Aircraft Gearbox Market Size, Share & Industry Analysis, By Component (Gear, Housing, Bearing, and Others), By Platform (Commercial, Civil, and Military), By Gearbox Type (Accessory Gearboxes, Reduction Gearboxes, Actuation Gearboxes, Tail Rotor Gearboxes, Auxiliary Power Unit (APU) Gearboxes, and Others), By End-User (OEM, MRO, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

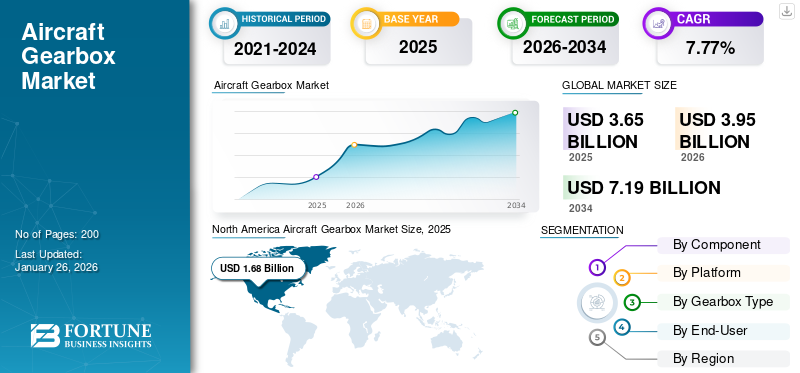

The aircraft gearbox market size was valued at USD 3.65 billion in 2025 and is projected to grow from USD 3.95 billion in 2026 to USD 7.19 billion by 2034, exhibiting a CAGR of 7.77%. North America dominated the aircraft gearbox market with a market share of 45.92% in 2025.

An aircraft gearbox is a mechanical device that transmits power from the aircraft engine to the propeller or rotor, adjusting rotational speed and increasing torque. It is a critical part of the aircraft's drivetrain, ensuring efficient and reliable power transmission propulsion systems. These gearboxes convert the high rotational speed of the engine to the lower speed required by the propeller or rotor, optimizing performance and thrust generation. They are designed to withstand demanding operating conditions, including high loads, vibrations, and temperature variations, and are made from high-strength materials such as steel and titanium alloys. The gearbox housing is often made of lightweight materials such as aluminum or magnesium alloys to reduce overall weight and improve aircraft performance.

Aircraft gearboxes come in several types, each with distinct roles. Reduction gearboxes adjust engine speed for propellers or rotors, while accessory gearboxes power auxiliary systems such as fuel pumps. Actuation gearboxes manage control surface movements, and tail rotor gearboxes in helicopters handle directional control. Modern gearboxes use advanced techniques such as finite element analysis and computational fluid dynamics to optimize their design. Precision machining and heat treatment enhance their quality and durability, and they feature lubrication and cooling systems to minimize friction and manage heat.

The COVID-19 pandemic negatively affected the aviation gearbox market due to its broader effects on the aviation sector. Reduced air passenger traffic led to a decline in aircraft demand and gearbox production, causing financial losses for market players. Aviation gearbox manufacturers faced operational issues due to supply chain disruptions and restricted site access, forcing many businesses to shut down their factories.

Download Free sample to learn more about this report.

GLOBAL AIRCRAFT GEARBOX MARKET OVERVIEW

Market Size & Forecast:

- 2025 Market Size: USD 3.65 billion

- 2026 Market Size: USD 3.95 billion

- 2034 Forecast Market Size: USD 7.19 billion

- CAGR: 7.77% from 2026–2034

Market Share:

- North America led the aircraft gearbox market with a 45.92% share in 2025, driven by the presence of major OEMs like Boeing, GE, and Pratt & Whitney, alongside robust defense spending and R&D investment.

- By component, the gear segment dominated in 2024 due to its critical role in power transmission, torque control, and engine optimization.

- By platform, the commercial aviation segment held the largest share in 2024, fueled by growing passenger traffic and global fleet expansion.

- By gearbox type, accessory gearboxes led the market as airline fleet expansion drove the need for auxiliary system support and engine compatibility.

