Aircraft Engine Forging Market Size, Share & Industry Analysis, By Type (Open Die Forging, Closed Die Forging, and Seamless Rolled Ring Forging), By Material (Aluminum Alloys, Titanium Alloys, Nickel Superalloys, Steel Alloys, and Others), By Engine Component (Turbine Disks, Compressor Blades, Shafts, Casings, and Others), By Engine Type (Turbofan Engines, Turbojet Engines, Turboprop Engines, and Turboshaft Engines), By Aircraft Type (Fixed Wing Aircraft, and Rotary Wing Aircraft), By End User (OEM and Aftermarket), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

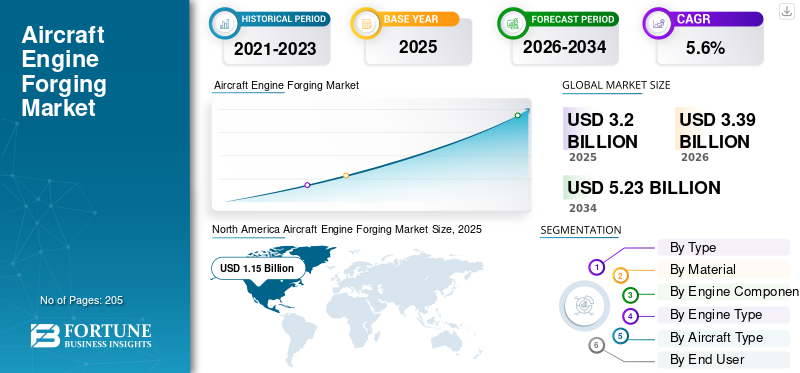

The global aircraft engine forging market size was valued at USD 3.20 billion in 2025. The market is projected to grow from USD 3.39 billion in 2026 to USD 5.23 billion by 2034, exhibiting a CAGR of 5.6% during the forecast period.

Aircraft engine forging involves controlled deformation of high-temperature alloys using powerful presses or hammers to create strong and defect-resistant preforms. The process of forging is conducted at precise temperatures, which causes the metal grain flow to follow the shape of the part. This improves the strength, fatigue life, and creep resistance of the forged components. The core methods used in forging technology include open-die and closed-die/precision forging, isothermal or near-isothermal forging for difficult superalloys, and ring rolling for seamless cases and large rings. Typical materials are nickel-based superalloys, titanium alloys, and high-strength steels, chosen for their performance in hot and high-load environments.

The aircraft engine forging market is led by key players such as Precision Castparts Corp., Safran Aircraft Engines, and ATI Inc., which are prominent in manufacturing high-performance forged components such as turbine disks, compressor blades, and shafts. Precision Castparts Corp. is recognized for its extensive portfolio of forged aerospace parts, while Safran Aircraft Engines collaborates globally to supply forgings for commercial engines such as the LEAP engine for Airbus and Boeing aircraft. ATI Inc. supports leading airframers such as Airbus through multi-year agreements supplying specialized titanium products.

Download Free sample to learn more about this report.

Aircraft Engine Forging Market Key Takeaways

- 2025 Market Size: USD 3.20 billion

- 2026 Market Size: USD 3.39 billion

- 2034 Forecast Market Size: USD 5.23 billion

- CAGR: 5.6% from 2026–2034

- North America dominated the market in 2025.

- Closed-die forging segment held the largest market share, driven by demand for high-precision engine components.

- OEM segment dominated the market, supported by rising production of next-generation aircraft engines.

North America

The market reached USD 1.15 billion in 2025, driven by a strong aerospace manufacturing base.

Asia Pacific

The region is expected to witness the fastest growth during the forecast period.

Europe

The market is supported by its mature aero-engine manufacturing ecosystem.

U.S.

The market is driven by investments in forging capacity and supply chain expansion.

