AI in Cardiology Market Size, Share & Industry Analysis, By Component (Hardware/Devices and Software & Services), By Deployment (Cloud-Based, On Premise, & Hybrid), By Technology (Machine Learning & Deep Learning, Natural Language Processing, & Others), By Indication (Arrhythmia/AF, Heart Failure, CAD/Ischemic, Structural/Valvular, Cardiomyopathies, & Others), By Application (Screening & Early Detection, Imaging Analysis, ECG Interpretation & Monitoring, Risk Stratification & Prognosis, Treatment Planning/CDS, Workflow/Ops Automation, & Others), By End User, and Regional Forecast, 2026-2034

AI in Cardiology Market Size and Future Outlook

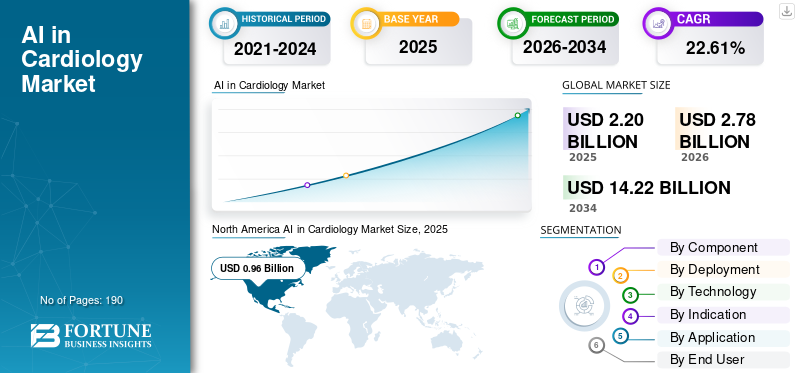

The global AI in cardiology market size was valued at USD 2.20 billion in 2025. The market is projected to grow from USD 2.78 billion in 2026 to USD 14.22 billion by 2034, exhibiting a CAGR of 22.61% during the forecast period. North America dominated the AI in cardiology market with a market share of 43.64% in 2025.

The global market is poised for significant growth in the upcoming years. The market focuses on using machine learning and advanced analytics to support faster, more consistent heart care decisions across applications such as ECG, echocardiography, and remote monitoring. The market is anticipated to grow as the cardiovascular disease burden rises. Cardiology health providers face heavier diagnostic workloads, prompting vendors to adopt AI tools to automate routine tasks and streamline reporting and triage within everyday clinical workflows. Over time, deeper integration of AI into EHR/PACS and cardiac imaging systems is accelerating adoption across sites, driving market growth. Key companies are participating in strategic collaborations and acquisitions to enhance their market capabilities.

- For instance, in December 2025, Koninklijke Philips N.V. acquired SpectraWAVE, Inc., an innovator in EVI (Enhanced Vascular Imaging) of coronary arteries, AI in medical imaging, and angiography-based physiology assessments. The team aims to advance next-generation coronary intravascular imaging and physiological assessment using AI. Such developments are anticipated to boost the global market growth.

Furthermore, leading players in the industry, such as GE HealthCare Technologies Inc., Koninklijke Philips N.V., Siemens Healthineers AG, and Canon Medical Systems Corporation, are directing their resources toward technological advancements and new product launches to strengthen their market positions.

Download Free sample to learn more about this report.

AI in Cardiology Market Key Takeaways

- 2025 Market Size: USD 2.20 billion

- 2026 Market Size: USD 2.78 billion

- 2034 Forecast Market Size: USD 14.22 billion

- CAGR: 22.61% from 2026–2034

- North America dominated the AI in cardiology market with a 43.64% share in 2025.

- The hardware/devices segment is projected to grow at a CAGR of 18.34% during the forecast period.

- The hybrid segment is projected to grow at a CAGR of 21.05% during the forecast period.

North America

North America maintained its leading position, reaching a market value of USD 0.96 billion in 2025.

Europe

Europe is projected to record the second-highest regional growth rate of 22.44% and reach USD 0.76 billion in 2026.

Asia Pacific

Asia Pacific is expected to reach USD 0.58 billion in 2026, securing the third-largest regional position.

U.S.

The market is estimated to reach USD 1.11 billion in 2026, accounting for approximately 39.75% of global revenue.

Japan

The market is estimated to reach USD 0.10 billion in 2026, representing around 3.62% of the global market.