- By end-user, OEMs accounted for the highest share, supported by integration of cutting-edge technology and long-term supply chain partnerships with aircraft manufacturers.

Key Country Highlights:

- United States: Strong demand driven by modernization of military aircraft and large commercial fleet. The U.S. Department of the Air Force requested USD 217.5 billion for FY2025, including USD 66.7 billion for procurement and R&D.

- Canada: A robust MRO ecosystem and presence of key suppliers such as Safran and Liebherr strengthen the regional supply chain.

- Germany: Aerospace investments and the presence of OEM suppliers like Liebherr-Aerospace continue to propel innovation in gearbox materials and designs.

- United Kingdom: Rolls-Royce focuses on high-performance gearbox systems for turboprop and regional jets, supporting the UK’s strong A&D sector.

- France: Safran continues to lead with development of lightweight and efficient gearboxes for next-gen aircraft, especially geared turbofans.

- China & India: Rapid fleet expansion, indigenous aircraft development (like COMAC C919 and HAL Tejas), and growing MRO demand drive gearbox adoption.

- Middle East: Growth driven by aircraft deliveries, airport expansion, and rising MRO demand, particularly in UAE and Saudi Arabia.

- Brazil & Mexico: Recovery in civil aviation and MRO investments support steady market growth across Latin America.

MARKET DYNAMICS

Market Drivers

Rising Demand for Lightweight Aircraft Components to Boost Aircraft Gearbox Market Growth

The growing demand for lightweight aircraft components significantly drives the aircraft gearbox market, stimulating the need for innovative solutions that contribute to overall weight reduction in aircraft. This demand is primarily influenced by the aviation industry's focus on enhancing fuel efficiency and reducing operational costs, prompting manufacturers to prioritize developing lightweight gearbox systems that can effectively support weight-saving initiatives. Lighter aircraft components contribute to improved performance, increased payload capacity, and enhanced maneuverability, thereby fostering the demand for advanced gearbox technologies that align with the industry's pursuit of more efficient and agile aviation solutions.

The industry is witnessing a strong inclination toward utilizing lightweight gearbox materials, such as advanced composites and alloys, to improve overall aircraft performance. The growing emphasis on lightweight, durable, and high-precision gears to enhance overall aircraft efficiency and reduce maintenance requirements has fueled the demand for innovative gear technologies. Advancements in gear manufacturing techniques, such as additive manufacturing and next-generations materials, have further facilitated the production of complex and specialized gears capable of meeting the stringent requirements of modern aircraft.

Market Restraints

Stringent Regulations within Aerospace Industry to Restrict Market Expansion

Stringent regulations in the aerospace industry mandate rigorous design, testing, and certification processes for gearboxes, which can impede the growth of the market. Adherence to strict safety standards is crucial, given the critical role these components play in aircraft safety. However, these regulations raise costs and extend development timelines, posing challenges for manufacturers.

The high costs associated with developing aviation gearboxes can act as a barrier to new market entrants, which limits competition and innovation. Extensive testing and certification required to meet regulatory standards raise costs further. The costly development of gearboxes stands as a significant restraint on the growth of the market due to the design, research, and manufacturing processes required to create advanced and reliable gearboxes.

The market is influenced by technological, economic, and regulatory factors. For aircraft component safety and airworthiness, the aviation sector has strict standards and certification requirements. As a result, manufacturers must prioritize comprehensive gearbox system testing and comply with worldwide aviation standards to guarantee gearbox dependability and regulatory compliance.

Market Opportunities

Increased Investments in Geared Turbofan Engines Offers Major Growth Opportunities for Market Players

Increased investment in geared turbofan engines presents significant opportunities for the market. Geared turbofan engines are known for their fuel efficiency and reduced emissions. These engines rely heavily on high-performance, lightweight, and durable gearboxes to drive their innovative design. As demand for these engines rises, the aviation gearbox market will benefit from a growing need for advanced, technologically sophisticated, and specialized gear systems.

