Aircraft Engine Market Size, Share, & Industry Analysis, By Engine Type (Turboprop, Turboshaft, Turbofan, and Piston Engine), By Technology (Conventional and Electric/Hybrid), By Component (Compressor, Turbine, Gear Box, Exhaust Nozzle, Fuel System, and Others), By End-Use (Commercial and Military), By Commercial (Narrow Body, Wide Body, Business Jet, General Aviation, and Civil Helicopters), By Military (Fighter, Transport, and Military Helicopter), By Offering (OEM Engine and Aftermarket & MRO), and Regional Forecast 2026-2034

(Offer valid till 31st Jul 2026)

KEY MARKET INSIGHTS

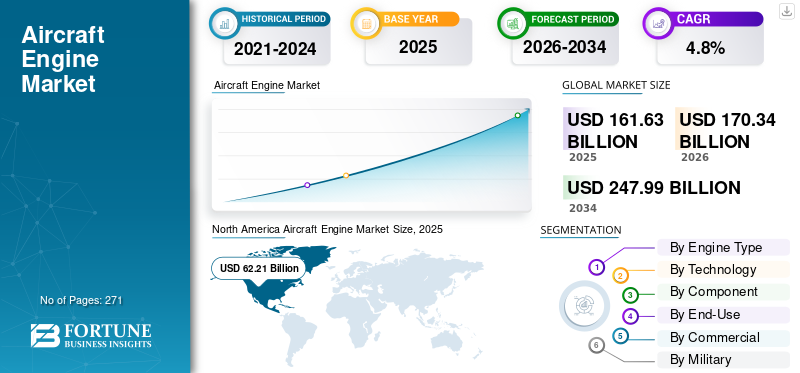

The global aircraft engine market size was valued at USD 161.6 billion in 2025 and is projected to grow from USD 170.3 billion in 2026 to USD 248 billion by 2034, exhibiting a CAGR of 4.8% during the forecast period. North America dominated the global aircraft engine market with a market share of 38.5% in 2025.

The aircraft engine market represents the global ecosystem of turbofan, turboprop, turboshaft, and piston propulsion systems powering commercial aviation, military platforms, business jets, and general aviation operations. Aircraft engines are deployed across diverse operational applications, including scheduled commercial passenger transportation on narrow-body and wide-body platforms, such as the Boeing 737 MAX and Airbus A320neo, and the Boeing 787 Dreamliner and Airbus A350. Second, military fighter operations include the F-35 with Pratt & Whitney F135 engines, and the F-16 with GE F110 engines; military transport and strategic airlift, such as the C-130J, C-17, and KC-46 tanker; military helicopter operations, such as Black Hawk and Apache helicopters that are transitioning to the GE T901 engines; regional air connectivity through turboprop aircraft; business jet engine charter services, and general aviation flight training.

The market is experiencing outstanding growth driven by numerous factors, including sustained commercial aviation recovery, with global air passenger traffic expansion considerably outstripping historic baselines. Extensive military modernization programs, with global defense spending surpassing USD 2.4 trillion annually, and a key emphasis on advanced fighter jet procurement and fleet modernization initiatives that transition aging turbofan-equipped aircraft toward next-generation, fuel-efficient LEAP and GTF platforms.

The market is highly consolidated, with four manufacturers supplying 99% of commercial and military aircraft engines: the CFM International-GE Aerospace/Safran joint venture Pratt & Whitney, Rolls-Royce, and General Electric, among others. Strategic competition focuses on optimizing fuel efficiency, developing compatible sustainable aviation fuels, integrating digital health monitoring, and implementing long-term performance-based maintenance contracts. This competitive differentiation comes through integrated lifecycle support rather than traditional unit-price competition.

Download Free sample to learn more about this report.

Aircraft Engine Market Key Takeaways

- 2025 Market Size: USD 161.6 billion

- 2026 Market Size: USD 170.3 billion

- 2034 Forecast Market Size: USD 248 billion

- CAGR: 4.8% from 2026-2034

- North America dominated the aircraft engine market with a 38.5% share in 2025.

- The turboprop segment accounted for the largest market share of 64.65% in 2026.

- The conventional segment held a dominant share of 89.62% in 2026.

