Aircraft Exhaust System Market Size, Share & Industry Analysis, By Aircraft Type (Commercial, Regional Jets, Business Aviation, Military Fixed-Wing, Helicopters (Civil & Military), and General Aviation (Piston/Turboprop)), By Engine Type (Turbofan, Turboshaft (Helicopter), Turboprop, and Piston (GA)), By System (Engine Exhaust System and Auxiliary Power Unit (APU) Exhaust System), By Application (Civil/Commercial and Military), By End User (Aftermarket and OEM), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

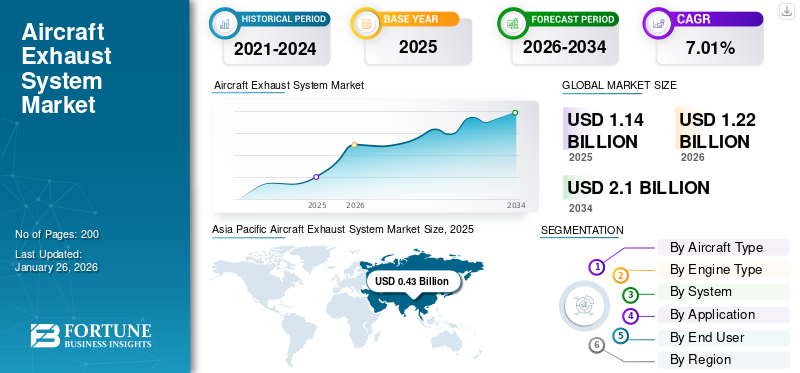

The global aircraft exhaust system market size was valued at USD 1.14 billion in 2025 and is projected to grow from USD 1.22 billion in 2026 to USD 2.1 billion by 2034, exhibiting a CAGR of 7.01% during the forecast period. Asia Pacific dominated the global market with a share of 37.85% in 2025.

The aircraft exhaust system market covers turbine and piston platforms and spans engine and APU exhaust assemblies’ nozzles, mixers, chevrons, liners, tailpipes, and ducts. Demand is anchored by three durable forces: high fleet utilization that accelerates hot-section wear, deep OEM backlogs that secure multi-year line-fit volumes, and tightening noise/emissions rules that reward quieter, hotter-capable architectures. Suppliers are lifting performance with advanced nickel superalloys, emerging CMC use, and additive manufacturing that enables complex acoustics and quicker spares. Airlines and cargo operators prioritize retrofits that cut fuel burn, ramp noise, and turn-time, while airports curb APU usage and promote monitoring kits. Regionally, Asia Pacific and the Middle East add line-fit momentum through rapid fleet growth, while North America and Europe compound aftermarket demand via aging aircraft and established MRO networks. The result is rising technology content per shipset and resilient, price-supported aftermarket revenue.

Doncasters, Ducommun, Hellenic Aerospace Industry (HAI), ITP Aero, Magellan Aerospace, Nexcelle, Nicrocraft, NORDAM, Safran, and Senior Aerospace anchor the aircraft exhaust value chain. They pair certified propulsion integration with hot-section metallurgy to deliver mixers, chevrons, liners, cones, nozzles, and ducts that cut fuel burn and noise. Advanced alloys/CMCs and additive manufacturing reduce weight and lead times. Deep MRO/DER repair capacity, rotable pools, and localized footprints compress turnarounds for LEAP, GTF, and legacy fleets. Long program ties and risk-sharing with engine/airframe OEMs secure durable backlogs, while airport noise rules and sustainability targets drive retrofits sustaining demand as build rates rise.

Download Free sample to learn more about this report.

Aircraft Exhaust System Market Takeaways

- 2025 Market Size: USD 1.14 billion

- 2026 Market Size: USD 1.22 billion

- 2034 Forecast Market Size: USD 2.10 billion

- CAGR: 7.01% from 2026–2034

- Asia Pacific dominated the aircraft exhaust system market with a 37.85% share in 2025.

- The turbofan segment is projected to lead the market with a 70.09% share in 2026.

- The aftermarket segment is expected to account for 53.71% of the global market in 2026.

North America

North America accounted for 29.70% of the global market in 2025 and is expected to reach USD 0.36 billion in 2026.

Europe

Europe represented 21.98% of the global market in 2025 and is projected to grow to USD 0.27 billion in 2026.

Asia Pacific

Asia Pacific led the global market with USD 0.43 billion in 2025 and is projected to reach USD 0.46 billion in 2026.

U.S.

