Agriculture Waste Management Market Size, Share & Industry Analysis, By Waste Type (Crop Residues, Animal Manure and Bedding Materials, Food Processing Waste, and Agricultural by Products), By Management Services (Waste Collection, Transportation, Storage, and Processing Services), By Disposal Treatment Process (Composting, Anaerobic Digestion, Biomass Conversion, Bioenergy Production, and Recycling), and Regional Forecast, 2025-2032

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

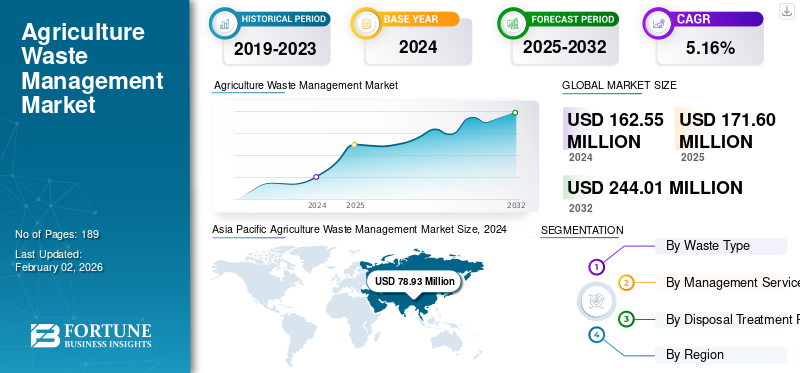

The global agriculture waste management market size was valued at USD 162.55 million in 2024. It is projected to be worth USD 171.60 million in 2025 and reach USD 244.01 million by 2032, exhibiting a CAGR of 5.16% during the forecast period. Asia Pacific dominated the global market with a share of 48.56% in 2024.

Governments and organizations globally are promoting circular economy approaches. Agricultural residues are increasingly reused as feedstock for compost, biogas, biochar, bioplastics, and other value-added products, pushing demand in the sector. Advancements in composting (e.g., aerobic, vermicomposting), anaerobic digestion, pyrolysis, and microbial treatment are significantly enhancing the efficiency and scale of waste to resource conversion, including bioenergy and organic fertilizers.

The growing market share of agriculture waste management is fueled by environmental regulations, economic opportunity from resource recovery, and technological evolution that turns waste into value. This leads to the growth of global agricultural waste. Veolia, Suez Environment, Clean Harbors, Inc. are among the world’s largest environmental services companies, operating across the entire water, waste energy lifecycle from collection to nutrient recovery and energy valorization.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increase in Agricultural Waste Generation to Drive Market Growth

The rapid expansion of global agricultural activities has led to a significant increase in waste generation, including crop residues, animal manure, agro-industrial byproducts, and farm wastewater. This surge in waste volume is putting pressure on traditional disposal methods and creating a strong demand for efficient, sustainable, and scalable agricultural waste management solutions. With growing environmental concerns and the need to comply with regulations on pollution control and nutrient runoff, farmers and agribusinesses are increasingly turning to structured waste management systems.

In June 2025, in order to address growing global demand and severe capacity deficits, Veolia, a company with headquarters in France that provides comprehensive hazardous waste solutions, stated that by 2030 it will have added 5,30,000 tons of new annual hazardous waste treatment capacity.

MARKET RESTRAINTS

High Initial Investment and Lack of Infrastructure to Hinder Market Growth

One of the primary restraints affecting the agricultural waste management market growth is the high initial cost of equipment and infrastructure required for proper waste handling, treatment, and recycling. Technologies including anaerobic digesters, composting systems, biogas plants, and wastewater treatment units often require significant capital investment, which can be a barrier, especially for small and marginal farmers.

In addition, many rural and developing regions lack the necessary infrastructure, such as waste collection systems, transportation logistics, and treatment facilities. This makes it difficult to implement efficient agricultural waste management practices on a large scale.

MARKET OPPORTUNITIES

Expansion of Bioenergy Projects to Create Opportunistic Growth for Market

The growing global demand for clean and renewable energy is leading to the rapid expansion of bioenergy projects, particularly biogas and biomass power plants. Agricultural waste, such as crop residues, animal manure, and organic farm byproducts, serves as a key feedstock for these projects. As countries work toward reducing greenhouse gas emissions and diversifying their energy mix, government policies and subsidies are increasingly supporting waste-to-energy initiatives. This creates a strong opportunity for agricultural waste management to grow, encouraging the collection and processing of farm waste for energy generation.

In February 2022, in Alagoas, steam from eucalyptus biomass will be used to generate renewable energy as part of a BRL 400 million (USD 71,566) investment agreement between Veolia and Braskem. The initiative will produce 900,000 tons of steam annually for 20 years, resulting in a reduction of around 150,000 tons of CO2 emissions annually.

