Snowmobile Market Size, Share & Industry Analysis, By Product Type (Touring, Trail, Mountain, Crossover, Performance, and Utility), By Engine Type (Two Stroke Engine and Four Stroke Engine), By Seating Capacity (Less than 400CC, 400-600CC, 600-800CC, and More than 800CC), By Seating (Single Seater, Two Seater, Three Seater, and Others), and Regional Forecast, 2026-2034

Snowmobile Market Future Outlook

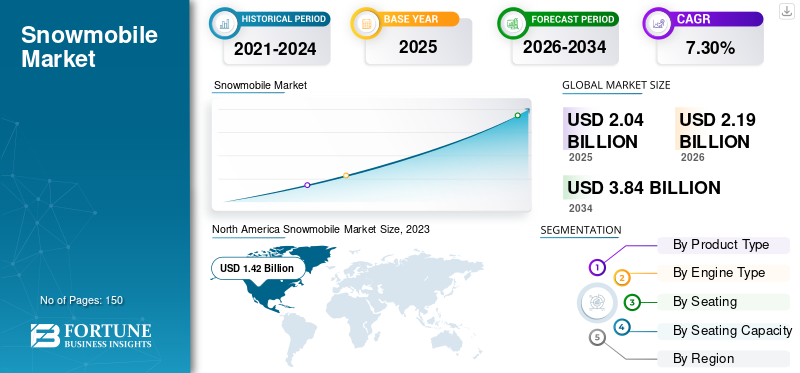

The global snowmobile market size was valued at USD 2.04 billion in 2025 and is projected to grow from USD 2.19 billion in 2026 to USD 3.84 billion by 2034, exhibiting a CAGR of 7.30% during the forecast period. North America dominated the snowmobile market with a share of 78.73% in 2025. The industry growth is driven by recreational demand, winter tourism expansion, utility applications in remote regions, product innovation, and climate variability dynamics

A snowmobile, a skimobile, Ski-Doo, or snow scooter, is a motorized recreational vehicle designed for winter sports activities or recreation on snow. This vehicle is designed to be operated on snow and does not require a trail or road, but most are driven on open terrain or trails.

Snowmobiles are popular in regions with heavy snowfall where winter tourism is prevalent. Tourists often seek out snowmobile rentals and tours for recreational activities, driving the demand for snowmobiles in these areas. The growing popularity of snowmobiling in the U.S., Canada, and Northern Europe is owing to the rise in winter sports activities. As per the International Snowmobile Manufacturers Association (ISMA) report, there were 1.2 million registered units in the U.S. and over 601,000 in Canada in 2020-21. The growing number of these vehicle registration indicates the growing popularity of snowmobiling as a healthy winter sport activity. Snowmobiling is a popular outdoor recreational activity for individuals and families. As people seek ways to enjoy outdoor activities during the winter months, the demand for snowmobiles for personal use increases.

Economic factors, such as rising disposable income levels, can impact consumer spending on recreational vehicles like snowmobiles. Consumers with more disposable income may be more likely to invest in high-ticket items such as snowmobiles. Weather patterns and snowfall fluctuations can affect the demand for snowmobiles. Regions experiencing consistent snowfall are likely to have a steady demand for snowmobiles, while areas with unpredictable snow conditions may see fluctuating demand. Effective marketing campaigns and promotions by manufacturers and dealers can stimulate interest and drive sales in the snowmobile market. Special events, demos, and sponsored races can attract potential buyers and enthusiasts.

The global snowmobile market reflects a specialized yet resilient recreational and utility vehicle segment influenced by climatic conditions, discretionary income cycles, and winter tourism infrastructure investment. While seasonal volatility affects short-term sales patterns, long-term demand remains structurally supported by lifestyle participation, backcountry exploration, and remote mobility needs.

Current snowmobile market size is estimated in the mid-single-digit billion-dollar range, with North America accounting for the majority of global market share. The United States and Canada collectively represent the core demand base, driven by established trail systems, high ownership penetration, and strong dealership networks. Europe follows with moderate contribution, particularly in Nordic countries and alpine regions. Snowmobile market growth is projected to remain steady through 2032, supported by product innovation in lightweight chassis design, fuel-efficient four-stroke engines, and enhanced suspension systems. Electrification remains in early-stage development, primarily targeting niche recreational and environmentally sensitive zones.