The geared turbofan can significantly reduce Nitrogen Oxides (NOx) emissions and micro-particulate pollution by lowering fuel consumption. As a result, more airlines are shifting to these engines, boosting gearbox production & sales. The increasing adoption of geared turbofans ensures precise functioning and power transmission across diverse aircraft components. This surge in investment can drive research and development activities, fostering innovation and encouraging manufacturers to produce more efficient and reliable gearbox solutions.

AIRCRAFT GEARBOX MARKET TRENDS

Adoption of Advance Materials to Enhance Gearbox Performance Boosts Market Growth

A significant trend in the market is the adoption of advanced materials to enhance performance, extend lifespan, and reduce weight. These materials offer superior properties compared to traditional materials, enabling the production of more efficient and reliable gearboxes.

Ceramics are gaining traction due to their exceptional hardness, thermal stability, and corrosion resistance. Their hardness provides wear resistance crucial for gears facing constant friction. Their thermal stability ensures reliable function in high-temperature environments while their corrosion resistance makes them suitable for challenging chemical conditions, offering an advantage over many metals. For example, KYOCERA Corporation has found that fine ceramics exhibit approximately 90% less abrasion compared to stainless steel.

Lightweight materials such as titanium alloys and composites are also becoming increasingly common in gearbox manufacturing. These materials contribute to reducing the overall weight of the aircraft, which improves fuel efficiency and lowers emissions. The growing demand for lightweight aircraft components is a significant driver for the market, stimulating the need for innovative gearbox solutions. This demand is influenced by the aviation industry's continuous efforts to enhance fuel efficiency and reduce operational costs, prompting manufacturers to prioritize the development of lightweight gearbox systems.

- North America witnessed a growth from USD 1246.46 million in 2023 to USD 1545.82 million in 2024.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Component

Gear Segment Dominates Owing to its Crucial Role in Power Transmission and Engine Optimization

By component, the market is classified into gear, housing, bearing, and others.

The gear segment dominated the market in 2026 with a share of 38.38% and is likely to be the fastest-growing segment from 2026-2034. Gears ensure proper rotation and torque transfer between the engine and propeller/rotor, meeting stringent safety and reliability standards. The growth of the segment is attributed to its application in a power transmission system, which enhances fuel efficiency and engine optimization.

The housing segment is anticipated to display significant growth during the study period. The growth is driven by the demand for lighter and more durable materials. Innovations in material science have enabled the development of gear housings that contribute to overall weight reduction and increased longevity of aviation gearboxes.

By Platform

Robust Expansion in Commercial Aviation Boosted Commercial Segment Growth

The market is segmented into commercial, civil, and military, based on platform.

The commercial segment dominated the global aircraft gearbox market share in 2024 and is likely to be the fastest-growing segment from 2025-2032. The growth is propelled by significant expansion in commercial aviation due to rising global travel demand and increasing airline fleet sizes. The surge in passenger traffic is expected to further contribute to the growth of the commercial aircraft market. The FAA reported 850 million passengers in the U.S. in 2023, highlighting the growing demand for air travel. The segment is expected to dominate the market with a share of 43.36% in 2026.

The military segment is anticipated to witness significant growth during the study period. Geopolitical tensions and the need for advanced defense capabilities are driving increased defense spending by various countries, which, in turn, fuels demand for military aircraft such as fighter jets, transport planes, and helicopters. These aircraft require robust gearboxes that can withstand rigorous operational conditions and ensure mission success and safety. The segment is likely to record a CAGR of 7.20% during the forecast period (2025-2032).

- The Civil segment is expected to hold a 26.13% share in 2024.

To know how our report can help streamline your business, Speak to Analyst

By Gearbox Type

Expansion of Aircraft Fleet Encouraged Accessory Gearbox Segment Growth

By gearbox type, the segment is categorized into accessory gearboxes, reduction gearboxes, actuation gearboxes, tail rotor gearboxes, Auxiliary Power Unit (APU) gearboxes, and others.

The accessory gearbox segment is expected to dominate the global aircraft gearbox market with a share of 25.12% in 2026. Airlines are expanding their fleets to accommodate more passengers and replace older aircraft with more fuel-efficient models, directly increasing the demand for new and advanced airplane gearboxes. The segment is anticipated to capture 25% of the market share in 2025.

