Smart Home Market Size, Share & Industry Analysis, By Application (Retrofit and New Construction), By Protocol (Wired and Wireless), By Device Type (Safety & Security Access Control, Home Appliances, HVAC, Lighting Control, Smart Entertainment Devices, Smart Kitchen Appliances, and Others), and Regional Forecast, 2026–2034

Smart Home Market Size & Share

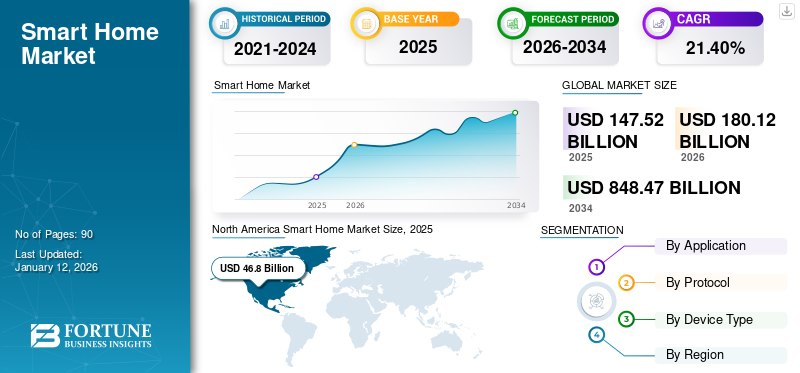

The global smart home market size was valued at USD 147.52 billion in 2025 and is projected to grow from USD 180.12 billion in 2026 to USD 848.47 billion by 2034, exhibiting a CAGR of 21.40% during the forecast period. North America dominated the smart home market with a share of 31.70% in 2025. Industry growth driven by connected device adoption, wireless interoperability, residential automation demand, energy management systems, and intelligent security integration (2026–2034).

As a part of their growth strategy, companies such as ABB, Alphabet, Samsung, and Emerson aim to engage in partnership, collaboration, mergers, and acquisitions (M&A) activities to expand their business and geographical presence.

The global smart home market continues transitioning from device-specific adoption toward integrated residential ecosystems that combine automation, connectivity, energy optimization, and security functionality. Earlier market expansion largely reflected premium consumer electronics demand. Current smart home market growth increasingly depends on interoperability, platform integration, and practical utility across energy management, home monitoring, appliance control, and residential convenience applications. Technology providers increasingly prioritize ecosystem compatibility rather than standalone hardware differentiation.

Consumer adoption patterns increasingly reflect functional value rather than novelty. Safety and security systems, connected lighting, heating, ventilation, and air conditioning (HVAC) controls, and smart appliances continue gaining traction because measurable benefits increasingly influence purchasing behavior. Energy efficiency, remote monitoring, predictive maintenance, and household convenience continue shaping the smart home market size across both retrofit and new construction environments. Household energy cost awareness increasingly strengthens demand for intelligent control systems capable of optimizing electricity consumption.

Wireless communication protocols continue strengthening market accessibility due to installation flexibility and lower deployment complexity. At the same time, interoperability challenges remain commercially relevant because fragmented ecosystems may reduce seamless device communication. Industry participants increasingly support cross-platform compatibility standards to reduce consumer friction and improve ecosystem reliability. Smart home market trends, therefore, increasingly reflect software integration, device compatibility, and centralized control capabilities rather than hardware expansion alone.

Residential construction activity also continues influencing demand dynamics. New construction projects increasingly integrate connected technologies during initial building phases, while retrofit demand remains supported by consumers upgrading legacy systems through modular installations. Device manufacturers increasingly collaborate with utilities, telecom operators, homebuilders, and digital platform providers to improve ecosystem integration and distribution reach. Despite cybersecurity concerns and pricing sensitivity across selected regions, smart home market growth remains supported by expanding broadband penetration, connected device familiarity, and increasing residential digitalization.

Download Free sample to learn more about this report.

SMART HOME MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 147.52 Billion

- 2026 Market Size: USD 180.12 Billion

- 2034 Forecast Market Size: USD 848.47 Billion

- CAGR: 21.40% from 2026–2034

- North America dominated the smart home market with a 31.70% share in 2025.

- Residential applications accounted for the largest share of the market in 2025.

- The Smart Entertainment Devices segment is projected to dominate the market with a share of 28.78% in 2026.

North America

The North American market was valued at USD 46.8 billion in 2025, capturing 31.70% of global revenue.

Europe

In 2025, Europe held 28.70% of the global market, reaching a valuation of USD 42.39 billion, and is projected to grow to USD 51.97 billion in 2026.

Asia Pacific

The market in the Asia Pacific reached USD 34.2 billion in 2025, representing 25.50% of total market revenue, and is expected to reach USD 42.46 billion in 2026.