Market trends indicate increasing consumer preference for performance-oriented models and crossover platforms capable of multi-terrain use. At the same time, utility snowmobiles maintain consistent demand in forestry, defense, and rural logistics applications. Rental and tourism operators are expanding fleet investments in response to experiential travel growth. However, climate variability introduces demand uncertainty. Shortened snow seasons and inconsistent snowfall patterns influence purchase timing and aftermarket service cycles. Manufacturers are responding through geographic diversification and flexible production planning.

Download Free sample to learn more about this report.

Snowmobile Market Key Takeaways

- 2025 Market Size: USD 2.04 Billion

- 2026 Market Size: USD 2.19 Billion

- 2034 Forecast Market Size: USD 3.84 Billion

- CAGR: 7.30% from 2026–2034

- North America dominated the snowmobile market with a 78.73% share in 2025.

- The Trail segment is projected to dominate the market with a 27.00% share in 2026.

- The Two-Stroke Engine segment is expected to lead the market with a 64.07% share in 2026.

Asia Pacific

Asia Pacific recorded USD 0.01 billion in 2025 and is projected to maintain steady growth in 2026.

North America

North America reached USD 1.61 billion in 2025 and is projected to grow to USD 1.72 billion in 2026.

Europe

Europe generated USD 0.38 billion in 2025 and is expected to reach USD 0.41 billion in 2026.

U.S.

The market is projected to reach USD 0.89 billion by 2026, driven by trail systems and winter tourism.

Japan

Winter tourism and recreational snow sports continue to support steady market demand.

Read More

Snowmobile Market Trends

Shift toward Electrification is Expected to Set a Positive Trend in the Snowmobile Market

Electric snowmobile technology can be a game changer in the market in the coming years. OEMs in this market are introducing electric snow machines with enhanced performance, maneuverability, and reliability. Electric motors provide instant torque, delivering quick acceleration and responsive handling on snow-covered terrain. Electric snowmobiles offer smooth and quiet operation, enhancing the overall riding experience for enthusiasts. There has been robust growth in the electric mobility market. The gradual shift from IC engine vehicles to electric vehicles will create growth opportunities for OEMs in the power sports industry. Electric snowmobiles produce zero emissions during operation, addressing air and noise pollution concerns in snow-covered environments. As environmental awareness grows, there is increasing demand for eco-friendly transportation options, including electric snowmobiles. Advances in battery technology have improved the performance and range of electric snowmobiles. Modern lithium-ion batteries offer longer run times and faster charging capabilities, making electric snowmobiles more practical and appealing to consumers.

A few manufacturers have entered the electric vehicle market by launching an electric variant of the snow vehicles to support the demand for zero-emission vehicles and widen their market share. For instance, in November 2022, Taiga Motors announced the launch of its new electric snow bike, the Nomad, with innovative features. Similarly, in February 2023, Ski-Doo and Lynx announced to launch their first electric lineup in 2024. The lineup will include Ski-Doo Grand Touring Electric and European-only Lynx Adventure Electric. Electric snowmobiles offer new opportunities for rental businesses and tour operators catering to eco-conscious travelers. Electric models may appeal to environmentally conscious tourists seeking sustainable and immersive outdoor experiences.

Product diversification remains a defining snowmobile market trend. Manufacturers increasingly segment offerings into touring, mountain, performance, and crossover categories to capture distinct rider profiles. Performance snowmobiles emphasize lightweight materials, enhanced horsepower, and advanced suspension geometry. Touring models prioritize comfort, storage capacity, and extended range. Another notable trend involves incremental electrification development. While internal combustion engines continue to dominate, early electric prototypes target eco-sensitive environments and regulated parks. Battery density constraints currently limit widespread adoption, yet research investment signals long-term strategic intent.

Digital integration is expanding gradually. Modern snowmobiles incorporate advanced instrumentation clusters, GPS navigation, and smartphone connectivity. These features enhance user experience and support safety in remote terrain. Dealers also utilize telematics data to support predictive maintenance services. Snowmobile market share remains concentrated among a limited number of global manufacturers, reflecting high capital intensity and specialized production processes. However, niche custom builders and performance modification firms maintain presence in enthusiast segments.

Download Free sample to learn more about this report.

