Allergy Diagnostics Market Size, Share & Industry Analysis By Product Type (Instruments [Immunoassay Analyzers, Luminometers, and Others] and Consumables), By Test Type (In Vivo and In Vitro), By Setting (Laboratory and Point-of-Care), By Allergen Type (Inhaled Allergens, Food Allergens, Drug Allergens, and Others), By End User (Hospitals & Clinics, Clinical Laboratories, and Others), and Regional Forecast, 2026-2034

Allergy Diagnostics Market Size and Future Outlook

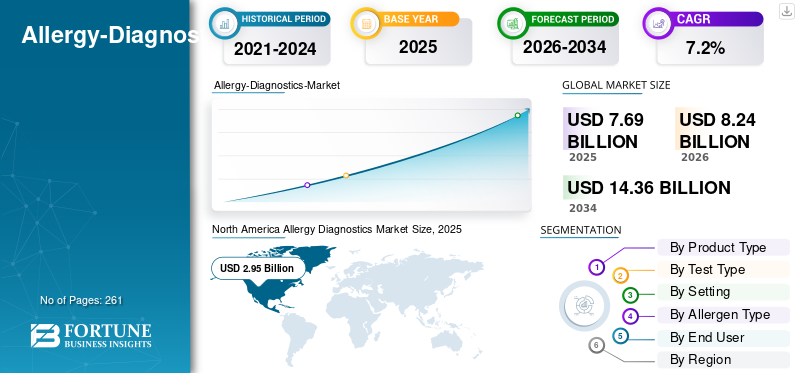

The global allergy diagnostics market size was valued at USD 7.69 billion in 2025 and is projected to grow from USD 8.24 billion in 2026 to USD 14.36 billion by 2034, exhibiting a CAGR of 7.2% during the forecast period. North America dominated the allergy diagnostics market with a market share of 38.36% in 2025.

Allergy diagnostics includes tests or methods used to identify specific allergens that cause an immune system overreaction among the patient population. The increasing prevalence of allergic conditions, growing number of diagnostic tests and the expansion of healthcare infrastructure are resulting in an increasing adoption rate of these devices in the market. The growing awareness about the advantages of these tests is further contributing to the demand for these devices in the market, thereby boosting the adoption rate in the market.

- For instance, according to 2024 statistics published by National Center for Biotechnology Information (NCBI), it was reported that the prevalence of allergic diseases is currently impacting approximately 10%–30% of the global population.

Furthermore, the growing integration of technological advancements in these devices among the major players, such as Thermo Fisher Scientific Inc., Siemens Healthineers AG, among others, is further contributing to the demand for these devices in the market.

Download Free sample to learn more about this report.

Allergy Diagnostics Market Key Takeaways

- 2025 Market Size: USD 7.69 billion

- 2026 Market Size: USD 8.24 billion

- 2034 Forecast Market Size: USD 14.36 billion

- CAGR: 7.2% from 2026–2034

- North America dominated the allergy diagnostics market with a 38.36% share in 2025.

- The instruments segment is expected to grow at a CAGR of 7.0% during the forecast period.

- The point-of-care segment is projected to expand at a CAGR of 7.7% during the forecast period.

North America

North America led the market with a valuation of USD 2.95 billion in 2025.

Europe

Europe is projected to reach USD 2.45 billion in 2026, driven by steady market growth.

Asia Pacific

Asia Pacific is expected to attain a market size of USD 1.89 billion in 2026, ranking as the third-largest regional market.

U.S.

The market is estimated to reach approximately USD 1.18 billion in 2026.

Japan

The market is estimated at around USD 0.39 billion in 2026.

Read More

Allergy Diagnostics Market Trends

Increasing Adoption of In-Vitro Allergy Diagnostics and Automated Testing Devices is a Key Trend

A key trend shaping the global market is the preferential shift toward in-vitro allergy diagnostic tests and automated laboratory devices. The adoption of in-vitro testing devices especially serum-specific IgE testing kits has significantly increased primarily due to their accuracy, improved safety, and compatibility with high-throughput laboratory settings.

Moreover, modern laboratory automation and immunoassay devices have improved the efficiency of allergy testing devices. The instruments including automated immunoassay analyzers and multiplex testing platforms allow laboratories to process huge volumes of patient samples with reduced manual intervention. These advancements also contribute to component-resolved diagnostics (CRD), allowing the identification of specific allergens responsible for allergic reactions.

