2-Propanol Market Size, Share & Industry Analysis, By Application (Solvent, Chemical Intermediate, Cleaning & Drying Agent, Antiseptic & Astringent, and Others), By End-Use Industry (Pharmaceuticals & Healthcare, Chemicals, Paints, Coatings & Printing, Electronics & Semiconductors, Cosmetics & Personal Care, and Others), and Regional Forecast, 2025-2032

2-Propanol Market Size and Future Outlook

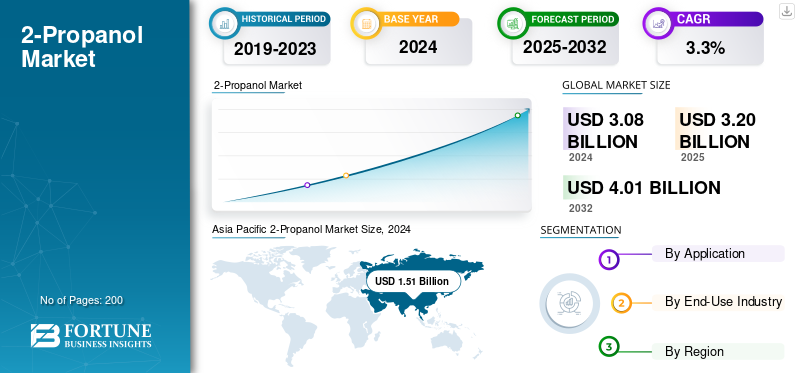

The global 2-Propanol market size was valued at USD 3.08 billion in 2024. The market is projected to grow from USD 3.20 billion in 2025 to USD 4.01 billion by 2032, exhibiting a CAGR of 3.3% during the forecast period. Asia Pacific dominated the global 2-propanol market with a market share of 49.02% in 2024.

2-Propanol (Isopropyl Alcohol, IPA) is a versatile solvent and chemical intermediate widely utilized across pharmaceutical, personal care, electronics, and industrial applications. It offers excellent solvency, rapid evaporation, and disinfectant properties, making it essential in cleaning agents, coatings, inks, and medical formulations. Its balance of purity, cost efficiency, and compatibility with diverse chemical systems support its dominance among secondary alcohols in both consumer and industrial markets.

The market is led by key players such as Dow Inc., Shell plc, LG Chem Ltd., ENEOS Corporation, and ExxonMobil Chemical. Their extensive production networks, integration with propylene feedstocks, and technological advancements in high purity and bio-based IPA manufacturing underpin their leadership. Through capacity expansion, process innovation, and sustainability-focused initiatives, these companies continue to strengthen their competitive positions while ensuring reliable global supply across healthcare, semiconductor, and specialty chemical industries.

Download Free sample to learn more about this report.

2-Propanol Market Key Takeaways

- 2024 Market Size: USD 3.08 billion

- 2025 Market Size: USD 3.20 billion

- 2032 Forecast Market Size: USD 4.01 billion

- CAGR: 3.3% from 2025–2032

- Asia Pacific dominated the 2-propanol market with a 49.02% share in 2024.

- The chemical intermediates segment is expected to grow at a CAGR of 3.8% during the forecast period.

- The electronics & semiconductors segment is expected to grow at a CAGR of 3.8% during the forecast period.

Asia Pacific

Asia Pacific maintained its leading position with a market value of USD 1.51 billion in 2024.

Europe

Europe reached USD 0.59 billion in 2025 and is projected to grow at a CAGR of 2.9% through 2032.

North America

North America recorded a market value of USD 0.56 billion in 2025.

U.S.

The 2-propanol market reached USD 0.48 billion in 2025.

Japan

Demand is supported by strong electronics and semiconductor manufacturing activities.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Drug Production Drives Solvent and Sanitization Use of 2-Propanol

The market is gaining strong momentum from the global expansion of pharmaceutical and healthcare manufacturing, where its use as a solvent, antiseptic, and cleaning agent is essential to process safety and product purity. Growing formulation output, stringent hygiene standards, and the localization of active pharmaceutical ingredient (API) production have significantly boosted industrial-grade and high-purity IPA consumption across major manufacturing regions.