Snowmobile Market Growth Factors

Growing Popularity of Winter Sports Activities is Accelerating the Snowmobile Market Growth

The growing popularity of outdoor recreational and winter sports activities surges the demand for snowmobiles. Growing expenditure on outdoor recreational activities, leisure, and rising sports competitions during winter surges the demand for these vehicles. According to the U.S. Bureau of Economic Analysis (BEA), the outdoor recreation economy accounted for 1.9% of the country's nominal Gross Domestic Product (GDP) in 2021.

There is growing usage of this vehicle by search & rescue teams as their primary vehicle in high altitudes during winters. This vehicle can also be used as an ambulance sled and puller in snow belts. This vehicle also allows rapid search for clues, allowing for rapid deployment of medical care in case of emergencies.

Recreational participation growth is a primary driver of snowmobile market growth. Winter tourism expansion across North America and select European regions supports rental fleet investments and new customer exposure. Organized trail systems and government-supported winter recreation programs enhance accessibility. Rising disposable income in cold-climate regions supports discretionary vehicle purchases. Snowmobiles are often positioned as lifestyle investments, particularly among rural households and outdoor enthusiasts. Financing availability through dealership networks further facilitates ownership expansion.

Utility applications represent another growth factor. Snowmobiles remain essential in remote logistics, forestry, emergency response, and defense operations. Their capability to operate in deep snow terrain provides practical mobility advantages where conventional vehicles cannot function effectively. Product innovation contributes materially to snowmobile market size expansion. Improvements in engine efficiency, reduced emissions, and advanced suspension systems enhance reliability and rider comfort. Lightweight chassis construction improves maneuverability and fuel economy.

Restraining Factors

High Maintenance Cost May Restraint the Market Growth

The high maintenance cost is a key factor restraining the market growth. As per the ISMA report, an average snowmobile owner spends approximately USD 3,000– USD 4,000 yearly on travel gear and related services. The annual ownership costs of this vehicle range between USD 1,500 to USD 5,500 for an average ride of 1,500 miles a year. Used sleds are cheaper to maintain but less reliable. Hence, they need more maintenance. Ownership costs of new sleds cost around USD 2,500-USD 5,500 a year, depending on the model, feature, and year.

Climate variability represents the most significant structural restraint within the snowmobile industry. Reduced snowfall frequency and shorter winter seasons in certain regions directly influence purchase cycles. Consumers may delay investment decisions during low-snow years, creating revenue volatility.

High acquisition cost also constrains broader penetration. Snowmobiles are discretionary purchases, often competing with other recreational expenditures. Economic downturns typically affect demand sensitivity within this segment. Environmental regulations impose additional pressure. Emission standards for internal combustion engines are tightening across multiple jurisdictions. Compliance requires continuous investment in cleaner engine technologies and exhaust after-treatment systems.

Fuel price volatility may influence operating cost perception. Although snowmobiles are not high-mileage vehicles, higher fuel costs can impact recreational usage frequency. Safety concerns represent another restraint. Snowmobile accidents receive regulatory scrutiny, leading to helmet mandates, speed restrictions, and designated trail enforcement. While these measures improve safety outcomes, they may limit spontaneous use in certain areas.

Market Opportunities

Electrification presents a long-term strategic opportunity within the snowmobile market. While current electric models face range limitations, technological advancements in battery density and cold-weather performance could enable broader adoption. Eco-tourism operators and regulated park environments represent early deployment niches. Expansion into emerging winter tourism destinations offers incremental growth potential. Regions in Eastern Europe and Central Asia are investing in ski resorts and recreational infrastructure. Snowmobile rentals form a complementary service offering within these ecosystems.

Fleet modernization among tourism operators presents recurring revenue opportunities. Institutional buyers prioritize durability, service efficiency, and fuel economy. Manufacturers offering extended warranty programs and service contracts strengthen competitive advantage. Sustainable manufacturing initiatives also create differentiation potential. Consumers increasingly value environmental stewardship. Adoption of recyclable materials and lower-emission engines supports brand positioning.

Digital engagement strategies present another opportunity. Telematics integration and connected services can enhance safety tracking and maintenance planning. These features appeal to both recreational users and fleet operators. Diversification into apparel, accessories, and branded equipment supports margin expansion. These segments provide counter-seasonal revenue stabilization.

