AI in Life Science Analytics Market Size, Share & Industry Analysis, By Component (Software and Services), By Technology (Machine Learning, Natural Language Processing, and Others), By Application (Discovery & Translational Analytics, Clinical Development Analytics, Pharmacovigilance & Safety Analytics, RWE/RWD Analytics, Manufacturing & Quality Analytics, and Others), By Deployment (Cloud-based, On-Premise, and Hybrid), By End User (Pharmaceutical & Biotechnology Companies, CROs/CDMOs, Medical Device Companies, and Others), and Regional Forecast, 2026-2034

AI in Life Science Analytics Market Size and Future Outlook

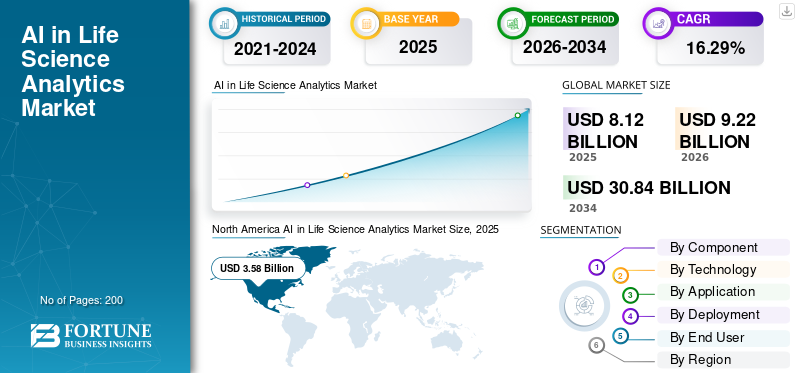

The global AI in life science analytics market size was valued at USD 8.12 billion in 2025. The market is projected to grow from USD 9.22 billion in 2026 to USD 30.84 billion by 2034, exhibiting a CAGR of 16.29% during the forecast period. North America dominated the AI in life science analytics market with a market share of 44.08% in 2025.

AI in life science analytics involves utilizing machine learning (ML), deep learning, natural language processing (NLP), and increasingly, generative/agentic AI to convert life-science data into insights that enhance R&D decisions, clinical development, manufacturing, and commercial outcomes for pharma, biotech, medtech, CROs, and occasionally payers/providers. Key factors driving this market growth include rising R&D and clinical trial complexity, expanding data volumes, and greater demand for real-world evidence (RWE).

Major companies such as IQVIA Inc., Oracle, and SAS Institute Inc. are focusing on technological improvements in their product lines to sustain their top market positions.

Download Free sample to learn more about this report.

AI in Life Science Analytics Market Key Takeaways

- 2025 Market Size: USD 8.12 billion

- 2026 Market Size: USD 9.22 billion

- 2034 Forecast Market Size: USD 30.84 billion

- CAGR: 16.29% from 2026–2034

- North America dominated the AI in life science analytics market with a 44.08% share in 2025.

- Software segment led the market due to scalable analytics platform adoption.

- Machine learning segment dominated with a 56.8% share in 2026.

North America

North America led the market with USD 3.58 billion revenue in 2025, driven by AI adoption in life sciences.

Europe

Europe is the second-largest market, supported by compliant analytics and digital healthcare initiatives.

Asia Pacific

Asia Pacific reached USD 1.89 billion in 2026, driven by pharma expansion and clinical trial growth.

U.S.

The U.S. market is estimated at USD 3.71 billion in 2026, supported by enterprise AI adoption.

Japan

The Japan market is estimated at USD 0.42 billion in 2026, driven by pharma innovation and analytics adoption.