North America

North America accounted for USD 62.2 billion in 2025 and is projected to reach USD 64.8 billion in 2026.

Asia Pacific

Asia Pacific was valued at USD 41 billion in 2025 and is estimated to reach USD 43 billion in 2026.

Europe

Europe accounted for USD 48 billion in 2025 and is projected to reach USD 50.7 billion in 2026.

U.S.

The market is estimated to reach USD 60.48 billion in 2026.

Japan

The market was valued at USD 4.46 billion in 2026.

Read More

Aircraft Engine Market Trends

Next-Generation High-Efficiency Engine Development and Revolutionary Design Paradigms Catalyze Market Trends

The aircraft engine industry is advancing a comprehensive portfolio of next-generation propulsion technologies specifically designed to achieve substantial improvements in thermal efficiency, fuel economy, and environmental performance while maintaining architectural compatibility with existing aircraft platforms and airport infrastructure.

CFM International's Revolutionary Innovation for Sustainable Engines program, unveiled in June 2021 and advancing rapidly through 2025, represents the most mature next-generation commercial engine initiative, targeting entry into service in the mid-2030s.

The RISE program encompasses development of an open fan architecture featuring variable-pitch carbon fiber composite blades, representing a fundamental departure from conventional enclosed turbofan design philosophy.

- In October 2025, CFM International completed comprehensive dust-ingestion testing on next-generation high-pressure turbine airfoils, marking an advanced milestone in the progression from component-level evaluations to module-level testing.

Download Free sample to learn more about this report.

Market Dynamics

MARKET DRIVERS

Sustained Global Aviation Recovery and Fleet Modernization Imperative Propel Market Growth

The global aircraft engine market growth is driven by an accelerating rebound in commercial aviation demand, coupled with an urgent industry-wide fleet modernization cycle.

- For instance, in December 2025, China Aircraft Leasing Group Holdings Limited (CALC) signed a firm order with Airbus for 30 A320neo Family aircraft to meet strong demand from its customer base. The agreement is the fifth order with Airbus, bringing the total number of Airbus aircraft ordered by CALC to 282, of which 203 are A320neo Family aircraft.

The International Air Transport Association projects that passenger volumes could reach 8.2 billion by 2037, effectively doubling current traffic, necessitating substantial expansion of existing airline fleets and corresponding engine procurement.

This structural demand growth is further amplified by regulatory mandates and industry commitments that require airlines to retire older, less efficient aircraft in favor of next-generation aircraft. The backlog of unfilled aircraft orders exceeds 17,000 units, representing unprecedented demand for new engines as these aircraft are delivered over the coming decade.

MARKET RESTRAINTS

Structural Engine Production Constraints and Manufacturing Capacity Limitations Hamper Market Growth

Despite robust demand, the aircraft engine industry faces acute supply-side constraints that systematically limit growth and create substantial economic inefficiencies across the aerospace ecosystem.

Engine production has demonstrably failed to keep pace with airframe manufacturing, creating a paradoxical situation in which newly completed aircraft are parked in holding areas awaiting engine availability.

The International Air Transport Association's December 2025 assessment documented that engine output remains constrained by ongoing technical issues with in-service engines, severely limited shop capacity at engine overhaul facilities, and extended maintenance timelines that have effectively consumed available repair resources.

MARKET OPPORTUNITIES

Alternative Fuel Integration and Zero-Emission Technology Pathways Create Emerging Opportunities for Market Growth

The aircraft engine industry faces a compelling market opportunity arising from the systematic transition toward sustainable aviation fuels and zero-emission propulsion architectures mandated by international climate commitments and regulatory frameworks.

According to the International Air Transport Association, the airline industry plans to achieve net-zero carbon emissions by 2050, establishing a mitigation pathway comprising 65% emissions reductions attributable to sustainable aviation fuel deployment, 13% from new aircraft and propulsion technologies, 3% from operational and infrastructure improvements, and 19% from carbon capture initiatives and offsetting mechanisms.

The ICAO global framework for sustainable aviation fuels establishes a collective aspirational vision to reduce CO2 emissions in international aviation by 5% by 2030 compared to baseline zero cleaner energy use, with the long-term aspiration targeting net-zero carbon emissions by 2050, supporting Paris Agreement climate objectives.