U.S.

The US market is projected to reach USD 35.28 billion by 2026, owing to the growing number of tech-savvy consumers in the country.

Japan

Market growth is supported by advanced consumer electronics adoption, smart housing initiatives, aging population needs, and increasing deployment of intelligent home automation technologies.

Read More

Key Metrics and Overview

|

Metric |

Details |

|

Market Size in 2025 |

USD 147.52 Billion |

|

Projected Market Size in 2034 |

USD 848.47 Billion |

|

CAGR (2026 - 2034) |

21.40% |

|

Market Segmentation |

By Application, Protocol, Device Type, and Region |

|

Top Key Players |

Honeywell International, ABB, Johnson Controls International plc, Siemens, Alphabet, Emerson, Robert Bosch Smart Home GmbH, Samsung, LG Electronics, Crestron Electronics, Apple, Ecobee, Schneider Electric, Vivint, Fantasia Trading LLC, Snap One, Govee, Xiaomi, Signify Holdings |

What is a Smart Home?

A smart home is a home with devices that can be handled remotely using a smartphone or computer. These devices can be used to control lighting, temperature, security, and other functions. Smart homes provide multiple benefits, including energy efficiency, convenience, and enhanced security. The automation of tasks reduces time for the residents, making their lives easier. The devices can also adapt to the behavior of the household, offering personalized service. For instance, a smart thermostat can provide the preferred temperature settings of the inhabitants and adjust the temperature accordingly.

IMPACT OF GENERATIVE AI

Synergy of Gen-AI and Smart Home is Unlocking Unprecedented Opportunity, Fueling Innovation and Growth

Gen-AI can create text, images, and human sounds, making it an impressive technology nowadays. The technology has improved rapidly in ten years, becoming more efficient and adaptable. From content to automation content, Gen-AI technology helps to modify multiple sectors. With the emergence of products such as ChatGPT, Google Bard, Amazon LLM, and others, Generative AI is positively creating a new way for smart technologies. The integration of Gen-AI into the smart home ecosystem has the potential to make everyday life more effective, practical, and pleasant. For instance,

- As per the St. Louis Fed Org's 2024 survey, nearly 40% of U.S. adults aged 18 to 64 used generative AI. About 1/3 of respondents stated using it daily or at least a few times per week. Remarkably, AI usage was slightly lower at work (28.1%) than at home (32.6%).

Key Market Dynamics

Smart Home Market Trends

Increasing Adoption of Home Automation is a Significant Market Trend

Home automation plays a pivotal role in driving the smart home market growth by enhancing convenience, improving energy efficiency, and providing increased security. The home automation system allows homeowners to remotely control various devices (lights, security cameras, appliances, and thermostats) through a smartphone or voice commands. This convenience appeals to consumers seeking a more seamless and efficient lifestyle.

- Nest Thermostat can learn a homeowner’s temperature preferences and adjust accordingly. This can be controlled remotely via a mobile app, allowing users to change their home’s temperature before they arrive.

- Philips Hue Smart Bulbs allow users to program their lighting to turn off when not needed or adjust brightness based on natural light levels, helping to save energy.

Smart home market trends increasingly reflect ecosystem integration, energy intelligence, and device interoperability rather than isolated product adoption. Consumers increasingly favor connected platforms capable of managing lighting, security, entertainment, and climate control through centralized interfaces. Demand increasingly shifts toward integrated experiences where devices function collectively rather than independently. This transition continues influencing product development strategies across the smart home industry.

Artificial intelligence-enabled automation continues gaining relevance across smart home applications. Smart systems increasingly adjust lighting, temperature, security settings, and appliance usage according to occupancy patterns and behavioral preferences. Predictive maintenance alerts, automated energy optimization, and voice-enabled controls continue expanding practical household applications beyond convenience-focused use cases.

Wireless communication technologies continue to strengthen market accessibility. Wi-Fi, Bluetooth, Zigbee, Z-Wave, and Matter-enabled ecosystems increasingly support flexible deployment and simplified device installation. Industry efforts to improve interoperability continue to reduce ecosystem fragmentation, strengthening consumer confidence and improving long-term adoption visibility across connected residential environments.

Smart Home Market Drivers

Integration of Advanced Technologies with Smart Home Appliances to Drive Market

Advanced technology plays a crucial role in smart homes by enabling devices to connect and communicate with each other. This connectivity allows for seamless control and automation of various aspects of a home, such as lighting, temperature, security systems, and appliances. By leveraging IoT, homeowners can remotely monitor and control their smart devices, enhancing convenience and efficiency. Companies are introducing new smart home products by incorporating the advanced technologies mentioned previously. For instance,

- In March 2025, ZTE Corporation launched a new home network product range at MWC Barcelona. The portfolio includes the next-gen 4K AI Soundbar, high-performance LinkPro Wi-Fi 7 BE9400/BE6500, and AI home media center. The product is equipped with an AI screen FTTR RoomPON 6.0 and the ZENIC ONE management platform.