Japan

The market is supported by growing domestic production of aircraft engine components.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increase In Commercial Single-Aisle Production to Improve Market Growth

Aircraft manufacturers and engine OEMs are prioritizing weight reduction and thermodynamic efficiency to meet zero-emission and sustainability targets. This is expected to directly increase demand for forged components with superior strength-to-weight ratios. Precise forging of titanium and nickel-based superalloys delivers aligned grain flow and low defect rates, enabling higher pressure ratios, hotter cores, and longer life for disks, rings/cases, and shafts. Moreover, the increase in commercial single-aisle production with rising demand for original-equipment forged parts and life-limited-part replacements is thereby expanding the aircraft engine forging market growth.

MARKET RESTRAINTS

High Development and Installation Costs to Limit Market Expansion

The capital-intensive nature of aircraft engine forging is a significant barrier to rapid capacity expansion. Equipment such as isothermal presses, large ring mills, heat-treat furnaces, dies, and tooling requires substantial upfront investment, which slows new capacity additions. In addition, extensive metallurgical qualifications, production part approval process (PPAP), first article inspections (FAI), and recurring coupon testing demand considerable time and financial resources before revenue generation can begin. The energy-intensive processes and volatility in prices of key raw materials such as nickel and titanium are expected to hamper the growth of the market.

MARKET OPPORTUNITIES

Surging Production of Next-Generation Aircraft Programs and Sustainable Aviation Initiatives Boost Industry Growth

The market is experiencing significant growth opportunities driven by the surging production of next-generation commercial and military aircraft requiring components made from advanced forging. Increasing global air travel and fleet modernization initiatives are amplifying demand for high-performance, fuel-efficient engines, prompting manufacturers to adopt innovative forging technologies and superior materials such as titanium and nickel-based superalloys. Sustainable aviation initiatives, including the shift toward hybrid-electric propulsion and sustainable aviation fuels (SAF), are promoting the development of specialized forged parts optimized for these new engine designs. Therefore, these factors are expected to present opportunities for the expansion of the market during the forecast period.

AIRCRAFT ENGINE FORGING MARKET TRENDS

Adoption of AI, Digital Twins, and Modular Design is a Significant Trend

A significant trend shaping the market is the integration of advanced digital technologies such as artificial intelligence (AI), machine learning, and digital twin simulations. These innovations optimize forging processes by enabling predictive maintenance, real-time quality control, and waste reduction, thereby enhancing production efficiency and product reliability. Moreover, the market is witnessing a shift toward modular component designs and the use of lightweight forged parts, which support evolving aircraft architectures and increasingly stringent environmental objectives.

MARKET CHALLENGES

Supply Chain Complexities and Regulatory Challenges to Constrain Market Growth

The market faces significant challenges from complex supply chains marked by raw material price volatility and geopolitical uncertainties that disrupt sourcing and timely delivery. The environmental and safety regulations are becoming stringent, which requires firms to invest continuously in innovation and compliance. This has increased operational costs and created barriers, particularly for smaller players entering the market. Furthermore, prolonged lead times for critical aerospace-grade materials such as titanium and nickel alloys exacerbate production delays, limiting supply chain responsiveness and hampering the growth of the market.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Ability to Provide Tight Tolerances Drives Closed-Die Forging Segment Growth

On the basis of type, the market is classified into open die forging, closed die forging, and seamless rolled ring forging.

The closed die forging segment acquires the largest share of the market due to its ability to deliver high repeatability, tight tolerances, and optimized grain flow for critical rotating parts at scale. These attributes are essential for turbine disks, shafts, and high-stress airfoils. This demand for closed die forging engine components continues to drive segment growth.

The seamless rolled ring forging is the fastest-growing segment of the market, driven by hotter core architectures and larger case diameters that require high-integrity rings. Seamless rolled ring forging is increasingly preferred in aircraft engines as it produces components with superior strength, durability, and resistance to high temperatures and fatigue. The growth of the segment will rise during the forecast period due to the enhanced structural integrity it provides for critical engine parts such as turbine disks and shafts.

By Material

Nickel Superalloys Segment Dominates the Market due to their Oxidation Behavior

Based on material, the market is segmented into aluminum alloys, titanium alloys, nickel superalloys, steel alloys, and others.