The reduction gearbox segment is anticipated to display moderate growth during the study period. Reduction gearboxes adjust engine output to optimal propeller speeds, which is crucial for maintaining aircraft efficiency and performance. Furthermore, innovations in gearbox technology, such as lighter materials and resilient designs, improve the durability and reliability of these components, extending their service life and reducing maintenance costs. The segment is expected to grow with a CAGR of 7.69% during the forecast period.

By End-User

OEM are the Leading End-users due to Technical Advancements in Aircraft Gearbox

By end-user, the market is categorized into OEM, MRO, and others.

The OEM segment dominated the market with a share of 43.85% in 2025. OEMs have established relationships with aircraft manufacturers and airlines, securing their position in the supply chain. OEMs are at the forefront of integrating the latest technologies into aircraft gearboxes, driving demand for their products. The segment is poised to gain 44% of the market share in 2025.

The MRO segment is projected to grow significantly during the forecast period. As the global fleet ages, the MRO market for gearboxes becomes increasingly important, fueling demand for gearbox replacements and upgrades. The increasing need for maintenance, repair, and overhaul services drives demand for replacement gearboxes and spare parts. The segment is anticipated to document a considerable CAGR of 7.32% during the forecast period (2025-2032).

AIRCRAFT GEARBOX REGIONAL OUTLOOK

Geographically, the market is segmented into North America, Europe, Asia Pacific, and the rest of the world.

North America Aircraft Gearbox Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America contributed approximately USD 1.68 billion to the global market in 2025, accounting for 45.92% share, and is expected to reach USD 1.82 billion in 2026. This growth is attributed to the presence of leading aerospace manufacturers and suppliers, such as Boeing and General Electric, and continuous investment in research and development. North America's technologically advanced aerospace industry emphasizes innovation and performance, leading to frequent upgrades and replacements of gearbox components. Additionally, the region's robust military aviation sector and established aviation regulations and safety standards, further contributes to market growth.

U.S.

The U.S. military's focus on modernizing its aircraft fleet fuels the aircraft gearbox market growth. The market witnesses increased defense budgets for developing and maintaining military aircraft, which require sophisticated gearbox systems. In fiscal year 2025, the Department of the Air Force requested USD 217.5 billion, marking a 1.1% increase from the previous year. This includes USD 29 billion for procurement and USD 37.7 billion for Research, Development, Testing, and Evaluation (RDT&E) to advance technologies such as Next-Generation Air Dominance systems and Collaborative Combat Aircraft (CCA). The U.S. market is set to be valued at USD 1.33 billion in 2026.

Europe

In 2025, the Europe market stood at USD 0.8 billion, representing 21.98% of global demand, and is projected to grow to USD 0.87 billion in 2026. Europe is anticipated to hold a significant market share in 2025, driven by substantial investments in R&D from leading aerospace companies aiming to enhance fuel efficiency and reduce carbon emissions. The U.K. market continues to expand, set to reach a market value of USD 0.28 billion in 2026. The region benefits from strong governmental support and collaborations between key industry players and research institutions. Germany is expected to hold USD 0.25 billion in 2026, while France is foreseen to gain USD 0.15 billion in the 2025.

Asia Pacific

The Asia Pacific region captured 17.11% of the global market in 2025, generating USD 0.63 billion in revenue, and is projected to reach USD 0.68 billion in 2026. Asia Pacific is expected to experience the fastest growth rate in the market. The rapid expansion of the region’s aircraft gearbox market is driven by increasing air traffic and the expansion of civil aircraft fleets in China and India. The Chinese market is set to be worth USD 0.22 billion in 2026. This presents a significant opportunity for local players to invest in the aerospace industry. As the region’s aviation industry matures, demand for high-performance and reliable gearboxes is expected to drive technological advancements. India is likely to reach USD 0.18 billion in 2026, while Japan is expected to gain USD 0.13 billion in the same year.

Middle East & Africa

The Middle East & Africa are witnessing modest growth, driven by expanding aviation sectors, increased aircraft deliveries and economic diversification efforts. Development of new airports and the increase in luxury and business travel are key growth factors in these regions.