Integrating these advanced technologies with smart home appliances drives the market by offering increased convenience, efficiency, security, and personalization.

The smart home market continues benefiting from expanding broadband penetration, connected device familiarity, and increasing residential digitalization. Growth increasingly reflects practical consumer priorities rather than discretionary technology spending alone. Safety monitoring, energy efficiency, convenience, and remote access capabilities continue strengthening household adoption across multiple income categories and residential formats. Connected living increasingly moves from premium positioning toward broader household utility.

Residential energy management remains an important market driver. Rising electricity costs and growing attention toward energy efficiency continue encouraging the deployment of smart thermostats, lighting systems, and appliance management technologies. Heating, ventilation, and air conditioning (HVAC) automation increasingly supports household energy optimization by adjusting temperature settings based on occupancy patterns and usage behavior. Utilities in several markets also continue supporting smart energy technologies through demand-response initiatives and digital grid programs.

Safety and security concerns continue to support smart home market growth. Connected cameras, video doorbells, biometric access systems, motion sensors, and remote monitoring capabilities increasingly attract consumer demand because households prioritize real-time visibility and property security. Insurance incentives and urban residential density also continue influencing purchasing behavior across selected markets.

Smart Home Market Restraints

Cybersecurity and Data Protection Concerns Restrict Market Growth

The rising cyberattacks on high-end connected technology are a major obstacle to market expansion. Smart technology connects to home systems and gadgets, which makes it vulnerable to hackers if it is not effectively protected. For instance,

- As per the Zscaler report, there has been a substantial rise in cyberattacks targeting smart home devices and the Internet of Things (IoT) in 2024.

- According to a new report by cybersecurity firm SonicWall, attacks on smart home products have increased by 124% in 2024.

Cybersecurity concerns remain one of the most significant restraints within the smart home market. Connected devices continue collecting substantial volumes of household data, increasing sensitivity to unauthorized access, privacy risks, and software vulnerabilities. Consumer concerns regarding surveillance, data ownership, and network security continue influencing adoption behavior, particularly among first-time buyers evaluating interconnected residential systems.

Interoperability limitations also continue to constrain ecosystem development. Device compatibility challenges across manufacturers, operating systems, and communication protocols may reduce installation simplicity and ownership convenience. Fragmented ecosystems occasionally require households to maintain multiple applications or control interfaces, limiting seamless automation experiences. Industry standardization efforts continue progressing, although compatibility inconsistencies remain commercially relevant.

Affordability considerations continue affecting adoption across price-sensitive consumer groups. Although entry-level connected devices have become more accessible, integrated smart home ecosystems may still involve relatively high installation and equipment costs. Professional installation requirements, subscription-based monitoring services, and upgrade expenses may further influence purchasing decisions in selected markets.

Smart Home Market Opportunities

Development of Advanced Monitoring Devices for Child Safety to Expand Market Growth

Advanced monitoring devices designed specifically for child safety offer a range of features and functionalities that address parents' unique needs and concerns. These devices utilize various smart home technologies and sensors to provide comprehensive monitoring, tracking, and alert systems to keep children safe. For instance,

- In September 2023, VTech launched its latest advanced product, the V-Care VC2105 Smart Nursery Baby Monitor. The monitor has unique local AI capabilities that provide baby sleep analytics and real-time alerts.

- In September 2022, Amazon.com, Inc. launched the Ring Spotlight Cam Pro, Ring Spotlight Cam Plus, and 2nd Gen Ring Alarm Panic Button. These products are incorporated with radar and 3D motion detection features, providing security and access control and enhancing child safety within smart homes.

Energy optimization continues to represent one of the strongest opportunities within the smart home market. Rising electricity costs and residential sustainability goals increasingly support the adoption of connected thermostats, smart lighting, occupancy sensors, and appliance automation technologies. Integration with rooftop solar systems, home batteries, and intelligent energy management platforms continues to broaden market potential beyond convenience applications alone.

Retrofit opportunities remain particularly important because a substantial share of global housing stock predates connected infrastructure. Wireless technologies and modular installations increasingly allow homeowners to adopt smart systems without extensive structural modifications. This transition continues expanding addressable demand across existing residential environments, particularly in mature housing markets.

Healthcare and aging-in-place applications continue creating additional growth opportunities. Remote monitoring systems, fall detection devices, medication reminders, and connected emergency response technologies increasingly support elderly care within residential environments. Healthcare providers and insurers in selected regions continue evaluating connected home technologies to improve patient monitoring and independent living outcomes.

