Alumina-Based Products Market Size, Share & Industry Analysis, By Type (Flat Alumina Substrates, Alumina EV Parts, and Others), By Application (Electronics & Electrical, Automotive, Industrial & High-Temperature, and Others), and Regional Forecast, 2025-2035

KEY MARKET INSIGHTS

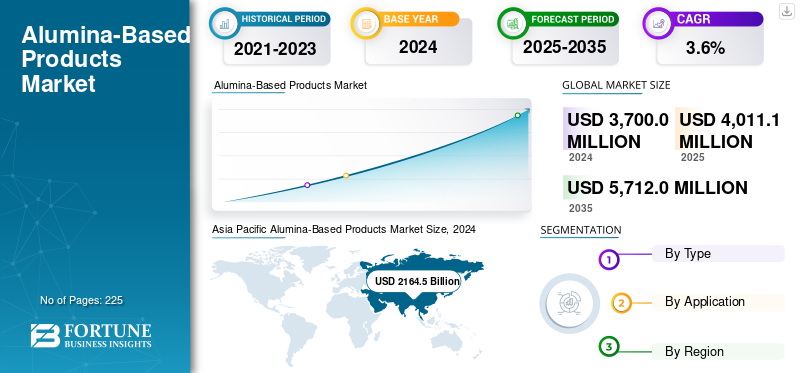

The global alumina-based products market size was valued at USD 3,700.0 million in 2024. The market is projected to grow from USD 4,011.1 million in 2025 to USD 5,712.0 million by 2035, exhibiting a CAGR of 3.6% during the forecast period. Asia Pacific dominated the global alumina-based products market with a market share of 58.5% in 2024.

Alumina-based products are engineered materials composed of high-purity aluminum oxide, renowned for their hardness, thermal stability, chemical inertness, and strong electrical insulation properties. Unlike metallic aluminum used for structural applications, alumina is crucial in ceramic and specialty forms that deliver performance superior to that of metals. These products originate from bauxite refining and advanced processing, producing calcined, tabular, fused, reactive, and high-purity grades. They are essential in refractory linings for steel, cement, and glass industries as they tolerate extreme heat and mechanical stress. Alumina also supports the production of ceramics, abrasives, polishing powders, catalysts, and electronic components. Production involves controlled thermal and chemical treatments that define purity and crystal phases, with higher-grade materials requiring tighter impurity limits, consistent processing, and higher energy input. These factors shape their adoption across high-performance industrial and technological sectors worldwide.

Furthermore, the market has several key players, including Kyocera Corporation, NGK Insulators, CoorsTek, CeramTec Group, and Morgan Advanced Materials, which are at the forefront of the industry. A broad product portfolio, expansion of production capacities, and a strong geographical presence have enabled these companies to maintain their dominance in the global market.

Download Free sample to learn more about this report.

Alumina-Based Products Market Key Takeaways

- 2025 Market Size: USD 3,700.0 million

- 2026 Market Size: USD 4,011.1 million

- 2035 Forecast Market Size: USD 5,712.0 million

- CAGR: 3.6% from 2025-2035

- Asia Pacific dominated the alumina-based products market with a 58.5% share in 2024.

- The flat alumina substrates segment held the largest market share in 2024.

- The electronics and electrical segment accounted for a 25.2% share in 2024.

Asia Pacific

Asia Pacific reached USD 2,164.5 million in 2024 after recording USD 2,041.0 million in 2023.

North America

North America is projected to reach USD 744.5 million in 2025, growing at a CAGR of 3.6%.

Europe

Europe is projected to reach USD 686.6 million in 2025.

U.S.

The market is expected to reach USD 543.4 million in 2025.