Latin America

Latin America is witnessing steady growth driven by the gradual recovery of the aviation industry, particularly in Brazil and Mexico. These countries are focusing on enhancing their aircraft maintenance and overhaul capabilities, further supporting market expansion.

Rest of the World

In 2025, Rest of the World represented USD 0.55 billion, accounting for 14.99% of the worldwide market, and is projected to grow to USD 0.58 billion in 2026.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Leading Players are Focusing on Technological Advancements, Product Innovation, and Strategic Partnerships to Gain Strong Foothold

Key players are concentrating on technological advancements, product innovation, and strategic partnerships to reinforce their market positions and meet the changing needs of the aviation industry. These companies are actively participating in product portfolio expansion, research and development activities, and strategic collaborations to broaden their market reach and fulfill the evolving needs of airlines and aircraft manufacturers. Few leading players in the market include Safran, Liebherr, United Technologies Corporation (UTC), Rexnord Aerospace, and Triumph Group.

List of Key Aircraft Gearbox Companies Profiled

- Safran (France)

- Liebherr (Switzerland)

- United Technologies Corporation (UTC) (U.S.)

- Rexnord Aerospace (U.S.)

- Triumph Group (U.S.)

- Aero Gear (U.S.)

- CEF Industries Inc. (U.S.)

- The Timken Company (U.S.)

- AAR Corp (U.S.)

- Rolls-Royce plc (U.K.)

- Regal Rexnord (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2025 – Bell Boeing received a USD 46 million contract for the V-22 Gearbox Vibration Monitoring System. This contract includes non-recurring engineering for the integration and supportability of a V-22 Gearbox Vibration Monitoring/Osprey Drive System Safety and Health Information (ODSSHI) system. Additionally, it covers the acquisition of up to 91 ODSSHI kits along with associated spare parts.

- August 2023 – Leonardo revealed AW09 single-engine helicopter agreements and partnership at Heli-Expo 2023. The alliance between the two firms seeks to aid the launch and establishment of the AW09 in the U.S.

- May 2023 – Triumph Group, Inc., declared that its Geared Solutions division received a long-term contract from General Electric (GE) for the Inlet Gearboxes (IGB) used in the LEAP-1A, LEAP-1B, and LEAP-1C initiatives. This task was executed at the TRIUMPH Geared Solutions plant located in Macomb, Michigan.

- February 2023 – Airbus Helicopters introduced an upgraded main gearbox for the H225 helicopter. The new gearbox, known as the eMGB, is designed to elevate safety standards and reduce maintenance workloads. It extends the component's Time Before Overhaul (TBO) from 1,000 hours to 2,000 hours.

- November 2022 – GE Aerospace and Tata Advanced Systems Ltd renewed their long-term agreement valued at USD 1 billion for the manufacturing and supply of commercial aircraft engine components. The engine components were produced at the Tata Centre of Excellence for Aero Engines (Tata-TCoE).

REPORT COVERAGE

The report outlines competitive dynamics by assessing business segments, product offerings, target market earnings, geographical reach, and significant strategic initiatives by leading manufacturers. The global market analysis provides detailed insights of the market. Besides this, the report offers insights into the global market trends. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market in the recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.77% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Component

|

|

By Platform

|

|

|

By Gearbox Type

|

|

|

By End-User

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the global market size was valued at USD 3.65 billion in 2025 and is anticipated to USD 7.19 billion by 2034.

The market is likely to grow at a CAGR of 7.58% during the forecast period (2026-2034).

The top ten leading players in the industry are Liebherr (Switzerland), United Technologies Corporation (UTC) (U.S.), Rexnord Aerospace (U.S.), Triumph Group (U.S.), Aero Gear (U.S.), CEF Industries Inc. (U.S.), The Timken Company (U.S.), AAR Corp (U.S.), Rolls-Royce plc (U.K.), and Regal Rexnord (U.S.)

North America dominated in the market in 2025.

The gear segment will be the fastest-growing component segment in this market during the study period.

Rising demand for lightweight aircraft components is a key factor boosting aircraft gearbox market growth.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us