AC Servo Motors and Drives Market Size, Share & Industry By Product Type (Servo Motors (Synchronous and Induction) and Servo Drives), By Voltage Range (Low Voltage, Medium Voltage, and High Voltage), By Phase Type (Two-Phase and Three-Phase), By Communication Protocol (Fieldbus, Industrial Ethernet, and Wireless), By End-Use Industry (Aerospace & Defense, Automotive and Transportation, Semiconductor and Electronics, Printing & Packaging, Food & Beverage, Chemicals and Petrochemicals, and Others), and Regional Forecast, 2026-2034

AC Servo Motor Market Size and Industry Overview

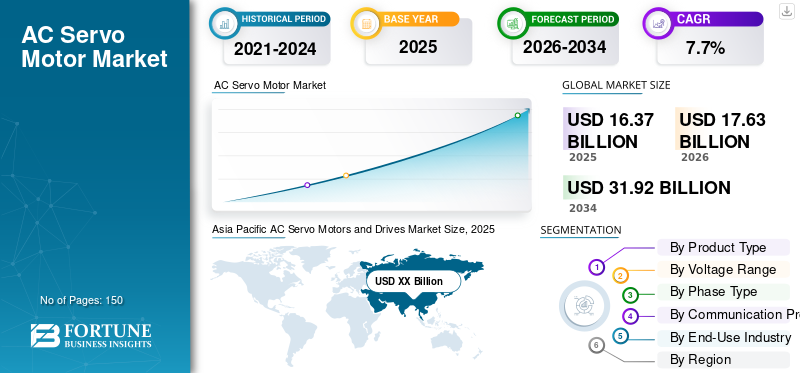

The global ac servo motors and drives market size was valued at USD 16.37 billion in 2025. The market is projected to grow from USD 17.63 billion in 2026 to USD 31.92 billion by 2034, exhibiting a CAGR of 7.70% during the forecast period. Asia Pacific dominated the AC servo motors and drives market with a market share of 34.56% in 2025.

The AC servo motors and drives market occupies a central role within modern industrial automation, enabling precise motion control across digitally integrated production environments. Demand is closely tied to capital investment cycles in manufacturing, robotics adoption, and the broader transition toward intelligent factories. As industries pursue higher throughput, tighter tolerances, and improved energy efficiency, AC servo motors and drives increasingly replace traditional motor systems in both discrete and process automation.

Market size expansion reflects sustained uptake across automotive manufacturing, electronics assembly, packaging, and emerging applications in aerospace, semiconductors, and advanced materials processing. AC servo systems offer closed-loop control, rapid response, and positional accuracy, which are essential for high-speed, multi-axis operations. These capabilities support productivity gains while reducing scrap rates and unplanned downtime. As a result, the AC servo motors and drives market continues to register steady growth across developed and industrializing economies.

From a technology perspective, integration between servo motors, drives, sensors, and industrial controllers is deepening. Vendors increasingly deliver bundled motion platforms rather than standalone components, simplifying commissioning and lifecycle management. Improvements in power electronics, digital signal processing, and thermal design enhance torque density and reliability. These advances contribute directly to rising AC servo motors and drives market share within high-performance automation segments.

End users increasingly evaluate suppliers on total cost of ownership rather than upfront pricing. Factors such as energy efficiency, predictive maintenance capabilities, software compatibility, and global service support influence procurement decisions. This shifts competition toward vendors with strong ecosystems and long-term support models.

Regionally, Asia-Pacific represents the largest consumption base, supported by large-scale manufacturing capacity and rapid automation adoption. North America and Europe maintain strong demand driven by reshoring initiatives, labor constraints, and modernization of legacy production assets. Across regions, the AC servo motors and drives industry remains resilient, supported by long-term structural demand for precision, flexibility, and digitally enabled motion control.

The AC servo motors and drives together form a closed-loop control system that utilizes position feedback to control its speed, motion, and final position. The market growth can be further attributed to an increased demand for servo motors and drives from the industrial manufacturing sector to design and develop more automated closed-loop control machinery. The closed-loop AC servo system provides several advantages, including high stability, low sensitivity to parameter variation, and enhanced performance.