- According to 2023 statistics published by World Health Organization (WHO), there are over 40,000 products are available today for in vitro diagnostic testing, covering a wide range of disorders.

Market Dynamics

Market Drivers

Download Free sample to learn more about this report.

Increasing Prevalence of Allergic Diseases to Drive Market Growth

The growing prevalence of allergic conditions including eczema, hay fever, and others is resulting in the rising number of diagnostic procedures among the patient population. It is consequently driving the demand for allergy diagnostics in the market.

- For instance, according to 2021 data published by the National Eczema Association (NEA), it was reported that eczema affects approximately 10% to 20% of children and 2% to 10% of adults globally.

This, coupled with growing healthcare awareness and increasing adoption of multiplex allergen testing technologies, is further augmenting the adoption rate of these devices in the market. Therefore, the factors above, along with the growing focus of key players on introducing research and development activities to introduce novel devices, are anticipated to drive the adoption rate of these devices, thereby supporting the global market size.

Market Restraints

High Cost of Advanced Allergy Diagnostic Tests to Hinder Market Growth

The high cost associated with advanced tests and laboratory workflows remains a key restraint for the global market. The modern allergy diagnostic devices including multiplex allergen testing platforms, automated immunoassay analyzers, and Component-Resolved Diagnostics (CRD) require huge capital investment along with ongoing costs associated with consumables, and maintenance services.

Additionally, many advanced allergy diagnostic tests must be conducted in specialized clinical laboratories with trained professional, which further adds to the financial burden. These cost barriers make it challenging for healthcare facilities in developing economies, further hampering the adoption rate of these products in the market.

- For instance, according to the 2025 statistics published by the Premier Allergy TX, the cost of blood test (IgE Test) is about USD 200 – USD 1,000.

Market Opportunities

Growth of Clinical Laboratories in Emerging Nations Create Market Opportunities

There is a rapid expansion of healthcare facilities in developing countries, including Brazil, China, and others. The growing diagnostic volumes, expansion of healthcare infrastructure, increasing number of diagnostic laboratories are subsequently contributing to the adoption of allergy diagnostics in the clinical settings. The governments and private healthcare providers are also expanding laboratory services to improve disease detection and preventive healthcare. It is further boosting the adoption rate of these devices, creating a lucrative opportunity in the market.

- According to 2026 data published by American Clinical Laboratory Association (ACLA), there are approximately 322,488 clinical laboratories in the U.S.

Market Challenges

Limited Healthcare Access in Developing Countries to Limit Market Growth

There is a growing R&D activities for innovative allergy tests among the patient population. However, limited awareness about the benefits of allergy tests, healthcare spending, stringent regulatory laws, shortage of technologically advanced devices, along with inadequate reimbursement framework, especially in developing countries, are resulting in reduced access to healthcare facilities among the patient population.

Furthermore, a limited number of clinical laboratories and limited healthcare professionals, among others, in emerging countries such as China and India are some of the crucial factors, resulting in the limited diagnostic procedures among the patient population.

- For instance, according to 2023 data published by the World Bank Group (WBG), approximately 4.5 billion people lack full access to essential health services globally.

ALLERGY DIAGNOSTICS MARKET SEGMENTATION ANALYSIS

By Product Type

Increasing Product Launches for Consumables Led to Segmental Dominance

Based on the product type, the market is classified into instruments and consumables. Additionally, instruments are further divided into immunoassay analyzers, luminometers, and others.

The consumables segment held the largest revenue share in 2025. The growth is due to the increasing prevalence of allergic disorders among the patient population, resulting in a rising number of allergic procedures globally. This, coupled with the growing focus of key companies on launching innovative devices, is further anticipated to contribute to the global allergy diagnostics market growth.

- For instance, according to 2023 statistics published by the American College of Allergy, Asthma & Immunology, asthma affects more than 24 million people in the U.S.

The instruments segment is expected to grow at a CAGR of 7.0% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Test Type

Growing Number of In-vitro Tests Led to Segmental Dominance

Based on test type, the market is bifurcated into in vivo and in vitro.

