Edge Computing Market Size, Share & Industry Analysis, By Component (Hardware, Application/Software, Edge Cloud Infrastructure, Services, and Network), By Enterprise Type (Small & Medium Enterprises and Large Enterprises), By Application (IoT Applications, Robotics & Automation, Predictive Maintenance, Remote Monitoring, Smart Cities, and Others), By Industry (Manufacturing, Oil & Gas, BFSI, Healthcare, Retail, IT & Telecom, Automotive, and Others), and Regional Forecast, 2026–2034

KEY MARKET INSIGHTS

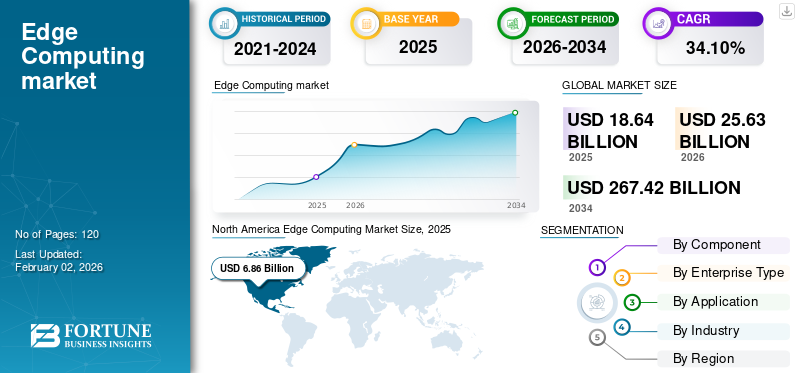

The global edge computing market size was valued at USD 18.64 billion in 2025 and is projected to grow from USD 25.63 billion in 2026 to USD 267.42 billion by 2034, exhibiting a CAGR of 34.10% during the forecast period. North America dominated the edge computing market with a market share of 35.70% in 2025.

Edge computing is a technology of processing and storing data closer to the source to allow rapid and real-time analysis. It is a mesh network of micro data centers processing and storing data locally and pushing all received data to the cloud storage.

- For instance, in July 2024, Armada, a computing company, raised USD 40 million in funding empowered by M12, a Microsoft venture fund to connect edge workloads with hyperscale cloud computing data centers seamlessly and aims to deliver better customer experience.

The global market is set to grow exponentially due to the increased use of edge devices. These devices range from Internet of Things (IoT) devices, such as mobile point-of-sale kiosks, smart cameras, industrial PCs, and medical sensors, to gateways and computing infrastructure for faster and real-time insights into the data source.

- According to industry experts, 75% of data will be created outside central data centers by 2025. Emerging technologies, such as Industry 4.0, artificial intelligence, and IoT, are likely to boost the global market during the forecast period.

The COVID-19 pandemic affected the market growth as well, with edge hardware devices experiencing a decline in production. As trade restrictions were enforced during the early stage of the pandemic, the production of edge chip sets, servers, and other devices were put on hold, affecting the progress of the global market. However, with the rapid adoption of advanced technologies and digitalization, businesses have developed innovative uses of edge devices. Also, with the rising introduction of IoT medical applications proved to be a life-saving technology for the healthcare industry during the COVID-19 outbreak.

Download Free sample to learn more about this report.

EDGE COMPUTING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 18.64 Billion

- 2026 Market Size: USD 25.63 Billion

- 2034 Forecast Market Size: USD 267.42 Billion

- CAGR: 34.10% from 2026–2034

- North America dominated the edge computing market with a 35.70% share in 2025.

- The large enterprises segment is anticipated to hold a 55.79% market share in 2026.

- The hardware segment is projected to lead the market with a 34.26% share in 2026.

North America

North America generated USD 6.86 billion in 2025 and is projected to reach USD 9.15 billion in 2026.

Asia Pacific

Asia Pacific accounted for USD 4.80 billion in 2025 and is expected to reach USD 6.95 billion in 2026.

Europe

Europe was valued at USD 4.10 billion in 2025 and is projected to grow to USD 5.52 billion in 2026.

U.S.

The market is projected to reach USD 4.56 billion by 2026.