The various industry verticals such as automotive, semiconductor and electronics, printing & packaging, paper, textile, food & beverage, chemicals, and petrochemicals need modern machinery for large volume production. Therefore, the increasing trend towards adopting industry automation technology to cater to the high product demand is expected to contribute to the growth of the market.

Recently, in September 2020, Yaskawa Electric Corporation announced that the company’s AC servo motor shipments reached 20 million units in August 2020. In February 2012, the company shipped 10 million units of the cumulative AC servo motor and presently offers a wide range of servo motors and drives for motion control applications.

According to the International Federation of Robotics, the demand for cleaning and medical robots has increased during the COVID-19 pandemic. It further states that these robots help deliver supplies across hospitals and support doctors in performing temperature and other checks. These factors are increasing the demand for AC servo motors and drives.

Download Free sample to learn more about this report.

AC Servo Motors and Drives Market Key Takeaways

- 2025 Market Size: USD 16.37 billion

- 2026 Market Size: USD 17.63 billion

- 2034 Forecast Market Size: USD 31.92 billion

- CAGR: 7.70% from 2026–2034

- Asia Pacific dominated the AC servo motors and drives market with a 34.56% share in 2025.

- The servo motors segment held the largest market share.

- The low voltage segment accounted for the largest market share.

Asia Pacific

Held a 34.56% market share and was valued at USD 2.35 billion in 2025.

North America

Held a significant market share, driven by rising industrial automation.

Europe

Expected to witness significant market growth during the forecast period.

U.S

Demand is driven by advanced manufacturing, semiconductor, and automotive industries.

Japan

The market is supported by strong robotics and precision manufacturing industries.

Read More

Key Market Dynamics

Market Trends

Download Free sample to learn more about this report.

Growing Adoption of Industrial Automation Technology to Boost Product Demand

Major industry verticals are adopting automation technology to enhance their production efficiency and capabilities. Additionally, automation aids in reducing human error during the manufacturing process. The growing penetration of emerging technologies such as artificial intelligence, machine learning, and the internet of things (IoT) in industrial manufacturing is further driving the demand for more automated, controlled, and connected industry solutions.

- Asia Pacific witnessed AC servo motors and drives market growth from USD 2.24 Billion in 2018 to USD 2.35 Billion in 2019.

A smart, automated solution can reduce production costs by properly organizing the manufacturing process. Moreover, emerging economies' increasing spending on industrial automation is likely to boost the market for AC servo motors and drives. Besides, the growing development of micro-sized servo drives with high power is further expected to drive the market for AC servo motors and drive market growth during the forecast period.

A notable trend within the AC servo motors and drives industry is the shift toward integrated motion solutions. Vendors increasingly combine motors, drives, encoders, and control software into compact, pre-engineered packages. This integration reduces wiring complexity, shortens commissioning time, and improves overall system reliability.

Digitalization shapes product evolution. Modern servo drives embed advanced diagnostics, condition monitoring, and parameter optimization algorithms. These features support predictive maintenance strategies, allowing operators to identify wear or misalignment before failures occur. As uptime becomes a strategic metric, such capabilities gain prominence.

Another key trend is the migration toward industrial Ethernet and real-time communication protocols. High-speed data exchange enables precise synchronization across multiple axes and machines. This supports flexible manufacturing cells that can be reconfigured quickly to accommodate changing product designs or volumes.

Miniaturization and higher power density also characterize current market trends. Advances in materials, cooling techniques, and power electronics allow smaller servo motors to deliver higher torque. Compact designs suit space-constrained machinery and mobile automation platforms.

Market Drivers

Growing Demand for AC Servo Systems for Industrial Applications to Aid Market Growth

AC servo motors and drives have several advantages over DC servo systems, such as low noise, constant speed, high torque, high efficiency, and accuracy. Additionally, these systems offer smooth operation and high longevity and flexibility. The AC servo motor can easily deal with a changing voltage than the DC servo motor. Such advantages make AC servo motors an ideal choice for machine tools, aircraft parts, CNC machines, printing machines, food processing machines, home appliances, off-road vehicles, robots, and wafer fabrication machines. Therefore, the AC servo motors and drives demand from several end-use industries, including printing and packaging, food and beverages, textile, healthcare, semiconductor and electronics, aerospace and defense, and robotics, is anticipated to boost the market growth.