AGRICULTURE WASTE MANAGEMENT MARKET TRENDS

Rising Adoption of Waste-to-Energy Technologies to Drive Market Growth

The increasing adoption of waste-to-energy technologies is a major factor driving the growth of the agricultural waste management industry market. Technologies such as anaerobic digestion, biogas production, pyrolysis, and biomass combustion are being widely implemented to convert agricultural waste such as crop residues, manure, and organic farm byproducts into useful energy forms such as electricity, heat, and biofuels.

By transforming waste into energy, these technologies not only help manage the large volume of agricultural waste sustainably but also create economic value for farmers and energy producers.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Waste Type

Increasing Livestock Farming Activities to Drive Animal Manure and Bedding Materials Segment Growth

The market by waste type covers crop residues, animal manure and bedding materials, food processing waste, and agricultural byproducts.

Animal manure and bedding materials are the dominating segment in the market. Governments (especially in the U.S., Europe, and parts of Asia) are enforcing stricter regulations on manure runoff, groundwater contamination, and methane emissions from livestock operations. Proper treatment and disposal of manure and bedding waste are now mandatory in many regions, driving growth in waste management systems.

Crop residues are the second largest segment in the market. Unlike manure or agro-processing waste, crop residues are produced on nearly every farm, making residue management a universal need across geographies and crop types.

By Management Services

Large Volume of Distributed Agricultural Waste to Lead Waste Collection Growth

By management services, the market is segmented into waste collection, transportation, storage, and processing services.

Waste collection dominates the agriculture waste management market. Waste collection forms the foundation of the entire waste management process. Without proper collection, agriculture waste such as crop residues, animal manure, and agro-processing byproducts cannot be processed, treated, or utilized effectively.

Transportation is the fastest growing segment in the market. The growth of bioenergy projects and large-scale composting units is increasing the need to move waste efficiently. More infrastructure means more trips, more volume, and more investment in transport systems.

By Disposal Treatment Process

High demand for Organic Fertilizers is Expected to Drive Composting Segment Growth

The market is segmented by disposal treatment process analysis into composting, anaerobic digestion, biomass conversion, bioenergy production, and recycling.

Composting is the dominating segment in the market. Composting is one of the most cost-effective and low-tech methods of managing organic agricultural waste. Due to its simplicity and minimal capital investment, it is widely adopted by smallholder farmers and large agribusinesses alike.

The Anaerobic digestion is the second largest segment in the market. Anaerobic digestion is ideal for treating organic waste such as animal manure, crop residues, food processing byproducts, and silage and green waste. Farms and agro-industrial units produce large volumes of these materials, making AD a practical and efficient waste treatment option.

AGRICULTURE WASTE MANAGEMENT MARKET REGIONAL OUTLOOK

The market has been analyzed geographically in North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa. Asia Pacific is the dominating region in the market.

Asia Pacific

Asia Pacific Agriculture Waste Management Market Size, 2024 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is dominating the agriculture waste management market share. Asia Pacific countries including China, India, Indonesia, and Vietnam are among the world’s largest producers of rice, wheat, sugarcane, and vegetables. This results in a massive volume of crop residues and animal waste, driving the urgent need for effective collection, treatment, and reuse. Countries in the Asia Pacific are supporting agricultural waste management through India’s National Bio-Energy Mission and China’s Five-Year Plans, promoting circular agriculture.

North America

North America, particularly the U.S. and Canada, has a large-scale, industrialized agricultural sector, which generates significant volumes of waste, including crop residues, animal manure, and agro-industrial waste. Agencies including the U.S. Environmental Protection Agency (EPA) and Environment and Climate Canada are enforcing waste disposal laws, water and soil protection standards, and emissions controls (methane, ammonia from manure). This regulatory push encourages farmers and agribusinesses to adopt proper waste management practices, including composting, anaerobic digestion, and recycling.

U.S.

The U.S. has one of the world’s largest agricultural sectors with massive livestock operations, extensive crop production. This generates large quantities of manure, crop residues, and agro-industrial waste, requiring structured waste handling and treatment systems. Agencies including EPA and state regulators have enforced manure lagoon standards, air and water pollution limits, and zero-waste goals.

Europe

The European Union has some of the world’s strictest environmental laws, such as the EU Waste Framework Directive, the Nitrates Directive, and the circular economy action plan. These push farms and agro industries to adopt sustainable waste management practices, including composting, anaerobic digestion, and nutrient recycling. Countries including Germany, France, the Netherlands, and Spain have intensive livestock farming that produces significant amounts of animal manure, bedding waste, and wastewater.