Snowmobile Market Segmentation Analysis

The snowmobile market demonstrates structured segmentation shaped by rider intent, engine configuration, displacement capacity, and seating configuration. Institutional buyers and dealers evaluate these segments based on durability, terrain compatibility, resale value, and aftermarket support. Understanding segmentation is essential for assessing snowmobile market share distribution and long-term snowmobile market growth potential.

By Product Type Analysis

Trail Segment is Anticipated to Lead the Market Owing to its Lightweight and Reliability

The market is divided into touring, trail, mountain, crossover, performance, and utility based on product type.

Trail Snowmobiles

The trail segment is projected to dominate the market with a share of 27.00% in 2026. Trail types are lightweight, agile, reliable, comfortable, and economical. These snowmobiles are popular among entry-level riders owing to their easy operation and are suitable for cruising around on groomed trails for recreational activities. Moreover, the growing popularity of trail-specific ski-doo among young-age group people will drive the segment growth.

Trail snowmobiles represent a core volume segment within the snowmobile industry. These models are optimized for groomed trails, balancing performance, fuel efficiency, and affordability. Lightweight chassis and responsive steering improve maneuverability. Trail models account for a substantial portion of North American snowmobile market share. Entry-level riders frequently select this category, supporting steady replacement demand cycles.

Touring Snowmobiles

The touring segment is anticipated to register the highest CAGR over the forecast period. The positive market outlook can be attributed to its higher reliability for long-distance travel. Touring type is meant to be ridden for a long time, usually more comfortable than other types of sleds, and has space to carry more cargo. Due to their enhanced stability, safety, and heavier sledge, they are ideal for long, comfortable rides.

Touring snowmobiles are engineered for long-distance comfort and stability. They typically feature extended track lengths, advanced suspension systems, heated seating, and integrated storage compartments. Demand originates from recreational riders prioritizing comfort over aggressive maneuverability. Touring models contribute meaningfully to snowmobile market size in regions with established trail networks. Buyers in this segment often exhibit higher purchasing power and willingness to invest in premium accessories. Rental operators in resort areas also favor touring models due to ease of operation and passenger capacity.

Mountain Snowmobiles

Mountain snowmobiles are designed for deep snow and steep terrain conditions. They incorporate longer tracks, high-horsepower engines, and aggressive suspension geometry. Demand is concentrated in alpine regions and western North America. This segment reflects strong performance orientation. Enthusiast communities influence product development, driving innovation in weight reduction and throttle response.

Crossover Snowmobiles

Crossover models combine trail and mountain capabilities. They appeal to riders seeking versatility across variable terrain. Adjustable suspension systems and adaptable track configurations characterize this segment. Crossover snowmobiles demonstrate rising snowmobile market growth due to their flexible application range. Dealers report strong demand among mid-experience riders upgrading from trail models.

Performance Snowmobiles

Performance snowmobiles emphasize speed, acceleration, and technical riding capability. These models typically feature high-displacement engines and sport-oriented ergonomics. While smaller in volume, performance models command higher price points. They contribute disproportionately to revenue and margin expansion within the snowmobile market.

Utility Snowmobiles

Utility snowmobiles are built for work-related applications, including forestry, patrol, and remote logistics. Reinforced chassis, towing capability, and cargo racks define this category. Utility demand remains stable across economic cycles. Government agencies and institutional operators prioritize durability and lifecycle cost efficiency.

By Engine Type Analysis

Two Stroke Engine is Anticipated to Register High CAGR over the Forecast Period Owing to its Lower Maintenance Cost

The market is categorized into two stroke engine and four stroke engine based on engine type.

Two-Stroke Engine

The two stroke engine segment is expected to lead the market, contributing 64.07% globally in 2026. Two stroke engines are lighter and generate more power than four stroke engines. Moreover, they are cheaper to build and have lower maintenance costs.

Owing to their lower maintenance cost and higher power-to-weight ratio, manufacturers are more focused on building reliable two stroke engine-powered snow vehicles. For instance, in January 2020, Ski-Doo launched a two stroke turbo snowmobile, the Summit 850 E-TEC Turbo, the world’s first factory-built two stroke turbo engine. The model is lighter and designed to provide consistent performance as altitude increases.

Two-stroke engines remain valued for lightweight construction and rapid throttle response. Performance and mountain segments historically relied on this configuration. However, tightening emission regulations are gradually reducing two-stroke engine penetration. Manufacturers invest in direct-injection systems to improve efficiency and compliance. Two-stroke models still contribute to snowmobile market share in enthusiast categories, particularly where weight reduction remains critical.