The nickel superalloys segment acquires the largest share of the market due to their indispensability in hot-section components operating at extreme temperatures and stresses. The nickel-based materials provide superior creep resistance, low-cycle fatigue performance, and oxidation behavior. Thus, the segment dominates the market, as it is extensively used in turbine disks, seals, rings, and structural cases.

- For instance, in February 2025, Hindustan Aeronautics Limited signed a long-term contract with Safran Aircraft Engines to manufacture turbine forged parts, including critical nickel ring forgings, for LEAP engines at its Bengaluru Ring Rolling facility.

The titanium alloys segment is the fastest-growing segment of the market, driven by fuel-burn reduction targets and broader adoption in fan and compressor structures. High specific strength, corrosion resistance, and fatigue performance support lighter designs, which is expected to increase the demand for titanium alloys in the construction of engine parts during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Engine Component

Ability to Withstand Extreme Engine Conditions Support Turbine Disks Segment Growth

Based on engine component, the market is segmented into turbine disks, compressor blades, shafts, casings, and others.

The turbine disks segment acquires the largest share of the market. The growth of forged turbine disks, specifically in aircraft engine forging, is driven by their critical role in withstanding extreme temperatures and centrifugal forces within modern engines, driving demand for high-strength superalloys and precision forging techniques. Material innovations such as advanced nickel-based superalloys and rapid-cooling forging methods directly improve turbine disk durability and are expected to drive the segment’s growth.

The compressor blades are the fastest-growing segment of the market, driven by rising overall pressure ratios and airfoil innovations that lift blade counts and precision requirements. The adoption of advanced systems and automation to expand the manufacturing of engine components is expected to drive segment growth.

- For instance, in June 2025, Safran Blades inaugurated a new USD 124 million state-of-the-art factory in Marchin, Belgium, to produce titanium compressor blades for aircraft engines, aimed at producing 700,000 blades annually by 2026 using advanced robotics, AI, and automation.

By Engine Type

Increasing Use of Advanced Composite Material for Development of Turbofan Engines Propels Segment Growth

Based on engine type, the market is segmented into turbofan engines, turbojet engines, turboprop engines, and turboshaft engines.

The turbofan engines segment captures the largest share of the market due to dominant commercial backlogs and aftermarket throughput. Large installed bases, expanding spare-engine pools, and recurrent LLP cycles drive demand for turbofan engines for narrowbody and widebody fleets. In addition, the use of advanced composite material for weight reduction and improved overall engine efficiency is expected to support segment growth.

- For instance, in October 2025, Rolls-Royce started building the UltraFan, the world’s largest turbofan engine with a 140-inch diameter fan, which promises 25% better fuel efficiency than current engines and uses advanced carbon-titanium fan blades and ceramic matrix composites to reduce weight and improve performance.

The turboshaft engines are the fastest-growing segment of the market, driven by rotary-wing procurement and expanding para-public missions. Expansion and modernization of military fleets across the globe which are critical for helicopters and other rotorcraft used in defense and law enforcement. This, in turn, drives demand for robust, high-performance forged engine components that can withstand extreme operational conditions.

By Aircraft Type

Increasing Aircraft Production Drives Fixed wing Aircraft Segment Growth

Based on aircraft type, the market is segmented into fixed wing aircraft and rotary wing aircraft.

The fixed wing aircraft segment secures the largest share of the market due to sustained engine production rates and high utilization in commercial operations. Advances in aerospace engine technologies and rising air travel demand are prompting manufacturers to invest in precision forging processes for critical parts such as turbine disks and compressor blades, which support the expansion of fixed wing fleet globally.

The rotary-wing aircraft is the fastest-growing segment of the market, driven by fleet renewal and high-frequency mission profiles. Elevated utilization compresses maintenance intervals, expanding demand for turboshaft-adjacent forgings in shafts, bearings, and hot-section rings from a smaller installed base.