The U.S. aircraft exhaust system market is projected to reach USD 0.31 billion by 2026.

Japan

The Japan aircraft exhaust system market is anticipated to reach USD 0.05 billion by 2026,

Read More

AIRCRAFT EXHAUST SYSTEM MARKET TRENDS

Decarbonisation, Acoustic Compliance, and Digital MRO are Reshaping Exhaust Architectures to Accentuate Market Growth

The aircraft exhaust system market share is trending toward lighter, hotter-capable, and quieter flowpaths as airlines chase fuel savings and airports tighten noise limits. OEMs and tier suppliers are redesigning mixers, chevrons, nozzles, and liners to squeeze out drag and decibels, while protecting durability at higher turbine exit temperatures. Ceramic matrix composites and advanced nickel superalloys are moving from trials to targeted production, often paired with additive manufacturing to unlock complex acoustics and weight reductions. On the services side, the center of gravity shifts toward data-driven maintenance: sensorized EGT probes, digital twins, and predictive analytics fold exhaust wear into shop-visit planning to control turn times. Sustainability programs, from SAF adoption to APU-use restrictions, nudge operators to retrofit quieter, cleaner exhaust and improve sealing/insulation for ramp workers’ health. Regionally, Asia Pacific and the Middle East add line-fit momentum through fleet growth, while North America and Europe compound aftermarket demand via aging fleets and stricter community-noise programs. Net effect: technology content per shipset rises, aftermarket intensity stays elevated, and qualified suppliers with repair capability and global footprints gain share.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Fleet Utilisation, OEM Backlogs, and Regulations Create Durable Demand for Hot-End Upgrades are Boosting Market Growth

Three forces power demand. First, utilisation: higher cycles and hotter cores accelerate fatigue in tailpipes, nozzles, and liners, bringing forward replacements and repairs. Second, production: deep Airbus/Boeing backlogs lock in line-fit volumes for years, with narrowbodies dominating exhaust shipsets and spares forecasts. Third, regulation: ICAO/FAA noise stages and airport community rules push airlines to quieter exhaust geometries and better acoustic treatments; environmental targets reinforce maintenance discipline and retrofit ROI. Supporting drivers add torque engine MRO capacity is tight, encouraging pre-positioned spares and PMA adoption where viable; fuel prices sustain payback for drag/noise-reducing exhaust upgrades; digital health-monitoring turns exhaust wear into predictable workscopes. Military programs contribute steady demand via thermal/signature management needs, while business aviation and cargo add resilient aftermarket activity. Together, these drivers raise technology content per shipset, keep shop-visit pipelines full, and reward suppliers that combine certified design, advanced materials, and scalable repair networks, in turn driving the aircraft exhaust system market growth.

MARKET RESTRAINTS

Qualification Cycles, Materials Volatility, and Certification Boundaries to Hamper Market Growth

Despite momentum, several brakes apply. Aerospace qualification is slow and capital-intensive; new alloys, liners, or AM geometries face lengthy testing before flight release, tying up cash and delaying revenue. Materials volatility nickel superalloys, titanium, specialty steels creates cost and lead-time spikes that squeeze margins and schedules. Certification boundaries limit rapid PMA penetration on young fleets, curbing competitive pricing in some jurisdictions. Supply-chain depth remains uneven; specialized forming, heat-treat, and acoustic perforation capacity can bottleneck major programs. Airlines’ capex cycles and balance-sheet constraints may defer optional retrofits in weaker regions. IP restrictions around nacelle/engine interfaces complicate third-party redesign, while offset and localization mandates raise setup complexity. Finally, variability in airport APU rules and noise enforcement creates fragmented demand timing. Collectively, these restraints slow conversion of technical wins into broad market adoption and require careful program selection, hedged sourcing, and early engagement with airworthiness authorities.

MARKET CHALLENGES

Hotter Cores, Quieter Cabins, and Greener Operations are Major Challenges in Market

Engineering must balance higher turbine exit temperatures and pressure ratios with stringent noise footprints, an endurance test for liners, seals, and joints under thermal cycling. Achieving quieter, lighter exhaust while preserving durability pushes the limits of CMCs, advanced superalloys, and additive builds, where repeatability and inspection standards are exacting. Quality and counterfeit-risk management tighten as demand shifts to rapid-turn repairs and rotable exchanges. Workforce skills of welding exotic alloys, AM process control, and NDT for complex lattices are scarce in some regions. Environmental rules challenge legacy processes (e.g., chromates), forcing new coatings and shop chemistries. Logistics and export-control hurdles complicate global part flows. Digitalization remains uneven: integrating sensor data, MRO records, and OEM advisories into reliable predictive models is a non-trivial change-management task. Looking ahead, hydrogen-capable architectures and higher-SAF blends may alter exhaust chemistry and condensation behavior, requiring fresh design rules and certification pathways. Meeting all this at competitive cost and compressed turn times is the market’s core execution challenge.