Deployment of Smart Machines and Robots for Quality Production to Foster Growth

In recent years, the penetration of industry 4.0 has been significantly high across the world. This has led to the high demand for highly automated, connected machines and robotic systems for quality and cost-effective production. The end-use industries adopt automation to reduce dependency on the workforce and develop a high-quality product with more efficiency and performance. These include aerospace & defense, automotive, semiconductor and electronics, printing & packaging, food & beverage, chemicals and petrochemicals, pharmaceutical, healthcare, and textile

According to the International Federation of Robotics, 373,240 industrial robot units worth USD 13.8 billion were installed worldwide in 2019. The automotive industry installed 28% of robots and 24% of robots by the electronics industry. Moreover, the rising adoption of automated guided vehicles (AGV) and computer numerically controlled (CNC) machines will boost the global AC servo motors and drives market growth in the forthcoming years.

Automation intensity remains the primary growth driver for the AC servo motors and drives market. Manufacturers across automotive, electronics, packaging, and machinery sectors prioritize precise, repeatable motion to meet quality and productivity targets. AC servo systems enable synchronized multi-axis control, which supports complex assembly, high-speed material handling, and adaptive production lines.

Industrial digitization further accelerates adoption. AC servo motors and drives integrate seamlessly with programmable logic controllers, industrial Ethernet networks, and manufacturing execution systems. This connectivity allows real-time monitoring, diagnostics, and optimization. As factories move toward data-driven operations, servo-based motion platforms become foundational assets rather than optional upgrades.

Energy efficiency regulations also play a decisive role. Compared with conventional motors, AC servo systems optimize power consumption by delivering torque only when required. Regenerative drives recover braking energy, lowering overall electricity usage. These features align with corporate sustainability targets and tightening energy standards in major industrial regions.

Labor dynamics contribute additional momentum. Skilled labor shortages push manufacturers to automate tasks that require consistency and precision. Servo-driven systems reduce reliance on manual intervention while maintaining output quality. This dynamic is especially visible in high-cost labor markets.

Market Restraints

Availability of Low-Cost Substitute for AC Servo Motor to Restrain Market Growth

The low-cost substitute for an AC servo motor, which is a brushless DC (BLDC) motor, is expected to hamper the market growth during the forecast period. The configuration of a BLDC motor system is similar to the an AC servo motor. It is powered by a DC source, which generates electricity in alternating current to energize each motor phase via a closed-loop controller. The BLDC motor offers high speed, low maintenance, and low cost, making it suitable for automobiles and several home appliances such as washing machines. However, the AC servo motor provides high consistency, accuracy, and proficiency, making it ideal for highly precise machine applications.

Market Opportunities

Significant opportunities exist for AC servo motors and drives suppliers as automation expands into new domains. Emerging industries such as battery manufacturing, electric vehicle production, and semiconductor fabrication demand extremely precise and repeatable motion. These applications favor advanced servo systems with high accuracy and stability.

Retrofitting legacy production lines represents another growth avenue. Many factories operate aging equipment with limited digital capabilities. Replacing conventional motors with AC servo systems improves performance without requiring complete line replacement. This incremental upgrade approach appeals to cost-conscious manufacturers seeking productivity gains.

Growth in collaborative robotics opens additional opportunities. Collaborative robots require smooth, safe, and responsive motion control. Servo motors and drives designed for low inertia and high feedback resolution align well with these requirements. As collaborative automation spreads beyond pilot projects, demand for specialized servo solutions will increase.

Geographically, industrialization in Southeast Asia, India, and parts of Eastern Europe creates new demand pools. Governments in these regions promote automation to improve manufacturing competitiveness. Local production facilities require scalable, reliable motion technologies, supporting long-term market expansion.

AC Servo Motors and Drives Market Segmentation Analysis

By Product Type Analysis

Growing Adoption of AC Servo Motors Over DC to Aid Market Growth

Based on product type, the market is divided into servo motors and servo drives.

The servo motor product type is further subdivided into synchronous and induction AC servo motors. The servo motors segment is expected to hold the dominant share during the forecast period. This growth is attributed to the rising demand for AC servo motors from manufacturing industries. The synchronous AC servo motor with a permanent magnet provides high performance and accuracy, making it favorable for aircraft parts such as starters, flaps, landing gears, and hydraulic pumps.