- According to the International Federation of Pharmaceutical Manufacturers & Associations (IFPMA), the global pharmaceutical output has expanded by nearly 30% over the past five years, led by large-scale investments in Asia and North America. This manufacturing upturn translates directly to higher solvent and sterilization needs with 2-Propanol extensively used for equipment cleaning, surface disinfection, and raw materials handling in sterile environments.

As healthcare infrastructure broadens and production shifts closer to demand centers, IPA remains the solvent of choice for its balance of cost, efficacy, and safety. Its critical role in ensuring process hygiene and pharmaceutical compliance reinforces its position as a strategic enabler within the healthcare supply chain, supporting long term market stability and value growth.

MARKET RESTRAINTS:

Stricter VOC / Emissions Regulations Impose Compliance Costs and Usage Limits

Regulatory regimes aimed at reducing volatile organic compound (VOC) emissions increasingly target the use of organic solvents in industrial, commercial, and formulation settings. As a volatile solvent, it falls under scrutiny in many jurisdictions, forcing producers and formulators to invest in emissions control, reformulation, or face usage caps. These constraints raise compliance costs, slow adoption in sensitive applications, and could limit market expansion in regulated end users.

- For example, under the EU’s Directive 2004/42/EC, member states are required to limit VOC content in paints, varnishes, and refinishing products, driving formulators to restrict high-volatility solvents.

MARKET OPPORTUNITIES:

Growth of Bio-Based Production Opens New Pathways for the Market

As sustainability becomes central to industrial strategy, the shift toward bio-based and renewable chemical production presents a strong opportunity. Producers are exploring biomass and waste-derived routes to reduce dependency on petrochemical feedstocks, cut emissions, and align with emerging carbon-neutral targets. The early adoption of such technologies can open access to green financing, improve brand positioning, and create a differentiated product portfolio.

- According to the International Energy Agency (IEA), the share of bio-based chemicals in total chemical output is expected to rise steadily through 2030 as global policies push for circular and low-carbon manufacturing. (IEA – Renewables 2023 Report)

This trend directly supports investment in renewable propanol pathways, strengthening long-term prospects for sustainable production.

2-PROPANOL MARKET TRENDS:

Precision Manufacturing Drives Uptake of High-Purity 2-Propanol

The shift toward precision chemical manufacturing in electronics and semiconductors is reinforcing the importance of high-purity as a key cleaning solvent. With microchip architectures becoming smaller and process steps more contamination-sensitive, the demand is rising for solvents that offer fast evaporation and residue-free performance. It has become indispensable in wafer cleaning, photoresist removal, and precision drying applications where ultra-clean surfaces are critical to yield quality.

- According to the SEMI Bulk Wet Chemicals Report, the market for bulk wet process chemicals used in semiconductor manufacturing, including isopropyl alcohol, is projected to grow from USD 3.2 million in 2024 to nearly USD 4.9 million by 2029, driven by an increase in cleaning and patterning steps across advanced nodes.

MARKET CHALLENGES:

Waste Management and Environmental Compliance to Create Operational Challenges

The handling and disposal of spent solvents such as 2-Propanol pose significant operational and regulatory challenges, particularly in regions with stringent environmental frameworks. Producers and end users must manage solvent recovery, emissions, and effluent treatment to comply with evolving waste directives. These requirements increase capital and operating costs, and smaller manufacturers often struggle to meet standards for safe disposal and volatile organic compound (VOC) recovery.

- According to the U.S. Environmental Protection Agency (EPA), solvents, including isopropyl alcohol, contribute to hazardous air pollutants and are subject to control under the Clean Air Act and Resource Conservation and Recovery Act (RCRA).

This regulatory scrutiny necessitates continuous investment in recovery systems, emissions control, and safe handling protocols, making environmental compliance a recurring challenge for the value chain.

Download Free sample to learn more about this report.

Segmentation Analysis

By Application

Solvent Segment Dominated with High Demand in Industrial Cleaning and Coatings Applications

On the basis of segmentation by application, the market is classified into solvent, chemical intermediate, cleaning & drying agent, antiseptic & astringent, and others.

To know how our report can help streamline your business, Speak to Analyst

The solvent segment dominated the global market in 2024, driven by its wide range of uses in coatings, inks, and industrial cleaning formulations. Its strong solvency, fast evaporation rate, and compatibility with water and hydrocarbons make it integral to high-precision cleaning and surface preparation processes. The growing demand from semiconductor, automotive, and paint industries, coupled with the shift toward lower-VOC and safer solvent systems, continues to reinforce 2-propanol’s leadership in industrial and specialty applications.

