middle-class population and rising disposable incomes. India is projected to reach USD 0.44 billion in 2025, while Japan is projected to reach USD 0.57 billion in 2026.

North America

In 2025, North America held 11.70% of the global market share, reaching a valuation of USD 2.22 billion, and is projected to grow to USD 2.36 billion in 2026, attributed to the region's rapid technological advancements and high disposable income among consumers. The increasing demand for lightweight and cost-effective automobiles, along with a rise in new construction and renovation activities, are the primary factors driving market growth. Additionally, heightened trade activities, including exports from the region, are contributing positively to the TiO2 market. Furthermore, the rising demand from the healthcare industry during the global pandemic played a significant role in driving this market. In 2024, the U.S. market was valued at USD 2.06 billion. As production increases in industries such as cosmetics, paints and coatings, and paper, the consumption of titanium dioxide is expected to rise significantly during the forecast period. The U.S. market is projected to be valued at USD 2.22 billion in 2026.

Europe

The market in Europe reached USD 4.28 billion in 2025, representing 22.40% of total market revenue, and is projected to reach USD 4.45 billion in 2026. The region is anticipated to experience significant market growth during the forecast period, driven by increasing demand for cost-effective and environmentally friendly lightweight automobiles among consumers across various economic levels. The U.K. market continues to grow, projected to reach a market value of USD 0.43 billion in 2026. Heightened awareness of environmental protection is driving the adoption of lightweight and durable products with fuel-efficient features, thus creating new market opportunities. Germany stands out as a key country in automotive manufacturing, bolstered by robust economic growth and technological advancements that offer cost-effective and fuel-efficient solutions for lightweight vehicles.Germany is expected to reach USD 0.7 billion in 2026, while France is projected to reach USD 0.44 billion in the same year.

Latin America

In 2025, Latin America generated USD 2.13 billion, contributing 11.20% to global market revenue, and is projected to grow to USD 2.28 billion in 2026. The region is expected to experience gradual growth over the forecast period. In Latin America, Brazil and Mexico are anticipated to observe rapid economic growth due to increasing urbanization, which is driving high construction activity in these countries. Additionally, the use of advanced technologies in the construction and consumer goods industries has led to a significant increase in the consumption of minerals.

Middle East & Africa

The Middle East & Africa region captured 7.70% of the global market in 2025, generating USD 1.47 billion in revenue, and is projected to reach USD 1.58 billion in 2026. The Middle East & Africa serve as major hubs for mining. As a result, raw materials are readily available and at lower prices for manufacturers in the region, which helps to reduce overall production costs. Furthermore, the growing economy in this region is improving consumers' lifestyles, leading to increased demand for finished goods such as cosmetics, fabrics, and electronic appliances. Saudi Arabia is expected to stand at USD 1.58 billion in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Joint Ventures and Capacity Expansion are Key Strategic Initiatives Implemented by Key Players to Strengthen their Market Position

Key players in the titanium dioxide (TiO₂) market include Tronox Holdings plc, The Chemours Company, Argex Titanium Inc., Evonik Industries, INEOS, and others. These companies are actively pursuing strategies such as capacity expansion, product innovation, mergers, acquisitions, and collaborations to strengthen their market position. For instance, DuPont adopted capacity enhancement as a competitive strategy by constructing a new TiO₂ production plant and upgrading existing facilities in Mexico. This initiative increased the company’s total production capacity to 350 kilotons (KT), reinforcing its ability to meet rising global demand and maintain a strong presence in the market.

LIST OF KEY TITANIUM DIOXIDE COMPANIES PROFILED:

- Tronox Holdings plc (U.S.)

- The Chemours Company (U.S.)

- Argex Titanium Inc. (Canada)

- Evonik Industries (Germany)

- The Kish Company, Inc. (U.S.)

- Ishihara Sangyo Kaisha Ltd. (Japan)

- Venator Materials PLC. (U.S.)

- Tayca Corporation (Japan)

- LB Group (China)

- Kronos Worldwide, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- May 2025: Venator launched a new TMP- and TME-free TIOXIDE TR85 pigment, aligning with sustainability goals and regulatory compliance while offering high-quality performance for coatings, plastics, and paper applications.

- March 2025: LB Group launched new high-performance TiO₂ pigments for plastics, enhancing its BILLIONS pigment portfolio and providing advanced solutions for plastic applications, strengthening its competitive position in the global TiO₂ pigment market.

- March 2025: Venator launched a new TIOXIDE TR81 pigment, providing the same opacity, brightness, dispersibility, and durability as previous products, without the use of TMP or TME, meeting evolving industry standards.

- July 2024: Kronos Worldwide, Inc. took full ownership of Louisiana Pigment Company (LPC), boosting its North American market position with LPC’s 156,000 metric tons of annual titanium dioxide production capacity and diversified product offerings.

- December 2022: LB Group signed a strategic deal to double its vanadium-titanium magnetite mines, ensuring a stable raw material supply for TiO₂ production, boosting integration, and further strengthening its long-term competitiveness in the market.

REPORT COVERAGE

The market research report provides a detailed analysis of the market and focuses on crucial aspects such as leading companies, sources, applications, and products. Additionally, the report offers insights into market trends and highlights vital industry developments. In addition to the factors mentioned above, the report encompasses various factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Growth Rate | CAGR of 7.1% from 2026 to 2034 |

| Segmentation | By Grade, Process, Application, and Region |

| By Grade |

|

| By Process |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 20.36 billion in 2026 and is projected to reach USD 35.35 billion by 2034.

Increasing at a CAGR of 7.1%, the market will exhibit steady growth in the forecast period (2026-2034).

Paint & coatings is expected to be the leading segment during the forecast period by application.

Increasing demand from the automotive and construction industries is a key factor driving market growth.

Tronox Holdings plc, The Chemours Company, Argex Titanium Inc., Evonik Industries, and INEOS are a few of the leading players in the global market.

Asia Pacific dominated the global market in 2025.

The continuous growth in the automotive and construction industries, along with technological innovation, shall drive product demand.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us