Servo motors represent the foundational hardware within the AC servo motors and drives market, translating electrical signals into precise mechanical motion. Synchronous servo motors dominate high-performance applications due to their superior torque control, fast dynamic response, and accurate position holding. These motors rely on permanent magnets and encoder feedback to maintain exact synchronization between electrical input and rotor position. As automation systems demand tighter tolerances and faster cycle times, synchronous servo motors gain preference in robotics, semiconductor fabrication, and precision machining.

Induction servo motors retain relevance in environments where robustness and cost control matter more than ultra-high accuracy. They perform reliably under harsh operating conditions, including elevated temperatures and dust exposure. Induction-based servo systems are commonly deployed in material handling, conveyors, and heavy-duty industrial machinery. Their simpler construction reduces dependency on rare-earth magnets, offering supply chain resilience. Together, synchronous and induction servo motors address a wide performance spectrum, supporting steady AC servo motors and drives market growth across diverse industrial profiles.

The AC servo drives segment is anticipated to display significant growth during the forecast period due to the rising development of more flexible, micro-sized, and next-generation AC servo drives with high power. Moreover, the increasing acceptance of AC servo drives to operate a servo motor in motion control applications will bolster market growth.

Servo drives act as the intelligence layer of motion systems, regulating voltage, current, and frequency supplied to the motor. Advanced servo drives integrate motion control algorithms, safety functions, and communication interfaces within compact enclosures. Their role extends beyond speed control to include position interpolation, torque limiting, and fault diagnostics. Demand for high-performance servo drives grows as manufacturers adopt multi-axis systems requiring precise synchronization.

Modern servo drives increasingly embed digital signal processors and real-time control loops. These features enable adaptive tuning and smoother motion under variable loads. Drives with regenerative braking capabilities further enhance energy efficiency. As factories emphasize reliability and predictive maintenance, servo drives with advanced analytics capabilities capture increasing AC servo motors and drives market share.

By Voltage Range Analysis

To know how our report can help streamline your business, Speak to Analyst

Low Voltage Segment to Augment Largest Market Share

The market is classified into low voltage, medium voltage, and high voltage based on voltage range.

The low-voltage (below 230V) segment held a major market share and is anticipated to grow at the highest CAGR during the forecast period. This growth is attributable to the growing utilization of low-voltage servo motors for mobile robot applications, which require a low maintenance cost.

Low-voltage AC servo motors and drives account for the largest market share due to widespread use in discrete manufacturing and light industrial automation. These systems typically operate below 1 kilovolt and support applications such as packaging, electronics assembly, and collaborative robotics. Low-voltage systems offer easier integration, lower installation costs, and broad component availability. Their compatibility with standard industrial power infrastructure makes them attractive to SMEs seeking scalable automation solutions.

- The Low Voltage segment is expected to hold a 45.2% share in 2019.

The medium (230 - 480V) and high voltage (Above 480V) segments are likely to display stable growth during the forecast period due to the rising use of medium and high voltage servo motors for improved reliability, accuracy, and quality. Medium-voltage servo systems serve heavy industrial environments where higher power levels are required.

Applications include steel processing, large machine tools, and high-capacity material handling equipment. Medium-voltage AC servo motors and drives reduce current levels, improving efficiency and minimizing thermal stress in high-load operations. Although adoption volumes are lower than low-voltage systems, this segment demonstrates stable growth driven by modernization of energy-intensive industries.

High-voltage servo systems occupy a niche position, primarily supporting specialized industrial and defense-related applications. These systems deliver high torque and power density for demanding environments such as naval propulsion systems, aerospace test rigs, and large-scale industrial simulators. High voltage introduces additional safety and compliance requirements, limiting widespread adoption. However, for applications requiring exceptional performance and durability, high-voltage servo solutions remain strategically important within the AC servo motors and drives industry.

By Phase Type Analysis

Increasing Acceptance of Three-Phase AC Servo Motor for Industrial Automation Application to Aid Growth

Based on phase type, the market is segmented into two-phase and three-phase AC servo motors.

The three-phase AC servo motor dominated the market in 2019. This segment is anticipated to grow with a high CAGR during the forecast period. This growth is mainly owing to technological developments for high-power applications. This phase type also provides high torque and high-speed response. Three-phase systems dominate the AC servo motors and drives market due to superior efficiency, smoother torque delivery, and higher power handling.