Read More

AI IN CARDIOLOGY MARKET TRENDS

Broader Use of AI to Standardize Cardiac Imaging Interpretation at Sites

Broader use of AI tools to standardize cardiac imaging is a prominent trend in the global market. As cardiology networks expand, the same cardiac scan can be performed on different machines by other operators across sites, often leading to variation in measurements and reporting. When results are inconsistent, clinicians spend extra time reconciling findings, repeat tests increase, and it becomes harder to compare a patient's disease progression over time. This creates strong demand for AI that standardizes cardiac imaging interpretation by automating key measurements, applying consistent quantification rules, and producing more uniform reports across echo and cardiac CT/MR workflows. As healthcare systems push for scalable, one-for-all care across hubs, integrating these AIs provides an efficient alternative to reduce inter-site variation. It also improves variability while improving turnaround time and confidence in clinical decisions.

- For instance, in August 2025, Koninklijke Philips N.V. highlighted AI driven cardiac solutions and its Cardiovascular Workspace to integrate imaging data across systems and support collaboration and workflow efficiency at ESC Congress 2025. Such developments are expected to boost market growth.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Cardiovascular Disease Burden and Aging Population to Drive Market Growth

The rising cardiovascular disease (CVD) burden and a fast-growing elderly population are key drivers of AI in cardiology market growth. Other factors comprise increasing patient volumes requiring cardiac screening, imaging, and long-term monitoring, resulting in high data output and prompting AI integration to improve workflows. As volumes rise, cardiology teams face heavier workloads and longer turnaround times, which can delay diagnosis and treatment decisions. This pressure makes manual interpretation and reporting harder to scale. As a result, providers are adopting AI to automate routine measurements, prioritize high-risk cases, and standardize interpretation, enabling more patients to be assessed with the same clinical capacity. These factors, collectively, result in higher demand and boost market growth.

Key companies are focusing on new product launches with innovative AI features integrated into their offering to capitalize on the market growth.

- For instance, in August 2024, Siemens Healthineers received the U.S. FDA clearance for ACUSON Origin, a dedicated cardiovascular ultrasound system powered by artificial intelligence (AI) These features can help physicians perform cardiac procedures more efficiently across diagnostics, structural heart disease, and electrophysiology. Such factors highlight the drivers, propelling market growth.

MARKET RESTRAINTS

Data Privacy, Security, and Consent Constraints for Cardiac Data to Hamper Market Growth

One of the critical factors restraining market growth is the concern about data privacy and security for cardiac data. Patient data is the fuel for artificial intelligence in cardiology, but these cardiac datasets are highly sensitive and often spread across multiple systems. When consent requirements, cross-border data rules, and hospital governance policies limit how data can be accessed or shared, companies and providers face delays in building, training, and validating models at scale. These constraints also make it harder to combine multi-site data, reducing model generalizability and slowing regulatory and clinical acceptance. As a result, deployments take longer, integrations become more complex, and some health systems postpone adoption until privacy and governance risks are fully addressed.

- For instance, in June 2025, a BMJ report noted that NHS England faced a referral to the U.K. Information Commissioner's Office over access granted for training an AI model on GP patient data, and that the model's development was paused, highlighting how privacy and consent concerns can slow AI initiatives.

MARKET OPPORTUNITIES

AI-Based Triage and Prioritization for Acute Cardiac Cases to Improve Time-To-Treatment and Unlock New Growth Opportunities

With increasing investment and the emergence of innovative AI features, the market offers expansion opportunities in AI based triage and prioritization of acute cardiac cases. Emergency departments deal with high volumes of chest pain and suspected heart attack cases, increasing the case load and fast decision-making for immediate escalations. AI adoption in these workflows addresses challenges such as delays and inconsistency, and escalates the time-to-treatment for patients with true acute coronary syndrome. This creates a clear opportunity for AI to standardize decision pathways and prioritize high-risk cases using objective signals so clinicians can move the right patient to the right care pathway faster.

- For instance, in April 2025, Hoffmann-La Roche Ltd received CE Mark from the U.S. FDA for its Chest Pain Triage algorithm to help differentiate cardiac vs. non-cardiac chest pain and support faster, standardized triage decisions in emergency care. Such developments offer market growth opportunities.

