Aerial Survey Services Market Size, Share & Industry Analysis, By Service Type (Photogrammetry, LiDAR, Thermal imaging, Multispectral imaging and Others), By Platform (Fixed-Wing Aircraft, Rotary-Wing Aircraft (Helicopters) and Unmanned Aerial Vehicles (UAVs/Drones)), By Application (Aerial Photography and Remote Sensing, Data Acquisition and Analytics, Mapping & Surveying, 3D Modelling, Disaster Risk Management and Mitigation and Others), By End User (Government and Defense, Oil and Gas, Mining and Minerals, Agriculture, Forestry and Others) and Regional Forecast, 2026-2034

AERIAL SURVEY SERVICES MARKET SIZE AND FUTURE OUTLOOK

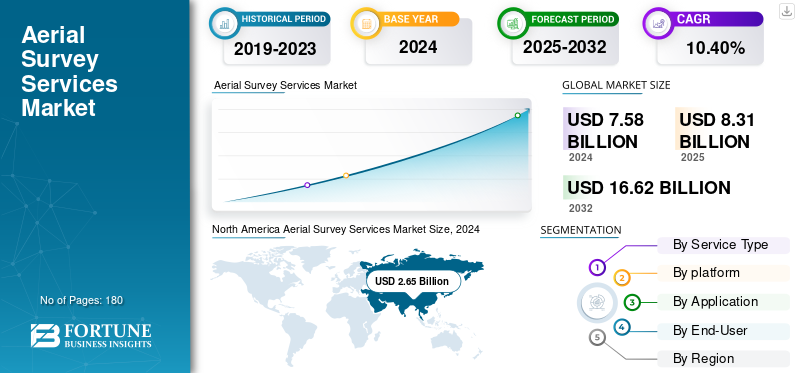

The global aerial survey services market size was valued at USD 8.31 billion in 2025. The market is projected to grow from USD 9.17 billion in 2026 to USD 20.13 billion by 2034, exhibiting a CAGR of 10.3% during the forecast period. North America dominated the global aerial survey services market with a market share of 34.9% in 2025.

The aerial survey services include capturing geographic, structural and environmental data with the use of aircraft, drones, and satellites to support the mapping, agriculture, construction, defense and urban planning.

The market is experiencing a rapid growth due to growing demand for highly precise mapping, infrastructure development, and increased use of UAVs owing to its lower costs and surging applications across environmental monitoring and disaster management.

Additionally, key players including Fugro, Hexagon AB (Leica Geosystems AG), NV5 Global Inc. (Quantum Spatial Inc.), PASCO Corporation, Trimble Inc., Topcon Corporation, CGG S.A., TGS ASA and others are adopting strategies such as investment in advanced sensors and LiDAR technology, forming partnerships with engineering firms and government bodies and expanding fleet of drones.

Download Free sample to learn more about this report.

Aerial Survey Service Market Key Takeaways

- 2025 Market Size: USD 8.31 billion

- 2026 Market Size: USD 9.17 billion

- 2034 Forecast Market Size: USD 20.13 billion

- CAGR: 10.3% from 2026–2034

- North America dominated the aerial survey services market with a 34.90% share in 2025.

- The Photogrammetry segment accounted for the largest market share of 41.22% in 2026.

- The Fixed-Wing Aircraft segment is projected to hold a 49.29% share in 2026.

North America

North America held 34.90% share in 2025, valued at USD 2.91 billion.

Asia Pacific

Asia Pacific market valued at USD 2.12 billion in 2025.

Europe

Europe market valued at USD 2.38 billion in 2025.

U.S.

Market projected to reach USD 2.45 billion by 2026.

China

Market projected to reach USD 1.14 billion by 2026.

Read More

MARKET DYNAMICS

Market Drivers

Technological Advancements Enhancing Aerial Data Precision and Efficiency Drives the Market Development

Increasing adoption of Unmanned Aerial Vehicles (UAVs), hyperspectral imaging technologies and advanced LiDAR systems tends to improve accuracy, efficiency, and cost-effectiveness of the aerial survey operations. Innovative sensors currently capture a high resolution topographic and geospatial data with a centimeter-level precision, thus supporting a diverse application across sectors including mining, infrastructure development, environmental monitoring and agriculture. Additionally, recent advancements are shifting the traditional surveying workflows into a data-driven and faster decision-making systems.

- For instance, according to the U.S. Federal Aviation Administration (FAA) and European Union Aviation Safety Agency (EASA), the commercial drone fleet is expanding at over 10% annually, reflecting the increasing reliance on aerial survey services for critical spatial intelligence.