Latin America

Latin America is projected to reach USD 134.6 million in 2025.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increasing Use of Alumina Materials in High-Performance Electronics and Advanced Ceramic Components to Push Industry Growth

Alumina materials are widely being used in high-performance electronics and advanced ceramics due to their strong thermal stability, excellent electrical insulation, and reliable mechanical strength. In electronics, high-purity alumina substrates support efficient heat dissipation and stable insulation, making them essential for power modules, semiconductor packaging, LEDs, sensors, and 5G communication devices. Their ability to handle high temperatures and maintain dimensional accuracy improves device reliability. In advanced ceramics, alumina enhances hardness, wear resistance, and chemical durability, enabling its use in components such as seals, cutting tools, sensor housings, and protective parts. With rising demand for compact electronics, growing EV power systems, and expanding industrial applications, the increasing use of alumina materials that improve performance and product lifespan is expected to drive the alumina-based products market growth.

- According to the U.S. Geological Survey (USGS, 2025), the U.S. calcined alumina production reached approximately 810,000 metric tons in 2024, reflecting the scale of domestic alumina refining that supports electronics, ceramics, and high-temperature industrial applications.

MARKET RESTRAINTS

Volatile Bauxite Prices and High Energy Requirements to Restrict Market Growth

The market for alumina-based products is restrained by fluctuations in bauxite prices and the high energy demands of refining and calcination. Variability in bauxite supply, driven by mining disruptions, export policies, and market imbalances, directly impacts production costs and limits pricing stability for manufacturers. At the same time, alumina refining relies heavily on electricity and fuel, resulting in significant expenses during periods of energy price volatility. Stricter environmental regulations on residue management, emissions, and sustainable mining add further compliance costs and operational complexity. These combined factors compress profit margins, hinder smaller producers, and slow capacity expansion, ultimately restricting the overall growth of the market.

MARKET OPPORTUNITIES

Rising Demand for Low-Carbon and Energy-Efficient Alumina Production to Create New Opportunities

Growing interest in low-carbon manufacturing is creating new opportunities for market players. Producers are investing in technologies that reduce energy use, emissions, and waste during refining and calcination. Advances such as high-efficiency burners, heat-recovery systems, improved residue handling, and optimized Bayer-process chemistry help lower operating costs while improving product consistency. These cleaner production methods support the use of high-purity alumina in ceramics, refractories, electronics, and industrial components. As manufacturers and end-users increasingly prefer materials produced with a lower environmental impact, energy-efficient alumina processing offers strong potential for new investment and market expansion.

ALUMINA-BASED PRODUCTS MARKET TRENDS

Rising Demand for Ultrafine and High-Performance Alumina Grades

The market is witnessing a growing demand for ultrafine and high-purity alumina grades as advanced manufacturing expands across various industries, including electronics, ceramics, and high-temperature applications. Producers are focusing on engineered powders with controlled particle size, narrow distributions, and enhanced purity to improve thermal stability, dielectric strength, and mechanical performance. These characteristics are essential for applications such as semiconductor substrates, LED packages, precision ceramics, and specialized refractories. Advancements in calcination, milling, and surface treatment technologies are enabling manufacturers to fine-tune material properties with greater accuracy. This shift toward highly engineered, application-specific alumina reflects a broader movement toward higher-value, performance-driven materials in modern industrial processes.

MARKET CHALLENGES

Insufficient Technological Upgrades May Limit the Production of High-Purity Alumina Grades

The market for alumina-based products faces a key challenge due to limited advancements in refining, calcination, and purification technologies in several major producing regions. Many facilities still operate older Bayer-process units and basic milling systems that restrict the production of ultra-fine, high-purity, and application-specific alumina. This limits control over particle size, morphology, and impurity reduction, making it difficult to meet the strict requirements of advanced electronics, ceramics, and high-temperature applications. As industries demand tighter specifications and consistent quality, the lack of modern processing infrastructure reduces producers’ competitiveness and constrains their ability to scale premium grades effectively.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Flat Alumina Substrates Led the Market Driven by Broad Electronics and Industrial Adoption

Based on form, the market is classified into flat alumina substrates, alumina EV parts, and others.

The flat alumina substrates segment held the dominant alumina-based products market share in 2024, driven by their extensive use in electronics, semiconductors, LED packages, sensors, and power devices. Their high thermal conductivity, excellent electrical insulation, dimensional stability, and resistance to thermal shock make them essential for heat dissipation and circuit reliability. As miniaturization and power density continue to rise across consumer electronics, telecom equipment, and industrial automation, the demand for high-performance alumina substrates remains strong. The segment is expected to retain its leading position throughout the forecast period.