By End User

Push Toward Next Generation Engines Drives OEM Segment Growth

Based on end user, the market is segmented into OEM and aftermarket.

The OEM segment dominates the market, driven by the push toward next-generation engines, integration of advanced materials and manufacturing technologies, such as additive forging hybrid processes. These technological and material advancements are encouraging OEMs to achieve high engine performance and weight reduction, which is propelling the growth of the segment in the market.

Aftermarket is the fastest-growing segment of the market, driven by the rapid recovery and expansion of global air travel, which is leading to more frequent maintenance, repair, and overhaul (MRO) activities. Airlines are adopting power-by-the-hour contracts and engine health management programs, increasing the need for high-quality forged spare parts to ensure engine reliability and longevity.

Aircraft Engine Forging Market Regional Outlook

North America Aircraft Engine Forging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America dominated the market and was valued at USD 1.15 billion in 2025, driven by a well-established base of skilled engine forgers and material suppliers proficient in nickel and titanium rotating parts. Sustained demand for life-limited disks, rings, and shafts is supported by rising shop visits across a large installed turbofan fleet. Moreover, ongoing investments in countries such as the U.S. in melt and forge capacity, along with selective restoration of critical materials, are enhancing supply chain security and supporting market expansion. Companies in the U.S. are developing various strategies to expand their aircraft engine forging market share.

- For instance, in June 2025, Pursuit Aerospace completed the strategic acquisition of Chicago-based Larson Forgings, expanding its U.S. capabilities in seamless rolled rings and open-die forgings for aircraft engines.

Europe

The market in Europe benefits from the region’s mature aero-engine ecosystem, which includes prime integrators, specialist forgers, and heat treatment and non-destructive testing (NDT) facilities, preserving high-value hot-section work within the region. Predictable aftermarket demand from European carriers drives steady replacement cycles for nickel disks and rings. Engine manufacturers are partnering with forging companies to secure high-quality key engine components and support increasing production and maintenance needs.

- For instance, in July 2024, U.K.-based Forged Solutions Group signed a multi-year supply agreement with Belgium’s Safran Aero Boosters to provide forged components for leading aircraft engines, including LEAP and GEnx platforms. The contract is expected to secure critical ring and shaft forging capacity in Europe to support long-term demand for Safran’s aero-engine modules.

Asia Pacific

Asia Pacific is the fastest-growing market region, fueled by expanding commercial fleets that drive both OEM engine intake and maintenance, repair, and overhaul (MRO) throughput. Nations including Japan, China, India, and South Korea are boosting local content in titanium and ring-rolled components, enhancing regional self-reliance. Government policies and industrial initiatives are strengthening domestic supply chains with qualified engine parts, which in turn support market growth in the region.

Latin America and the Middle East & Africa

Market momentum is increasing in Latin America and the Middle East & Africa regions due to a growing aerospace footprint and ongoing fleet renewals that support incremental increases in OEM and aftermarket volumes. The presence of large widebody fleets and high utilization rates at Gulf hubs sustains consistent aftermarket demand for hot-section ring and disk replacements. National strategies in Saudi Arabia and the UAE are expanding local MRO capacity while introducing selective component manufacturing to boost regional content.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic OEM Collaborations Drive Competitive Leadership in the Aircraft Engine Forging Market

The aircraft engine forging market is moderately consolidated, dominated by key global players including Precision Castparts Corp., ATI Inc., Doncasters Group, Safran SA, and Bharat Forge. Competition centers on technological innovation in forging processes, advanced materials such as nickel-based superalloys and titanium alloys, and strong partnerships with aerospace OEMs. These companies leverage extensive research and development capabilities, strategic collaborations, and government affiliations to maintain leadership in producing high-strength, fatigue-resistant forged components critical for next-generation engine performance, fuel efficiency, and sustainability.

LIST OF KEY AIRCRAFT ENGINE FORGING COMPANIES PROFILED

- Precision Castparts Corp. (U.S.)

- ATI Inc. (U.S.)

