3D Printing Materials Market Size, Share & Industry Analysis, By Type (Plastics, Metals, Ceramics, and Others), By Application (Automotive, Aerospace & Defense, Industrial, Medical, Consumer Products, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

3D Printing Materials Market Size and Industry Overview

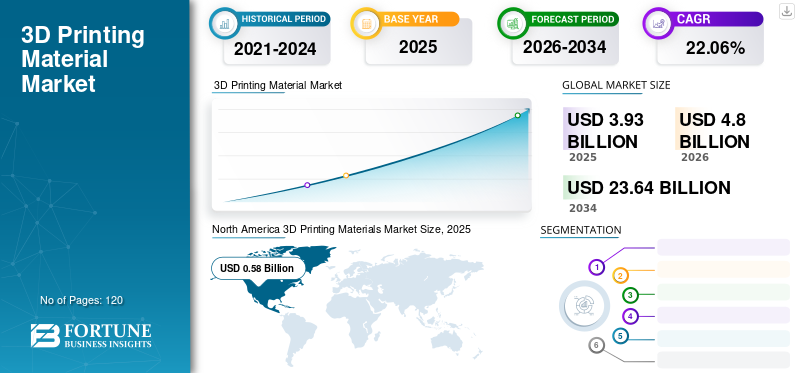

The global 3D printing materials market size was valued at USD 4.29 billion in 2025. The market is projected to grow from USD 4.95 billion in 2026 to USD 23.67 billion by 2034, exhibiting a CAGR of 21.6% during the forecast period. North America dominated the global market with a market share of 40.33% in 2025.

3D printing materials are specialized feedstocks used in additive manufacturing processes to create complex components layer by layer. These materials include plastics, metals, ceramics, and advanced composites tailored for applications across automotive, aerospace & defense, industrial manufacturing, healthcare, and consumer products. Compared to conventional manufacturing, additive manufacturing reduces material waste, shortens prototyping cycles, and enables highly customized production. Growing adoption of Industry 4.0 technologies, increasing demand for lightweight components, and rising investments in advanced manufacturing are significantly supporting market growth. Additionally, improvements in material performance, including heat resistance, mechanical strength, and biocompatibility, are expanding the range of end-use applications. As manufacturers increasingly prioritize design flexibility, rapid product development, and production efficiency, demand for high performance 3D printing materials continues to accelerate, thus strengthening the long-term outlook of the global market.

The major players operating in the market are Stratasys Ltd., Materialise NV, Arkema SA, and Evonik Industries AG.

Download Free sample to learn more about this report.

3D PRINTING MATERIALS MARKET TRENDS

Industrialization of Additive Manufacturing and High-Performance Material Development are Reshaping Demand

The market is witnessing a shift from rapid prototyping toward end-use part production, increasing demand for engineering-grade materials. Manufacturers are developing advanced polymers, metal powders, and ceramic materials with enhanced mechanical and thermal properties to support industrial-scale production. Additionally, aerospace and automotive industries are increasingly utilizing lightweight materials to improve fuel efficiency and component performance. The emergence of sustainable and bio-based printing materials is also gaining attention as environmental concerns grow. Furthermore, advancements in multi-material printing and high-speed additive manufacturing technologies are expanding commercial applications. These technological developments and industrial adoption trends are reshaping material demand patterns, thus driving continued evolution of the market.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Demand for Lightweight Components and Rapid Prototyping to Drive Market Growth

The primary driver of the market is the growing need for lightweight, high-performance components across automotive and aerospace industries. 3D printing enables complex geometries while reducing material waste and production lead times. Rapid prototyping capabilities also accelerate product development cycles, allowing manufacturers to bring products to market faster. Additionally, increasing healthcare applications and expanding industrial automation are reinforcing material consumption. Continuous advancements in material science further improve performance characteristics and broaden application possibilities. These efficiency, customization, and performance advantages collectively sustain strong market demand, thus maintaining 3D printing materials market growth.