MARKET CHALLENGES

Supply Chain and Manufacturing Constraints Limiting Production Rate Expansion Despite Record Aircraft Order Backlogs

The supply chain for global aircraft engines has severe bottlenecks that create structural mismatches between demand and availability, to the extent that newly completed aircraft are parked while awaiting engine deliveries. Engine manufacturers face an approximately 30% shortfall against projected 2025 production targets, with CFM International unable to meet Airbus A320neo requirements and Pratt & Whitney struggling to accelerate geared turbofan deliveries despite 100+ engines-per-month targets by 2026-2027.

Constraints are driven by persistent in-service engine issues that require extended maintenance turnaround times, limited MRO shop capacity with 12-24-month backlogs, and extended component procurement timelines from single- or near-single-source suppliers that turn minor disruptions into major delays.

SEGMENTATION ANALYSIS

By Engine Type

Growing Advancements in High-Bypass Designs that Enhance Fuel Economy Boosted Turboprop Segment Growth

Based on the engine type, the market is divided into turboprop, turboshaft, turbofan, and piston engine.

The turboprop segment dominated the global market in 2025. It accounted for 64.65% market share in 2026 and is anticipated to be the growing segment at a CAGR of 4.56% during the forecast period of 2026-2034. Dominance driven by increased demand for air travel and by optimization for short-haul routes, with fuel efficiency on routes below 500 nautical miles, places turboprops as the preferred propulsion for regional carriers connecting smaller airports and underserved communities.

The turbofan sub-segment is anticipated to be the fastest-growing, with a 6.86% CAGR during the forecast period of 2026-2034.

By Technology

Growing Ongoing Evolutions Fostered Conventional Segmental Dominance

Based on technology, the market is divided into conventional and electric/hybrid.

The conventional segment will dominate the global market with share of 89.62% in 2026. It accounts for 89.80% market share in 2025 and is anticipated to grow at a CAGR of 4.56% during the forecast period of 2026-2034. Conventional engine manufacturers continue to evolve through systematic technology development in pursuit of next-generation architectures, including CFM's RISE program, with its open fan architecture, which combines turbofan bypass efficiency with turboprop fuel-economy characteristics.

The electric/hybrid segment is estimated to be the fastest-growing segment in the global market, with the highest CAGR of 6.75% during the forecast period.

By Component

Growing Adoption of Ceramic Matrix Composites (CMCS) Versus Traditional Alloys Augmented Turbine Segmental Growth

Based on the component, the market is divided into compressor, turbine, gearbox, exhaust nozzle, fuel system, and others.

The turbine segment dominated the global aircraft engine market share in 2025. It accounted for 34.60% market share in 2025 and is anticipated to grow at a CAGR of 5.40% during the forecast period. The turbine segment represents one of the higher-value aircraft engine segments, experiencing transformational growth through the adoption of CMCs, which enable operating temperatures 200-400°F above those of conventional super alloy materials while reducing turbine blade weight by 30-50% compared to metal alternatives. The compressor segment is expected to lead the market, contributing 28% globally in 2026.

The fuel system segment is projected to be the fastest-growing, with a 5.93% CAGR during the forecast period of 2026-2034.

By End-Use

Sustained Program of Fleet Modernization Propelled Commercial Segment Growth

Based on the end-use, the market is divided into commercial and military.

The commercial segment dominated the global market in 2025. It will account for a 73.58% market share in 2026 and will be the fastest-growing segment, registering a CAGR of 4.97% during the forecast period. The commercial segment is seeing a remarkable boom, fueled by record global aircraft orders of more than 17,000 units to establish multi-decade production pipelines; a sustained program of fleet modernization at the world's airlines as they transition ageing turbofan engines to next-generation, fuel-efficient platforms; and strong growth in regional aviation.

The military sub-segment is expected to grow significantly during the forecast period, with a CAGR of 4.34% from 2026 to 2034.

By Commercial

Capitalizing On High-Volume Production Ramps Fueled Narrow Body Segmental Growth

Based on the commercial, the market is divided into narrow body, wide body, business jet, general aviation, and civil helicopters.