MARKET OPPORTUNITIES

Retrofit Waves, Additive-enabled Designs, and Regional MRO Expansion Unlock New Revenue Pools to Accentuate Market Growth

The biggest near-term opportunity is retrofit: airlines can meet noise curfews and sustainability goals by upgrading mixers, chevrons, and acoustic liners without waiting for new aircraft. Additive manufacturing opens profitable niches, lightweight nozzle plugs, intricate liner panels, and rapid-turn spares that bypass casting bottlenecks. As engine shop visits swell, DER-approved repairs (diffusers, cones, ducts) and PMA parts present cost-down options where regulators permit, creating room for independents with proven process control. APU exhaust remains a steady play as airports curb ground emissions; sealing, insulation, and monitoring kits offer fast payback. Regionally, India, Southeast Asia, and the Gulf are scaling MRO corridors, inviting joint ventures that localize exhaust repair and shorten logistics chains. For OEM-aligned suppliers, the narrowbody delivery skyline underwrites multi-year line-fit volumes; for MROs, exchange pools and rotable programs monetize availability. Longer-term, hydrogen-ready architectures and higher-SAF blend operations will demand new thermal and condensation management solutions and fresh IP for early movers. Packaging all of this as lifecycle bundles (hardware + repair + digital) can lift margins and customer stickiness.

SEGMENTATION ANALYSIS

By Aircraft Type

Commercial Segment Driven by Narrowbody Rate Hikes, Widebody Recovery, and Noise/emissions Compliance

By aircraft type, the market is segmented into commercial, regional jets, business aviation, military fixed-wing, helicopters (civil & military), and general aviation (piston/turboprop).

The commercial segment captured the largest share of the market in 2024. In 2025, the segment is anticipated to dominate with 52.91% share. Demand surges as narrowbody build-rates climb and long-haul recovers. Airlines chase fuel burn and community-noise cuts, driving mixers, chevrons, and advanced liners. High utilization accelerates wear, pushing replacements between shop visits. Sustainability targets and stricter ICAO/FAA standards force retrofits, while delivery backlogs lock multi-year line-fit volumes for exhaust assemblies globally.

The military fixed-wing segment is expected to grow at a CAGR of 7.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Civil/commercial Segment Sustained by Airline/cargo Utilization, Airport Policies, and Regional Fleet Expansion

The application segment is classified into civil/commercial and military.

The civil/commercial segment captured the largest share of the market in 2024. In 2026, the segment is anticipated to dominate with 53.14% share. Civil demand is anchored by airline and cargo operations needing reliability, cabin comfort, and tighter noise footprints. Airport APU restrictions and carbon programs push exhaust improvements and monitoring. Busy schedules raise cycles, accelerating tailpipe wear. Fleet expansion in Asia and Middle East sustains line-fit orders while mature markets fund upgrades.

The military segment is expected to grow at a CAGR of 6.8% over the forecast period.

By Engine Type

Turbofan Segment Propelled by Record Single-aisle Backlogs and High-temperature Efficiency Upgrades

The engine type segment is classified into turbofan, turboshaft (Helicopter), turboprop, and piston (GA).

The turbofan segment captured the largest share of the market in 2024. In 2026, the segment is anticipated to dominate with 70.09% share. Turbofan demand tracks record narrowbody backlogs and steady twin-aisle recovery. High exhaust temperatures and acoustic limits favor advanced liners, CMCs, and optimized mixers/chevrons. Massive LEAP and GTF fleets generate recurring spares between shop visits. Airlines pursue fuel and noise gains via retrofit nozzles and seals, boosting both line-fit and aftermarket. In 2026, the aftermarket segment is projected to lead the market with a 53.71% share.

The piston (GA) segment is expected to grow at a CAGR of 7.0% over the forecast period.

By System

Engine Exhaust System Segment Leading as it Directly affects Thrust, Noise, and Thermal Management

By system, the market is classified into engine exhaust system and auxiliary power unit (APU) exhaust system.