MARKET RESTRAINTS

High Material Costs and Limited Standardization Restricting Wider Adoption

Advanced 3D printing materials, particularly metal powders and specialty polymers, remain significantly more expensive than conventional manufacturing materials. Additionally, limited material standardization across industries can create qualification and certification challenges. High equipment costs and specialized processing requirements may also restrict adoption among small and medium-sized enterprises. Material performance limitations in certain high-volume production applications further constrain market penetration. These cost and standardization-related factors create adoption barriers, hence moderating market growth in some sectors.

MARKET OPPOTUNITIES

Mass Customization and Healthcare Innovation Creating Long-Term Growth Potential

Significant opportunities exist in customized manufacturing and patient-specific healthcare solutions. The medical sector is increasingly utilizing 3D printing materials for dental devices, orthopedic implants, prosthetics, and surgical guides. Additionally, automotive manufacturers are adopting additive manufacturing for lightweight components and low-volume production runs. Expansion of localized manufacturing and digital inventory management systems further supports material demand. Emerging applications in electronics, construction, and energy sectors provide additional growth avenues. Increasing adoption of additive manufacturing in developing economies and growing investments in smart factories are expected to further strengthen market penetration. As industries continue to prioritize customization and production flexibility, demand for advanced 3D printing materials is expected to rise steadily, therefore supporting long-term market growth.

MARKET CHALLENGES

Material Qualification Requirements and Supply Chain Constraints Influencing Market Development

A major challenge in the market is ensuring material consistency and certification for critical applications such as aerospace, defense, and medical devices. Manufacturers must comply with stringent quality standards and performance validation requirements. Additionally, supply chain limitations for high-purity metal powders and specialty materials can affect production reliability. Balancing material performance, printability, and cost remains a key challenge for material developers. These technical and regulatory complexities influence commercialization timelines, therefore shaping competitive dynamics within the market.

RESEARCH AND DEVELOPMENT TRENDS

R&D activities are focused on developing stronger, lighter, and more sustainable materials for additive manufacturing. Innovations include high-performance thermoplastics, aerospace-grade metal powders, bio-based polymers, and advanced ceramic materials. Multi-material printing capabilities and recyclable feedstocks are also emerging as key innovation areas.

SEGMENTATION ANALYSIS

By Type

Plastics Segment to Hold Dominant Share Owing to Broad Compatibility with Various 3D Printing Technologies

Based on type, the market is segmented into plastics, metals, ceramics, and others.

Plastics segment hold the largest 3D printing materials market share, due to their cost-effectiveness, ease of processing, and broad compatibility with various 3D printing technologies. Growing adoption of additive manufacturing across automotive, aerospace, defense, and industrial sectors is significantly driving demand for high-performance plastic materials. Additionally, plastics enable rapid prototyping, complex design fabrication, reduced component weight, and minimal material wastage, making them highly attractive for manufacturers seeking efficient production solutions. These advantages continue to strengthen the segment’s dominant position in the global market.

The metals segment is expected to witness the significant growth during the forecast period. Metal materials are increasingly preferred in healthcare applications for manufacturing customized implants, prosthetics, and surgical components due to their superior strength and durability. Moreover, the ability of metal additive manufacturing to produce complex parts with minimal material loss and shorter production cycles is accelerating adoption. Rising utilization of 3D-printed metal components in aerospace, automotive, and industrial machinery applications is further supporting market growth. As industries increasingly seek lightweight, high-performance, and precision-engineered parts, demand for metal-based 3D printing materials is expected to expand rapidly with a CAGR of 21.4% throughout the forecast period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Aerospace & Defense Segment Dominated Market Owing to Enhanced Design Flexibility and Lower Material Waste

Based on application, the market is segmented into automotive, aerospace & defense, industrial, medical, consumer products, and others.