Japan

The market is forecast to reach USD 1.82 billion by 2026.

Read More

IMPACT OF GENERATIVE AI

Gen-AI with Computing Solutions Reduced the Latency to Deliver a Better Customer Experience

Generative AI is poised to have a significant impact on the market, reshaping how data is processed, analyzed, and utilized across industries. Generative AI is influencing edge computing factors as follows:

- On-device AI Capabilities:

-

- Generative AI models, such as those used in image synthesis, language models, and other tasks, traditionally required significant computational power often found in cloud-based environments.

- This leads to advancement among edge models to run on smaller and less powerful devices such as cameras, IoT sensors, and smartphones. This centralization allows real-time generative applications without relying on the cloud to improve privacy and data accuracy.

- According to a research survey, integrated gen-AI solutions with computing operations aim to improve the productivity of business operations by 56% to fulfill the growing needs of customers.

- Minimize Latency:

- Integrated Gen AI helps to reduce the latency by data processing using real-time applications, such as augmented reality, gaming, and others.

- Gen-AI-driven control systems can deliver better customer experience by enabling smoother business operations.

Thus, integrated gen-AI with computing solutions leads to driving the market by delivering a better customer experience.

KEY MARKET TRENDS

Rising Introduction of AIoT and Enormous Investments to Bolster Market Growth

Artificial Intelligence of Things (AIoT) has gained immense traction in recent years. From fitness trackers to AR & VR goggles and smart public transit, AI and machine learning are rapidly being used to make IoT devices more secure. With the help of AIoT, networks, and systems are becoming capable of solving problems across industry verticals. The introduction of AI in programs, chipsets, and edge infrastructure can improve analytics and decision-making processes.

Virtual Reality (VR) and Augmented Reality (AR) are being rapidly adopted by both developed and developing economies. Metaverse-based online games, virtual shopping, and smart cities are connecting with digital worlds, enabling consumers to have a virtual experience.

As per industry analysts, global spending on AR/VR was USD 13.8 billion in 2022 and is expected to grow to USD 50.9 billion by 2026. The need for real-time applications on edge networks combined with hybrid-cloud technologies plays a significant role in creating virtual worlds. For instance,

- In September 2023, Lenovo announced the launch of edge AI solutions and services for businesses to fast-track their AI readiness. It enabled users to use the firm’s recent solutions and services through a pay-as-you-go model to deploy the edge technology and gain AI-powered insights straight at the source of data generation.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Key Market Drivers

Surging Need for Edge Infrastructure for 5G Network to Drive Market Growth

Edge-powered SaaS on 5G networks is gaining popularity. Companies across the globe are integrating their services with the cloud, but with increased online reliance on IoT and AI devices, there is heavy data and processing traffic.

As businesses continue to implement artificial intelligence and Internet of Things solutions to analyze progressions and data from their tools, the necessity for low-latency, high-speed wireless connections are growing rapidly. Also, the perspective of 5G and MEC (Multi-access Edge Computing) has progressed substantially. With 5G, users can install these computing applications built on a cloud-driven distributed structure for solutions that require low latency and determined service quality. For instance,

With the rollout of 5G, investments by global companies continue to increase. More than 380 telecom operators are investing in 5G to boost their speed and agility. The edge technology with 5G/6G infrastructure can reduce complexity, save costs, and strengthen cybersecurity defenses. For instance,

- According to the GSMA Mobile Economy Report 2023, there will be 5 billion 5G users by 2030 and more than 50% adoption by 2030. 5G is projected to surpass 4G in 2029. The technology would add approximately USD 1 trillion to the economy globally in 2030, with advantages spread across various industries.

Market Restraint

High Initial Capital Investments Might Restrain Market Growth

The high initial investment can confine the edge computing market growth. The installation and maintenance of edge infrastructure can increase the Capital Expenditure (CAPEX) of many companies. It is hard to construct a complete and robust solution, as investing in edge nodes, devices, and data centers can be quite expensive.

The computing solutions cost varies differently depending on data, scale, expertise, and location. Total costs can depend on the architecture present in place at edge surroundings.