Read More

AI in LIFE SCIENCE ANALYTICS MARKET TRENDS

Shift toward Cloud and Enterprise Data Platforms Pose as Notable Market Trend

The transition to cloud and enterprise data platforms is a prominent market trend in AI for life science analytics. This is owing to the reason that life-science AI requires scalable computing, quicker data access, and consistent model deployment across various functions. As pharma/biotech transition from fragmented on-premises systems, cloud-native data platforms minimize data silos and redundant pipelines, accelerating cohort development, trial operations analysis, PV signal assessment, and manufacturing quality insights. Standardized cloud data layers enhance governance and auditability, facilitating the deployment of AI/GenAI in regulated environments. This directs expenditure toward software-driven subscriptions and facilitates quicker deployment of new analytics modules in various regions. The acceleration during the COVID period intensified this, as organizations needed to rapidly update data access and expand their digital operations. In general, cloud data infrastructures are emerging as the standard framework for enterprise AI analytics initiatives in life sciences. Moreover, these above mentioned factors are further supporting the overall global AI in life science analytics market growth.

- For example, in December 2024, AWS announced the next generation of Amazon SageMaker. The release notes that Roche plans to use SageMaker Lakehouse to unify data from Amazon Redshift and Amazon S3 data lakes to reduce silos and support analytics/AI use cases.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising R&D and Clinical Trial Complexity Propels Market Growth

Rising R&D and clinical trial complexity is a key market driver for AI in life science analytics as protocols are becoming harder to execute with more endpoints, tighter eligibility, more sites/countries, and heavier operational oversight. Thus, sponsors and CROs need AI to keep timelines and budgets under control. As complexity increases, teams rely on AI analytics to improve trial feasibility, site/country selection, enrollment forecasting, and risk-based monitoring, helping detect underperforming sites early and correct courses faster. This directly raises demand for AI-enabled analytics platforms that can combine operational trial data with external signals and continuously update forecasts. It also pushes companies to standardize analytics stacks across portfolios so they can replicate best practices across studies. Overall, complexity turns AI from an innovation project into an operational necessity for predictable delivery and faster decision-making. Thus, the overall market growth is driven by all these factors cumulatively mentioned above.

- For instance, in June 2025, IQVIA announced it launched new AI agents for life sciences and healthcare, positioned to help the industry enhance, streamline, and focus clinical trials using AI applications trained on healthcare-specific information.

MARKET RESTRAINT

Regulatory, Privacy, and Governance Constraints to Hamper Market Growth

Regulatory, privacy, and governance constraints restrain the market as life-science data is highly-sensitive (trial, patient-level, and safety) and the output is often used to support regulated decisions. As a result, companies must implement strict controls around data provenance, consent/permissions, audit trails, model transparency, and ongoing monitoring for drift, which increases cost and lengthens deployment timelines. Cross-border data rules and data residency expectations can further limit the ability to centralize datasets for model training, forcing fragmented architectures that slow scaling. For GenAI/NLP use cases, governance is even harder as organizations must manage prompt/context controls, hallucination risk, and traceability for generated outputs. These requirements typically push firms from quick pilots to longer validation-heavy programs, delaying ROI and slowing broader rollouts, especially in clinical and safety workflows. Further, this results in limiting the growth in the market to a certain extent.

- For instance, in January 2025, the U.S. FDA published a Federal Register notice announcing a draft guidance titled “Considerations for the Use of Artificial Intelligence (AI) to Support Regulatory Decision-Making for Drug and Biological Products”, which emphasizes expectations around the AI system’s context of use, data quality, transparency, and risk management—adding compliance workload that can slow adoption of AI-generated evidence in regulated submissions.

MARKET OPPORTUNITIES

Manufacturing & Quality Digitalization to Present Significant Market Growth Opportunities

The digitization of manufacturing and quality presents a significant market opportunity in AI for life science analytics, as biopharma facilities face the challenge of enhancing right-first-time production, minimizing deviations/CAPA cycle time, and boosting throughput without a corresponding increase in capital expenditure. By digitizing batch records, equipment data, and quality events, companies establish a more robust data foundation that enables AI to advance from mere reporting to predictive quality, process enhancement, and earlier identification of drift, which may lead to investigations or batch loss. This creates ongoing demand for AI analytics platforms that integrate MES/QMS/LIMS data, standardize governance, and implement validated models across multi-site networks. The potential is particularly significant since manufacturing programs generally expand across facilities after ROI has been demonstrated, leading to consistent software deployments along with integration and validation services. However, all these above factors would be responsible to drive the growth in the market in the forthcoming years.