MARKET CHALLENGES

Integration Challenges with EHR/PACS and Cardiology Workflows May Hamper Market Growth

A prominent challenge in the market is the lack of compatibility and integration with standard formats. Cardiology AI can only deliver value when its results appear in the tools clinicians already use. When AI outputs are housed in a separate portal, it adds clicks, interrupts routine workflows, and increases the IT workload of building, testing, and maintaining integrations. This friction slows deployments, limits day-to-day usage, and makes it harder to scale AI beyond a pilot site, even if the algorithm performs well clinically. Over time, the operational burden of integration and ongoing maintenance becomes a practical barrier for many hospitals, especially those running mixed vendor systems and legacy infrastructure.

- For instance, in June 2024, an RSNA Radiology primer on adopting AI in imaging workflows notes that custom integrations create a substantial operational and maintenance burden and can increase the likelihood of unanticipated problems. This illustrates why seamless PACS/EHR integration is a key hurdle for real-world deployment. Such high implementation costs are slowing adoption.

Segmentation Analysis

By Component

New Product Launches to Propel Software & Services Segment Growth

Based on component, the market is categorized into hardware/devices and software & services.

Among these, the software & services segment accounted for the largest share of the AI in cardiology and pharma in 2025. Cardiology teams generate large volumes of ECG, echo, and cardiac imaging data. Still, the biggest bottleneck is not the device itself. It is the time needed to interpret results, document findings, and turn them into clinical decisions. When hospitals want faster turnaround and more consistent reporting, they typically adopt AI first as software modules and service layers that automate measurements, support interpretation, and streamline workflow inside existing systems. This makes adoption easier as software can be deployed across multiple sites and modalities without replacing installed hardware, and upgrades can be delivered continuously as AI algorithms improve. As a result, software & services tends to dominate as it scales faster, integrates more readily into daily routines, and provides measurable productivity and standardization benefits at lower disruption than hardware refresh cycles. Such bundled AI solutions for implementation/support drive segment growth.

Additionally, new product launches by key companies to digitalize manufacturing workflows are likely to push segmental expansion.

- For instance, in June 2024, Philips announced AI capabilities for cardiovascular ultrasound to help diagnose more patients by integrating them into cardiovascular ultrasound workflows. Such developments are expected to drive the segment's growth.

The hardware/devices segment is expected to grow at a CAGR of 18.34% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Shift toward Cloud-Based Platforms for Scalability to Drive the Segmental Growth

Based on deployment, the market is segmented into cloud-based, on-premises, and hybrid.

Among these, cloud-based deployment accounted for the largest AI in cardiology market share in 2025. Cardiology networks increasingly operate across multiple hospitals and outpatient centers, creating a need for shared, immediate access to images, reports, and longitudinal patient history. Cloud-based deployment allows centralized data access, enables faster software updates, and supports remote reading and collaboration across sites. As health systems prioritize operational efficiency and scalability, cloud-based models are the preferred approach for consistently expanding AI enabled cardiology workflows across medical players. Key companies are depicting a shift toward cloud-based models that improve scalability and reduce the operational burden of maintaining complex manufacturing applications.

- For instance, in October 2025, Intelerad announced the next generation of InteleHeart, described as a cloud-native cardiology workflow solution that unifies viewing, reporting, analytics, and workflow orchestration.

In addition, the hybrid segment is projected to grow at a CAGR of 21.05% over the study period.

By Technology

Increasing Research and Development to Bring Forward Innovative Technologies Reinforcing Others Segmental Growth

Based on technology, the market is segmented into machine learning & deep learning, natural language processing, and others.

In 2025, the others segment dominated the market in terms of technology. The other segment comprises innovative technologies such as computer vision, statistics and probabilistic models, scheduling, and analytics, among others. Cardiology problems cannot be solved by a single AI technique alone as real-world workflows combine signals, images, clinical context, and operational rules. As datasets become more multi-modal and implementation expectations rise, buyers increasingly prefer platforms that support broader applications. Furthermore, investment and technological advancements in the segment are increasing to bring forward innovative technologies. Such factors drive the segment's growth.

- For instance, in July 2025, Philips launched an ECG AI Marketplace to give cardiac teams access to a broad portfolio of AI tools to enhance early cardiac diagnosis.

The natural language processing segment is projected to grow at a CAGR of 24.11% during the forecast period.

By Indication

Rising Prevalence of Arrhythmia/AF to Fuel Segmental Growth

Based on indication, the market is segmented into arrhythmia/AF, heart failure, CAD/ischemic, structural/valvular, cardiomyopathies, and others.