SEGMENTATION ANALYSIS

By Application

Surge in Adoption of Energy-Efficient Devices Accelerated Retrofit Segment Growth

Based on application, the market is divided into retrofit and new construction.

Retrofit

The Retrofit segment led the market, accounting for 51.18% market share in 2026, owing to the increasing adoption of energy-efficient devices and renewable energy sources by homeowners, which includes solar panels to reduce energy consumption and promote sustainable living.

Retrofit applications continue accounting for a substantial share of the smart home market because existing residential housing stock remains significantly larger than new construction activity across many economies. Consumers increasingly adopt connected systems incrementally rather than through full-home automation investment. Wireless installation flexibility and modular product availability continue strengthening retrofit demand, particularly among homeowners seeking practical functionality without extensive property modifications.

Connected lighting systems, video doorbells, smart locks, home surveillance devices, and intelligent thermostats remain among the most frequently adopted retrofit technologies. Consumers generally prioritize products capable of improving household convenience, energy efficiency, or security without requiring major electrical rewiring or structural renovation. Installation simplicity increasingly influences purchasing decisions because homeowners prefer systems that integrate with existing digital ecosystems.

Affordability considerations continue shaping retrofit adoption behavior. Entry-level connected devices allow households to expand automation gradually according to budget flexibility and usage priorities. Subscription services, bundled connectivity packages, and smartphone-based controls continue improving accessibility for mainstream consumers. At the same time, retrofit fragmentation occasionally creates interoperability challenges because households may integrate products from multiple manufacturers across different purchasing cycles.

New Construction

New construction is anticipated to grow at the highest CAGR during the forecast period. New homes are deploying AI-driven automation, enhanced security systems, and immersive entertainment options that provide residents with modern, connected living spaces. For instance,

- American Scientific Publishing Group 2024 stated that AI-powered smart home systems offer improved convenience by providing personalized experiences and automating routine tasks.

New construction continues to represent an important segment within the smart home market because builders increasingly integrate connected infrastructure during initial residential development phases. Home automation systems increasingly form part of premium and mid-tier residential offerings as homebuyers demonstrate stronger familiarity with connected living technologies. Early-stage integration also allows developers to reduce installation complexity and improve system compatibility.

Residential developers increasingly incorporate connected lighting, heating, ventilation, and air conditioning (HVAC) controls, smart security systems, energy monitoring technologies, and centralized automation hubs within newly constructed properties. Pre-installed systems generally improve interoperability because devices are selected within coordinated ecosystems rather than added incrementally over time. This structured deployment often supports smoother automation experiences and reduced installation costs.

Energy efficiency regulations also continue influencing new construction adoption. Building standards increasingly encourage the deployment of intelligent climate management systems, occupancy sensors, and connected energy controls to improve electricity optimization. Sustainable construction initiatives and rising residential electrification further strengthen demand for integrated automation infrastructure.

By Protocol

Wireless Segment Led Due to Rising Consumer Demand for Convenience

Based on the protocol, the market is divided into wired and wireless.

Wireless

The wireless segment dominated the market, accounting for 55.65% market share in 2026, and is anticipated to grow at a prominent CAGR during the forecast period. This has been propelled by advancements in technology, consumer demand for convenience, and the seamless integration of devices. AI and ML have become central to modern smart homes, enabling devices to learn user preferences and habits for a personalized experience. For instance,

- Smart thermostats such as the Nest Learning Thermostat adjust temperature settings based on occupancy patterns, optimizing comfort and energy efficiency.

Wireless communication systems account for a substantial share of the smart home market due to installation flexibility, lower deployment complexity, and broad compatibility across connected devices. Wi-Fi, Bluetooth, Zigbee, Z-Wave, Thread, and Matter-enabled ecosystems continue strengthening accessibility by allowing consumers to install connected technologies without major structural modifications. Wireless deployment remains particularly important across retrofit housing environments where rewiring may be impractical or cost-intensive.

Consumer preference increasingly favors wireless smart home systems because of scalability and ease of installation. Households can generally expand device ecosystems incrementally by adding lighting controls, security systems, entertainment devices, or connected appliances according to budget and functionality priorities. Smartphone integration and cloud-based management also continue improving user accessibility and centralized control.

Interoperability remains a key industry focus. Device manufacturers increasingly support cross-platform compatibility standards to reduce fragmentation and simplify connected experiences across multiple brands. Matter-enabled ecosystems, in particular, continue improving communication consistency between devices and digital assistants, supporting stronger long-term consumer confidence.

