Aluminum Scrap Market Size, Share & Industry Analysis, By Grade (New and Old), By Application (Automotive, Building & Construction, Packaging, Electrical & Electronics, and Others), and Regional Forecast, 2026-2034

Aluminum Scrap Market Size and Future Outlook

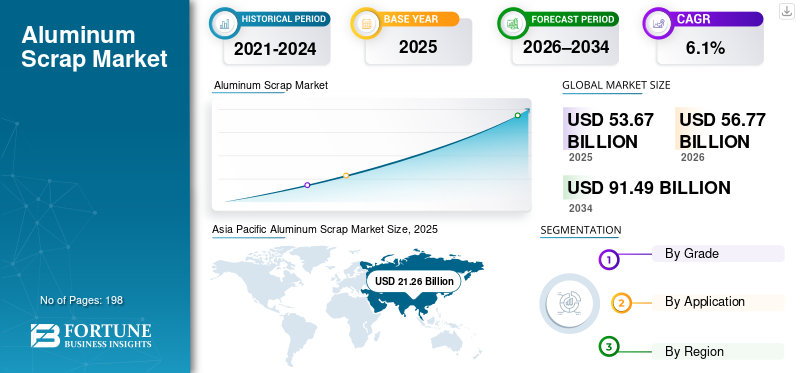

The global aluminum scrap market size was valued at USD 53.67 billion in 2025. The market is projected to grow from USD 56.77 billion in 2026 to USD 91.49 billion by 2034 at a CAGR of 6.1% during the forecast period. Asia Pacific dominated the global aluminum scrap market with a market share of 39.61% in 2025.

Aluminum scrap represents recycled aluminum recovered from manufacturing processes (new scrap) and end-of-life products (old scrap). It serves as the primary feedstock for secondary aluminum production, offering significant energy and carbon savings compared to primary aluminum. As sustainability pressures intensify across metals supply chains, aluminum scrap has shifted from a by-product of manufacturing to a strategic raw material closely linked to circular-economy goals and decarbonization strategies.

Asia Pacific represents the largest regional market by both volume and value, reflecting the concentration of aluminum production, recycling capacity, and downstream manufacturing in China and neighboring economies. Automotive and packaging applications account for the largest share of demand, while secondary aluminum producers and integrated rolling mills serve as the key demand anchors. Major recycling groups, secondary smelters, and integrated aluminum producers dominate the competitive landscape. Novelis Inc., Hydro Aluminium AS, Constellium SE, Arconic Corporation, Real Alloy Holding GmbH, RUSAL, and OmniSource Corporation are the key players operating in the market.

Download Free sample to learn more about this report.

Aluminum Scrap Market Takeaways

- 2025 Market Size: USD 53.67 Billion

- 2026 Market Size: USD 56.77 Billion

- 2034 Forecast Market Size: USD 91.49 Billion

- CAGR: 6.1% from 2026–2034

- Asia Pacific dominated the aluminum scrap market with a 39.61% share in 2025.

- The old scrap segment held the dominant market share and is expected to grow faster as recycling systems mature.

- The automotive segment accounted for the largest market share due to strong demand for recycled aluminum in vehicle manufacturing.

North America

North America remains a mature and high-value market, driven by strong automotive and packaging recycling systems and growing demand for secondary aluminum.

Europe

Europe’s market growth is supported by strict circular economy regulations, high recycling rates, and strong demand from construction and automotive sectors.

Asia Pacific

Asia Pacific led the global market in 2025, supported by China’s extensive aluminum production base, secondary smelting capacity, and favorable recycling policies.

U.S.

The market reached USD 11.24 billion in 2025, accounting for approximately 20.9% of global sales, driven by robust industrial demand.

Japan

The market is expected to benefit from increasing aluminum recycling initiatives, advanced manufacturing activities, and sustainability-focused resource management practices.

Read More

ALUMINUM SCRAP MARKET TRENDS

Shift Toward Higher-Quality Scrap Streams and Closed-Loop Recycling is a Key Market Trend

A key trend shaping the market is the increasing differentiation between scrap grades and the growing importance of quality consistency. Rather than treating aluminum scrap as a uniform commodity, downstream users increasingly distinguish between clean wrought scrap, used beverage cans (UBC), cast scrap, and mixed or contaminated material. Tighter alloy control requirements in automotive, packaging, and advanced manufacturing applications drive this trend.

Closed-loop recycling systems are gaining traction, particularly in automotive and beverage packaging. OEMs and can producers are increasingly recycling their own production scrap and post-consumer material back into the same product streams. This reduces material losses, improves traceability, and supports recycled-content commitments. As a result, value growth in the aluminum scrap market is increasingly tied to grade quality and supply reliability, rather than just tonnage availability.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Secondary Aluminum Production, Driven by Decarbonization Pressure to Boost Market Growth

Aluminum scrap demand is underpinned by the rapid expansion of secondary aluminum production, which consumes significantly less energy and emits lower emissions than primary aluminum smelting. As aluminum producers and downstream users face mounting pressure to reduce carbon footprints, secondary aluminum has become a preferred material choice across multiple industries.