The narrow body segment dominated the global market in 2025. It accounted for 47.91% market share in 2025 and is anticipated to be the fastest-growing segment at a CAGR of 5.59% during the forecast period. Narrow-body production is experiencing unprecedented expansion, driven by backlogs of 17,000-plus-unit aircraft orders, which represent 12- to 15-year production pipelines and fleet modernization, transitioning aging aircraft toward next-generation fuel-efficient engines.

The wide-body segment is estimated to be the second-fastest-growing during the forecast period, with a CAGR of 4.43% from 2026 to 2034.

To know how our report can help streamline your business, Speak to Analyst

By Military

Fighter Segment Led Market Due to Stealth Tech and Vectored Thrust Capabilities

Based on the military, the market is divided into fighter, transport, and military helicopter.

The fighter segment dominated the global market in 2025. It accounted for 55.71% market share in 2025 and is anticipated to be the fastest-growing segment at a CAGR of 5.54% during the forecast period. Dominant engines include Pratt & Whitney F135, exclusive to the F-35; Pratt & Whitney F119, exclusive to the F-22; GE F110, primarily used in the F-16; and Rolls-Royce EJ200, used in the Eurofighter jets. Integrate advanced stealth capabilities, including radar-absorbent coatings, specialized exhaust nozzles to reduce infrared detection, and vectored thrust for superior maneuverability.

The military helicopter segment is experiencing robust growth with a CAGR of 4.56% during the forecast period of 2026-2034.

By Offering

Expansion of Commercial Aircraft Fleet Boosted Aftermarket & MRO Segment Expansion

Based on the offering, the market is divided into OEM engine and aftermarket & MRO.

The aftermarket & MRO segment accounted for the largest share of the global market in 2025. It accounted for 64.42% market share in 2025 and is anticipated to be the fastest-growing segment at a CAGR of 5.31% during the forecast period. Aftermarket demand is driven by the commercial aircraft fleet expanding from 28,000 to 39,000+ aircraft by 2043, establishing an unprecedented installed base supporting distributed global maintenance services. Commercial aircraft accumulating 400-500 flight hours per month generate recurring maintenance requirements at standardized intervals, creating predictable long-term aftermarket revenues independent of new-production cycles.

The OEM sub-segment is anticipated to grow at a significant rate, with a CAGR of 3.79% during the forecast period.

Aircraft Engine Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America Aircraft Engine Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America contributed 38.50% to the global market in 2025, with a valuation of USD 62.2 billion, and is projected to reach USD 64.8 billion in 2026, establishing the region as the dominant global market leader through mature commercial aviation, extensive military operations, and advanced manufacturing capabilities.U.S. Aircraft Engine Market

Given U.S. dominance in the region, the U.S. market can be approximated at around USD 60.48 billion in 2026, with an estimated growth rate of 3.35% during the forecast period.

Europe

Europe accounted for USD 48 billion in 2025, representing 29.70% of the global market share, and is projected to reach USD 50.7 billion in 2026, establishing the region as the second-largest, with a distinct sustainability emphasis and advanced technology focus.

U.K. Aircraft Engine Market

The U.K. market in 2026 was valued at USD 9.53 billion, with an estimated growth rate of 4.94% during the forecast period.

Germany Aircraft Engine Market

The German market in 2026 was valued at USD 7.35 billion, with an estimated growth rate of 6.27% during the forecast period.

Rest of Europe Aircraft Engine Market

The rest of the European market in 2025 was valued at USD 11.68 billion, with an estimated growth rate of 6.26% during the forecast period.

Asia Pacific

The Asia Pacific market was valued at USD 41 billion in 2025, capturing 25.30% of global revenue, and is estimated to reach USD 43 billion in 2026. Also, the region is estimated to be the fastest-growing, with the highest CAGR of 6.56% during the forecast period.

China Aircraft Engine Market

The Chinese market in 2026 was valued at USD 15.09 billion, with an estimated growth rate of 7.16% during the forecast period.

India Aircraft Engine Market

The Indian market in 2026 was valued at USD 5.59 billion, with an estimated growth rate of 6.27% during the forecast period.

Japan Aircraft Engine Market

The Japanese market in 2026 was valued at USD 4.46 billion, with an estimated growth rate of 9.20% during the forecast period.