Securing the entire computing network results in huge costs for the providers, thereby restraining market expansion.

Key Market Opportunities

Integration of Industry 4.0 Solutions with Computing Solutions to Enhance Performance of Process Operations

The Industry 4.0 project establishes a structure for updating manufacturing processes in response to industry changes, paving the way for the deployment of edge technologies. Industry 4.0 promotes operational flexibility through the use of technologies that harmonize cyber and physical systems. Smart manufacturing facilities can utilize edge technologies to only send processed data to their cloud servers, which also increases the demand for AI edge computing. The edge acts as a conduit for analyzing data at the local level and then sending summarized data to the cloud. It also used to:

Enhance process excellence: The capacity to make instant decisions, incorporate refined data, and manage intricate data analysis can elevate the standard of industrial operations to unprecedented heights. Equipment and facilities will undergo thorough and precise examination.

Predictive maintenance for better equipment reliability: The exchange of velocity, temperature, and quantity data from a machine offers immediate insights into its condition and efficiency. Should any malfunctions or recurring fluctuations in variables, such as temperature, be identified, the manager can implement proactive strategies to prevent interruptions.

SEGMENTATION ANALYSIS

By Component Analysis

Increased Investment by Hardware Vendors Resulted in Deployment of Hardware Solutions across Several Industries

Based on component, the market is divided into hardware, application/software, edge cloud infrastructure, services, and network.

The hardware segment generated maximum revenue for the market in 2023. Hardware edge vendors are increasing their investments in the market across the globe. For instance, HPE invested around USD 4 billion over four years and is enhancing its already launched computing device, Edgeline Converged Edge Systems. In 2026, the hardware segment is projected to lead the market with a 34.26% share.

The edge cloud infrastructure will grow at the highest CAGR during the forecast period. Deploying edge cloud infrastructure provides a cost-effective and high-performance solution to reduce latency and enhance the customer experience by processing data and services.

In the coming years, the demand for such edge services is expected to increase. Companies, including Intel Corporation and Dell Technologies Inc., are engaging in strategic investments to develop and enhance edge intelligence tools for commercial and industrial IoT. These investments are expected to boost the demand for these tools and their related services globally.

By Enterprise Type Analysis

Large Enterprises to Heavily Adopt Edge Solutions Due to Rising Deployment of IoT-Connected Devices

Based on enterprise type, the market is segmented into small & medium enterprises and large enterprises. The large enterprises segment is predicted to hold the largest market share in the coming years. There has been a rise in the production of IoT-connected devices across the globe. Enterprises require edge solutions to compute the data generated, enable quicker delivery of information, and enhance customer experience. The large enterprises segments is anticipated to hold a dominant market share of 55.79% in 2026. For instance,

- According to a research survey in 2023, global spending on edge computing was estimated to grow by 15.4% from 2023 and reach USD 232 billion in 2024. Thus, to fulfill the performance and scalability requirements, companies aim to adopt the distributed network architecture that computing technologies offer.

A cloud solution might not meet the latency requirements for real-time processing and performing functionalities to keep the data more secure. Computing solutions manages the challenge of increasing data volumes by strategically handling the traffic, which improves the speed of analyzing real-time data. Owing to these advantages, larger enterprises have showcased a higher level of adoption of edge solutions than small & medium-sized enterprises. However, in the mid-term of the forecast period, small enterprises are expected to adopt edge solutions.

By Application Analysis

IoT Applications Leads due to Increased Investments in IoT Projects

Based on application, the market is divided into IoT applications, robotics & automation, predictive maintenance, remote monitoring, smart cities, and others.

IoT applications dominated the market due to their extensive applications. According to Omdia, investments and innovations across IoT projects across the globe are continuously increasing despite economic uncertainties. The IoT applications segment is expected to account for 29.26% of the market in 2026.

Smart cities function effectively by deploying computing-enabled technologies, such as IoT and 5G systems. This technology aids smart cities in comprehending benefits, such as minimizing transmission delays, helping data centralization, and creating better network resilience by empowering IoT and 5G systems to work with better proficiency. Such factors have increased the need for edge solutions in smart cities.