Wired

Wired communication systems continue to maintain relevance within the smart home market, particularly across premium residential environments, commercial properties, and newly constructed homes, where infrastructure installation can occur during development. Wired protocols generally provide stronger reliability, lower latency, and reduced signal interference relative to wireless alternatives, supporting stable long-term system performance.

High-end automation systems frequently prioritize wired connectivity for lighting control, centralized entertainment systems, HVAC management, and integrated security infrastructure. Wired systems remain particularly relevant where uninterrupted performance and low network dependency are operational priorities. Large residential properties often benefit from wired infrastructure because stable communication reduces connectivity interruptions across extensive device ecosystems.

Installation complexity remains a key adoption constraint. Wired systems generally require professional deployment, structural modifications, and higher upfront investment, limiting suitability for retrofit environments. Consumers seeking flexible or incremental automation frequently prefer wireless alternatives because deployment costs and installation barriers remain comparatively lower.

By Device Type

To know how our report can help streamline your business, Speak to Analyst

Rising Adoption of Smart Entertainment Devices to Enhance User Experience Fostered Segment Expansion

Based on device type, the market is studied into safety & security access control, home appliances, HVAC, lighting control, smart entertainment devices, smart kitchen appliances, and others (smart furniture, home healthcare, etc.).

Safety & Security Access Control

Safety and security access is anticipated to grow at a prominent CAGR during the forecast period. Security cameras and video doorbells have become a major part of smart home security systems. Manufacturers are continually improving these devices with features such as two-way audio, motion detection, and high-definition video recording. Integration with cloud storage allows homeowners to review and access footage remotely, boosting security and market growth.

Safety and security access control devices continue accounting for a major share of the smart home market because security-related use cases frequently represent the first entry point into connected residential ecosystems. Video doorbells, connected surveillance cameras, smart locks, biometric entry systems, alarm systems, and motion sensors continue demonstrating strong adoption across both single-family and multi-unit housing environments. Consumer willingness to invest in security technologies generally remains stronger than discretionary automation spending because perceived value is immediate and measurable.

Remote monitoring functionality continues to strengthen demand behavior. Homeowners increasingly prioritize real-time notifications, mobile device integration, cloud video storage, and two-way communication features to improve visibility and property awareness. Urban residential density, rising parcel delivery activity, and household safety concerns continue supporting adoption momentum across developed and emerging markets.

Smart entertainment devices captured the largest market share in 2026. The rising adoption of home entertainment systems to control several smart devices, play music, and deliver news and weather information to enhance the user experience boosts the demand for smart entertainment devices. The Smart Entertainment Devices segment is projected to dominate the market with a share of 28.78% in 2026.

Home Appliances

Connected home appliances continue expanding their role within the smart home market as consumers increasingly prioritize convenience, energy efficiency, and remote management capabilities. Refrigerators, washing machines, dishwashers, ovens, robotic vacuum cleaners, and connected water systems increasingly incorporate automation features designed to improve operational visibility and optimize household routines. Smart appliance adoption continues to strengthen in higher-income households and digitally connected residential environments.

Manufacturers increasingly position connected appliances around measurable efficiency rather than novelty. Predictive maintenance alerts, remote diagnostics, automated scheduling, and electricity optimization capabilities continue to improve practical household value. Appliance manufacturers increasingly integrate artificial intelligence and sensor-driven monitoring to improve operational performance and reduce unnecessary energy consumption.

Interconnectivity continues to become more important across appliance ecosystems. Consumers increasingly favor products capable of integrating with centralized control platforms and voice-enabled assistants. Device compatibility increasingly influences purchasing decisions because fragmented ecosystems may reduce convenience and limit automation effectiveness.

Price sensitivity continues affecting broader adoption, particularly in emerging markets where connected appliances typically command premium pricing. However, replacement cycles, energy efficiency concerns, and smart ecosystem expansion continue supporting long-term smart home market growth across appliance categories.

HVAC

Heating, ventilation, and air conditioning (HVAC) systems continue to represent one of the most commercially significant categories within the smart home market because energy management remains a primary consumer motivation for automation investment. Connected thermostats, climate monitoring systems, occupancy sensors, and automated temperature controls increasingly support household electricity optimization and comfort management.

Energy cost awareness continues driving HVAC adoption. Consumers increasingly deploy connected climate systems to reduce unnecessary electricity usage through scheduling automation, remote temperature control, and occupancy-based optimization. Utilities in several markets continue supporting smart thermostat adoption through incentive programs and demand-side energy initiatives.

HVAC automation also continues strengthening within new construction environments where connected climate infrastructure can be integrated during building design. Retrofit opportunities remain equally important because wireless thermostats and sensor systems generally require limited structural modification. This flexibility broadens adoption across both legacy housing and newly developed properties.