The in vitro segment dominated the global market in 2025. By test type, the in vitro segment held the share of 58.8% in 2025. The growth is due to the rising prevalence of allergy disorders, resulting in an increasing number of in vitro diagnostic tests, thereby contributing to the adoption rate of these devices in the market.

- For instance, according to 2021 statistics published by the Pew Charitable Trusts, an estimated 3.3 billion in-vitro diagnostics tests are performed in the U.S. annually.

The segment of in vivo is set to flourish with a growth rate of 7.1% across the forecast period.

By Setting

Growing Number of Lab Developed Tests Led to Dominance of Laboratory Segment

Based on setting, the market is segmented into laboratory and point-of-care.

The laboratory segment dominated the global market in 2025. By setting, the laboratory segment held the share of 78.5% in 2025. The growth is due to the growing demand of lab developed tests, resulting in an increasing number of lab developed tests in these settings globally, thereby contributing to the adoption rate of these devices in the market.

- For instance, according to the 2021 statistics published by the Pew Charitable Trusts, an estimated 12,000 lab facilities use lab developed tests in the U.S.

The segment of point-of-care is set to flourish with a growth rate of 7.7% across the forecast period.

By Allergen Type

Growing Prevalence of Seasonal Allergy Led to Dominance of Inhaled Allergens Segment

Based on allergen type, the market is segmented into inhaled allergens, food allergens, drug allergens, and others.

The inhaled allergens segment dominated the global market in 2025. By application, the inhaled allergens segment held the share of 46.4% in 2025. The growth is driven by the growing prevalence of seasonal allergic disorders due to allergens such as pollen dust mites, resulting in an increasing number of diagnostic procedures globally, thereby contributing to the adoption rate of these devices in the market.

- For instance, according to a 2021 finding published by Centers for Disease Control & Prevention (CDC), nearly 1 in 3 adults reported having a seasonal allergy, eczema or food allergy in the U.S.

The segment of food allergens is set to flourish with a growth rate of 7.6% across the forecast period.

By End User

Increasing Number of Clinical Laboratories Led to Segmental Dominance

Based on end user, the market is segmented into hospitals & clinics, clinical laboratories, and others.

The clinical laboratories segment dominated the market in 2025. The increasing prevalence of allergies, rising number of diagnostic procedures in hospitals, and growing number of hospitals, are some of the crucial factors contributing to the growth of the market segment. Furthermore, the segment is set to hold a 58.0% share in 2026.

- For instance, according to 2026 statistics published by Byte Scraper, it was reported that there are 1,131 medical laboratories in Australia.

In addition, hospitals & clinics end users are projected to grow at a 7.0% CAGR during the forecast period.

Allergy Diagnostics Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Allergy Diagnostics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2024, valued at USD 2.77 billion, and also took the leading share in 2025 with USD 2.95 billion. The growing prevalence of allergic disorders such as asthma, food and drug allergies, high number of diagnostic laboratories, and advanced healthcare infrastructure, are some of the factors supporting the growth of the segment in the market.

- For instance, according to 2026 statistics published by the American College of Allergy, Asthma & Immunology, the prevalence of food allergy is estimated to be around 4% of children and 1% of adults globally.

U.S. Allergy Diagnostics Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1.18 billion in 2026, accounting for roughly 37.6% of global sales.

Europe

Europe is projected to record a growth rate of 5.6% in the coming years, which is the second fastest growing among all regions, and reach a valuation of USD 2.45 billion by 2026. The growing air pollution, rising in vitro and vivo tests among patients, and significant adoption of diagnostic technologies are anticipated to support the market growth.

U.K. Allergy Diagnostics Market

The U.K. market in 2026 is estimated at around USD 0.29 billion, representing roughly 3.5% of global revenues.

Germany Allergy Diagnostics Market

Germany’s market is projected to reach approximately USD 0.39 billion in 2026, equivalent to around 4.8% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 1.89 billion in 2026 and secure the position of the third-largest region in the market. The fastest growth in diagnostic procedures, expanding healthcare expenditure, and improving healthcare access, is mostly to support the growth of the market. In the region, India is estimated to reach USD 0.31 billion in 2026.

Japan Allergy Diagnostics Market

The Japan market in 2026 is estimated at around USD 0.39 billion, accounting for roughly 4.8% of global revenues. Japan has historically reported a relatively high prevalence of allergy diseases, with a large number of diagnostic volumes.

