Custom Procedure Packs Market Size, Share & Industry Analysis, By Product Type (Anesthesia Packs, Cardiovascular Surgery Packs, Neurosurgery Packs, Ophthalmic Surgery Packs, Orthopedic Surgery Packs, and Other Procedure Packs), By End-user (Hospitals {Operating Room, Intensive Care Unit (ICU), Outpatient Department, and Others}, Clinics, Ambulatory Surgery Centers, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

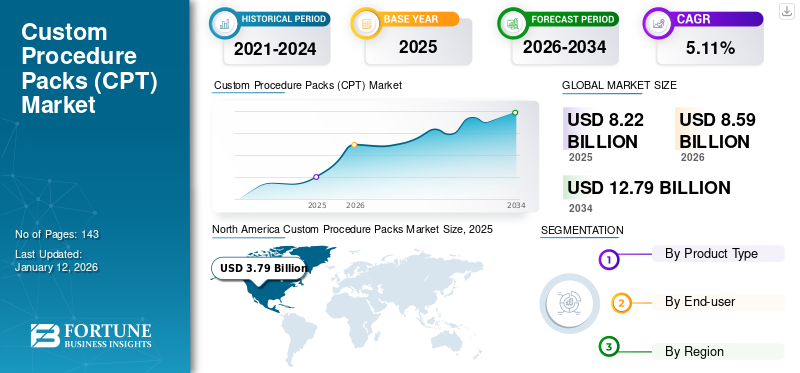

The global custom procedure packs market size was valued at USD 8.22 billion in 2025. The market is projected to grow from USD 8.59 billion in 2026 to USD 12.79 billion by 2034, exhibiting a CAGR of 5.11% during the forecast period. North America dominated the custom procedure packs market with a market share of 46.12% in 2025.

Custom procedure packs streamline surgeries by providing pre-arranged, tailored sets of instruments and supplies, reducing the preparation time, and ensuring surgical efficiency, consistency, and cost-effectiveness in healthcare settings. These packs consist of drapes, swabs, sutures, knives, syringes, and others. It is a single presentation of all the surgical consumable items required for a specific procedure such as knee arthroscopy, cardiovascular, cataract packs, and others. These kits enable faster clinical procedure setups and help in managing the cost of surgical products.

An increase in the number of surgical procedures and awareness about the benefits of these packs has led to a rise in the demand for custom procedure packs. Such a scenario has increased the interest of the major and emerging market players to conduct initiatives to start new facilities for manufacturing of these surgical procedure packs. Thus, these factors are driving the growth of the global market.

- For instance, in May 2023, Surgeine Healthcare (India) Pvt. Ltd started a new manufacturing facility to produce custom procedure packs to distribute the products in the Australian, American, African, and European markets, and these initiatives led to the growth of the custom procedure packs in the forecast period.

Additionally, key players in the market are focusing on product launches of advanced surgical solutions, which are environmentally sustainable and eco-friendly packs. Also, various emerging players are introducing new manufacturing facilities and distribution networks to cater to the growing demand for custom procedure packs in the market. Such factors are responsible for the global custom procedure packs market growth.

Global Custom Procedure Packs Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 8.22 billion

- 2026 Market Size: USD 8.59 billion

- 2034 Forecast Market Size: USD 12.79 billion

- CAGR: 5.11% from 2026–2034

Market Share:

- North America dominated the custom procedure packs market with a 46.12% share in 2025, driven by a strong healthcare infrastructure, rising number of surgical procedures, and growing awareness of the efficiency benefits of these packs.

- By product type, the Other Procedure Packs segment is expected to retain its largest market share, supported by the increasing demand for procedure-specific kits across diverse surgical specialties such as gynecological, urological, and bariatric surgeries.

Key Country Highlights:

- United States: Market growth is fueled by a high volume of elective surgeries, increasing hospital adoption of pre-arranged surgical kits, and a strong presence of key manufacturers focusing on product innovation.

- Europe: Rising surgical volumes, especially in gynecological and cardiovascular procedures, coupled with robust healthcare infrastructure, are enhancing the adoption of custom procedure packs.

- China: Rapid improvements in healthcare facilities, increasing number of surgical interventions, and growing awareness of cost-effective surgical solutions are driving market expansion.

- Japan: An aging population with a growing need for surgical care and a strong focus on surgical efficiency and safety standards is propelling demand for custom procedure packs.

COVID-19 IMPACT

Cancellations and Delays in Elective and Non-elective Surgeries during the Pandemic Negatively Impacted Market Growth

Due to the pandemic, the market experienced negative growth in 2020. Some of the factors that affected the growth of the market during the pandemic was a decline in the number of elective surgeries and non-elective surgeries. Hence, the growth of the market was negatively impacted during the pandemic.