In 2025, the arrhythmia/AF segment dominated the market. The segment's high share is due to its increasing prevalence. Atrial fibrillation is a high-volume, high-impact condition where missed or delayed detection can lead to serious downstream events such as stroke and hospitalization. AI can automate detection, reduce review burden, help prioritize clinically reasonable events for faster action, and assist with large data sets. As providers focus on scaling monitoring programs without overwhelming staff, AI adoption is concentrated in arrhythmia/AF workflows, reinforcing this segment's dominance. Highlighting the critical nature of the indications, many key companies are participating in strategic collaborations for research and development to expand the understanding of indications.

- For instance, in September 2025, HeartBeam reported that its deep learning algorithms showed high accuracy in detecting arrhythmias, including the classification of atrial fibrillation patterns.

The heart failure segment is projected to grow at a CAGR of 23.74% during the forecast period.

By Application

Wide Utilization of Cardiac Imaging to Fuel Imaging Analysis Segmental Growth

Based on application, the market is segmented into screening & early detection, imaging analysis, ECG interpretation & monitoring, risk stratification & prognosis, treatment planning/CDS, workflow/ops automation, and others.

In 2025, the imaging analysis segment dominated the market by application. These applications produce complex datasets in which clinicians must extract multiple measurements and observations before reaching a diagnosis, and manual steps can introduce variability and slow reporting. As imaging volumes rise, hospitals seek AI that automates routine measurements, standardizes quantification, and speeds interpretation, enabling imaging labs to deliver consistent results across operators and sites. AI tools are widely used for the image analysis of large datasets. Underscoring these varied advantages, key companies are directing their resources toward strategic collaborations and new product launches to commercialize the segment's growth potential.

- For instance, in March 2025, FUJIFILM announced a partnership with Us2.ai to provide AI-automated echocardiography analysis using its ultrasound system, automating analysis and reporting.

The treatment planning/CDS segment is projected to grow at a CAGR of 23.49% during the forecast period.

By End User

Revenue Generation Potential for Healthcare Providers to Push Segment Growth

Based on end user, the market is segmented into healthcare payers, healthcare providers, academic & research institutes, diagnostic laboratories, and others.

By end user, the healthcare providers segment accounted for the largest market share in 2025. They bear the direct operational burden of cardiac diagnosis and treatment, fueling the demand. Further, they are most strongly impacted by backlogs, staffing constraints, and turnaround times. When providers adopt AI, they can realize immediate workflow benefits with faster reads, standardized reporting, and better prioritization of high-risk cases. Recognizing the critical applications, the market is witnessing strategic collaborations between AI solution providers and healthcare providers to increase the adoption of these tools.

- For instance, in November 2025, GE HealthCare Technologies Inc. announced plans to acquire Intelerad to expand cloud-enabled enterprise imaging and workflow solutions across care settings, showing how major vendors are investing to scale AI- and cloud-driven imaging informatics.

The healthcare payers segment is projected to grow at a CAGR of 23.59% over the study period.

AI in Cardiology Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America AI in Cardiology Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 with a value of USD 0.76 billion and maintained its leading position in 2025 with a valuation of USD 0.96 billion. The market in North America is expected to grow significantly over the forecast period, as the region faces high cardiac test volumes and strong pressure to shorten the turnaround times for diagnosis and reporting.

U.S. AI in Cardiology Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market can be estimated at around USD 1.11 billion in 2026, accounting for roughly 39.75% of the global market.

Europe

The Europe market is projected to grow at a rate of 22.44% over the forecast period, the second-highest among all regions, and reach a valuation of USD 0.76 billion by 2026. The region is expected to experience robust growth driven by regulatory bodies' push for standardized cardiac imaging and faster reporting across regions.

U.K. AI in Cardiology Market

The U.K. market is estimated to touch around USD 0.13 billion in 2026, representing roughly 4.73% of the global market.

Germany AI in Cardiology Market

The Germany market is projected to reach approximately USD 0.16 billion in 2026, equivalent to around 5.69% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 0.58 billion in 2026 and secure the position of the third-largest region in the market. The region's growth is driven by the rising CVD burden and large patient populations, which are increasing the demand for faster screening and follow-up.

Japan AI in Cardiology Market

The Japan market is estimated to reach around USD 0.10 billion in 2026, accounting for approximately 3.62% of the global market.