Aerospace & defense segment held the largest market share in 2025. This is due to the extensive use of additive manufacturing for producing lightweight, complex, and high-performance components. Aircraft parts such as engine components, brackets, tooling fixtures, and structural elements are increasingly manufactured using 3D printing materials, particularly metals and advanced polymers. The 3D printing technology enables significant weight reduction, enhanced design flexibility, lower material waste, and improved dimensional precision, making it highly valuable for aerospace and defense applications. These benefits continue to accelerate adoption across the sector, supporting the segment’s dominant market position.

The automotive segment is expected to witness substantial growth during the forecast period. Automotive manufacturers are increasingly utilizing 3D printing materials, including plastics and metals, for rapid prototyping, tooling, and production of lightweight components. The ability to create complex geometries with high dimensional accuracy while reducing production time and material consumption has made additive manufacturing an attractive solution for the industry. Furthermore, the growing production of electric vehicles and the increasing focus on vehicle lightweighting to improve fuel efficiency and performance are driving demand for advanced 3D printing materials. As a result, the expanding automotive sector is expected to significantly contribute to market growth by growing at a CAGR of 21.8% during the forecast period.

3D PRINTING MATERIALS MARKET REGIONAL OUTLOOK

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America 3D Printing Materials Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America is a leading market for 3D printing materials, supported by strong aerospace, defense, healthcare, and automotive industries. The U.S. accounts for the majority of regional demand due to significant investments in additive manufacturing technologies and advanced material development. Aerospace manufacturers increasingly utilize metal powders and engineering plastics for lightweight, high-performance components, while the healthcare sector drives demand for customized implants, prosthetics, and medical devices. Additionally, the growing use of additive manufacturing for rapid prototyping and low-volume production supports material consumption. These technological advancements and industrial investments continue to strengthen regional market growth.

U.S. 3D Printing Materials Market

The U.S. market accounted for USD 1.52 billion in 2025, accounting for approximately 35.4% of global revenues. Growth is driven by increasing adoption of the 3D printing materials in aerospace, defense, and healthcare industries for high-performance and customized components.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe represents a significant market for 3D printing materials, driven by strong automotive, aerospace, and industrial manufacturing sectors. Germany, the U.K., France, and Italy are increasingly adopting additive manufacturing to improve production efficiency and reduce material waste. Automotive manufacturers utilize 3D printing materials for prototyping, tooling, and lightweight component production, while aerospace companies employ advanced metal and polymer materials for complex applications.

Germany 3D Printing Materials Market

Germany’s market accounted for USD 0.26 billion in 2025, equivalent to around 6.0% of global revenues. Growth is fueled by strong automotive manufacturing activity and increasing use of 3D printing materials for prototyping and lightweight vehicle components.

Asia Pacific

Asia Pacific is the fastest-growing market for 3D printing materials due to rapid industrialization and expanding manufacturing capabilities. China, Japan, South Korea, and India are major contributors, supported by growing automotive, electronics, aerospace, and healthcare industries. China remains a key manufacturing hub and continues to invest heavily in additive manufacturing technologies, while Japan and South Korea focus on precision industrial applications. Rising demand for customized products, rapid prototyping, and advanced manufacturing solutions is increasing material consumption. Government initiatives promoting digital manufacturing and Industry 4.0 adoption further support market growth, thus strengthening Asia Pacific’s position in the global market.

China 3D Printing Materials Market

China’s market accounted for USD 0.57 billion in 2025, representing approximately 13.2% of global revenues. Growth is driven by large-scale manufacturing expansion, government support for additive manufacturing, and rising industrial applications.

India 3D Printing Materials Market

The Indian market accounted for USD 0.07 billion in 2025. Expansion is fueled by increasing adoption of Industry 4.0 technologies, growing automotive production, and expanding healthcare infrastructure.