Four-Stroke Engine

The four stroke engine segment held a significant market share in 2026. Four stroke engines are quieter and more complex and require more maintenance as compared to two stroke engines. Four stroke engines are gaining popularity in recent years as they are more fuel-efficient and offer near-complete combustion, resulting in better performance. They are ideal for long-distance trail riding owing to liquid-cooled engines and better gas mileage. Moreover, four stroke engines help ensure better fuel, higher torque, and lower emission levels.

Four-stroke engines dominate current snowmobile market growth. They offer improved fuel efficiency, lower emissions, and extended durability. Regulatory compliance increasingly favors four-stroke platforms. Touring and utility segments predominantly adopt four-stroke engines due to reliability and lower operating noise. Institutional buyers frequently prioritize these attributes. Engine segmentation highlights the industry’s gradual transition toward cleaner combustion technologies while maintaining performance expectations.

By Seating Capacity Analysis

600-800CC Segment to Lead the Market due to its Higher Performance and Enhanced Maneuverability

The market is categorized into less than 400CC, 400-600CC, 600-800CC, and more than 800CC based on seating capacity.

600–800CC

The 600-800CC segment will account for 29.29% market share in 2026. When navigating tight terrain, these engine capacities provide higher torque, enhanced performance, and extra maneuverability. These vehicles with higher engine capacity can also be used in winter rescue work, repairing power and telephone lines, checking forest land, and providing winter transportation for professional conservationists.

Snowmobiles in the 600–800CC range represent a significant volume segment. They deliver enhanced performance without entering premium price tiers. Both touring and crossover categories frequently operate within this displacement band. Dealers report consistent replacement demand within this range.

More than 800CC

High-displacement snowmobiles above 800CC serve performance and mountain riders. These models deliver high horsepower output and aggressive acceleration. Although smaller in unit volume, this category contributes strongly to revenue generation. Enthusiast loyalty supports stable snowmobile market growth in this segment.

400–600CC

Mid-range displacement models balance power and efficiency. They are commonly selected for trail and crossover applications. Buyers value fuel economy and controllable acceleration. This displacement category maintains steady snowmobile market share due to broad rider suitability.

Less than 400CC

The less than 400CC segment is anticipated to register a significant CAGR over the forecast period. Snowmobiles with engine capacity of less than 400CC are lightweight, affordable, and easy to handle and are mostly used in touring and trailing. This range of engine capacity is suitable for kids owing to their easy handling and operation.

Snowmobiles under 400 cubic centimeters (CC) primarily target entry-level riders and youth segments. Lower displacement engines offer manageable power output and affordability. This segment supports long-term customer pipeline development but contributes modestly to total snowmobile market size.

By Seating Analysis

To know how our report can help streamline your business, Speak to Analyst

Two Seater Held a Considerable Market Share Owing to its Higher Application in Touring

The market is categorized into single seater, two seater, three seater, and others based on seating.

Two Seater

The two seater segment is expected to account for 50.80% of the market in 2026. Two seater snowmobiles are designed to accommodate two passengers. Two seaters are primarily used for touring, designed to provide comfort for the driver and passenger on longer tours on groomed trails.

Two-seater snowmobiles are common within touring and rental applications. They provide enhanced comfort and passenger capability. Resort operators prioritize these configurations for guided tours. Two-seater models contribute significantly to snowmobile market size in tourism-driven regions.

Single Seater

Single seater segment accounts for a substantial growth rate over the forecast period. Single seaters are generally used for racing activities. Rising winter sports activities across different regions, especially in North America and Europe, have positively impacted the expansion of the single seater segment share globally.

Single-seater snowmobiles dominate overall snowmobile market share. Most recreational riders prefer individual performance control and maneuverability. Lightweight design enhances handling precision. Performance, mountain, and trail segments predominantly feature single-seat configurations.

Three Seater

Three-seater configurations are less common but exist within specific touring categories. They support family-oriented recreational use. Although niche, this configuration supports incremental revenue opportunities.

