Acute Coronary Syndrome Therapeutics Market Size, Share & Industry Analysis, By Drug Class (Antiplatelet agents, Anticoagulant agents, Fibrinolytics, Anti-ischemic agents, Beta-blockers, Lipid-lowering agents, Renin–angiotensin system inhibitors, Mineralocorticoid receptor antagonists, and Others), By Disease Type (ST-elevation myocardial infarction, Non–ST-elevation myocardial infarction, and Unstable Angina), By Route of Administration (Oral and Parenteral), By Distribution Channel (Hospital Pharmacies, Drug Stores & Retail Pharmacies, & Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

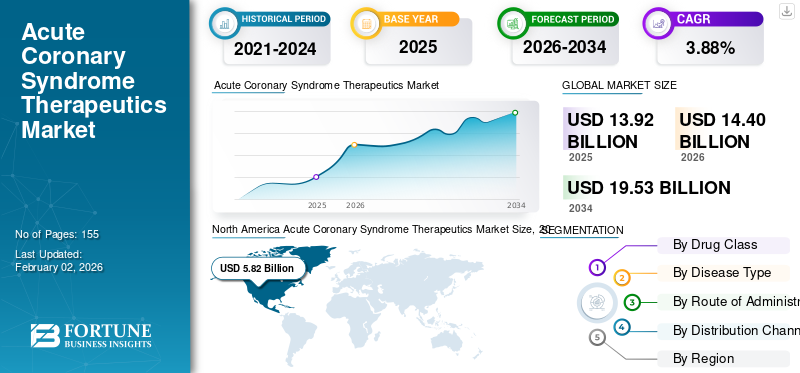

The global acute coronary syndrome therapeutics market size was valued at USD 13.92 billion in 2025. The market is projected to grow from USD 14.40 billion in 2026 to USD 19.53 billion by 2034, exhibiting a CAGR of 3.88% during the forecast period. North America dominated the global market with a share of 41.81% in 2025.

The global market is projected to grow at a steady rate, particularly driven by a global population that suffers from several comorbidities, such as aging, diabetes, and obesity that further contribute to the strong patient caseload of acute coronary syndrome. Furthermore, the treatment of acute coronary treatment involves the administration of a multi-drug regimen that often results in a higher therapy intensity per event. Despite pressures from generic competition, some of the parameters that will contribute to the market growth include a greater adoption of premium lipid-lowering therapies coupled with protocolization of therapeutic measures and improved systems of care. This has led to an increased emphasis on R&D initiatives with innovative pipeline candidates by key market players, which also augments market growth during the forecast period.

- For instance, in July 2025, Novartis AG announced that the U.S. FDA approved a regulatory label update for Leqvio (inclisiran), which is administered twice a year. The U.S. FDA allowed the utilization of this drug as a monotherapy coupled with diet and exercise for the reduction of low-density lipoprotein cholesterol (LDL-C) in adults with hypercholesterolemia. This label update is particularly helpful as it coincides with the latest 2025 ACC/AHA Joint Committee Clinical Practice Guideline for the Management of Patients with Acute Coronary Syndromes, which recommends aggressive administration of lipid-lowering therapies to achieve a patient’s LDL-C targets.

Furthermore, numerous pharmaceutical companies such as AstraZeneca, Sanofi, and DAIICHI SANKYO COMPANY LIMITED are amongst the major players in the market. These players are focused on the expansion of the clinical indication labels of their existing product portfolio in conjunction with an emphasis on switching patients to more premium therapies and also improving the access mechanics to their drugs.

Download Free sample to learn more about this report.

ACUTE CORONARY SYNDROME THERAPEUTICS MARKET TRENDS

Emphasis on the Development of Precise Treatment Protocols Boosts Market Development

Some of the most notable trends witnessed in the global market are the creation of treatment guidelines that consider critical factors such as the heterogeneity of ischemic and bleeding risks across patients. The creation of advanced treatment protocols allows for the therapy choice/duration to become more individualized, leading to better treatment outcomes. Additionally, the intensification of lipid-lowering therapeutics also allows for improved clinical outcomes and leads to the earlier adoption of these premium, high-cost drugs. In recent times, the strengthening of treatment guidelines for acute coronary syndrome in emerging countries such as India is also a key trend in the acute coronary syndrome therapeutics market.