- For instance, in November 2025, Teva launched “Rise,” a global open innovation platform explicitly aimed at accelerating AI, Industry 4.0 and smart manufacturing solutions including manufacturing and supply chain challenges.

MARKET CHALLENGES

Lack of Skilled Professionals Pose a Prominent Challenge to Market Growth

The lack of skilled personnel poses a significant market challenge for AI in life science analytics, as expanding beyond pilot projects requires individuals who can integrate domain workflows with AI/ML/GenAI engineering, along with skills in validation and governance. Numerous organizations can purchase software, yet they face difficulties in operationalizing it due to deficiencies in data engineering, model risk management, and expertise for “GxP-ready” implementation. This delays the incorporation into SOPs, raises reliance on costly outside services, and leads to bottlenecks in model oversight, record-keeping, and audit preparedness. The disparity is greater when teams need to manage unstructured data (PV narratives, protocols, batch records) as NLP/GenAI necessitates stringent controls. All the factors cumulatively affect the market growth.

- For instance, according to the BioPharm International survey-based report published in October 2025, nearly half of respondents said their organization’s workforce was unprepared for digital transformation (skills/training/mindset).

Segmentation Analysis

By Component

Advancements in Software Deployments to Boost Segment’s Growth

Based on the component, the market is bifurcated into services and software.

The software segment captured the largest global market share. This is as most buyers prefer scalable, reusable platforms that can be rolled out across multiple functions such as clinical, RWE, safety, manufacturing without rebuilding the same analytics logic every time. Additionally, the growth of the segment is also supported by the launch of new products in the market by the operating players.

- For instance, in October 2025, Oracle launched Oracle Analytics Intelligence for Life Sciences, positioned as a pre-built, continuously updated analytics platform leveraging real-world data sources to accelerate insight generation.

The services segment is anticipated to rise with a CAGR of 14.16% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

High Usage in Various Applications to Boost Segmental Growth

In terms of technology, the market is divided into machine learning, natural language processing, and others.

The machine learning segment dominated the global market in 2025. This is as most early, high-value use cases run on structured and semi-structured data, clinical operations metrics, RWE/claims tables, lab results, manufacturing sensor/process data, where ML delivers measurable gains in prediction and optimization. Buyers also trusted ML sooner as it supports quantifiable performance metrics that fit validation and governance expectations better than early-stage GenAI. In addition, many enterprise analytics stacks already had ML toolchains, so scaling ML across trial feasibility, enrollment forecasting, signal detection support, and predictive quality was relatively straightforward. Furthermore, the segment is set to hold 56.8% share in 2026.

- For instance, in September 2025, Eli Lilly announced the launch of Lilly TuneLab, an AI/ML platform that provides biotech companies access to drug discovery models trained on Lilly’s research data.

The natural language processing segment is anticipated to rise with a CAGR of 20.72% over the forecast period.

By Application

High Usage in Clinical Development Analytics to Boost Segmental Growth

On the basis of application, the market is divided into discovery & translational analytics, clinical development analytics, pharmacovigilance & safety analytics, RWE/RWD analytics, manufacturing & quality analytics, and others.

The clinical development analytics segment captured the highest share of the global market in 2025. This is due to the fact that clinical trials are the single biggest cost and timeline driver in the life-science value chain, so sponsors prioritize analytics that directly improves speed, quality, and predictability of trial execution. Furthermore, the segment is set to hold 26.8% share in 2026.

- For instance, in November 2025, SAS announced the general availability of SAS Clinical Acceleration, positioned to modernize and streamline clinical trial data management, analysis, and regulatory submission for life sciences.

The RWE/RWD analytics segment is anticipated to rise with a CAGR of 18.45% over the forecast period.