The engine exhaust system segment captured the largest share of the market in 2024. In 2026, the segment is anticipated to dominate with 86.51% share. Core engine exhaust leads as it directly shapes thrust, noise, and thermal signatures. Efficiency programs reward lighter, hotter-capable ducts, cones, and nozzles, increasingly designed for additive manufacture. Fleet cyclical wear drives replacements, while sensorized EGT hardware enables predictive maintenance. OEM rate increases lock line-fit volume; retrofits chase measurable fuel savings.

The auxiliary power unit (APU) exhaust system segment is expected to grow at a CAGR of 7.0% over the forecast period.

By End User

Aftermarket Segment Accelerating due to Aging Fleets, High Cycles, and MRO Capacity Constraints

By end user, the market is classified into aftermarket and OEM.

The aftermarket segment captured the largest share of the market in 2024. In 2025, the segment is anticipated to dominate with 53.62% share. Aftermarket demand is buoyed by aging fleets, high utilization, and longer turn-times at engine shops. Exhaust parts face heat-cycle fatigue, spurring replacements and repairs. Airport APU limits, inspections, and noise programs add workscopes. Supply bottlenecks support PMA/STC adoption and pricing, while rotable pools and exchanges keep aircraft available between visits.

The OEM segment is expected to grow at a CAGR of 7.0% over the forecast period.

AIRCRAFT EXHAUST SYSTEM REGIONAL OUTLOOK

In terms of geography, the market is divided into North America, Europe, Asia Pacific, and the Rest of the World.

ASIA PACIFIC

Asia Pacific Aircraft Exhaust System Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market generated USD 0.43 billion in 2025, representing 37.85% of the global market landscape, and is expected to reach USD 0.46 billion in 2026. Asia Pacific demand is propelled by rapid fleet additions, new airport capacity, and strong domestic travel. Narrowbody deliveries dominate line-fit exhaust volumes, while rising utilization accelerates wear in hot sections. Emerging MRO clusters in India, Singapore, and China expand capabilities. Middle-class growth sustains ticket demand, stabilizing aftermarket replacements.

In 2026, India market is estimated to reach USD 0.08 billion. In India, demand accelerates as airlines expand narrowbody fleets, add international routes, and push high daily utilization rapidly. Growing MRO investments and policy support deepen local repair capability. Hot-section fatigue raises replacements of liners, cones, and ducts. Airport environmental rules and APU restrictions encourage retrofits and sensorized exhaust monitoring. The Japan market is anticipated to reach USD 0.05 billion by 2026, while the China market is projected to reach USD 0.18 billion by 2026.

NORTH AMERICA

North America recorded a market size of USD 0.34 billion in 2025, capturing 29.70% of the global market share, and is projected to reach USD 0.36 billion in 2026. Demand in North America is anchored by a large installed fleet, high utilization, and long-haul recovery today. Engine and APU shop visits surge, raising replacement of nozzles, liners, and tailpipes. Sustainability and airport noise programs drive retrofits. OEM output normalizes, while business aviation and cargo add dependable aftermarket volume. The U.S. market is projected to reach USD 0.31 billion by 2026.

EUROPE

In 2025, Europe represented USD 0.25 billion, accounting for 21.98% of the worldwide market, and is projected to grow to USD 0.27 billion in 2026. Europe’s demand reflects strict noise and emissions policies, mature fleets, and resilient regional traffic and capacity. Carriers prioritize acoustic liners, mixers, and chevrons to meet airport rules. OEM and tier suppliers push lightweight alloys and CMCs. Engine MRO pipelines stay busy, supporting repairs, PMA options, and predictive maintenance hardware integration.The UK market is expected to reach USD 0.04 billion by 2026, while the Germany market is projected to reach USD 0.06 billion by 2026.

REST OF THE WORLD

The market in Rest of the World reached USD 0.12 billion in 2025, representing 10.47% of total market revenue, and is projected to reach USD 0.13 billion in 2026. Rest-of-world demand centers on Middle East widebody operations, Africa’s fleet renewals, and Latin America’s recovery. Long-haul hubs push thermal and acoustic upgrades, while harsh operating environments drive frequent tailpipe and duct replacements. OEM partnerships and offset programs localize content, steadily increasing service opportunities and exhaust component sourcing.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Due to Stricter Noise/emissions Rules, OEM Backlogs, and an MRO Surge Favor Certified Exhaust Integrators with Global Capacity and Advanced Materials Key Players are Growing

Aircraft exhaust-system leaders are in demand as they combine certified propulsion integration, hot-section metallurgy, and acoustic engineering with global production and MRO footprints. They deliver complete flowpaths mixers, chevrons, liners, cones, and nozzles proving measurable fuel, noise, and durability gains. Tightening ICAO/FAA noise and emissions rules, plus airline sustainability targets, force retrofit and line-fit upgrades. Record narrowbody backlogs and a bulge in engine shop visits amplify spares, repairs, and rotable demands. Additive manufacturing and advanced superalloys/CMCs reduce weight and lead times, improving cost of ownership. Risk-sharing with OEMs ensures multi-year volumes, while localized supply chains and DER repair capability compress turnaround times.