Three-phase servo motors support demanding industrial environments requiring continuous operation and precise motion. Their widespread adoption across automotive, semiconductor, and packaging industries reinforces their leadership position. Three-phase architectures also align well with industrial Ethernet networks and modern servo drives, supporting advanced automation strategies.

The two-phase AC servo motor is likely to witness moderate growth during the forecast period. This growth is due to the increased use of a two-phase AC servo motor for low-power machine tools. Two-phase AC servo motors and drives find limited but consistent use in compact systems and legacy automation architectures. Their simpler control schemes suit applications where moderate precision suffices. Educational equipment, small laboratory instruments, and select legacy machinery continue to utilize two-phase systems. While market share remains modest, replacement and retrofit demand sustains this segment.

By Communication Protocol Analysis

Fieldbus Communication Protocol Segment to Hold Major Share in the Market

Based on the communication protocol, the market is classified into fieldbus, industrial Ethernet, and wireless.

The fieldbus communication protocol segment held a major market share due to its flexibility to support several network topologies, including tree, ring, and star. This communication protocol requires a single cable to connect with AC servo drives, reduces system complexity, and improves communication speed. Fieldbus-based communication protocols maintain relevance in established industrial environments.

Protocols such as PROFIBUS and DeviceNet support reliable data exchange between servo drives, controllers, and sensors. Many legacy factories rely on fieldbus systems due to existing infrastructure investments. As a result, servo vendors continue to support fieldbus compatibility to serve installed bases and retrofit projects.

The industrial Ethernet segment is expected to grow with a substantial compound annual growth rate during the forecast period. The growth is attributed to the rising use of the industrial Ethernet protocol for servo drives as they offer high communication speed, real-time control, and large-capacity communication.

Industrial Ethernet represents the fastest-growing communication segment within the AC servo motors and drives market. Protocols such as EtherCAT, PROFINET, and Ethernet/IP enable high-speed, deterministic communication critical for multi-axis synchronization. These protocols support real-time diagnostics, remote configuration, and seamless integration with digital manufacturing platforms. As factories adopt smart manufacturing and digital twins, Industrial Ethernet-based servo systems become the preferred choice for new installations.

Additionally, it includes communication protocols such as CC-Link IE, EtherCAT, EtherNet/IP, and PROFINET. For example, Mitsubishi Electric Corporation offers servo amplifiers with industrial Ethernet communication protocols such as MR-J4-which provide support to PROFINET, EtherCAT, and EtherNet/IP.

The wireless Ethernet segment will experience ample growth opportunities in the forthcoming years, owing to the rising design and development of servo motors and drives with wireless technologies. Wireless communication remains an emerging segment, primarily used in mobile automation and flexible manufacturing environments.

Automated guided vehicles, mobile robots, and reconfigurable production cells benefit from reduced cabling and faster deployment. While concerns around latency and cybersecurity limit adoption in mission-critical motion control, ongoing improvements in industrial wireless standards support gradual growth. Wireless-enabled servo drives are expected to complement, rather than replace, wired communication in the near term.

By End-Use Industry Analysis

Automotive and Transportation Industry Segment to Dominate, Backed by Increasing Vehicle Demand

Based on the end-use industry, the market is bifurcated into aerospace & defense, automotive and transportation, semiconductor and electronics, printing & packaging, food & beverage, chemicals, and petrochemicals.

The aerospace and defense sector demands servo systems capable of extreme precision, reliability, and compliance with rigorous standards. Applications include flight simulators, actuator control, radar systems, and unmanned platforms. AC servo motors and drives in this sector emphasize redundancy, thermal stability, and long service life. Although volumes are relatively low, unit value remains high, contributing meaningfully to overall market revenue.

Automotive manufacturing represents a core demand driver for the AC servo motors and drives market. Servo systems power robotic welding, painting, assembly, and inspection lines. Electrification trends further expand demand as electric vehicle production introduces new automation requirements. Transportation applications, including rail systems and logistics hubs, rely on servo-driven automation to improve throughput and reliability.

The automotive industry segment is anticipated to dominate the market and grow faster during the forecast period. This growth can be attributed to the increasing adoption of robotics systems for high-volume production to meet the rising demand for ground vehicles.