Integration with broader smart home ecosystems increasingly improves value perception. HVAC systems increasingly communicate with occupancy sensors, weather forecasting platforms, and energy management tools to optimize performance. As residential electrification expands, HVAC systems are expected to remain a major contributor to smart home market share and connected energy management strategies.

Lighting Control

Lighting control systems continue to represent one of the most widely adopted categories within the smart home market due to relatively low installation complexity and measurable energy-saving potential. Smart bulbs, connected switches, dimmers, occupancy sensors, and automated lighting schedules increasingly support convenience, energy optimization, and residential personalization. Adoption remains particularly strong among consumers seeking entry-level automation without substantial upfront investment.

Wireless deployment flexibility continues strengthening demand. Consumers frequently adopt lighting control technologies because installation generally requires limited structural modification and integrates easily with smartphones or voice-enabled ecosystems. Automated lighting scenes, motion-triggered controls, and remote access capabilities increasingly improve convenience while supporting household energy management objectives.

Smart Entertainment Devices

Smart entertainment devices continue accounting for a substantial portion of the smart home market because media consumption habits increasingly depend on connected ecosystems and digital streaming services. Smart televisions, voice-enabled speakers, streaming hubs, connected gaming systems, and multi-room audio technologies continue gaining traction as households prioritize seamless entertainment access and centralized control functionality.

Smart Kitchen Appliances

Smart kitchen appliances continue gaining relevance within the smart home market as consumers increasingly prioritize convenience, energy efficiency, and time optimization across food preparation and household management activities. Connected refrigerators, ovens, coffee makers, dishwashers, microwaves, and cooking systems increasingly integrate remote monitoring, automated scheduling, and predictive maintenance features to improve everyday functionality.

Regional Insights

By region, the market is categorized into North America, Europe, Asia Pacific, the Middle East & Africa, and South America.

North America Smart Home Market Analysis

North America Smart Home Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North American market was valued at USD 46.8 billion in 2025, capturing 31.70% of global revenue, and is estimated to reach USD 56.29 billion in 2026, owing to the presence of major players, including Honeywell International Ltd, Snap One LLC, SmartRent LLC, Creston Corporation, and others. Key players in the region are adopting strategies such as acquisition, partnership, and product launches to expand their business, enhance their presence, and improve their customer base. For instance,

- In October 2024, Develco Products acquired Datek Smart Home, one of three divisions of the Norwegian company Datek. With this acquisition, the two companies offer dedicated white-label cloud services and IoT hardware for home care, smart energy, and security providers in North America.

North America continues to represent a major smart home market due to high broadband penetration, strong consumer familiarity with connected devices, and established digital infrastructure. Safety systems, connected entertainment, and energy management technologies continue supporting adoption. Utility partnerships, subscription-based services, and residential renovation activity increasingly contribute to smart home market growth across urban and suburban housing environments.

Download Free sample to learn more about this report.

United States Smart Home Market

The US market is projected to reach USD 35.28 billion by 2026, owing to the growing number of tech-savvy consumers in the country. According to the Enterprise Apps Today survey 2023, the total number of smart homes in the U.S. is expected to reach USD 35.28 billion by 2026. Furthermore, household penetration is expected to grow 39% by 2027.

The United States accounts for a substantial share of the smart home market because of advanced connectivity infrastructure, strong technology adoption, and extensive product availability. Consumer demand increasingly favors integrated security systems, connected appliances, and intelligent energy management technologies. Broadband accessibility, home renovation activity, and ecosystem partnerships continue supporting smart home market size expansion.

Europe Smart Home Market Analysis

In 2025, Europe held 28.70% of the global market, reaching a valuation of USD 42.39 billion, and is projected to grow to USD 51.97 billion in 2026. There are major factors that drive the market, including the rising number of IoT services, government initiatives, and integrations of various technologies such as Artificial Intelligence and Machine Learning. The UK market is projected to reach USD 12.29 billion by 2026, while the German market is projected to reach USD 12.72 billion by 2026. For instance,

- The European Commission stated that 266 million electric smart meters are expected to be installed in the EU by 2030.

- In May 2023, Sky and Zurich Insurance unveiled a smart home protection IoT service that offers customers smart home tech products and comprehensive home insurance.

Europe remains an important smart home market supported by energy efficiency priorities, sustainability regulations, and increasing residential digitalization. Connected heating, ventilation, and air conditioning (HVAC) systems, intelligent lighting, and home security technologies continue gaining traction. Rising electricity costs and building efficiency requirements increasingly strengthen regional smart home market growth and energy automation demand.