- For instance, as per data published in November 2025, in the Indian state of Andhra Pradesh, the government’s STEMI (ST-segment elevation myocardial infarction) protocol has saved an estimated 3,027 patients in the time period of June 1st, 2024, to November 15th, 2025. The government treatment protocol allows for the free administration of the drug Tenecteplase during the golden hour or the first hour of the patient experiencing sudden chest pain.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Adoption of Premium Therapies to Drive Market Growth

The most important driver for the growth of the global market is the increasing adoption of premium therapies such as nonstatin lipid-lowering agents, which have increasingly recommended by several regulatory agencies. Following an acute coronary syndrome event, patients are automatically classified as very high cardiovascular risk under most clinical pathways. This classification triggers the initiation of aggressive LDL-C (Low-Density Lipoprotein Cholesterol) lowering protocol, which is often not managed with statins alone. As a result, there is growing reliance on nonstatin lipid therapies such as PCSK9 inhibitors to achieve LDL-C levels. This shift has significantly broadened the patient population for advanced lipid-lowering treatments, thereby driving growth in the global acute coronary syndrome market.

- For instance, in August 2025, Amgen, Inc. announced that its drug Repatha (evolocumab) gained broadened approval for use in adults at increased risk of major adverse cardiovascular events (MACE) due to uncontrolled low-density lipoprotein cholesterol (LDL-C).

MARKET RESTRAINTS

Competition from Generic Equivalents and Reimbursement Barriers for Premium Therapies to Impede Growth Prospects

The most critical restraining factor that limits the overall growth rate of this market is the dominance of generic drugs, which compresses value across core therapeutic segments. Most staple drugs prescribed for the treatment of acute coronary syndrome have widely available generic equivalents, and the resulting pricing pressures significantly limit market growth. Another notable restraint is the presence of insurance coverage and reimbursement barriers, limits the widespread uptake of higher-priced drugs. For instance, the National Health Service (NHS) in November 2025, negotiated the continued access to Novartis' inclisiran, despite a slower uptake. Such concerns regarding coverage and cost-effectiveness continue to hinder the acute coronary syndrome therapeutics market growth.

- For example, in May 2025, Alembic Pharmaceuticals Limited received the U.S. FDA approval for ticagrelor, the generic equivalent of AstraZeneca’s Brilinta.

MARKET OPPORTUNITIES

Development of Safer and Long-Acting Therapies for Patients to Provide Opportunities for Market Growth

In recent times, market players developing innovative therapies in this space have increasingly focused on therapies that offer longer adherence times in patients. This shift is driven by the fact that several patients with acute coronary syndrome suffer from recurrent episodes of the disease as they do not adhere to the treatment guidelines. Hence, major companies such as Novartis AG have focused on developing medications with a limited dosing burden, such as Leqvio (inclisiran), which can be used as monotherapy and requires only twice-yearly administration. Furthermore, other players are focused on the development of safer antithrombotic ecosystems, allowing medical practitioners to prescribe drugs such as antiplatelet agents more widely.

- For instance, in March 2025, SFJ Pharmaceuticals & SERB Pharmaceuticals announced positive final results from their important Phase 3 REVERSE-IT trial that was developed to investigate their pipeline candidate of Bentracimab (PB2452), a monoclonal antibody. Bentracimab (PB2452) was designed to reverse the antiplatelet effects of ticagrelor (Brilinta) in patients needing urgent surgery or experiencing life-threatening bleeding.

MARKET CHALLENGES

Issues with Treatment Adherence and Complexities Pose Challenges to Continued Market Growth

One of the most important challenges associated with the acute coronary syndrome therapeutics market is inconsistent treatment adherence across patient populations. In many cases, the patients do not adhere to prescribed treatment for the recommended duration and often stop the intake of key drugs such as statins. This creates a situation in which clinical trials reflect higher treatment efficacy, while real-world effectiveness remains lower due to poor adherence. This gap further leads to the discrepancies in the priorities of the key stakeholders present in the market. The payers and healthcare providers push for improving adherence rates, whereas innovators prioritize broader market access and uptake. Such challenges restrict the possibility of a greater market growth rate.

- For instance, in February 2025, according to a study published in the Indian Heart Journal, which evaluated a 2025 registry-based prospective study in the post-acute coronary syndrome patients who underwent percutaneous coronary intervention (PCI), it was noted that the medication adherence rates had fallen sharply by 6 months.

Segmentation Analysis

By Drug Class

Antiplatelet Agents Segment due to its Growing Utilization

In terms of drug class segment, the market is segmented into antiplatelet agents, anticoagulant agents, fibrinolytics, anti-ischemic agents, beta blockers, lipid-lowering agents, renin–angiotensin system inhibitors, mineralocorticoid receptor antagonists, and others.

The antiplatelet agents segment is projected to account for the largest acute coronary syndrome therapeutics market share. The segment’s dominating market share is owing to its status as a non-optional backbone of acute coronary syndrome pharmacotherapy and its utilization beyond the acute hospitalization. In addition, these drug classes are considered universal, as every acute coronary syndrome patient receives aspirin and, in many cases, a P2Y12 inhibitor; therefore, the addressable treated population is close to the entire patient population.