The alumina EV parts segment accounts for a steadily growing share of the market, driven by increasing electric vehicle production and the shift toward thermally stable, corrosion-resistant ceramic components. Alumina is used in battery insulation plates, power module substrates, charging system components, and high-voltage insulators, where safety, heat resistance, and long-term durability are critical. Although smaller than the substrate segment, EV applications are expanding rapidly as OEMs adopt advanced ceramic materials to improve efficiency and reliability in next-generation electric vehicles.

By Application

Electronics & Electrical Segment Leads the Market due to Rising Product Deployment

Based on application, the market is segmented into electronics & electrical, automotive, industrial & high-temperature, and others.

To know how our report can help streamline your business, Speak to Analyst

The electronics and electrical segment holds the dominant share of the alumina-based products industry, driven by the essential use of alumina substrates, insulators, and ceramic components in semiconductors, power electronics, LEDs, sensors, and communication devices. High thermal conductivity, strong electrical insulation, and resistance to heat and corrosion make alumina indispensable for circuit reliability and thermal management. Its role in high-frequency modules, EV power systems, and miniaturized electronic components further strengthens demand. With continuous growth in consumer electronics, 5G infrastructure, industrial automation, and energy-efficient devices, the segment is set to remain the leading consumer of alumina-based materials throughout the forecast period.

The automotive segment continues to witness an increased adoption of alumina-based components, primarily driven by the rapid expansion of electric vehicles. Alumina is widely used in battery insulation plates, power module substrates, charging components, high-voltage insulators, and sensor housings, where thermal stability, lightweight properties, and long-term durability are critical. As EV platforms demand higher power density, improved safety, and enhanced heat dissipation, alumina ceramics offer a reliable performance advantage over metallic alternatives. The increasing adoption of vehicle electrification, growth in power electronics, and stricter thermal safety requirements are expected to drive the steady growth of this segment during the forecast period. Additionally, the segment held a 25.2% share in 2024.

Alumina-Based Products Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Alumina-Based Products Market Size, 2024 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region held the dominant share in 2023, valued at USD 2,041.0 million, and continued to strengthen its position with USD 2,164.5 million in 2024. China leads the market due to its extensive electronics manufacturing base, strong ceramic production capacity, and large alumina refining network. Japan generates significant demand through its advanced semiconductor, LED, and automotive electronics industries, which rely on high-purity alumina substrates and ceramic components. India contributes to the growing consumption of steel, cement, and glass, where alumina-based refractories are essential for high-temperature operations. With the expansion of EV manufacturing, battery technologies, and power electronics production, the region is expected to remain the fastest-growing and the largest consumer of alumina-based products during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is anticipated to experience steady growth in the coming years. During the forecast period, the region is projected to record a growth rate of 3.6%, the second strongest among all regions, and reach a valuation of USD 744.5 million in 2025. In North America, the market demand is supported by well-established electronics, semiconductor, aerospace, and high-temperature industrial sectors. The U.S. leads in consumption due to its large semiconductor and power electronics manufacturing base, which relies heavily on high-purity alumina substrates and ceramic components. Strong demand also comes from the aerospace, defense, and industrial ceramics sectors, where alumina is essential for insulation, durability, and thermal stability. Canada adds stable consumption through its alumina refining, industrial ceramics, and emerging EV supply chain activities. This diversified industrial presence positions North America as an important and steadily expanding market. Backed by these factors, the U.S. is expected to record a valuation of USD 543.4 million, Canada USD 53.9 million, and Mexico USD 147.2 million in 2025.

Europe

The European market is projected to reach USD 686.6 million in 2025 and become the third-largest region. Germany leads consumption, driven by strong demand from electronics, automotive, and advanced ceramics industries. Its semiconductor and power electronics sectors rely on high-purity alumina substrates and ceramic components for heat dissipation and insulation. Europe’s wider aerospace, industrial processing, and refractory industries also contribute to steady demand for alumina grades that offer durability and thermal stability in high-temperature environments. With growing focus on quality, reliability, and application-specific ceramic materials, the region continues to show stable growth. In 2025, the German market is estimated to reach USD 220.3 million.