China AI in Cardiology Market

The China market is projected to be among the largest worldwide, with 2026 revenues estimated at around USD 0.22 billion, representing approximately 8.02% of global sales.

India AI in Cardiology Market

The India market is estimated to reach around USD 0.08 billion in 2026, accounting for roughly 3.01% of the global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market is set to reach a valuation of USD 0.15 billion in 2026. The regional market is expanding driven by increased government support and growing regional healthcare modernization programs. In the Middle East & Africa, the GCC segment is set to reach USD 0.04 billion in 2026.

South Africa AI in Cardiology Market

The South African industry is projected to reach approximately USD 0.04 billion by 2026, accounting for roughly 1.27% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

New Product Launches by Prominent Players to Enhance their Market Share

The global AI in cardiology market is highly consolidated, with companies such as GE HealthCare Technologies Inc., Koninklijke Philips N.V., Siemens Healthineers AG, and Canon Medical Systems Corporation holding a considerable market share. Increased investments, strategic collaborations, new product launches, technological advancements, and strategic takeovers in the sector drive these companies' market share gains.

- For instance, in December 2025, Siemens Healthineers launched Syngo.CT Coronary Cockpit Software to advance coronary artery disease management. The software is equipped with AI-driven and automated plaque analysis and PCI planning with coronary CT imaging. Such developments are aimed at driving market growth.

Other notable players in the global market include Medtronic plc, iRhythm Technologies, Inc., and Heartflow, Inc. These companies are anticipated to prioritize strategic partnerships, technological advancements, and new product launches for consolidating their position during the forecast period.

LIST OF KEY AI IN CARDIOLOGY COMPANIES PROFILED

- GE HealthCare Technologies Inc. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Siemens Healthineers AG (Germany)

- Canon Medical Systems Corporation (Japan)

- Medtronic plc (Ireland)

- iRhythm Technologies, Inc. (U.S.)

- Heartflow, Inc. (U.S.)

- Cleerly, Inc. (U.S.)

- Ultromics Ltd. (U.K.)

- Eko Health, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: UltraSight received clearance from the U.S. FDA for PVAD IQ, an imaging tool utilized with the company's Echo Stewardship Platform. The solution is designed for supporting echocardiography in managing patients with a microaxial flow pump.

- February 2026: Gentuity LLC collaborated with GE HealthCare to improve the availability of Gentuity's HF-OCT Imaging System and Vis-Rx PRIME Micro-Imaging Catheter. The collaboration aimed to advance patient care by providing innovative tools designed to enable more precise planning and treatment for percutaneous coronary interventions (PCIs).

- October 2025: Heartflow, Inc. introduced Heartflow PCI Navigator for the Heartflow One platform. PCI Navigator is an AI-driven and integrated PCI (percutaneous coronary interventions) planning tool that provides interventional cardiologists with a patient-specific 3D model detailing plaque composition, anatomy, and lesion-specific physiology, aligned for the optimization of potential stent placement.

- October 2025: Medtronic partnered with DASI simulations for advancing the future of TAVR through personalized planning and predictive modeling. The partnership launched an AI solution for the personalization of valve treatment planning decisions and improving predictive heart valve visualization, allowing TAVR’s future for structural heart patients.

- July 2021: Medtronic plc received 51(k) clearance for two AccuRhythm AI algorithms for usage with the LINQ II ICM (insertable cardiac monitor). AccuRhythm AI applies AI to heart rhythm event data collected by LINQ II, enhancing the precision of information physicians receive so that they can better treat and diagnose abnormal heart rhythms.

REPORT COVERAGE

The global AI in cardiology market analysis includes a comprehensive study of market size & forecast across all market segments covered in the report. It contains details on the market dynamics and trends expected to drive the global market over the forecast period. It provides information on key aspects, including technological advancements and new product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments. The global market research report also provides a detailed competitive landscape, including market share and profiles of major operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 22.61% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Technology, Indication, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Technology |

|

| By Indication |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.20 billion in 2025 and is projected to reach USD 14.22 billion by 2034.

In 2025, North Americas market value stood at USD 0.96 billion.

The market is expected to grow at a CAGR of 22.61% over the forecast period of 2026-2034.

The software & services segment led the market in 2025.

The increasing prevalence of cardiovascular diseases is a key factor driving market growth.

GE HealthCare Technologies Inc., Koninklijke Philips N.V., Siemens Healthineers AG, and Canon Medical Systems Corporation are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us