- For instance, according to the clinical guidelines released by the ACC and the American Heart Association in February 2025, which comprise recommendations for managing patients with acute coronary syndromes, dual antiplatelet therapy (DAPT) with aspirin and an oral P2Y12 inhibitor is recommended for a minimum duration of 12 months as the default strategy in patients who do not have a high risk of bleeding.

The lipid-lowering agents segment is anticipated to rise with a CAGR of 5.03% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Type

Non–ST-elevation myocardial infarction (NSTEMI) Segment Dominated due to Growing Geriatric Population

Based on disease type, the market is segmented into ST-elevation myocardial infarction (STEMI), Non–ST-elevation myocardial infarction (NSTEMI), and unstable angina (UA).

In 2025, the Non–ST-elevation myocardial infarction (NSTEMI) segment accounted for the largest share of the global market. This dominance of the segment is primarily due to the fact that this disease type accounts for the largest share of myocardial infarction hospitalizations, which are increasingly being identified through modern diagnostic techniques. Additionally, the older population is more susceptible to this form of the disease, which further increases case volume and drives segmental growth.

- For instance, according to the data published by the National Center for Biotechnology Information (NCBI) in January 2020, NSTEMI accounted for 60%-70% of myocardial infarction hospitalizations.

The ST-elevation myocardial infarction (STEMI) segment is projected to grow at a CAGR of 2.82% over the forecast period.

By Route of Administration

Oral Segment Led the Market Due to Strong Adoption Rates

On the basis of the route of administration, the market is segmented into oral and parenteral.

The oral segment accounted for the largest market share over the forecast period. This is because most medications administered over a longer duration for acute coronary syndrome are given orally. Additionally, in the current scenario, oral drugs are administered to patients for several months, as opposed to parenteral drugs, which are given for hours; this further boosts the segment’s growth.

- For instance, according to the data published by the National Center for Biotechnology Information (NCBI) in February 2025, oral statins were still used substantially at the stage of six months, with usage at around 70%.

The parenteral segment is projected to grow at a CAGR of 4.25% over the forecast period.

By Distribution Channel

High Outpatient Consumption of Drugs for Acute Coronary Syndrome Enabled Drug Stores & Retail Pharmacies’ Leading Position

In terms of distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, and online pharmacies.

The drug stores & retail pharmacies dominated the global acute coronary syndrome therapeutics market share. This high market share is owing to the fact that while hospitals initiate treatment, patients often visit a retail pharmacy or drug store over a longer duration to continue their treatment. Furthermore, the segment is set to hold a 54.16% share in 2026.

- For instance, in February 2025, CVS opened a new store that included a pharmacy in Bridgeport, Connecticut, in the U.S.

The online pharmacies segment is projected to grow at a CAGR of 8.77% during the forecast period.

Acute Coronary Syndrome Therapeutics Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Acute Coronary Syndrome Therapeutics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 5.63 billion, and also maintained its leading share in 2025, with USD 5.82 billion. The market in the region is estimated to grow significantly during the forecast period, owing to a considerable case load of acute coronary syndrome patients and an intense R&D environment. These factors, coupled with developed systems of healthcare and strong expenditure on hospital inpatient care, are set to drive market growth in the region.

U.S Acute Coronary Syndrome Therapeutics Market

Based on North America’s regional dominance and the U.S.’s largest share within the region, the U.S. market can be analytically approximated at around USD 5.59 billion in 2026, accounting for roughly 38.8% of global sales.

Europe

Europe is expected to record a growth rate of 2.85% in the coming years, ranking as the fourth-highest-growing region globally, and is projected to reach a market size of USD 3.77 billion by 2026. Some of the contributive factors to the region’s strong market share includes presence of clear treatment pathways/guidelines, strong drug prices despite payer controls, and faster uptake of advanced therapeutics.

U.K Acute Coronary Syndrome Therapeutics Market

The U.K.’s market in 2025 is estimated at around USD 0.64 billion, representing roughly 4.6% of global acute coronary syndrome therapeutics revenues.

Germany Acute Coronary Syndrome Therapeutics Market

Germany’s market is projected to reach approximately USD 0.80 billion in 2025, equivalent to around 5.8% of global sales.

Asia Pacific

In the Asia Pacific, the acute coronary syndrome therapeutics market is estimated to reach USD 3.28 billion in 2025 and secure the position of the third-largest region in the market. In the region, India and China are both estimated to reach USD 0.49 billion and USD 1.11 billion, respectively, in 2025.

Japan Acute Coronary Syndrome Therapeutics Market

Japan’s acute coronary syndrome therapeutics market in 2025 is estimated at around USD 0.78 billion, accounting for roughly 5.6% of global acute coronary syndrome therapeutics revenues. Japan has a large share in the global market owing to the country’s large number of patients and strong, sustained outpatient care for this disease.