Market Restraints

Regulatory Barriers and Skilled Workforce Shortage to Deters the Market Growth

The market for aerial survey services faces persistent regulatory and operational challenges. Stringent airspace management rules, limitations on Beyond Visual Line of Sight (BVLOS) flights, different drone operational policies across the countries delay the large-scale deployment of these services. Additionally, the shortage of certified pilots and expert data analysts capable of processing a high-volume LiDAR and photogrammetry datasets also constraints the scalability of projects. Different regulatory bodies and institutions including International Civil Aviation Organization (ICAO) and national aviation bodies are refining the UAV frameworks. However, inconsistency in implementation adds to the cost and uncertainty for global operators. These factors collectively limit the market expansion particularly for cross-border or government based projects.

Market Opportunities

Expanding Infrastructure and Energy Transition Projects Offers Lucrative Growth Opportunities

The global infrastructure renewal cycle and the augmenting transition toward a renewable energy offers substantial opportunities for aerial survey providers. Different projects in transportation, coastal resilience, urban planning, and offshore wind development is increasingly relying on the high-resolution geospatial data for environmental and design assessment.

- For instance, the World Bank and OECD estimate that infrastructure investment will exceed USD 90 trillion by 2040, with significant allocations for sustainable and digital infrastructure.

Additionally, aerial survey services, especially bathymetric, LiDAR, and thermal mapping, are vital for such projects, locating providers to capture value through unified data analytics and long-term monitoring contracts.

AERIAL SURVEY SERVICES MARKET TRENDS

Shift Toward Integrated Geospatial Intelligence Platforms Has Emerged as a Prominent Market Trend

The market is noticing a shift from standalone data collection toward end-to-end geospatial intelligence solutions. Leading players including Hexagon AB, Fugro and NV5 Global are expanding their services portfolios to include the cloud-based visualization, real-time data processing, and AI-driven asset analytics.

This also reflects a strategic pivot toward a recurring and software-based revenue models where the aerial survey data is continuously integrated and updated into client’s digital twins and asset management systems. This results in evolving competitive landscape from a traditional survey contractor to technology based geospatial partners thus offering continuous insight delivery instead of one-time mapping services.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Service Type

Surge in Use of Photogrammetry for a Large Scale-Mapping Boosts Segment Growth

Based on service type, the market is segmented into photogrammetry, LiDAR, thermal imaging, multispectral imaging, and others.

In 2024, photogrammetry segment held the largest aerial survey services market share and with a revenue of USD 297.90 billion. The photogrammetry segment is expected to lead the market, contributing 41.22% globally in 2026. This dominance is driven by surging use of photogrammetry for a large scale-mapping, environmental monitoring, infrastructure planning, majorly across the mining, construction and urban development projects. Its capability of delivering a high-resolution imagery with a cost effective data collection also supports the segment’s growth. It is also growing due to public sector policies boosting digital mapping and cadastral modernization.

On the other hand, the multispectral imaging segment held the highest CAGR of 15.60% in 2024. This growth is owing to its growing adoption in forestry management, precision agriculture, and coastal ecosystem monitoring. Additionally, the capability to capture detailed spectral data for soil quality, crop health, and vegetation analytics coupled with advancements in sensor and drone technology is also propelling the segment’s growth majorly across emerging economies.

To know how our report can help streamline your business, Speak to Analyst

By Platform

Longer Flight Endurance and High Payload Capacity Drives Fixed-Wing Aircraft Segment Growth

The market is divided into fixed-wing aircraft, rotary-wing aircraft (helicopters) and unmanned aerial vehicles (UAVs/drones), based on platform.

Among these, fixed-wing aircraft segment dominates the market with a revenue share of USD 3.90 Billion in 2024. The fixed-wing aircraft segment will account for 49.29% market share in 2026. This segmental growth is attributed to its ability to cover a large area effectively, thus making them a preferred platform for national mapping programs, wide-area environmental assessments, and corridor surveys. Additionally, their longer flight endurance and high payload capacity also allow the use of advanced LiDAR systems and cameras, thus supporting for a consistent demand from utilities, government agencies, and large-scale infrastructure projects.

The Unmanned Aerial Vehicles (UAVs/Drones) segment held highest CAGR of 14.25% in 2024. This segment’s growth is owing to its expanding use in small-area inspections, data acquisition and high frequency tasks across different sectors including construction, agriculture, energy and disaster response. Additionally, a lower operational cost, ongoing improvements and flexible deployment in sensor miniaturization as well as automated data processing are also augmenting the segment growth.