Germany Smart Home Market:

Germany continues to contribute significantly to the smart home market due to strong residential energy efficiency priorities and advanced building automation adoption. Connected heating systems, smart thermostats, and intelligent lighting controls remain commercially important. Sustainable construction practices, digital infrastructure improvements, and increasing demand for energy management technologies continue to strengthen smart home market development.

United Kingdom Smart Home Market:

The United Kingdom smart home market continues to expand through growing demand for residential security technologies, connected entertainment systems, and intelligent heating controls. Rising household energy costs increasingly support the deployment of smart thermostats and monitoring systems. Broadband penetration, home renovation activity, and connected service ecosystems continue supporting long-term smart home market growth.

Asia-Pacific Smart Home Market Analysis:

The market in the Asia Pacific reached USD 34.2 billion in 2025, representing 25.50% of total market revenue, and is expected to reach USD 42.46 billion in 2026. The Asia Pacific market is driven by many factors, including energy saving, a rising number of IoT-connected devices, regulatory initiatives by the government, awareness of sustainable ecosystems, and others.

Moreover, increasing demand for smart consumer electronics is also a growth factor that is driving the market in the region. Companies are launching many innovative products and solutions that aid consumers in a better, more sustainable life. The Japan market is projected to reach USD 9.15 billion by 2026, the China market is projected to reach USD 14.34 billion by 2026, and the India market is projected to reach USD 6.97 billion by 2026. For instance,

- In January 2025, Dreame Technology launched a series of smart home appliances at CES 2025, comprising the X50 Ultra robot vacuum with advanced detangling features and obstacle navigation.

Asia-Pacific accounts for a substantial smart home market share due to urbanization, residential construction growth, and expanding digital connectivity. China, Japan, South Korea, and India continue influencing regional demand across connected appliances, entertainment systems, and residential automation technologies. Rising middle-income households and smartphone penetration continue to strengthen smart home market expansion.

Japan Smart Home Market:

Japan continues supporting smart home market growth through advanced consumer electronics adoption, residential automation demand, and aging population requirements. Connected healthcare monitoring, intelligent appliances, and energy management technologies continue gaining traction. Smart housing initiatives, technological innovation, and strong digital infrastructure continue supporting connected residential ecosystem development.

China Smart Home Market:

China represents one of the largest smart home market participants due to rapid urbanization, connected device manufacturing leadership, and increasing household digitalization. Smart appliances, surveillance technologies, and connected entertainment systems continue witnessing strong demand. Residential construction growth, digital platform integration, and expanding broadband access continue to strengthen the smart home market size.

Middle East & Africa

In 2025, the Middle East & Africa market stood at USD 15.45 billion, representing 24.70% of global demand, and is expected to reach USD 18.96 billion in 2026. The Middle East & Africa region is witnessing higher demands for smart consumer electronics and home appliances. The smart entertainment category, especially TV’s the main growth factor for the market. For instance,

- According to industry analysis, around 8.73 million smart home devices were shipped across the META region, which is an increase of 35.1 % from the last year. The introduction of 5G in the GCC region and the acceptance of 4G in most countries within the META region have also added to the growth of the market.

The Middle East & Africa continue to witness a gradual smart home market expansion supported by premium residential development, urban digitalization, and rising demand for connected security technologies. Smart lighting, climate management, and surveillance systems continue gaining adoption. Infrastructure development and increasing residential connectivity continue to support long-term market growth.

Latin America

Latin America maintained a strong presence in the global market, reaching USD 8.68 billion in 2025, accounting for 21.70% share, and is expected to reach USD 10.45 billion in 2026. Latin America continues demonstrating gradual smart home market growth through increasing smartphone penetration, residential connectivity improvements, and rising interest in home security technologies. Connected surveillance systems and smart appliances continue attracting demand across urban housing markets. Broadband expansion, urbanization, and increasing digital familiarity continue supporting regional smart home market development.

Smart Home Industry Competitive Landscape

Product Enhancement & Innovation among Key Players to Propel Market Growth

Players in the market are upgrading their existing solutions and innovating new ones to expand their business and meet customer needs. The enhancement and expansion of the current product portfolio raise the position of vendors in the market.

The smart home market demonstrates a fragmented yet increasingly platform-driven competitive structure shaped by consumer electronics manufacturers, software ecosystem providers, home security companies, telecommunications operators, and specialized automation vendors. Competition increasingly extends beyond hardware performance toward interoperability, ecosystem integration, software functionality, and recurring service models. Companies increasingly differentiate through connected ecosystems rather than standalone device capabilities.

Major global vendors continue strengthening competitive positioning through integrated product portfolios spanning security, lighting, climate control, appliances, and entertainment systems. Large technology providers increasingly prioritize ecosystem lock-in by enabling centralized device management through proprietary applications, cloud platforms, and voice-enabled digital assistants. Cross-device compatibility increasingly influences market positioning because consumers generally prefer unified control environments over fragmented automation systems.