This dynamic directly increases aluminum scrap consumption, particularly in regions with established recycling infrastructure. Automotive, construction, and packaging producers are actively increasing recycled aluminum content in their products, ensuring stable long-term demand for both new and old scrap. The decarbonization imperative therefore, acts as a sustained volume and value driver for the global aluminum scrap market growth.

MARKET RESTRAINTS

Quality Variability and Processing Complexity of Old Scrap to Hinder Market Expansion

Despite strong demand fundamentals, the market faces structural restraints linked to scrap quality variability, particularly for old scrap. Post-consumer aluminum scrap often contains mixed alloys, coatings, and contaminants, which reduce remelt yields and increase processing costs. Advanced sorting and treatment are required to upgrade such material for higher-value applications.

In regions with fragmented collection systems or limited recycling technology, these challenges cap value realization and discourage penetration into premium end uses. While new scrap remains relatively clean and predictable, the higher growth potential of old scrap is partially constrained by processing economics and infrastructure gaps.

MARKET OPPORTUNITIES

Expansion of End-of-Life Aluminum Pool Unlocks Long-Term Growth

A major opportunity for the market lies in the growing stock of aluminum reaching end-of-life, particularly from vehicles, buildings, infrastructure, and consumer goods placed into service over the past two decades. As this installed aluminum base matures, the availability of old scrap is expected to increase structurally over the long term.

This expanding end-of-life pool creates opportunities for recyclers, secondary smelters, and technology providers to capture additional volumes through improved collection, sorting, and alloy separation. Regions with strong recycling policy frameworks and investment in processing capacity are best positioned to capitalize on this opportunity and drive sustained market growth.

MARKET CHALLENGES

Price Volatility and Exposure to Primary Aluminum Cycles are Key Market Challenges

Aluminum scrap prices remain closely linked to primary aluminum pricing, energy costs, and global macroeconomic conditions. This exposes the market to price volatility even when underlying scrap volumes are stable or growing. Sharp swings in aluminum prices can compress recycler margins, disrupt procurement strategies, and delay investment decisions.

In addition, transportation and logistics costs can materially affect delivered scrap prices, especially for international trade flows. These factors create short-term uncertainty about market-value growth and complicate long-term contracting between scrap suppliers and secondary aluminum producers.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade policy and geopolitical considerations increasingly influence aluminum scrap flows. Several producing regions are debating or implementing measures to retain scrap domestically to support local secondary aluminum production and reduce reliance on primary imports. Such policies can disrupt established export channels and alter regional supply-demand balances.

From a structural perspective, these dynamics encourage the regionalization of scrap markets, with downstream consumers prioritizing supply security over lowest-cost sourcing. While this can raise cost-to-serve, it also supports long-term domestic recycling investments and stabilizes demand for locally generated scrap.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D in the aluminum scrap market is increasingly focused on advanced sorting, alloy recognition, and impurity-removal technologies. Sensor-based systems such as LIBS, XRF, and AI-driven optical sorting are being adopted to improve yield and enable higher-value reuse of mixed scrap streams.

These innovations are significant for unlocking greater use of scrap in applications that traditionally rely on primary or clean secondary aluminum. As technology improves, the value gap between new and old scrap is expected to narrow, supporting faster value growth in the old scrap segment.

SEGMENTATION ANALYSIS

By Grade

Old Segment Dominates as Recycling Systems Mature and End-Of-Life Aluminum Availability Increases

Based on grade, the market is segmented into new and old.

The old segment holds the dominant market share, reflecting the growing recovery of aluminum from end-of-life products such as vehicles, buildings, packaging, and appliances. Its share is expected to grow faster over time as recycling systems mature and end-of-life aluminum becomes more available.

New scrap, generated during manufacturing and fabrication, remains critical due to its higher purity and predictable alloy composition. This segment supports value stability and premium pricing, particularly in closed-loop recycling systems. While its volume growth is more closely tied to manufacturing output, new scrap continues to play a key role in supporting high-quality secondary aluminum production.

By Application

To know how our report can help streamline your business, Speak to Analyst

Automotive Leads Market Due to High Aluminum Intensity and Casting Demand

Based on application, the market is segmented into automotive, building & construction, packaging, electrical & electronics, and others.

The automotive segment dominates the market. Aluminum scrap is widely recycled for vehicle components such as body panels, wheels, engine parts, and frames to reduce weight and boost fuel efficiency. Stricter emissions regulations drive this demand. Recycled scrap lowers production costs and supports sustainability in electric vehicle manufacturing.

The building & construction segment is set to register significant growth during the forecast period. This segment drives scrap consumption by using recycled aluminum for windows, doors, facades, roofing, and structural frameworks. Its corrosion resistance and durability make it ideal for long-lasting building applications. Scrap recycling here significantly reduces energy use while meeting construction growth needs.

The packaging segment registers positive growth in the market. Recycled aluminum scrap is used to make beverage cans, foils, food containers, and other lightweight packaging. High recycling rates (especially for cans) stem from their infinite recyclability without quality loss. This application benefits from scrap's cost-effectiveness and environmental compliance in consumer goods.