Latin America

Countries such as Brazil, Argentina, and Mexico have vast agricultural sectors producing sugarcane, soybean, maize, coffee, and beef, resulting in significant amounts of crop residues, manure, and agro-industrial waste. This creates a growing need for efficient waste collection, treatment, and reuse systems. Brazil is leading with sugarcane biogases-based power and on-farm digesters. Colombia and Chile are scaling up bioenergy from animal waste.

Middle East and Africa

Despite arid conditions in parts of the Middle East and water scarcity in Africa, countries including Egypt, South Africa, Kenya, Morocco, and Nigeria. Saudi Arabia and the UAE (through controlled environment farming) are seeing increased agricultural production, which results in rising volumes of crop residues, animal manure, and agro-industrial waste. South Africa, Egypt, and Kenya are investing in biogas digesters and biomass-to-energy systems. Gulf countries (E.g., UAE, Saudi Arabia) are exploring waste valorization for energy as part of Vision 2030 and green transition initiatives.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Leading Vendors are Increasingly Focusing on Strategic Collaboration and Joint Ventures, Driving Market Growth

In July 2025, in order to test the agronomic benefits of biochar on a number of farms in the Loiret department in the center of France, SUEZ and Seabex, a French AgriTech startup that specializes in agricultural resource management and irrigation optimization, announced the signing of a partnership. With offices in Orléans, Strasbourg, and Nancy, Aquanova is a center for water industry competitiveness that leads initiatives to create innovative projects in response to issues facing France's water resources and regional development. This groundbreaking collaboration between a large French corporation and an AgriTech startup is a direct result of Aquanova's efforts.

List of Key Agriculture Waste Management Companies Profiled

- Veolia (France)

- Suez Environment (France)

- Clean Harbors (U.S.)

- Waste Management, Inc. (U.S.)

- Renewi PLC (U.K.)

- Biogen (U.S.)

- Agrivert (U.K.)

- Recology (U.S.)

- Viridor (U.K.)

- HomeBiogas (Israel)

- FCC Environment (U.K.)

- Covanta Holding Corporation (U.S.)

- Advanced Disposal Services Inc. (U.S.)

- Stericycle Inc. (U.S.)

- Republic Services Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In March 2024, in order to collaborate on finding technological solutions in the area of waste management and recovery, SUEZ and the MAScIR Foundation, the Moroccan Foundation for Advanced Science, Innovation, and Research, which is a part of the Mohammed VI Polytechnic University (UM6P), have signed a Memorandum of Understanding (MoU). The goal of the collaboration is to create sustainable, cutting-edge circular solutions for waste management and recycling.

- In March 2024, SUEZ, a global leader in circular solutions for water and waste management, and AFYREN, a greentech firm that uses fermentation technology to create sustainable, low-carbon ingredients for manufacturers using a circular model, are collaborating on a novel method of extracting value from organic waste.

- In August 2023, Biogen, a firm that owns and manages green energy anaerobic digestion (AD) facilities, purchased a portfolio of five operating plants from The Ingenious Group.

- The transaction, the financial specifics of which are not made public, enhances Biogen's production capability and extends its footprint of green energy AD facilities throughout the U.K.

- Organic waste, the majority of which would otherwise be disposed of in landfills, is recycled by Biogen to create sustainable energy and nutrient-rich fertilizer.

- In April 2022, Valencia Waste Management was the new name for the company that owns Viridor's landfill and landfill gas operations. The sale of Viridor's assets to Frank Solutions was made public. Valencia Waste Management is the new name for Frank Solutions. The sale involved the operation and administration of 44 locations around the nation, with all 200 employees moving across and the senior management staff remaining in place.

- In July 2021, Covanta Holding Corporation, a Waste-to-Energy facility owner and operator in North America, was acquired by EQT Infrastructure. The agreement, which Covanta's Board unanimously approved of Directors, calls for shareholders to get USD 20.25 in cash for each share of Covanta's common stock in a transaction valued at USD 5.3 billion, including the assumption of Covanta's net debt commitments.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects such as leading companies, products, service processes, competitive landscape, and the leading agriculture waste management market. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 5.16% from 2025 to 2032 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Waste Type

|

|

By Management Services

|

|

|

By Disposal Treatment Process

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 162.55 million in 2024.

In 2024, the Asia Pacific market value stood at USD 78.93 million.

The market is expected to exhibit a CAGR of 5.16% during the forecast period of 2025-2032.

The waste collection segment led the market by management services.

Rising Agricultural Waste Generation to drive the Market

Some of the top major players in the market are Veolia, Suez Environment, Clean Harbors, Inc., and Others.

Asia-Pacific dominated the market in 2024.

- 2019-2032

- 2024

- 2019-2023

- 189

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us