China Allergy Diagnostics Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.63 billion, representing roughly 7.7% of global sales.

India Allergy Diagnostics Market

The Indian market size in 2026 is estimated at around USD 0.31 billion, accounting for roughly 3.8% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.43 billion in 2026. The growth is due to the gradual growth tied to healthcare investment and medical tourism hubs in the region. The Middle East & Africa is also expected to grow due to growing healthcare access and rising product launches in the region. In the Middle East & Africa, the GCC is set to reach a value of USD 0.12 billion in 2026.

South Africa Allergy Diagnostics Market

The South Africa market is projected to reach around USD 0.06 billion in 2026, representing roughly 0.8% of global revenues.

Competitive Landscape

Key Industry Players

Increasing Number of Product Launches to Support Dominance of Key Companies

The companies operating in the allergy diagnostic market is experiencing significant growth globally owing to rising number of product launches further contributing to the dominance of these companies in the market. Thermo Fisher Scientific, Inc. and Siemens Healthineers AG, are major companies in the market in 2025. Furthermore, the growing emphasis of key companies on the establishment of diagnostic laboratories is expected to strengthen their presence is mostly to support the global allergy diagnostics market share.

- For instance, in March 2026, Thermo Fisher Scientific Inc., established a new 8,000-square-meter distribution and labeling centre supporting its immunodiagnostics business in Uppsala.

Other key players, including Canon Medical Systems Corporation and others, are also growing in the market, primarily due to their growing focus on collaborations among other companies to strengthen their presence in the market.

List of Key Allergy Diagnostics Companies Profiled

- Thermo Fisher Scientific Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Canon Medical Systems Corporation (Japan)

- Lincoln Diagnostics (U.S.)

- ALK (Denmark)

- Omega Diagnostics Ltd (U.K.)

- Stallergenes Greer (Switzerland)

- HYCOR Biomedical (U.S.)

- EUROIMMUN Medizinische Labordiagnostika AG (Germany)

- Danaher Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Reacta Healthcare which develops specialist products used in food allergy clinical trials expanded into a new facility with an aim to increase its brand presence in the U.S.

- September 2025: Siemens Healthineers AG added nine new component allergens to its 3gAllergy assay portfolio, including six targeting peanut proteins, a leading cause of fatal food-related anaphylaxis with an aim to strengthen its product channel

- August 2025: Mayo Clinic researchers are developing an artificial intelligence-powered tool designed to automate skin allergy patch testing, enabling patients to self-administer tests and use smartphone cameras to monitor reactions over time.

- July 2025: InBio and Beckman Coulter Life Sciences collaborated to enhance the performance of Basophil Activation Tests (BAT) for food allergy research to integrate InBio’s Food Protein Standards and purified allergens with the Next-Generation BAT platform from Beckman Coulter Life Sciences.

- April 2025: Inamdar Multispecialty Hospital launched a state-of-the-art Allergy Department, aimed at providing early diagnosis, evidence-based treatment and comprehensive patient education for a wide range of allergic disorders among the patient population.

- April 2025: Beckman Coulter Life Sciences, a global player in laboratory automation and innovation, introduces the Next-Generation BAT for research use only to more effectively characterize food allergies without exposure to potentially harmful allergens.

- May 2023: Thermo Fisher Scientific, Inc., expanded the access for ImmunoCAP Specific IgE tests to more patients across the U.S.

REPORT COVERAGE

The report provides a detailed global allergy diagnostics market analysis and focuses on key aspects such as leading companies and market segmentation, including product type, test type, setting, allergen type, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Test Type, Setting, Allergen Type, End User, and Region |

| By Product Type |

|

| By Test Type |

|

| By Setting |

|

| By Allergen Type |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 7.69 billion in 2025 and is projected to reach USD 14.36 billion by 2034.

In 2025, the market value stood at USD 2.95 billion.

Growing at a CAGR of 7.2%, the market will exhibit steady growth over the forecast period.

By product type, the consumables segment is the leading segment in this market.

The introduction of novel allergy diagnostic devices is one of the major factors driving the markets growth.

Thermo Fisher Scientific Inc. and Siemens Healthineers AG are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of allergy conditions, the growing number of diagnostic procedures, among others, are some of the crucial factors anticipated to boost the adoption of these devices globally.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us