Home security companies remain important participants within the smart home industry due to recurring subscription revenue and strong consumer trust around safety technologies. Connected surveillance systems, access control devices, and professional monitoring services continue expanding through bundled service models. Telecommunications providers also continue strengthening market relevance by integrating smart home offerings with broadband subscriptions, managed connectivity services, and home network infrastructure.

Emerging players increasingly focus on specialized automation niches, including intelligent energy management, connected healthcare monitoring, occupancy analytics, and predictive maintenance technologies. Smaller firms frequently compete through software differentiation, interoperability solutions, and niche use cases underserved by larger ecosystem providers. Strategic partnerships increasingly help specialized companies strengthen distribution reach and platform compatibility.

List of Top Smart Home Companies Profiled

- Honeywell International, Inc. (U.S.)

- ABB (Switzerland)

- Johnson Controls International plc (Ireland)

- Siemens (Germany)

- Alphabet, Inc. (U.S.)

- Emerson (U.S.)

- Robert Bosch Smart Home GmbH (Germany)

- Samsung (South Korea)

- LG Electronics (South Korea)

- Crestron Electronics, Inc. (U.S.)

- Apple, Inc. (U.S.)

- Ecobee (Canada)

- Schneider Electric (France)

- Vivint, LLC (U.S.)

- Fantasia Trading LLC (U.S.)

- Snap One, LLC (U.S.)

- Govee (China)

- Xiaomi (China)

- Signify Holdings (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- March 2025: Samsung Electronics expanded Matter protocol integration across its SmartThings ecosystem to improve interoperability between connected residential devices and strengthen multi-brand compatibility. The initiative focused on centralized home management capabilities, artificial intelligence-enabled automation, and cross-platform communication technologies to reduce ecosystem fragmentation within smart home environments.

- January 2025: Google introduced expanded artificial intelligence capabilities within Google Home to improve predictive automation, voice interaction accuracy, and household device coordination. The strategy aimed to strengthen ecosystem engagement through machine learning-enabled routines, contextual automation, and enhanced compatibility across connected residential technologies.

- In January 2025, ABB acquired Lumin, a U.S.-based provider and pioneer of energy management systems. This acquisition will help to expand the company’s home energy management abilities in the North American residential sector.

- In January 2025, LIFX, the smart lighting company, and Feit Electric introduced four new lighting products at CES. From Katalyst's collection of ceiling and Feit’s Vista Skylight LED Fixtures to Luna Smart Lamp and LIFX’s futuristic smart oval supercolor ceiling light. These additions offer unmatched customization, versatility, and simplicity, available entirely at The Home Depot.

- In October 2024, ABB and Austrian-based Zumtobel Group, a professional lighting solutions provider, partnered aimed at innovating smart building solutions. The partnership will help to create significant added value for customers in multiple sectors by offering smart and integrated solutions for smart buildings.

- In August 2024, Huawei Digital Power launched its “Smart Home Energy” solution in the Philippines. This will help the country to achieve a sustainable and energy-efficient future.

- In October 2022, ASSA ABLOY acquired Bird Home Automation GmbH, a German company specializing in IP door intercoms for single and multifamily buildings. This strategic acquisition will be crucial in ASSA ABLOY’s expansion into the growing smart home market.

INVESTMENT ANALYSIS AND OPPORTUNITIES

Investment in smart home technology is increasing, driven by increasing consumer demand for energy efficiency, convenience, and security. Key players like Amazon (Alexa), Google (Nest), and Apple (HomeKit) are growing their ecosystems through strategic acquisitions and R&D. Startups such as Wyze and Ecobee are attracting venture capital for innovative, affordable solutions. Asia-Pacific, especially India and China, is emerging as a high-growth market due to urbanization and rising disposable incomes. The integration of IoT and AI is creating new monetization models through data analytics and subscription services. Overall, the market offers strong mid-to-long-term ROI potential for both institutional and corporate investors.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product/service types, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 21.40% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Application

By Protocol

By Device Type

By Region

|

|

Companies Profiled in the Report |

|

Frequently Asked Questions

The market is projected to reach USD 848.47 billion by 2034.

In 2025, the market was valued at USD 147.52 billion.

The market is projected to grow at a CAGR of 21.40% during the forecast period of 2026 – 2034.

By device type, the smart entertainment device segment led the market.

Integration of advanced technologies with smart home appliances to Drive the Market

ABB, Alphabet, Samsung, and Emerson are the top players in the market.

North America is expected to hold the highest market share.

- 2021-2034

- 2025

- 2021-2024

- 90

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us