By Application

Widespread Application of Aerial Photography and Remote Sensing Across Infrastructure Planning Drives Segment Growth

The market is divided into aerial photography and remote sensing, data acquisition and analytics, mapping & surveying, 3D Modelling, disaster risk management and mitigation and others, based on application.

Among these, aerial photography and remote sensing segment dominated the market with a revenue share of USD 2.49 Billion in 2024. The aerial photography and remote sensing segment is expected to account for 31.62% of the market in 2026. This segment’s growth is driven by its widespread application across infrastructure planning, cartography, environmental monitoring and land-use management. Additionally, governments, commercial enterprises, and infrastructure planning are also relying on high resolution aerial imagery for spatial analytics and mapping, aided by sustained investment in geospatial infrastructure as well as urban development initiatives across the emerging and developed economies.

The data acquisition and analytics segment held highest CAGR of 14.17% in 2024. This segmental growth is attributed to growing demand for an integrated geospatial intelligence solution that integrates aerial data with advanced AI, analytics, and cloud based processing. Additionally, the surge in adoption of data based decision making across different sectors including agriculture, utilities and mining, coupled with the use of predictive modeling as well as 3D visualization tools is also expected to fuel the segment’s growth during the forecast period.

By End User

Crucial Role of Aerial Survey Services in Border Surveillance Drives Government and Defense Segment Growth

Based on end-user, the market is divided into government and defense, oil and gas, mining and minerals, agriculture, forestry, and others.

Among these, the government and defense segment dominates the market with a share of USD 2.10 billion in 2024. The government and defense segment will account for 27.26% market share in 2026. This growth is due to its crucial role in border surveillance, national mapping, and infrastructure monitoring. Additionally, government agencies as well as defense organizations are consistently investing in aerial data collection for coastal management, land administration, environmental protection, and disaster preparedness. Moreover, the integration of LiDAR, high-resolution photogrammetry, and multispectral imaging into a public geospatial infrastructure programs aided by agencies including U.S. Geological Survey (USGS), the European Space Agency, and National Defense Mapping Services, also boosts the segmental growth globally.

On the other hand, the agriculture segment held highly CAGR of 13.96% in 2024. This is attributed to the growing adoption of drone based monitoring solutions and precision farming technologies. Different aerial surveys equipped with a hyperspectral and multispectral sensors are growingly used for monitoring soil conditions, crop health and irrigation efficiency. Additionally, government supported digital agriculture initiatives across North America, Asia Pacific and Europe coupled with surging private sector investments in agritech platforms also foster the demand for data driven and high-frequency data to improve sustainability and productivity across modern farming operations.

AERIAL SURVEY SERVICES MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America Aerial Survey Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The market in North America reached USD 2.91 Billion in 2025, representing 34.90% of total market revenue, and is projected to reach USD 3.19 Billion in 2026. The regional growth is due to extensive government based geospatial programs and upgraded commercial adoption across different sectors including defense, infrastructure and environmental monitoring. Particularly, the U.S. benefits from advanced aviation ecosystem, strong presence of established aerial service providers and highly regulated airspace framework. Additionally, the United States Geological Survey’s 3D Elevation Program (3DEP) and the USDA’s National Agriculture Imagery Program (NAIP) have established continuous demand for high-resolution aerial mapping and LiDAR data. The U.S. leads the regional market with an expected revenue share of USD 2.45 billion in 2026.

Europe

Europe contributed approximately USD 2.38 Billion to the global market in 2025, accounting for 28.60% share, and is expected to reach USD 2.59 Billion in 2026. The Europe region is growing with an expected share of USD 2.38 billion in 2025. This regional growth is due to growing demand for a high resolution geospatial data, increased adoption of drones and LiDAR, and expanding infrastructure and urban planning. U.K., Germany, and France are some of the major contributors to the market growth with an expected revenue share of USD 0.46 billion, USD 0.52 billion and USD 0.34 billion respectively by 2026.

Asia Pacific

In 2025, the Asia Pacific market stood at USD 2.12 Billion, representing 25.50% of global demand, and is projected to grow to USD 2.39 Billion in 2026. This regional growth is attributed to the surge in large-scale infrastructure development, rapid urbanization and growing public-private investments in spatial data modernization. Additionally, countries including India, Japan, and China are also deploying aerial survey solutions for transportation planning, smart city initiatives, and resource mapping. The rapid adoption of multispectral imaging technologies and drones, supportive regulatory policies and cost effectiveness of UAV operations tends to enable a broader accessibility of aerial mapping services. With private and government enterprises looking for data-driven planning and environmental monitoring, the market is noticing a rapid growth globally. India and China are the major contributors for the market growth with an expected revenue share of USD 0.34 billion and USD 1.14 billion by 2026.