Latin America and Middle East & Africa

Latin America is witnessing gradual growth in the market, supported by industrial modernization and increasing adoption of advanced manufacturing technologies. Brazil and Mexico lead regional demand due to their established automotive and industrial sectors. Companies are increasingly utilizing additive manufacturing for rapid prototyping, tooling, and product development to improve efficiency and reduce costs. The healthcare sector is also adopting 3D printing technologies for dental and orthopedic applications. The Middle East & Africa market is experiencing steady growth due to increasing investments in advanced manufacturing and healthcare infrastructure. GCC countries, particularly the UAE and Saudi Arabia, are promoting additive manufacturing through smart manufacturing and industrial diversification initiatives. The healthcare sector is increasingly adopting 3D printing for customized implants, prosthetics, and surgical planning models.

GCC 3D Printing Materials Market

The GCC market accounted for USD 0.05 billion in 2025, representing approximately 1.3% of regional revenues. Expansion is fueled by industrial diversification programs and investments in advanced manufacturing technologies under Vision 2030.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players to Focus on Material Innovation and Strategic Expansion to Strengthen Market Presence

The global 3D printing materials market is moderately fragmented, with competition primarily driven by product innovation, material performance, and application diversity. Leading companies focus on expanding their portfolios of plastics, metals, ceramics, and specialty materials to address the evolving requirements of automotive, aerospace & defense, medical, and industrial sectors. Continuous investments in research and development are aimed at enhancing mechanical properties, improving printability, and reducing material costs to strengthen market competitiveness. Additionally, manufacturers are increasingly pursuing strategic initiatives such as capacity expansions, partnerships, joint ventures, acquisitions, and new product launches to broaden their market presence. The growing adoption of additive manufacturing across multiple industries continues to encourage innovation, therefore intensifying competition among global and regional material suppliers along with fueling market growth during the forecast period.

LIST OF KEY 3D PRINTING MATERIALS COMPANIES PROFILED IN REPORT

- Stratasys Ltd. (Israel)

- 3D Systems, Inc. (U.S.)

- Materialise NV (Belgium)

- Markforged, Inc. (U.S.)

- EOS GmbH (Germany)

- Höganäs AB (Sweden)

- ExOne (Germany)

- Arkema SA (France)

- Evonik Industries AG (Germany)

- BASF SE (Germany)

- Augment3Di (India)

- Solvay SA (Belgium)

- American Elements (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Stratasys added new 3D printing materials, including ULTEM 1010 filament, P3 Deflect 110 resin, Loctite 3D IND3785 Low Migration, PolyJet ToughONE White and Black, and Somos WaterShed White.

- January 2026: 3D Systems expanded its NextDent Jetted Denture material offering with three new base shades, NextDent Jet Base DP, LP, and RP, for dental additive manufacturing applications.

- November 2025: 3D Systems introduced Accura SbF, an SLA casting resin for QuickCast investment casting patterns, and Accura Xtreme Black, a high-performance SLA prototyping resin for durable functional parts.

- May 2025: Stratasys acquired assets from Forward AM GmbH, a Germany-based BASF spin-off, expanding its advanced 3D printing materials portfolio and strengthening its capabilities in Selective Absorption Fusion (SAF) and Digital Light Processing (DLP) technologies.

- June 2024: Materialise partnered with ArcelorMittal Powders to integrate Materialise’s next-generation build processor with ArcelorMittal’s AdamIQ steel powders, supporting productivity, quality, and cost-efficiency in metal 3D printing.

REPORT COVERAGE

The 3D printing materials market report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading applications of the product. Besides this, the report offers insights into the market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 21.6% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Application, and Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 4.29 billion in 2025 and is projected to reach USD 23.67 billion by 2034.

In 2025, the North America’s market value stood at USD 1.73 billion.

Growing at a CAGR of 21.6%, the market will exhibit steady growth during the forecast period.

North America held the highest market share in 2025.

Demand for lightweight components and rapid prototyping is driving the market.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us