REGIONAL INSIGHTS

North America Snowmobile Market Size, 2023 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The North America market generated USD 1.61 Billion in 2025, representing 78.73% of the global market landscape, and is expected to reach USD 1.72 Billion in 2026. It will dominate over the forecast period owing to increased expenditure on recreational activities and tourism-related businesses. As per the New Hampshire Snowmobile Association, snowmobiling generates over USD 30 billion worth of economic activity in North America. Over 70% of snowmobilers in North America are club or snow sports association members. Moreover, the region's presence of major manufacturers such as Polaris, Arctic Cat, Bombardier Recreational Products, and Yamaha contributes to the market growth. These manufacturers are emphasizing on diversifying their product portfolio to widen their customer base.

North America represents the largest snowmobile market globally, accounting for the majority of market share. Strong trail infrastructure, high ownership penetration, and established dealer networks support stable demand. Climate variability influences annual sales cycles, yet long-term participation remains resilient. Utility applications in rural Canada and northern United States reinforce baseline snowmobile market growth across core regions.

United States

The U.S. market is projected to reach USD 0.89 billion by 2026. The United States snowmobile market benefits from organized trail systems, state-level recreational funding, and tourism-driven rental activity. Replacement demand drives consistent market size stability. Western states support mountain segment growth, while Midwest regions anchor trail model volume. Dealers emphasize financing programs and service contracts to maintain snowmobile market share amid seasonal variability.

Europe

Europe contributed 18.66% to the global market in 2025, with a valuation of USD .38 Billion, and is projected to reach USD .41 Billion in 2026. The rising popularity of winter sports activities is leading to the expansion of the Europe market. As per the ISMA, around 25,880 new sledge were sold in Europe in 2021-2022. The growing number of snowmobiling clubs in Scandinavian countries, trail development, and sports show further propels the regional market growth. In some European countries, snowmobiling is a major part of their winter economic engine and provides thousands of employment opportunities.

Europe snowmobile market remains concentrated in Nordic countries and alpine regions. Regulatory oversight on emissions influences engine selection trends. Tourism activity supports fleet purchases, particularly in Scandinavia. Market growth remains moderate, shaped by environmental policies and snowfall consistency. Cross-border winter tourism contributes incremental snowmobile industry expansion. The Sweden market is projected to reach USD 0.14 billion by 2026, and the Russia market is projected to reach USD 0.11 billion by 2026.

Germany

Germany snowmobile market is relatively niche due to limited snowfall regions. Demand primarily arises from tourism operators and specialty outdoor enthusiasts. Import reliance shapes pricing dynamics. Regulatory compliance standards influence product availability. Growth remains modest but stable within controlled recreational zones and alpine destinations.

United Kingdom

The United Kingdom snowmobile market remains small due to limited snow conditions. Demand centers on export distribution, specialty recreation, and controlled winter tourism environments. Market size is constrained by geography, though high-income recreational buyers contribute premium model demand.

Asia-Pacific

Asia Pacific accounted for USD 0.01 Billion in 2025, representing 0.65% of the global market share, and is projected to reach USD 0.01 Billion in 2026. Asia-Pacific exhibits emerging snowmobile market potential in northern Japan and select high-altitude regions. Tourism-led demand shapes market size expansion. Broader adoption remains limited due to climate conditions. Institutional buyers in remote logistics represent niche opportunities. The steady market growth in Asia Pacific countries can be attributed to the growing popularity of winter tourism in countries, including India, Australia, China, and Japan. For instance, the number of people participating in seasonal winter sports in China has grown from 170 million in 2016 to 2017 to 254 million in 2020 to 2021.

Japan

Japan’s snowmobile market is concentrated in Hokkaido and mountainous regions. Winter tourism and recreational events support demand. Domestic consumer interest remains selective but consistent. Rental fleets contribute meaningfully to snowmobile market share in resort destinations.

China

China’s snowmobile market remains early-stage but shows incremental growth in northern provinces. Winter sports development initiatives encourage limited expansion. Institutional and tourism demand represent primary drivers. Market growth remains gradual.

Latin America

Latin America maintains a minimal snowmobile market presence, primarily in southern Chile and Argentina. Tourism-led demand anchors sales. Geographic constraints limit broader expansion. Market size remains modest.

Middle East & Africa

The Middle East and Africa snowmobile market is negligible due to climate limitations. Demand is restricted to niche tourism zones and import-based recreational use. Market growth prospects remain limited.