Moreover, automated manufacturing can reduce the operation cost and issues related to non-automated production technology. It also helps to develop a high-quality product. As per Forbes data in 2019, the U.S. has 228 industrial robots per 10,000 of its workers. Besides, the rising adoption of smart robots for product supply is expected to drive the market growth during the forecast period

The semiconductor and electronics segment is anticipated to grow significantly due to the increasing adoption of smart home appliances, mobile phones, and other electronic devices worldwide. The rising manufacturing of these devices will create high demand for innovative, internet-of-things (IoT) - enabled advanced machinery, coupled with AC servo drives and servo motors for chip fabrication.

Semiconductor fabrication and electronics assembly rely heavily on ultra-precise motion control. AC servo motors and drives enable nanometer-level positioning, high-speed pick-and-place, and wafer handling. This segment demands advanced feedback systems, vibration suppression, and cleanroom-compatible designs. As global semiconductor capacity expands, demand from this segment strengthens steadily.

Printing and packaging operations require synchronized motion to maintain quality at high speeds. Servo systems support precise tension control, cutting accuracy, and rapid format changes. The shift toward shorter production runs and customized packaging increases reliance on flexible servo-driven machinery. This segment benefits from consistent demand across food, consumer goods, and pharmaceutical packaging.

Food and beverage manufacturers adopt AC servo motors and drives to improve hygiene, efficiency, and traceability. Washdown-rated servo motors support sanitary environments, while precise control minimizes product waste. Automation adoption grows as producers address labor shortages and stricter quality standards. This segment favors reliable, easy-to-maintain servo solutions with strong local service support.

In chemical processing, servo systems control valves, pumps, and mixers with high precision. Safety, durability, and resistance to harsh environments are critical requirements. Although adoption is selective, servo-driven automation improves process consistency and energy efficiency. As chemical producers modernize facilities, demand for robust AC servo motors and drives gradually increases.

The demand for modern automated and motion control solutions in the printing and packaging, aerospace and defense, food and beverage, chemicals, and petrochemicals industries is increasing due to reduced operating costs and time and enhanced efficiency and quality.

AC Servo Motors and Drives Market REGIONAL Analysis

Asia Pacific AC Servo Motors and Drives Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The global market is segmented into North America, Europe, Asia Pacific, and the Rest of the World.

Asia-Pacific AC Servo Motors and Drives Market Analysis:

Asia Pacific market stood at USD 2.35 billion in 2025 and is anticipated to dominate the global AC servo motors and drives market during the forecast period. This dominance is attributed to key market players in Japan, such as Yaskawa Electric Corporation, Mitsubishi Electric Corporation, and Fuji Electric Co., Ltd. The exponential growth in manufacturing industries in several countries such as China, South Korea, Japan, and India is expected to boost the AC servo motors and drives in the region. According to Forbes data, 73% of all new industrial robots were installed in just five countries, including Japan, China, South Korea, the United States, and Germany, in 2019.

Asia-Pacific represents the fastest-growing regional market, driven by large-scale manufacturing expansion and automation adoption. Electronics, automotive, and semiconductor industries fuel high-volume demand. Regional buyers favor cost-effective yet high-performance servo solutions. Government-led industrial modernization programs and rising labor costs accelerate automation investments, positioning Asia-Pacific as a critical growth engine for the AC servo motors and drives market.

Japan AC Servo Motors and Drives Market:

Japan’s market reflects deep expertise in precision motion control and robotics. AC servo motors and drives are integral to electronics assembly, robotics, and automotive manufacturing. Japanese buyers emphasize reliability, compact design, and long operational life. Continuous innovation in control algorithms and miniaturization supports replacement demand, maintaining Japan’s influence within the global servo technology landscape.

China AC Servo Motors and Drives Market:

China drives substantial volume growth as manufacturers automate production to improve quality and efficiency. AC servo motors and drives support electronics, automotive, and heavy machinery sectors. Domestic suppliers gain competitiveness through cost optimization, while international vendors serve high-precision applications. National initiatives promoting advanced manufacturing accelerate adoption, reinforcing China’s role as a major contributor to global market growth.

North America AC Servo Motors and Drives Market Analysis:

North America registered a significant share in the base year due to the increased implementation of robot arms in the manufacturing process to have flexible flow lines. Strong adoption across automotive, aerospace, semiconductor, and packaging industries supports stable demand. Manufacturers prioritize high-performance motion control, cybersecurity-ready communication, and integration with digital manufacturing platforms. Investment in smart factories and reshoring of industrial production sustain replacement and upgrade cycles, reinforcing long-term market stability across the United States and Canada.