To know how our report can help streamline your business, Speak to Analyst

By Industry Analysis

IT & Telecom Holds Leading Position Due to Increasing Business Complexities

Based on industry, the market is classified into manufacturing, oil & gas, BFSI, healthcare, retail, IT & telecom, automotive, and others. The pandemic changed the daily business operations of many companies, forcing them to shift most of their processes to the cloud. IT & telecom industries have rapidly shifted their business operations to the cloud. The inclination of enterprises toward the cloud has played a vital role in increasing the volume of data generation. The automotive segment will account for 24.19% market share in 2026.

- According to a research analyst survey in 2023, 30% of companies spend their money on IT budgets on enhancing edge cloud computing over the next three years.

This has created the need for instantaneous processing, which has been a restraining factor in the adoption of cloud computing processes. Owing to this, the IT & telecom industries held the largest market share in 2023.

Furthermore, the manufacturing industry is expected to flourish in the upcoming years due to the rising number of applications of computing solutions in the sector. Moreover, the rising adoption of such solutions across the retail, automotive, and oil & gas sectors is expected to increase the edge computing market share.

Regional Insights

Regionally, the market is studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Edge Computing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for USD 6.86 billion in 2025, representing 35.70% of the global market share, and is projected to reach USD 9.15 billion in 2026. The regional market is majorly influenced by the growing presence of leading players based in the U.S. Some of these players include IBM, Intel, Microsoft, and many others. These companies have been strategically expanding their geographic presence and customer base by merging with and acquiring small-scale companies.

- For instance, in February 2022, IBM acquired Sentaca to accelerate its hybrid cloud consulting business and add intricate skills to help Communications Service Providers (CSPs). With this acquisition, the company expected to modernize its cloud platforms and transform its business.

Globally, North America held the maximum share in 2023 as compared to other regions. Increasing demand for edge computing solutions across different industrial sectors to fulfill the growing network architectural needs of the customers and to provide better customer experience drive the growth of the market.

The U.S. held the maximum share in 2023 compared to other countries in North America. The growing adoption of advanced technologies such as big data and IoT among different industries, such as healthcare, education, and manufacturing, to improve the reliability and security of advanced IT infrastructure boosts the market's growth during the forecast period. The U.S. market is expected to reach USD 4.56 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

South America

Various market leaders present across South America are contributing to developing a standard regulatory framework for computing solutions to address the current challenges in the market. There are a limited number of technology substitutes for the market. Technologies, such as cloud computing, can be used as an alternative to the computing technology to fulfill the specific business needs of the end-user present across Brazil, Argentina, and other countries present across the region.

Europe

The Europe market was valued at USD 4.1 billion in 2025, capturing 21.50% of global revenue, and is estimated to reach USD 5.52 billion in 2026. Europe is projected to grow at a moderate rate over the forecast period. Different industrial sectors present across Germany, France, Italy, and the U.K., such as Information Technology & telecommunications, healthcare, shopping, transport & supply chain, energy & services, and more, are offering profitable chances for the market. Additionally, the continuous development of internet networks throughout the area is anticipated to accelerate the market's expansion in the near future. The UK market is anticipated to reach USD 0.87 billion by 2026, while the Germany market is estimated to reach USD 1.6 billion by 2026.

Middle East & Africa

Middle East & Africa contributed approximately USD 1.09 billion to the global market in 2025, accounting for 5.90% share, and is expected to reach USD 1.51 billion in 2026. The Middle East & Africa have been adopting advanced technologies on a large scale amid the pandemic crisis. Companies across these regions have been modernizing their existing processes with advanced technologies. More data generated through connected devices, rising deployment of cloud-based solutions, increasing demand for Industrial Internet of Things (IIoT) solutions, and other factors are expected to impact the market during the forecast period positively.