Rest of World

In 2025, the Rest of the World market stood at USD .04 Billion, representing 1.95% of global demand, and is projected to grow to USD .04 Billion in 2026.

Competitive Landscape

Key Players are Focusing on Mergers & Acquisitions and Partnerships to Gain a Competitive Edge in the Market

The companies are focusing on cost-reduction strategies, electrifying their sledge, strategic partnerships, and acquisitions to enhance their product offerings. They use modern technologies to improve their products and strengthen their footprint in the global market. For instance, In February 2022, BRP Inc. launched the fifth generation of the REV, designed for a more natural and controlled driving position, particularly for deep snow and trail riders.

The snowmobile industry exhibits high concentration, with a limited number of global manufacturers controlling the majority of snowmobile market share. Leading vendors maintain vertically integrated operations spanning engine development, chassis engineering, and dealer-based distribution networks. Brand loyalty plays a critical role in sustaining long-term competitive positioning. Product innovation remains central to differentiation. Manufacturers invest in lightweight materials, enhanced suspension systems, and improved four-stroke engine efficiency to maintain snowmobile market growth. Performance segmentation continues to drive premium pricing strategies.

Dealer networks represent a structural competitive advantage. Established service infrastructure supports aftermarket revenue and strengthens customer retention. Independent dealerships influence regional snowmobile market size dynamics through localized marketing and financing solutions. Niche players operate within performance modification and specialty custom segments. These firms cater to enthusiast communities seeking tailored configurations. Although limited in scale, they influence brand perception and innovation direction.

Strategic partnerships with tourism operators and government agencies support fleet sales stability. Utility snowmobiles supplied to forestry and emergency services create recurring procurement relationships. Barriers to entry remain significant due to capital-intensive manufacturing, regulatory compliance requirements, and seasonal demand concentration. Economies of scale and brand equity reinforce incumbent positioning.

List of Key Companies Profiled:

- Artic Cat Inc. (U.S.)

- Bombardier Recreational Products (Canada)

- Polaris Inc. (U.S.)

- Yamaha Motor Corporation (Japan)

- Alpina Snowmobiles S.r.l.

- TAIGA (Canada)

- Aurora Powertrains (Finland)

- AD Boivin Inc. (Canada)

- Crazy Mountain Xtreme (Canada)

KEY INDUSTRY DEVELOPMENTS:

- January 2024 – X Games, the foremost global event for action sports, and Taiga Motors Corporation, a leading Canadian brand specializing in electric powersports, unveiled an unprecedented partnership. This landmark agreement designates Taiga as the exclusive provider of Electric Snowmobiles for X Games Aspen 2024, marking a significant milestone in electrified winter sports.

- January 2024 – The Forest Service granted a contract to Weller Recreation Inc. for procuring and transporting 18 snowmobiles to the Dillon Ranger District within the White River National Forest. The contract, valued at $18,000, underscores efforts to bolster mobility and operational capabilities within the district's snowy terrain.

- March 2023- Arctic Cat, a subsidiary of Textron Inc., announced its 2024 snowmobile lineup, the all-new CATALYST platform, a lightweight, durable, and centralized platform designed with the rider in mind. The company also reintroduced the full-size touring Pantera 7000, ZR 7000, and ZR 9000 RR.

- March 2023 – Polaris Inc. announced the launch of a comprehensive snow bike portfolio with new and improved rider-driven innovations and features to deliver high performance, agility, and control. The lineup includes the new Series 9 325 track and Timbersled's new RIOT Gen 2 system.

- July 2022 – Pro Armor, one of the leaders in aftermarket powersports, a subsidiary of Polaris’ PG&A, launched its snowmobile line. With this launch, the company aims to enhance riders’ adventures with customized, purpose-built style, and performance accessories.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The report provides the market analysis and focuses on key aspects such as leading companies, product/service types, and leading product applications. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the market growth in recent years.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.30% from 2026 to 2034 |

|

Unit |

Value (USD Billion) Volume (Units) |

|

Segmentation |

By Product Type

By Engine Type

By Seating Capacity

By Seating

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 2.04 billion in 2025.

The market is likely to grow at a CAGR of 7.30% over the forecast period (2026-2034).

The trail segment is expected to lead the market due to its growing popularity among young riders.

Some of the top players in the market are Arctic Cat, Polaris, Yamaha, and Taiga.

North America dominated the snowmobile market with a share of 78.73% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us