By Deployment

Rising Shift toward Cloud-based Solutions Supported Segmental Dominance

Based on the deployment, the market is divided into cloud-based, on-premise, and hybrid.

The cloud-based segment is anticipated to capture the largest global AI in life science analytics market share in 2025. Cloud based deployment shortens time-to-value by enabling faster environment provisioning, frequent model updates, and easier integration across data sources through standardized connectors and AP. Moreover, vendors increasingly ship new AI features cloud-first, so customers adopt cloud to access the latest capabilities and reduce maintenance burden. Furthermore, the segment is set to hold 47.1% share in 2026.

- For instance, in May 2025, Salesforce announced a Strategic Life Sciences Alliance to accelerate customer migration to Life Sciences Cloud, positioning it as a HIPAA-ready, pre-validated, GxP-compliant cloud platform and linking upgrades to deploying Agentforce (agentic AI).

The hybrid segment is anticipated to rise with a CAGR of 13.10% over the forecast period.

By End User

High Demand from Pharmaceutical & Biotechnology Companies to Support Segment’s Leading Position

On the basis of end user, the market is further classified into pharmaceutical & biotechnology companies, CROs/CDMOs, medical device companies, and others.

In 2025, the pharmaceutical & biotechnology companies segment held the leading position in the market globally. Such growth is due to the fact that they are the primary budget owners for the most data- and decision-intensive functions, R&D, clinical development, PV/safety, RWE, and GMP manufacturing, where AI can directly reduce cycle time and failure risk. They also control the largest proprietary datasets (trial data, molecule/assay data, safety cases, and quality events), so they invest in enterprise platforms to standardize data governance, model monitoring, and audit readiness across portfolios. Moreover, in 2026 the segment is anticipated to be holding a share of 60.3% .

- For instance, in June 2025, Pfizer expanded its research collaboration with XtalPi to build an enhanced AI-driven molecular modeling platform aimed at improving predictive tools and throughput for small-molecule drug discovery.

In addition, CROs/CDMOs are projected to grow 18.01% growth rate during the forecast period.

AI in Life Science Analytics Market Regional Outlook

By region, the market is segmented into Asia Pacific, North America, Europe, Latin America, and the Middle East & Africa.

North America

North America AI in Life Science Analytics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America market size was USD 3.16 billion in 2024 and dominated the global market. The region also maintained its dominance in 2025, with USD 3.58 billion. The growth in North America is driven by early adoption of enterprise AI platforms and strong demand for productivity gains across clinical development, RWE, and safety operations.

U.S. AI in Life Science Analytics Market

The U.S. market dominated the North American market and can be analytically approximated at around USD 3.71 billion in 2026, accounting for roughly 40.3% of the global market.

Europe

Europe market size is anticipated to grow at 15.97% CAGR during the forecast period. The region is anticipated to capture the second leading position among all regions. Europe’s growth is supported by rising focus on compliant, governed analytics that can operate across multi-country environments and varied data systems.

U.K. AI in Life Science Analytics Market

The U.K. market size in 2026 is estimated at around USD 0.49 billion, representing roughly 5.3% of the global revenues.

Germany AI in Life Science Analytics Market

Germany market size is projected to reach approximately USD 0.56 billion in 2026, equivalent to around 6.1% of the global sales.

Asia Pacific

Asia Pacific market size is projected to be valued at USD 1.89 billion in 2026 and secure the position of the third largest region in the global life sciences industry. Further, the region is growing rapidly due to expanding pharma/biotech pipelines, increasing clinical trial activity, and large-scale manufacturing footprint expansion, which together create strong demand for AI analytics across clinical, quality, and supply operations.

Japan AI in Life Science Analytics Market

The Japan market size in 2026 is estimated at around USD 0.42 billion, accounting for roughly 4.5% of the global revenues.

China AI in Life Science Analytics Market

China’s market is projected to reach revenues of around USD 0.48 million in 2026, representing roughly 5.2% of global sales.

India AI in Life Science Analytics Market

The Indian market value in 2026 is estimated at around USD 0.36 billion, accounting for roughly 4.0% of global revenues.