Asia Pacific

In 2025, Asia Pacific held 27.10% of the global market, reaching a valuation of USD 4.8 billion, and is projected to grow to USD 6.95 billion in 2026. Asia Pacific is also expected to grow significantly in the coming years. This is owing to the increasing adoption of edge solutions across Japan, India, and China. Besides this, government regulations supporting IT infrastructure have boosted the region's market growth. The Japan market is forecast to reach USD 1.82 billion by 2026, the China market is poised to reach USD 1.99 billion by 2026, and the India market is set to reach USD 1.67 billion by 2026. For instance,

- In September 2022 - India's telecom operator, Bharti Airtel, partnered with IBM Corporation to deploy its computing platform in India. This partnership will include over 120 network data centers in around 20 cities.

Latin America

The Latin America region captured 9.80% of the global market in 2025, generating USD 1.78 billion in revenue, and is projected to reach USD 2.5 billion in 2026.

KEY INDUSTRY PLAYERS

Technological Developments by Leading Enterprises to Aid Market Proliferation

Companies operating in the market mainly include IBM Corporation, Intel Corporation, Amazon.com, Inc., Google LLC, Microsoft Corporation, ADLINK Technology Inc., and Hewlett Packard Enterprise Development LP. These firms are focusing on bringing innovations in the market. To enhance their operations across the globe, market players are using various strategic methods, such as partnerships, product launches, investments, acquisitions, and mergers.

List of Edge Computing Market Players Profiled:

- IBM Corporation (U.S.)

- Intel Corporation (U.S.)

- Amazon.com, Inc. (U.S.)

- Google LLC (U.S.)

- Microsoft Corporation (U.S.)

- ADLINK Technology Inc. (Taiwan)

- Hewlett Packard Enterprise Development LP (U.S.)

- Cisco Systems, Inc. (U.S.)

- Huawei Technologies Co., Ltd. (U.S.)

- EdgeConneX Inc. (U.S.)

- ABB (Switzerland)

- Aricent, Inc. (U.S.)

- Atos (France)

- Cisco Systems, Inc. (U.S.)

- Rockwell Automation, Inc. (U.S.)

- SAP SE (Germany)

- Siemens AG (Germany)

- General Electric Company (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- February 2024 – At MWC Barcelona, ADLINK revealed 5G and industrial edge computing. Moreover, partners and customers of ADLINK, including AgrandTech, SageRAN, and Askey, would be representing several 5G network solutions built on the MECS series of ADLINK Edge Server.

- January 2024 – EQT Infrastructure announced a collaboration with EdgeConneX to progress data centers for hyperscale customers globally. This new alliance would build numerous megawatts of new data center capability to aid future cloud, artificial intelligence, and other precarious digital infrastructure necessities.

- January 2024 – IBM and American Tower announced an alliance to propel the adoption of edge computing. The purpose of the collaboration is to accelerate the deployment of a multi-cloud, hybrid cloud computing platform at the edge, transporting business applications closer to essential data sources.

- December 2023 – McDonald's Corporation announced a collaboration with Google to join the Google Cloud mechanism across its thousands of restaurants globally. With the partnership, McDonald's would make use of Google Cloud’s edge computing to empower these new platforms, transporting data storage and high power-driven computing into separate restaurants.

- March 2023 – BT Group and Amazon Web Services expanded their alliance on 5G edge computing services, cloud networking proposals, and IoT solutions for U.K.-based enterprise customers. The deal aims at a USD 500 million revenue prospect to sell IoT services and connectivity to U.K. businesses, predominantly over the coming five years.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product/service types, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 34.1% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component

By Enterprise Type

By Application

By Industry

By Region

|

|

Companies Profiled in the Report |

|

Frequently Asked Questions

The market is projected to reach USD 267.42 billion by 2034.

In 2025, the market was valued at USD 18.64 billion.

The market is projected to grow at a CAGR of 34.1% during the forecast period.

The hardware segment holds the largest market share.

Surging need for edge infrastructure for 5G network to drive market growth

IBM Corporation, Intel Corporation, Amazon.com, Inc., Google LLC, Microsoft Corporation, ADLINK Technology Inc., Hewlett Packard Enterprise Development LP, and Cisco Systems, Inc. are the top players in the market.

North America held the highest market with a share of 35.7% in 2025.

By industry, the IT & telecom sector is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us