Acoustical Ceiling Market Size, Share & Industry Analysis, By Product Type (Mineral Fibre, Gypsum, and Others), By Application (Non-Residential, Residential, and Industrial), and Regional Forecast, 2026-2034

Acoustical Ceiling Market Size and Future Outlook

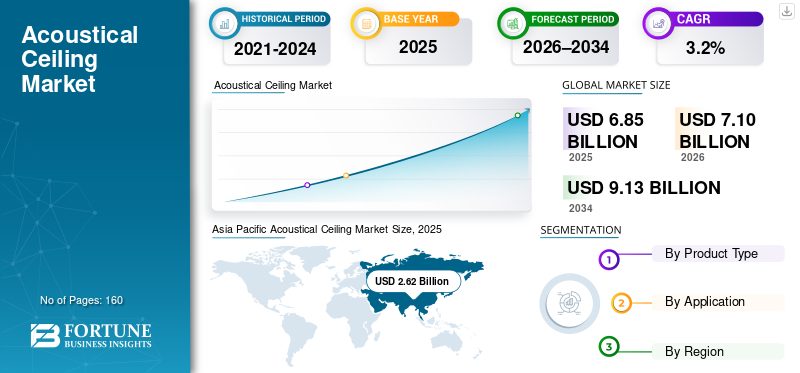

The global acoustical ceiling market size was valued at USD 6.85 billion in 2025. The market is projected to grow from USD 7.10 billion in 2026 to USD 9.13 billion by 2034, exhibiting a CAGR of 3.2% during the forecast period. Asia Pacific dominated the acoustical ceiling market with a market share of 38.25% in 2025.

Acoustical ceilings are ceiling systems engineered to manage reverberation, improve speech intelligibility, and enhance occupant comfort through sound absorption and related acoustic performance. They are deployed across suspended grid ceilings, monolithic and perforated gypsum solutions, and specialty ceiling formats, such as baffles and islands, to meet acoustic, fire, cleanability, and aesthetic requirements in interior spaces.

The market growth is driven by renovation-led upgrades in commercial and institutional buildings, tighter indoor environmental quality expectations, and the continued need to integrate acoustics with lighting and mechanical systems. Growth is also supported by sustainability-led specification changes, including the use of lower-carbon materials and circular take-back models for ceiling tiles and grids.

Furthermore, the market comprises several major players, including Armstrong World Industries, G&S Acoustics, ROCKWOOL, Knauf, and OWA. A broad portfolio, innovative product launches, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

ACOUSTICAL CEILING MARKET TRENDS

Low-Embodied-Carbon Ceilings, Design-Led Acoustic Islands, and Healthy-Building Fit-Outs Are the Significant Market Trends

Demand for acoustical ceilings is increasingly shaped by sustainability and design requirements that go beyond baseline sound absorption. In the mineral fiber industry, manufacturers are introducing lower-carbon panels to support decarbonization goals in commercial buildings. In parallel, architects are adopting ceiling islands, baffles, and monolithic acoustic systems to achieve open-ceiling aesthetics while maintaining acoustic performance in hybrid work and hospitality spaces. Healthcare and education continue to be stable demand anchors, where cleanability, durability, and controlled acoustics are tightly specified.

- For instance, Armstrong World Industries introduced Ultima Low Embodied Carbon (LEC) ceiling panels to help reduce embodied carbon in commercial projects, reflecting a rising preference for sustainability-linked ceiling specifications.

MARKET DYNAMICS

MARKET DRIVERS

Commercial Renovation Cycles, Indoor Acoustic Comfort, and Integrated Ceiling Systems to Drive the Market Growth

Acoustical ceilings are a core component of interior fit-outs as they enable consistent acoustic performance, conceal building services, and support fast installation for renovation and tenant improvement projects. Open-plan offices, collaborative learning environments, and patient-centered healthcare designs are increasing the importance of controlled reverberation and speech privacy, sustaining demand for high-NRC ceiling solutions. At the same time, integrated ceiling systems that coordinate acoustics with lighting, air distribution, and fire protection simplify design and installation, supporting adoption in non-residential buildings.

- For instance, manufacturer portfolios increasingly position ceiling panels and grid systems as part of integrated interior solutions, supporting coordinated design across acoustics and building services in renovation-heavy commercial markets.

MARKET RESTRAINTS

Material Cost Volatility, Design Shifts Toward Exposed Ceilings, and Skilled Labor Constraints Limit Market Expansion

Raw material and energy cost volatility can pressure margins and pricing, particularly for mineral-fiber and gypsum-based ceiling products, which are energy-intensive to manufacture. In some office and retail designs, exposed ceilings are favored for an industrial aesthetic, which can reduce the ceiling area specified unless compensated for by acoustic baffles or islands. Installation timelines may also be constrained by the availability of skilled labor, especially in markets with high renovation activity and competing interior trades.