- According to McGroup (2025), isopropyl alcohol remains one of the most widely used precision cleaning solvents in semiconductor and electronic manufacturing due to its fast evaporation and non-conductive nature, aligning with industry efforts toward safer, lower-impact formulations.

The chemical intermediates segment is expected to grow at a CAGR of 3.8% over the forecast period.

By End-Use Industry

Pharmaceuticals and Healthcare Segment Dominated driven by Vital role in Surface Sterilization and Drug Formulation

In terms of end-use industry, the market is categorized into pharmaceuticals & healthcare, chemicals, paints, coatings & printing, electronics & semiconductors, cosmetics & personal care, and others.

The pharmaceuticals & healthcare segment accounted for the largest 2-Propanol market share in 2024, supported by its critical role in drug formulation, disinfection, and surface sterilization. In 2025, the segment dominated with a 25.5% share. The compound’s rapid evaporation, broad antimicrobial activity, and compatibility with pharmaceutical excipients make it indispensable in both production environments and clinical applications. The growing emphasis on infection control and GMP-certified manufacturing have expanded its use in pharmaceutical-grade solvents, antiseptic wipes, and hand sanitizers. As healthcare systems continue to strengthen hygiene protocols and quality benchmarks, the demand for high-purity, pharmacopeia-compliant 2-propanol remains consistently strong across both developed and emerging markets.

- The U.S. Pharmacopeial Convention (USP) specifies that pharmaceutical-grade isopropyl alcohol must contain not less than 99.0% purity to ensure compliance with drug manufacturing standards.

- Shell Chemicals states that their pharmaceutical-grade Isopropyl Alcohol (IPA) GMP is manufactured to a minimum purity of 99.9% m/m and is specifically certified for pharmaceutical, medical, and food-contact applications.

The electronics & semiconductors segment is expected to grow at a CAGR of 3.8% over the forecast period.

2-Propanol Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific 2-Propanol Market Size, 2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific held the dominant share in 2023, valued at USD 1.49 billion, and maintained its lead in 2024 with a valuation of USD 1.51 billion. The region drives the market through large-scale chemical production, rapid industrialization, and growing healthcare consumption. China anchors growth with its vast pharmaceutical and chemical base, while Japan and South Korea lead in high-purity solvent use across electronics and semiconductor cleaning. India’s expanding pharmaceutical exports further boost regional output. Asia Pacific sets global cost and supply benchmarks, making it the central hub for both industrial and pharmaceutical-grade 2-propanol. In 2025, the China reached USD 0.83 billion.

- According to Sinopec Engineering (2024), China’s acetone-hydrogenation expansions and integration of propylene-based IPA units are strengthening the capacity leadership of the country in the Asia Pacific solvent chain.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe reached a value of USD 0.59 billion in 2025 and is projected to grow at a rate of 2.9% over 2025-2032. VOC and REACH compliance mandates, along with circular-economy policies, are driving the demand for safer, low-emission solvents. Germany, France, and Italy remain key centers for specialty chemicals, coatings, and healthcare manufacturing, where it is widely used for its performance reliability and regulatory acceptance. The rising adoption of bio-based and recovered solvents underpins 2-propanol market growth. Backed by these factors, Germany recorded a valuation of USD 0.17 billion, France USD 0.06 billion, and the U.K. USD 0.09 billion in 2025.

North America

The North American market reached USD 0.56 billion in 2025, ranking second globally. Strong healthcare infrastructure, FDA-regulated production standards, and advanced semiconductor manufacturing sustain regional demand. The U.S. dominates consumption through high pharmaceutical and cleaning-grade applications, while Canada contributes via coatings and intermediate chemicals. In 2025, the U.S. market reached USD 0.48 billion.

Latin America

Latin America reached a value of USD 0.32 billion in 2025, driven by growing demand for pharmaceuticals, coatings, and cleaning chemicals. Brazil and Mexico lead consumption, propelled by hygiene and industrial applications. The expansion of local production capacities is improving self-sufficiency and supporting a stable regional supply.

Middle East & Africa

The Middle East & Africa market touched a value of USD 0.15 billion in 2025. Industrial diversification, healthcare infrastructure development, and expanding chemical processing capacity are key drivers of growth. Saudi Arabia and the UAE are investing in downstream petrochemical clusters for local production, while the pharmaceutical and coatings sectors in North Africa are steadily expanding.