South America and Middle East & Africa

Middle East & Africa maintained a strong presence in the global market, reaching USD 0.41 Billion in 2025, accounting for 5.00% share, and is expected to reach USD 0.46 Billion in 2026. This is attributed to the rising mining and oil & gas projects, rising infrastructure development and increased demand or environmental monitoring. GCC countries are predicted to have a market share of USD 0.21 billion by 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Focusing on Strategic Partnerships to Retain their Market Positions

The aerial survey services industry includes different global giants including Fugro, Hexagon AB (Leica Geosystems AG), NV5 Global Inc. (Quantum Spatial Inc.), PASCO Corporation, Trimble Inc., Topcon Corporation, CGG S.A., TGS ASA and others. These firms focus on strategic partnerships, bundled offerings to drive differentiation, and adopting new technologies to sustain market consistency.

LIST OF KEY AERIAL SURVEY SERVICES COMPANIES PROFILED:

- Fugro (Netherlands)

- Hexagon AB (Leica Geosystems AG) (Sweden)

- NV5 Global Inc. (Quantum Spatial Inc.) (U.S.)

- PASCO Corporation (Japan)

- Trimble Inc. (U.S.)

- Topcon Corporation (Japan)

- CGG S.A. (France)

- TGS ASA (Norway)

- BGP Inc., China National Petroleum Corporation (CNPC) (China)

- WesternGeco (Schlumberger Limited) (U.S.)

- Kokusai Kogyo Co., Ltd. (Japan)

- Blom ASA (NRC Group ASA) (Norway)

- Woolpert Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- November 2025: Egypt is set to conduct a comprehensive airborne geophysical survey of mineral potential nationwide under a Memorandum of Understanding (MoU) signed between the Mineral Resources and Mining Industries Authority and Spain’s Xcalibur Smart Mapping. The project will provide technological solutions for planning and evaluating mineral-rich deposits across the nation.

- November 2025: Califf Surveying, a leader in precision surveying and geospatial solutions, has launched new products. They are currently an Authorized Distributor of Leica Geosystems' advanced 3D laser scanning technology. The new lineup changes the way teams plan and deliver projects. This includes construction, infrastructure, and engineering projects. These changes affect Southeast Asia and the rest of the world.

- October 2025: Vexcel Imaging announced that the UltraCam Dragon 4.2, unveiled at Intergeo 2025, has been awarded the Wichmann Innovations Award 2025 in the 'Hardware and Software' category. The Dragon 4.2 impressed both the expert and audience juries as a highly efficient and versatile hybrid aerial mapping system for high-resolution mapping of complex environments. At its core are the new IMX811 CMOS sensors from Sony, which power two nadir (RGB and NIR) and four oblique RGB cameras (each 19,136 × 12,736 pixels).

- April 2025: Terra Drone Corporation (“Terra Drone”), recognized as the No.1 Drone Service Provider in the world, has signed a Memorandum of Understanding (MOU) with Aramco, one of the world’s leading integrated energy and chemicals companies in Saudi Arabia. This collaboration signifies a strategic partnership to explore innovation in drones, robotics, and AI-driven solutions tailored to the oil and gas sector, supporting localization efforts.

- April 2025: JTB Corp., fly Inc. and Japan Airlines Co., Ltd. announced the launch of "SKYPIX", Japan's first automated unmanned aerial photography service using drones with AI-powered automated video editing, to create attractive sightseeing spots.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, service type, platform, application and end user of the product. Besides this, it offers insights into the aerial survey services market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Growth Rate |

CAGR of 10.3% from 2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Service Type, Platform, Application, End User and Region |

|

By Service Type |

|

|

By Platform |

|

|

By Application |

|

|

By End User |

|

|

By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 9.17 billion in 2026 and is projected to reach USD 20.13 billion by 2034.

The market is expected to exhibit steady growth at a CAGR of 10.3% during the forecast period.

Technological advancements enhancing aerial data precision and efficiency drives the market growth.

Fugro, Hexagon AB (Leica Geosystems AG), NV5 Global Inc. (Quantum Spatial Inc.), PASCO Corporation, Trimble Inc., Topcon Corporation, CGG S.A., TGS ASA, and others are some of the top players in the market.

The North America region held the largest market share.

North America was valued at USD 2.91 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us