MARKET CHALLENGES

Fragmented Specifications, Substitution by Alternative Acoustic Treatments, and Non-Residential Construction Cyclicality Can Hamper Growth

Acoustical ceiling demand is sensitive to non-residential construction and renovation cycles, which can be disrupted by interest-rate changes and delayed capital spending. In addition, some applications substitute toward wall panels, acoustic sprays/plasters, or modular baffles, depending on design intent and installed cost. Moreover, project specifications vary widely by region and end use, requiring manufacturers to maintain broad test data, code-compliance documentation, and distributor support to avoid losing share in bid-driven channels.

MARKET OPPORTUNITIES

Low-Carbon Specifications, Circular Take-Back Programs, and Growth in Acoustic Islands Create Lucrative Growth Opportunities

As embodied carbon reporting and green building programs become more common in project specifications, demand is rising for acoustical ceilings with verified environmental product declarations, higher recycled content, and improved life-cycle profiles. Circularity initiatives, such as take-back and recycling programs, can strengthen customer retention and reduce the total cost of ownership for large building portfolios. Design-led acoustic islands and baffles also create higher-value opportunities in spaces where full-suspended ceilings are not desired.

- For example, ROCKWOOL’s Rockfon business continues to expand design-oriented baffle and island offerings, supporting projects that require acoustic control without a full ceiling plane.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Cost-Effective Versatility Across Commercial Spaces Drives Mineral Fibre Segment Growth

Based on product type, the market is segmented into mineral fibre, gypsum, and others.

The mineral fibre segment accounted for the largest acoustical ceiling market share in 2025. The segment is supported by its cost-effective performance, wide specification acceptance, and suitability for fast-install grid systems in offices, education, and healthcare. Furthermore, the segment held a 71.1% share in 2025.

The gypsum segment is expected to grow favorably throughout the forecast period, supported by demand for monolithic aesthetics and perforated gypsum ceilings used in corridors, auditoriums, and high-design commercial interiors, where acoustic backing and perforation patterns balance absorption and appearance. The gypsum segment is projected to grow at a 3.5% CAGR during the forecast period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Non-Residential Segment Dominates the Market Due to the Extensive Use of the Product

By application, the market is categorized into non-residential, residential, and industrial.

The non-residential segment accounted for the largest share in 2025, driven by suspended ceilings and acoustic systems used in offices, education, healthcare, retail, hospitality, and public buildings, where acoustic performance, fire ratings, and integration with building services are important. Furthermore, the segment held a 79.5% share in 2025.

The residential segment is also expected to grow favorably over the projected period. The segment's growth is driven by basements, multi-family common areas, and premium acoustic upgrades, where cost sensitivity and alternative finishes limit widespread adoption. Industrial demand is supported by reverberation control in production areas, labs, and warehouses, as well as hygiene and durability requirements in select facilities. The segment is expected to grow at a CAGR of 2.9% over the forecast period.

Acoustical Ceiling Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Acoustical Ceiling Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 2.62 billion, and is expected to maintain the leading share in 2026, with USD 2.73 billion. The region's growth is driven by expanding commercial floor space, rising investment in healthcare and education infrastructure, and greater adoption of acoustics in modern office and hospitality projects.

China Acoustical Ceiling Market

In 2025, the China market reached a valuation of USD 1.03 billion. The market is driven by large-scale commercial construction and an increasing focus on acoustic comfort in offices, transport hubs, and public buildings, which support demand for both mineral fibre ceilings and design-led specialty systems.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is expected to experience significant acoustical ceiling market growth in the coming years. During the forecast period, the region is projected to grow at 3.5% and reach a valuation of USD 1.85 billion in 2026. The region benefits from high renovation activity across commercial interiors and strong adoption of suspended ceiling systems in offices, education, and healthcare, supported by mature contractor and distribution networks.

U.S. Acoustical Ceiling Market

In 2025, the U.S. market was valued at USD 1.58 billion. The demand is supported by commercial renovation cycles, healthcare and education fit-outs, and sustainability-led product upgrades in ceiling specifications.

Europe

Europe is also a significant contributor to the market, with the market estimated to reach USD 1.73 billion by 2026. The market’s growth is supported by renovation-focused building programs, stringent indoor environmental performance expectations, and strong specification pull for sustainable acoustic solutions in commercial and institutional buildings.

Germany Acoustical Ceiling Market

Germany’s market recorded a valuation of USD 0.44 billion in 2025, equivalent to around 3.0% of global sales, supported by renovation activity and strong demand in education, healthcare, and office interiors.