United States AC Servo Motors and Drives Market:

The United States anchors regional demand due to advanced manufacturing intensity and early adoption of automation technologies. Automotive electrification, semiconductor fabrication expansion, and defense modernization programs drive servo system deployment. Buyers emphasize reliability, lifecycle support, and compatibility with Industrial Ethernet protocols. Domestic manufacturers increasingly favor energy-efficient servo solutions to meet sustainability targets, supporting consistent AC servo motors and drives market growth.

Europe AC Servo Motors and Drives Market Analysis:

The European market is anticipated to witness significant growth during the forecast period due to the strong presence of end-use industries. For instance, in December 2020, Yaskawa Electric Corporation, a Japanese company, invested USD 28.03 million to establish its new European headquarters in Hattersheim.

Europe’s AC servo motors and drives market reflects strong emphasis on precision engineering, energy efficiency, and regulatory compliance. Industrial automation investments span automotive, packaging, and advanced machinery sectors. European manufacturers value modular servo platforms that support flexible production and rapid reconfiguration. Sustainability mandates encourage adoption of efficient servo drives with regenerative capabilities, supporting steady regional market expansion.

Germany AC Servo Motors and Drives Market:

Germany remains a technology leader within the AC servo motors and drives industry, supported by its machine tool, automotive, and industrial automation sectors. German manufacturers prioritize precision, durability, and system interoperability. Industry 4.0 initiatives accelerate demand for servo systems integrated with real-time analytics and digital twins. Strong export-oriented machinery production sustains continuous innovation and high-value deployments.

United Kingdom AC Servo Motors and Drives Market:

The United Kingdom market emphasizes automation to improve productivity amid labor constraints. AC servo motors and drives support applications in packaging, food processing, and advanced manufacturing. Adoption focuses on compact, flexible systems suitable for mid-sized production facilities. Investments in smart manufacturing and logistics automation encourage modernization of existing equipment, sustaining gradual but consistent market growth.

Latin America AC Servo Motors and Drives Market Analysis:

Latin America shows emerging demand as industries modernize production facilities. Automotive assembly, food processing, and packaging drive servo system adoption. Budget sensitivity influences purchasing decisions, favoring reliable mid-range solutions. Gradual industrial digitization and foreign direct investment support long-term growth, although adoption remains uneven across countries.

Middle East & Africa AC Servo Motors and Drives Market Analysis

The Middle East & Africa market grows steadily through industrial diversification and infrastructure development. AC servo motors and drives support oil and gas processing, utilities, and emerging manufacturing hubs. Buyers prioritize durability and service availability. While market size remains smaller, modernization initiatives and industrial automation investments support gradual adoption.

Competitive Landscape

Yaskawa Electric Corporation to Set New Standard with Its Innovative Servo Motor and Drives Product Line

With its investments in the research & development of next-generation servo motors and drives, Yaskawa Electric Corporation is expected to sustain its position in the market. The company focuses on expanding the robotic systems and motion control product line with its collaborative partners. In April 2019, the company established its new robot production plant in Slovenia through a partnership with the European robotics development center. For this establishment, the company invested around USD 30.41 million. With strategic acquisitions and partnerships, the company is focused on growing its capabilities.

The AC servo motors and drives market features a competitive landscape shaped by global automation leaders, regional specialists, and niche technology providers. Large multinational vendors offer comprehensive portfolios combining servo motors, drives, controllers, and software. Their strengths include extensive R&D resources, global service networks, and deep integration with industrial automation ecosystems. These players typically serve high-volume manufacturing, advanced robotics, and mission-critical applications.

Regional and niche players focus on specific performance attributes, cost optimization, or localized support. Many specialize in compact servo systems, application-specific designs, or retrofitting solutions for legacy machinery. Their agility allows faster customization and competitive pricing, particularly for SMEs and regional manufacturers. Niche suppliers often gain traction in packaging, food processing, and light industrial automation.