Latin America and Middle East & Africa

The Middle East & Africa and Latin America regions would grow at a comparatively slower growth over the forecast period. The Latin America market size is set to reach a valuation of USD 0.50 billion in 2026. Prominent factors such as gradual modernization of clinical trial operations and increasing adoption of cloud to reduce infrastructure barriers and speed deployment are expected to drive the market growth.

Among the Middle East & Africa region, the GCC market in 2026 is estimated at around USD 0.16 billion, accounting for roughly 1.7% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Enterprise Analytics Platforms, GenAI Enablement, and Evidence Automation to Strengthen Market Share

The global AI in life science analytics sector is semi-consolidated. Major companies including IQVIA, Veeva, Oracle, SAS, Medidata (Dassault Systèmes), and others represent a substantial portion of enterprise implementations, while also competing with specialized providers in PV, RWD integration, and trial analytics. These firms are progressively focusing on GenAI/NLP-driven automation, scalable cloud-based analytics structures, and ready-made modules for RWE cohorting, trial performance tracking, and predictive quality. To enhance market share and enlarge footprint, these companies are bolstering data governance, validation preparedness, and model oversight, while forming alliances with RWD suppliers, CROs/CDMOs, and hyperscalers to accelerate implementation and expand use-case coverage.

Other significant players enhancing the competitive environment consist of Microsoft (Azure), AWS, Google Cloud, SAP, Salesforce (Life Sciences Cloud ecosystem), Saama, and others. These entities are promoting workflow-specific accelerators and pre-packaged analytics applications.

- For instance, in April 2025, Veeva Systems announced “Veeva AI,” a major initiative to add AI to the Veeva Vault Platform and Veeva applications using AI Agents and AI Shortcuts to automate critical industry-specific functions from clinical to commercial.

LIST OF KEY AI in LIFE SCIENCE ANALYTICS COMPANIES PROFILED

- IQVIA Inc. (U.S.)

- Oracle (U.S.)

- SAS Institute Inc. (U.S.)

- Veeva Systems Inc. (U.S.)

- Inovalon (U.S.)

- Snowflake Inc. (U.S.)

- Databricks (U.S.)

- Axtria (U.S.)

- Sorcero, Inc. (U.S.)

- Palantir Technologies Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: ZS announced it will bring ZAIDYN intelligence into Salesforce Agentforce Life Sciences (availability starting January 2026) to improve life-sciences sales/marketing performance via embedded intelligence.

- October 2025: Certara launched Certara IQ, an AI-powered Quantitative Systems Pharmacology (QSP) solution to accelerate modeling and decision-making in drug development.

- September 2025: Inovalon made its real-world data (RWD) and analytics capabilities available on Snowflake’s AI Data Cloud for Healthcare & Life Sciences, supporting faster research and evidence generation.

- June 2025: Komodo Health was recognized by Databricks as 2025 Healthcare & Life Sciences Partner of the Year, reflecting deeper go-to-market/solution alignment around RWD analytics on Databricks.

- April 2025: Axtria announced the next generation of Axtria InsightsMAx.ai, positioning it as an agentic AI platform with ready-to-deploy agents/apps/APIs to scale AI adoption in life sciences.

REPORT COVERAGE

The global AI in life science analytics market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements in products, the regulatory environment, and new product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments in the market. The global market forecast report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 16.29% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Technology, Application, Deployment, End User, and Region |

| By Component |

|

| By Technology |

|

| By Application |

|

| By Deployment |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 8.12 billion in 2025 and is projected to reach USD 30.84 billion by 2034.

In 2025, the market value stood at USD 3.58 billion.

The market is expected to exhibit a CAGR of 16.29% during the forecast period.

By component, the software segment is expected to lead the market.

The rising R&D and clinical trial complexity, expanding data volumes, and greater demand for real-world evidence (RWE), are primarily driving market expansion.

IQVIA Inc., Oracle, and SAS Institute Inc. are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us