U.K. Acoustical Ceiling Market

The U.K. market in 2025 was estimated at around USD 0.22 billion, representing approximately 1.9% of global market revenue.

Latin America

Latin America is experiencing steady growth. This region is expected to reach a valuation of USD 0.42 billion in 2026. The demand in the region is linked to selective commercial construction, retail, and hospitality projects, as well as the modernization of education and healthcare buildings in major urban centers.

Middle East & Africa

The Middle East & Africa region is gradually expanding, with estimated sales of around USD 0.35 billion in 2026. GCC countries account for a meaningful share of regional demand due to high-value commercial and hospitality projects, while other markets remain smaller and more project-driven.

GCC Acoustical Ceiling Market

GCC market reached a valuation of USD 0.22 billion by 2025, accounting for approximately 4.3% of global revenues. The growth is supported by hospitality, retail, and public infrastructure developments that require acoustics and aesthetic differentiation.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Adopt Specification-Led Selling, Circularity Positioning, and Fabrication Capability to Maintain Market Positions

Competition is shaped by specification breadth (acoustic, fire, humidity, and cleanability), access to established contractor channels, and the ability to provide complete ceiling systems, including grids, trims, and specialty formats. Some of the key market players include Armstrong World Industries, G&S Acoustics, ROCKWOOL, Knauf, and OWA. Major players differentiate through product innovation (including low embodied carbon panels and design-led acoustic islands), certified environmental documentation, and strong service support for architects, designers, and installers.

LIST OF KEY ACOUSTICAL CEILING COMPANIES PROFILED

- Armstrong World Industries (U.S.)

- Saint-Gobain (France)

- ROCKWOOL (Denmark)

- Knauf (Germany)

- OWA (Germany)

- Hunter Douglas Architectural (Netherlands)

- CertainTeed (U.S.)

- SAS International (U.K.)

- Rockfon (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Saint-Gobain Ecophon highlighted Ecophon Fade (spray-applied acoustic plaster system) as a seamless alternative to modular solutions, signaling growth in monolithic/ invisible acoustics for premium interiors.

- May 2025: Saint-Gobain Ecophon expanded into wood wool acoustic ceilings with Ecophon Saga, signaling broader material choices (warm aesthetics) while keeping modular acoustic performance in focus.

- June 2024: Armstrong World Industries acquired 3form, LLC (architectural resins and glass used in ceilings/walls), signaling continued portfolio expansion into higher-design, specifiable architectural ceiling solutions.

- April 2024: Armstrong World Industries introduced Ultima Low Embodied Carbon (LEC) ceiling panels, signaling faster adoption of low-carbon interior materials aligned with EPD/embodied-carbon targets.

- March 2023: Armstrong World Industries launched Ultima Templok mineral fiber ceiling panels with integrated phase-change material, signaling product differentiation around energy efficiency and carbon reduction in commercial buildings.

- October 2020: Armstrong World Industries launched the 24/7 Defend portfolio (including AirAssure self-sealing ceiling systems and an in-ceiling UV-C air purification solution), signaling acceleration of health/IAQ-driven acoustical ceiling innovation.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.2% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Application, and Region |

|

By Product Type |

· Mineral Fibre · Gypsum · Others |

|

By Application |

· Non-Residential · Residential · Industrial |

|

By Geography |

· North America (By Product Type, Application, and Country) o U.S. (By Application) o Canada (By Application) · Europe (By Product Type, Application, and Country) o Germany (By Application) o France (By Application) o Italy (By Application) o U.K. (By Application) o Rest of Europe (By Application) · Asia Pacific (By Product Type, Application, and Country) o China (By Application) o Japan (By Application) o India (By Application) o South Korea (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Product Type, Application, and Country) o Brazil (By Application) o Mexico (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Product Type, Application, and Country) o GCC (By Application) o South Africa (By Application) o Rest of the Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights estimates that the global market size was USD 6.85 billion in 2025 and is projected to reach USD 9.13 billion by 2034.

Recording a CAGR of 3.2%, the market is slated to exhibit steady growth during the forecast period.

The non-residential application segment led the market in 2025.

Asia Pacific held the highest market share in 2025.

Armstrong World Industries, G&S Acoustics, ROCKWOOL, Knauf, and OWA are some of the prominent players in the market.

Commercial renovation cycles, indoor acoustic comfort, and integrated ceiling systems are the key factors driving the market.

The major factors expected to favor product adoption in the market are stricter indoor acoustic expectations, faster/modular installation benefits, and growing preference for aesthetic and functional ceilings.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us