China Acute Coronary Syndrome Therapeutics Market

China’s acute coronary syndrome therapeutics market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 1.11 billion, representing roughly 7.9% of global sales.

India Acute Coronary Syndrome Therapeutics Market

In India, the acute coronary syndrome therapeutics market in 2025 is estimated at around USD 0.49 billion, accounting for roughly 3.5% of global revenues.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness lower but steady growth in this market during the forecast period. The Latin America market is set to reach a valuation of USD 0.67 billion in 2025. Substantial patient population, coupled with emphasis on primary care and strong emphasis on health initiatives, is set to drive market growth in these regions. In the Middle East & Africa, the GCC is set to reach a value of USD 0.17 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Critical Clinical Trials to Approve Major Innovative Drugs

The global acute coronary syndrome therapeutics market comprises a semi-fragmented competitive landscape, comprising major players such as AstraZeneca, Sanofi, DAIICHI SANKYO COMPANY, LIMITED. The significant company revenue share accounted for by these companies is due to the presence of strong branded products, diverse geographical presence, and presence in key end-user settings such as hospitals.

- For instance, in April 2024, results from the EMPACT-MI phase III clinical trial conducted by Eli Lilly and Company demonstrated a 10% relative risk reduction for patients who were initiated on Jardiance (empagliflozin) versus placebo, within 14 days of an acute myocardial infarction.

Other notable players in the global market include Eli Lilly and Company, Novartis AG, and Hoffmann-La Roche Ltd. These companies are engaged in critical clinical trials for the approval of major innovative drugs.

LIST OF KEY ACUTE CORONARY SYNDROME THERAPEUTICS MARKET COMPANIES PROFILED

- AstraZeneca (U.K.)

- Sanofi (France)

- Eli Lilly and Company (U.S.)

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- Novartis AG (Switzerland)

- Amgen Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- DAIICHI SANKYO COMPANY, LIMITED. (Japan)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Gland Pharma announced that it had received the U.S. FDA approval for cangrelor for injection, which is a P2Y12 inhibitor, administered for percutaneous coronary intervention (PCI)

- December 2024: Health Sciences Authority (HSA), which is the health regulatory agency of Singapore, announced the approval of Plavix tablet (75 mg), which is also indicated for acute coronary syndrome.

- February 2024: Viatris Inc. and Idorsia Ltd announced a research and development collaboration for selatogrel, a self-administered P2Y12 inhibitor being developed for very-early suspected acute myocardial infarction.

- January 2024: Avenacy, an U.S. based specialty pharmaceutical company, announced the launch of bivalirudin for injection, which is the generic equivalent of Angiomax for Injection, in the U.S.

- December 2023: Jiangsu Vcare PharmaTech Co., Ltd. (Jiangsu Vcare), announced the successful submission of a New Drug Application (NDA) to the U.S. FDA for their product of Vicagrel capsule, which is indicated for acute coronary syndrome.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2019-2024 |

|

Growth Rate |

CAGR of 3.88% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Drug Class, Disease Type, Route of Administration, Distribution Channel, and Region |

|

By Drug Class |

· Antiplatelet agents · Anticoagulant agents · Fibrinolytics · Anti-ischemic agents · Beta-blockers · Lipid-lowering agents · Renin–angiotensin system inhibitors · Mineralocorticoid receptor antagonists · Others |

|

By Disease Type |

· ST-elevation myocardial infarction (STEMI) · Non–ST-elevation myocardial infarction (NSTEMI) · Unstable Angina (UA) |

|

By Route of Administration |

· Oral · Parenteral |

|

By Distribution Channel |

· Hospital Pharmacies · Drug Stores & Retail Pharmacies · Online Pharmacies |

|

By Region |

· North America (By Drug Class, Disease Type, Route of Administration, Distribution Channel, and Country) o U.S. o Canada · Europe (By Drug Class, Disease Type, Route of Administration, Distribution Channel, and Country/Sub-Region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Drug Class, Disease Type, Route of Administration, Distribution Channel, and Country/Sub-Region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Drug Class, Disease Type, Route of Administration, Distribution Channel, and Country/Sub-Region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Drug Class, Disease Type, Route of Administration, Distribution Channel, and Country/Sub-Region) o GCC o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 13.92 billion in 2025 and is projected to reach USD 19.53 billion by 2034.

In 2025, the market value stood at USD 5.82 billion.

The market is expected to exhibit a CAGR of 3.88% during the forecast period (2026-2034).

By drug class, the antiplatelet agents segment is expected to lead the market.

The surging adoption of premium therapies is the key factor driving market expansion.

AstraZeneca, Sanofi, and DAIICHI SANKYO COMPANY Limited are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 155

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us