Rest of the World

The Rest of the World region captured 6.50% of the global market in 2025, generating USD 10.6 billion in revenue, and is projected to reach USD 11.7 billion in 2026. The Rest of the World, comprising the Middle East & Africa and Latin America regions, is expected to witness moderate growth in this market space during the forecast period.

Middle East & Africa

The Middle East & Africa market in 2025 was valued at USD 7.69 billion, with an estimated growth rate of 3.16% during the forecast period.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Structure Demonstrating Oligopolistic Consolidation with Dominant Manufacturers Controlling Largest Market Share

The global market is dominated by a tight oligopoly of four main players that effectively control commercial propulsion and create powerful barriers to new entrants or disruption. The major players are CFM International (a 50/50 joint venture between GE Aerospace and Safran), Pratt & Whitney, Rolls-Royce, and GE Aerospace, which hold the majority of the global market share.

Competition here is not primarily driven by price but rather by technological differentiation, improved fuel efficiency, and superior integrated aftermarket service. Performance and service superiority are used to press rivals rather than cut-price tactics.

LIST OF KEY AIRCRAFT ENGINE COMPANIES PROFILED

- CFM International SA (France)

- Honeywell International Inc. (U.S.)

- GE Aviation (U.S.)

- Rolls-Royce Holdings Plc. (U.K.)

- Safran SA (France)

- International Aero Engines AG (U.S.)

- MTU Aero Engines AG (Germany)

- Textron Inc. (U.S.)

- Pratt & Whitney (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: The Air Force granted Boeing Defense Systems a contract exceeding USD 2 billion to initiate the initial engine replacements for the B-52H Stratofortress, representing a significant advancement in the refurbishment of the long-serving Cold War-era bomber.

- January 2026: RESIDCO revealed the completion of a USD 100 million financing facility for the acquisition of commercial aircraft engines. This new debt facility aims to bolster RESIDCO’s strategic growth in the global secondary aviation sector, with a particular focus on the purchase of in-demand commercial aircraft engines.

- November 2025: Azad Engineering from India entered into a partnership with Pratt & Whitney Canada Corporation to create and manufacture components for aircraft engines. Based in Hyderabad, Azad produces industrial machinery and equipment for the aerospace, defense, and energy industries.

- February 2025: During the Aero India trade exhibition in Bengaluru, India, Safran Aircraft Engines agreed with Hindustan Aeronautics Limited (HAL), the prominent aviation firm in India, to manufacture forged turbine components for LEAP engines. The aim is to bolster the significant expansion of the Indian aviation sector and facilitate increased production of LEAP engines that power single-aisle commercial aircraft.

- February 2025: GE Aerospace entered into a five-year Performance Based Logistics (PBL) agreement with the Indian Air Force (IAF) to deliver a complete sustainment solution for the T700-GE-701D engines that power the IAF’s AH-64E-I Apache helicopter fleet.

REPORT COVERAGE

The global aircraft engine market analysis includes a comprehensive study of the market size & forecast across all market segments covered in the report. It includes details on the market dynamics and global market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments, as well as their prevalence by key regions. The global market research report also provides a detailed competitive landscape, including market share and profiles of key players operating in the market.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.81% from 2026-2034 |

|

Unit |

USD Billion |

|

Segmentation

|

By Engine Type · Turboprop · Turboshaft · Turbofan · Piston Engine By Technology · Conventional · Electric/hybrid By Component · Compressor · Turbine · Gear Box · Exhaust Nozzle · Fuel System · Others By End-Use · Commercial · Military By Commercial · Narrow Body · Wide Body · Business Jet · General Aviation · Civil Helicopters By Military · Fighter · Transport · Military Helicopter By Offering · OEM Engine · Aftermarket & MRO By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 161.6 billion in 2025 and is projected to reach USD 248 billion by 2034.

In 2025, the market value in Europe stood at USD 50.7 billion.

The market is expected to grow at a CAGR of 4.8% over the forecast period of 2026-2034.

By engine type, the turboprop segment led the market.

Sustained global aviation recovery and the imperative of fleet modernization propel market growth.

The major players are CFM International, Pratt & Whitney, Rolls-Royce, and GE Aerospace, which hold the majority of the global market share.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 271

-

(Offer valid till 31st Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us