LIST OF KEY AIRCRAFT EXHAUST SYSTEM COMPANIES PROFILED

- Doncasters (U.K.)

- Ducommun (U.S.)

- Hellenic Aerospace Industry (Greece)

- ITP Aero (Spain)

- Magellan Aerospace (Canada)

- Nexcelle (U.S.)

- Nicrocraft (U.S.)

- NORDAM (U.S.)

- Safran (France)

- Senior Aerospace (U.K.)

KEY INDUSTRY DEVELOPMENTS

- July 2025 - ST Engineering’s Middle River Aerostructure Systems (MRAS) has been selected by JetZero to design and manufacture the exhaust nozzle for JetZero’s full-scale, all-wing demonstrator aimed at sharply reducing fuel burn and carbon emissions. Working with JetZero and propulsion partners, MRAS will bring engineering, design, and production expertise to a component central to the aircraft’s propulsion and overall performance.

- June 2025 - Safran Electronics & Defense and Babcock International Group announced plans to expand their partnership across multiple domains, including mission systems, aircraft engines, space systems, and tactical and strategic communications. This move aims to strengthen joint offerings and accelerate capability development across defense programs where both companies already work closely.

- October 2024 - ST Engineering said its Commercial Aerospace unit has signed a 15-year, exclusive maintenance, repair and overhaul agreement with Akasa Air to service LEAP-1B engines powering the airline’s Boeing 737 MAX fleet. The long-term pact makes ST Engineering Akasa’s sole engine MRO provider, supporting the fast-growing Indian carrier’s expansion.

- April 2021 - Barnes Aerospace, a unit of Barnes Group Inc. (NYSE: B), said it has secured a multi-year contract from Northrop Grumman to produce a major metallic subassembly for the B-2 Spirit Tailpipe Mid/Aft Assembly Full Fleet Replacement Program. Production will take place at Barnes Aerospace’s Ogden, Utah site, noted for precision exotic metal forming and complex assemblies, extending the companies’ long-standing partnership.

REPORT COVERAGE

The report on the aircraft exhaust system market offers a deep dive into the space, profiling leading companies, key product segments, and primary applications. It also maps current trends and notable developments. Together, these insights explain the factors that have fueled the market’s rapid growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.01% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Aircraft Type · Commercial · Regional Jets · Business Aviation · Military Fixed-Wing · Helicopters (Civil & Military) · General Aviation (Piston/Turboprop) |

|

By Engine Type · Turbofan · Turboshaft (Helicopter) · Turboprop · Piston (GA) |

|

|

By System · Engine Exhaust System · Auxiliary Power Unit (APU) Exhaust System |

|

|

By Application · Civil/Commercial · Military |

|

|

By End User · Aftermarket · OEM |

|

|

By Region · North America (By Aircraft Type, Engine Type, System, Application, and End User) o U.S. (By End User) o Canada (By End User) · Europe (By Aircraft Type, Engine Type, System, Application, and End User) o U.K. (By End User) o Germany (By End User) o France (By End User) o Russia (By End User) o Rest of Europe (By End User) · Asia Pacific (By Aircraft Type, Engine Type, System, Application, and End User) o China (By End User) o Japan (By End User) o India (By End User) o Rest of Asia Pacific (By End User) · Rest of the World (By Aircraft Type, Engine Type, System, Application, and End User) o Middle East and Africa (By End User) o Latin America (By End User) |

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 1.14 billion in 2025 and is estimated to reach USD 2.1 billion by 2034.

The market is growing at a CAGR of 7.01% during the projection period (2026-2034).

The turbofan segment is estimated to be the leading segment in this market during the forecast period.

The commercial segment is estimated to be the leading segment in this market during the forecast period.

Doncasters (U.K.), Ducommun (U.S.), Hellenic Aerospace Industry (Greece), ITP Aero (Spain), Magellan Aerospace (Canada) are some of the leading OEMs in the market.

Asia Pacific is projected to be the largest shareholder in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us