Latin America

The Latin America market, in 2025, is projected to reach USD 134.6 million. Growth is driven by the region’s expanding ceramics and construction sectors, where alumina-based materials are utilized in tiles, refractories, and engineered ceramic components that require strength and heat resistance. Brazil leads consumption due to large ceramic production bases and rising infrastructure activity. Increasing industrial output in steel, cement, and glass also supports the demand for high-performance alumina products, contributing to steady market expansion across the region.

Middle East and Africa

The Middle East and Africa market is expected to grow at a CAGR of 1.4% during the forecast period. Growth in the GCC is driven by strong demand for alumina-based refractories used in steelmaking, cement production, and petrochemical operations, where high thermal stability and durability are essential. Ongoing investment in industrial infrastructure and advanced material capabilities further supports consumption. The GCC region is projected to reach USD 45.9 million in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Industry Players Emphasize Takeovers and Expansion Initiatives to Enhance their Market Share

Large companies deploy their R&D capabilities, scale, and sustainability efforts to secure an edge over their competitors, whereas regional firms focus on proximity to local infrastructure projects and cost savings. Some of the leading market players include Kyocera Corporation, NGK Insulators, CoorsTek, CeramTec Group, and Morgan Advanced Materials. These players are adopting strategies such as expansion initiatives, acquisitions, and collaborations to gain market share.

LIST OF KEY ALUMINA-BASED PRODUCTS COMPANIES PROFILED

- Kyocera Corporation (Japan)

- Saint-Gobain Ceramics (France)

- Ortech, Incorporated (U.S.)

- NGK Insulators (Japan)

- CoorsTek (U.S.)

- Du-Co Ceramics (U.S.)

- CeramTec Group (Germany)

- Edgetech Industries (U.S.)

- Valley Design Corp. (U.S.)

- Morgan Advanced Materials (U.K.)

KEY INDUSTRY DEVELOPMENTS

- April 2022: Saint-Gobain Ceramics acquired Monofrax, strengthening its portfolio of fused-cast refractories used in glass, steel, and high-temperature industrial applications. The acquisition expands Saint-Gobain’s ability to supply advanced alumina-based materials with enhanced performance and reliability.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2035 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2035 |

|

Historical Period |

2021-2023 |

|

Growth Rate |

CAGR of 3.6% from 2025-2035 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Type, Application, and Region |

|

By Type |

· Flat Alumina Substrates · Alumina EV Parts · Others |

|

By Application |

· Electronics & Electrical · Automotive · Industrial & High-Temperature · Others |

|

By Geography |

· North America (By Type, Application, and Country) o U.S. o Canada o Mexico · Europe (By Type, Application, and Country) o Germany o France o Italy o Rest of Europe · Asia Pacific (By Type, Application, and Country) o China o India o Japan o Rest of Asia Pacific · Latin America (By Type, Application, and Country) o Brazil o Rest of Latin America · Middle East & Africa (By Type, Application, and Country) o GCC o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3,700.0 million in 2024 and is projected to reach USD 5,712.0 million by 2035.

In 2024, the Asia Pacific market value stood at USD 2,164.5 million.

The market is expected to exhibit a CAGR of 3.6% during the forecast period of 2025-2035.

The flat alumina substrates segment led the market by type in 2024.

The key factors driving the market are the growing demand for alumina in electronics, advanced ceramics, and high-temperature industrial applications.

Kyocera Corporation, NGK Insulators, CoorsTek, CeramTec Group, and Morgan Advanced Materials are some of the prominent players in the market.

Asia Pacific dominated the market in 2024.

The increasing demand for high-purity, thermally stable, and mechanically strong alumina materials across various applications, including electronics, advanced ceramics, refractories, and industry, is expected to favor product adoption.

- 2021-2035

- 2024

- 2021-2023

- 225

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us