The others segment consists of aerospace (structural parts), machinery, appliances, and furniture using scrap alloys. Niche uses leverage aluminum's strength-to-weight ratio in defense and equipment. Emerging applications include consumer goods, driven by sustainability mandates.

ALUMINUM SCRAP MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Aluminum Scrap Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for the leading aluminum scrap market share in 2025. The growth is driven by China’s dominant aluminum production base and extensive secondary smelting capacity. The region benefits from scale, integrated supply chains, and increasing policy support for recycling, making it both volume- and value-dominant.

China Aluminum Scrap Market

China’s market is one of the largest globally, with 2025 revenue at USD 10.79 billion, representing roughly 20.1% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America represents a mature, high-value scrap market supported by strong automotive and packaging recycling systems. Policy discussions around domestic scrap retention further reinforce regional demand for secondary aluminum.

U.S. Aluminum Scrap Market

In 2025, the U.S. accounted for a USD 11.24 billion market in North America, driven primarily by strong demand from the industrial sector. The U.S. accounts for roughly 20.9% of global market sales.

Europe

Europe’s market is shaped by stringent circular economy regulations and high recycling rates. Demand is anchored in the automotive, construction, and packaging sectors, with a strong emphasis on sustainability compliance.

Germany Aluminum Scrap Market

The Germany market in 2025 was valued at USD 3.39 billion, representing roughly 6.3% of global market revenues.

U.K. Aluminum Scrap Market

The U.K. market in 2025 was valued at USD 1.30 billion, representing roughly 2.4% of global market revenues.

Latin America

Latin America remains a smaller but growing market, supported by construction activity, beverage can recycling, and automotive industry supply chains, particularly in Brazil and Mexico.

Middle East & Africa

The Middle East & Africa market is comparatively limited in volume but linked to industrial hubs, construction activity, and selective secondary aluminum production. Growth is expected to track infrastructure development and recycling investments.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Leading Players Emphasize Boosting Manufacturing Efficiency to Maintain Their Dominance

The market is seeing strong capital investment as producers respond to rising pressure for sustainable, high-performance solutions. Industry leaders such as Novelis Inc., Hydro Aluminium AS, Constellium SE, Arconic Corporation, Real Alloy Holding GmbH, RUSAL, and OmniSource Corporation are prioritizing manufacturing efficiency, product refinement, and eco-friendly production methods. Ongoing innovation focuses on improving purity standards, minimizing environmental impact, and developing specialized grades tailored for advanced applications.

LIST OF KEY ALUMINUM SCRAP COMPANIES PROFILED

- Novelis Inc. (U.S.)

- Hydro Aluminium AS (Norway)

- Constellium SE (France)

- Arconic Corporation (U.S.)

- Real Alloy Holding GmbH (Germany)

- RUSAL (Russia)

- OmniSource Corporation (U.S.)

- Sims Metal Management (Australia)

- Century Aluminum Company (U.S.)

- Kaiser Aluminum (U.S.)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Novelis Inc. announced a partnership with a DRT Holdings, LLC (DRT) to develop an energy-efficient aluminum recycling process. The initiative aims to significantly reduce energy consumption across its recycling operations. This move strengthens Novelis’s leadership position in sustainable aluminum It also improves operational efficiency while aligning the company with rising demand for low-carbon and environmentally responsible solutions.

- July 2025: Hindalco Industries Limited launched a new initiative to strengthen circular economy practices in the aluminum sector. The program focuses on collaborating with local communities and businesses to improve recycling and reduce aluminum waste. This initiative reinforces Hindalco’s positioning as a sustainability-focused aluminum producer. It also enhances stakeholder engagement by aligning environmental goals with community participation and long-term resource efficiency.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, grade, and application. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report also covers several factors contributing to market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion), Volume (Kiloton) |

|

Growth Rate |

CAGR of 6.1% from 2026 to 2034 |

|

Segmentation |

By Grade, By Application, By Region |

|

By Grade |

· New · Old |

|

By Application |

· Automotive · Building & Construction · Packaging · Electrical & Electronics · Others |

|

By Region |

· North America (By Grade, By Application, By Country) o U.S. (By Application) o Canada (By Application) · Europe (By Grade, By Application, By Country) o Germany (By Application) o U.K. (By Application) o France (By Application) o Italy (By Application) o Rest of Europe (By Application) · Asia Pacific (By Grade, By Application, By Country) o China (By Application) o India (By Application) o Japan (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Grade, By Application, By Country) o Mexico (By Application) o Brazil (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Grade, By Application, By Country) o GCC (By Application) o South Africa (By Application) o Rest of Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 53.67 billion in 2025 and is projected to reach USD 91.49 billion by 2034.

Recording a CAGR of 6.1%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

By application, the automotive segment leads the market.

Asia Pacific held the highest market share in 2025.

Rising secondary aluminum production, driven by decarbonization pressure, boosts market growth.

- 2021-2034

- 2025

- 2021-2024

- 198

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us