- ADNOC Group (2024) highlights the integration of new IPA production within its Ruwais petrochemical complex, aimed at meeting domestic healthcare and industrial solvent needs across the Gulf.

COMPETITIVE LANDSCAPE

Key Industry Players:

Strategic Investments and Sustainability Initiatives Influences the Competitive Landscape

The global market is moderately consolidated, with a small group of multinational chemical producers shaping global production, trade, and technology advancement. These companies focus on capacity expansion, product innovation, and sustainable manufacturing to meet the rising demand across the pharmaceuticals, personal care, and electronics industries. Recent investments in high-purity and bio-circular IPA reflect a broader industry transition toward cleaner and more specialized solvent production.

Key manufacturers in the global 2-Propanol market include Dow Inc., Shell plc, LG Chem Ltd., ENEOS Corporation, and ExxonMobil Chemical. Their large-scale production facilities, feedstock integration, and advanced purification systems enable them to supply diverse end-use sectors ranging from pharmaceuticals to semiconductors. LG Chem’s launch of its Bio-Circular Balanced IPA demonstrates a growing focus on renewable feedstocks and ISCC PLUS certification, while ExxonMobil’s planned USD 100 million ultra-pure IPA expansion at Baton Rouge reinforces North America’s position in high-purity solvents. Deepak Chem Tech’s upcoming IPA plant in India highlights the rise of new regional suppliers aiming for backward integration in acetone-based production.

Other leading players, including Sasol Limited, continue to enhance market responsiveness through capacity ramp-ups and supply-chain optimization to meet hygiene and healthcare demand surges, as seen during the COVID-19 period. Collectively, these developments signal an evolving landscape centered on supply resilience, purity advancement, and sustainability integration, driving long-term competitiveness across key global markets.

LIST OF KEY 2-PROPANOL COMPANIES PROFILED:

- Dow (U.S.)

- Shell (Netherlands)

- LyondellBasell Industries Holdings B.V. (U.S.)

- LG Chem. (South Korea)

- ENEOS Corporation (Japan)

- Kellin Chemicals (Zhangjiagang) Co., Ltd (China)

- Exxon Mobil Corporation (U.S.)

- INEOS (U.K.)

- Deepak Fertilisers & Petrochemicals Corporation Ltd (DFPCL) (India)

- Sasol (South Africa)

KEY INDUSTRY DEVELOPMENTS:

- April 2025 – Deepak Chem Tech Ltd. (India) approved a greenfield investment of ~INR 3,500 crore (USD 390 million) to construct new phenol (300 KTA), acetone (185 KTA), and IPA (100 KTA) plants at Dahej, Gujarat. The project strengthens its backward-integrated solvent manufacturing base and positions India as a regional IPA supply hub.

- March 2025 - ExxonMobil Chemical announced a USD 100 million expansion at its Baton Rouge facility to produce 99.999% ultra-pure IPA by 2027, targeting semiconductor and precision-cleaning markets. The investment reinforces North America’s high-purity solvent supply chain.

- August 2023 – LG Chem Ltd. launched its Bio-Circular Balanced IPA, derived from renewable feedstocks and certified under ISCC PLUS, reinforcing its sustainability credentials in low-carbon solvents for coatings, pharmaceuticals, and electronics.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2019-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Period | 2019-2023 |

| Growth Rate | CAGR of 3.3% from 2025-2032 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Application, End-Use Industry, and Region |

| By Application |

|

| By End-Use Industry |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.08 billion in 2024 and is projected to reach USD 4.01 billion by 2032.

In 2024, the Asia Pacific market value stood at USD 1.51 billion.

The market is expected to exhibit a CAGR of 3.3% during the forecast period of 2025-2032.

The solvent segment led the market by application in 2024.

Rising drug production driving the solvent and sanitization use of 2-propanol is a key factor propelling industry growth.

Dow Inc., Shell plc, LG Chem Ltd., ENEOS Corporation, and ExxonMobil Chemical, are some of the prominent players in the market.

Asia Pacific dominated the market in 2024.

The growth of bio-based production is a major factor expected to favor product adoption.

- 2019-2032

- 2024

- 2019-2023

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us