Partnerships play a central role in competitive positioning. Servo manufacturers collaborate with controller vendors, robot OEMs, and system integrators to deliver turnkey automation solutions. Alliances with Industrial Ethernet providers ensure compatibility with evolving communication standards. Semiconductor and electronics manufacturers increasingly engage in co-development initiatives to meet ultra-precision requirements.

Key competitive differentiation factors include:

- Motion accuracy and dynamic response

- Energy efficiency and regenerative capabilities

- Communication protocol flexibility

- Ease of integration and commissioning

- Lifecycle support and global service reach

List of Top AC Servo Motors and Drives Companies:

- ABB Group (Switzerland)

- Delta Electronics, Inc. (Taiwan)

- FANUC Corporation (Japan)

- Fuji Electric Co., Ltd. (Japan)

- Kollmorgen Corporation (The U.S.)

- Mitsubishi Electric Corporation (Japan)

- Nidec Corporation (Japan)

- Rockwell Automation, Inc. (The U.S.)

- Schneider Electric SE (France)

- Siemens AG (Germany)

- Yaskawa Electric Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS:

- March 2025: Siemens AG introduced an advanced servo drive platform designed to enhance multi-axis synchronization, integrating real-time Industrial Ethernet communication and embedded energy-optimization algorithms for high-speed manufacturing environments.

- January 2025: Yaskawa Electric Corporation expanded its servo motor portfolio with compact high-torque models aimed at robotics and electronics assembly, leveraging improved encoder resolution and adaptive control firmware.

- September 2024: Mitsubishi Electric launched a next-generation AC servo system optimized for predictive maintenance, incorporating condition-monitoring sensors and analytics-ready drive architecture to reduce unplanned downtime.

- June 2024: Rockwell Automation enhanced its servo drive lineup with cybersecurity-hardened communication modules, supporting secure Industrial Ethernet connectivity for digitally integrated production lines.

- February 2024: Schneider Electric partnered with a leading machine tool manufacturer to co-develop energy-efficient servo solutions, focusing on regenerative braking and reduced power consumption for sustainable industrial automation.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The AC servo motors and drives market report provides a detailed analysis of the market. It focuses on key aspects such as leading companies, types of servo motors, and leading applications. Moreover, the report offers insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the market report encompasses several direct and indirect factors that have contributed to the market's growth over recent years.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

By Segmentation |

By Product Type

|

|

By Voltage Range

|

|

|

By Phase Type

|

|

|

By Communication Protocol

|

|

|

By End-Use Industry

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global AC servo motors and drives market was valued at USD 16.37 billion in 2025 and is projected to reach USD 31.92 billion by 2034, growing at a CAGR of 7.7% during the 2026–2034 forecast period.

The market is projected to grow at a CAGR of 7.7% during the forecast period (2026-2034).

The primary growth drivers include increased automation in industrial manufacturing, adoption of Industry 4.0 technologies, and rising demand for high-performance, closed-loop control systems in automotive, electronics, and packaging sectors.

Asia Pacific held the largest market share in 2019, accounting for USD 2.35 billion. Countries like China, Japan, and South Korea lead the region due to strong manufacturing infrastructure and key players like Yaskawa Electric and Mitsubishi Electric.

Key end-use industries include automotive and transportation, semiconductor and electronics, printing and packaging, aerospace & defense, food & beverage, and chemicals & petrochemicals, all driven by automation and robotics adoption.

The industry uses two primary motor types: synchronous and induction AC servo motors. Synchronous motors with permanent magnets are preferred for high-precision applications like CNC machines, aircraft parts, and robotics.

Communication protocols like Fieldbus, Industrial Ethernet, and Wireless Ethernet enable fast and accurate control. Fieldbus remains dominant due to its simplicity, while Industrial Ethernet is growing due to real-time control and high-speed communication.

Low-voltage AC servo motors (below 230V) are increasingly used in mobile robotics and compact manufacturing equipment, offering low maintenance, cost-efficiency, and energy-saving benefits, especially for SMEs and emerging markets.

Top players include Yaskawa Electric Corporation, Mitsubishi Electric, ABB Group, FANUC, Siemens, Schneider Electric, Delta Electronics, and Rockwell Automation. These companies invest heavily in R&D and global expansion.

Trends include the development of micro-sized high-power drives, integration of AI and IoT, and a surge in demand for automated guided vehicles (AGVs) and CNC machinery across smart factories and Industry 4.0 setups.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us