- Howmet Aerospace Inc. (U.S.)

- Forged Solutions Group Ltd. (U.K.)

- Bharat Forge Limited (India)

- Doncasters Group Ltd. (U.K.)

- Kobe Steel, Ltd. (Japan)

- MTU Aero Engines AG (Germany)

- IHI Corporation (Japan)

- Independent Forgings & Alloys Ltd. (U.K.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Rolls-Royce signed a manufacturing agreement with Bharat Forge to produce advanced fan blades in India for its Pearl 700 and Pearl 10X business-jet engines, expanding its aero-engine component sourcing footprint.

- July 2025: Bharat Forge announces its plans to set up an advanced ring mill in Pune dedicated to aero-engine components after winning a major supply contract with Pratt & Whitney Canada, significantly boosting its forging capacity for global aerospace programs.

- June 2025: Forged Solutions Group signed a multi-year supply deal with Safran Aero Boosters for ring components and shafts used in leading commercial aircraft engines, securing long-term forging capacity for LEAP and other programs.

- February 2025: China’s Aerospace Science & Technology Co. signed a long-term supply agreement with a major international commercial aero-engine manufacturer for annular forgings worth about USD 65 million over 2025-2030, locking in multi-year export volumes.

- February 2025: Safran Aircraft Engines signed a contract with Hindustan Aeronautics Limited for turbine forged parts, including nickel ring forgings, for LEAP engines.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.6% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, By Material, By Engine Component, By Engine Type, By Aircraft Type, By End User, and Region |

|

By Type |

· Open Die Forging · Closed Die Forging · Seamless Rolled Ring Forging |

|

By Material |

· Aluminum Alloys · Titanium Alloys · Nickel Superalloys · Steel Alloys · Others |

|

By Engine Component |

· Turbine Disks · Compressor Blades · Shafts · Casings · Others |

|

By Engine Type |

· Turbofan Engines · Turbojet Engines · Turboprop Engines · Turboshaft Engines |

|

By Aircraft Type |

· Fixed Wing Aircraft o Commercial Aircraft o Business Aircraft o General Aviation Aircraft o Military Aircraft · Rotary Wing Aircraft o Military Helicopters o Civil Helicopters |

|

By End User |

· OEM · Aftermarket |

|

By Geography |

· North America (By Type, By Material, By Component, By Engine Type, By Aircraft Type, By End User, and Country) o U.S. (By Aircraft Type) o Canada (By Aircraft Type) · Europe (By Type, By Material, By Component, By Engine Type, By Aircraft Type, By End User, and Country) o U.K. (By Aircraft Type) o Germany (By Aircraft Type) o France (By Aircraft Type) o Russia (By Aircraft Type) o Rest of Europe (By Aircraft Type) · Asia Pacific (By Type, By Material, By Component, By Engine Type, By Aircraft Type, By End User, and Country) o China (By Aircraft Type) o Japan (By Aircraft Type) o India (By Aircraft Type) o South Korea (By Aircraft Type) o Rest of Asia Pacific (By Aircraft Type) · Latin America (By Type, By Material, By Component, By Engine Type, By Aircraft Type, By End User, and Country) o Brazil (By Aircraft Type) o Mexico (By Aircraft Type) o Rest of Latin America (By Platform) · Middle East & Africa (By Type, By Material, By Component, By Engine Type, By Aircraft Type, By End User, and Country) o UAE (By Aircraft Type) o Saudi Arabia (By Aircraft Type) o Rest of Middle East & Africa (By Aircraft Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.20 billion in 2025 and is projected to reach USD 5.23 billion by 2034.

In 2025, the market value stood at USD 1.15 billion.

The market is growing at a CAGR of 5.6% during the forecast period (2026-2034).

The closed die forging segment leads the market by type.

The key factor driving the market is the surging production of next-generation aircraft programs.

Precision Castparts Corp. (U.S.), ATI Inc. (U.S.), Howmet Aerospace Inc. (U.S.), and Forged Solutions Group Ltd. (U.K.) are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us