- For instance, according to an article published by the British Journal of Surgery (BJS), in 2020, a significant number of operations were cancelled or postponed owing to the disruptions caused by COVID-19 across the globe.

The custom procedure packs (CPP) market revenue growth and sales of major market players declined in 2020. This decline was basically from the disruption in the distribution channel. The market saw a recovery in product sales in 2021.

- For instance, Cardinal Health recorded net sales of USD 15,444.0 million in 2020 from its medical segment (including custom procedure packs) segment, with a decline of 1.2% compared to the previous year. This was due to lower demand for surgical products resulting from reduced elective procedures.

- Furthermore, the medical segment sales increased by 8.0% in 2021 compared to 2020 as the demand improved during the fourth quarter of 2021.

The resumption of the normal frequency of hospital visits for surgeries contributed to the full normalization of the market in 2022. The market is expected to witness significant growth during the forecast period of 2025-2032.

- As per the article published by Stanford Medicine in 2022, after the COVID-19 shutdown in 2020, there was a decline in non-urgent surgery rates, but within months, they bounced back and remained at pre-pandemic levels in the U.S.

Custom Procedure Packs Market Trends

Significant Product Launches by Key Players are a Prominent Trend

During recent years, the prevailing trend in the global market is an increased focus and initiatives by major key players on developing innovative procedure products. Sterile and effective products with cutting-edge innovations are now widely used in surgical settings globally. The packs consist of drapes, swabs, sutures, knives, syringes, and others. All these components are specific to the surgery. These kits enable faster clinical procedure setup and help in managing the cost of surgical products. Similarly, many market players have increased their focus on introducing advanced drapes, sutures, and others, that can be used in the customization of these packs. Such growing demand for custom procedure products and recent product launches are propelling the market growth in the future.

Furthermore, certain initiatives are undertaken by the major key players, such as mergers and acquisitions, to develop these products. Such a scenario will fulfil the growing demand of the surgical industry.

- For instance, in March 2021, Lohmann & Rauscher acquired the German company Angiokard Medizintechnik GmbH, a producer and distributor of customized sets for cardiology, anaesthesia, angiography, minimally invasive surgery and cardiac surgery, to strengthen its position in the global hospital sector.

Currently, more companies are entering the market with new and innovative packs/kits to grow their business around the world.

Download Free sample to learn more about this report.

Custom Procedure Packs Market Growth Factors

Rising Number of Surgical Procedures and Rising Adoption of These Products in Surgeries to Boost Market Growth

One of the most prevalent drivers in the market is the increasing number of surgical procedures and the usage of these packs in those procedures. Some common surgical procedures include cardiovascular, general surgery, and ophthalmic. The growing prevalence of chronic diseases and rising awareness about surgical options are promoting the number of surgeries.

Also, the rising surgical healthcare expenditure and reimbursement facilities in various countries are increasing the surgical volumes. Such an increasing number of surgical procedures are expected to enhance the product penetration in the market.

- For instance, according to the data published by Mass General Brigham in 2023, more than 900,000 cardiac surgeries are performed in the U.S., including coronary bypass surgeries. Such a rise in cardiac surgeries is expected to drive the market in the forecast timeframe.

Additionally, the rise in orthopedic surgeries, such as hip, knee, or joint replacement surgeries, also enhances product demand in the market. Such a substantial demand for packs, due to the increasing number of surgeries, contributes to the growth of the market during the forecast period.

RESTRAINING FACTORS

Stringent Regulatory Framework for Maintaining Quality of Packs and Product Recalls Hinders Market Growth

Maintaining the products’ sterility and efficiency is challenging for the majority of manufacturers.

The strict regulations governing the manufacturing, testing, and use of these products raise the difficulty level for developing and introducing new products to the market. This poses a challenging situation for manufacturers striving to innovate and keep up with the evolving demands of the surgical industry. Such a regulatory scenario is expected to hamper the global market growth during the projected period.

Additionally, the market is observing numerous product recalls due to manufacturing errors in the packaging and sterility issues. Product recalls potentially damage the company’s reputation and result in significant financial losses for the business. Such factors hamper the market growth.

- As per the information published by the Government of Canada in December 2022, Medline Industries, LP recalled custom procedure packs containing Medtronic non-absorbable sutures due to an error in the manufacturing and packaging of the sutures that may cause a gap or wrinkle in the breather pouch seal resulting in a sterile barrier breach.

Such stringent regulatory scenarios and product recalls for these packs are anticipated to limit market growth during the forecast period.

Custom Procedure Packs Market Segmentation Analysis

By Product Type Analysis

Increase in Number of Surgical Procedures and Innovative Products Launches to Propel Others Segment Growth

Based on product type, the market is fragmented into anesthesia packs, cardiovascular surgery packs, neurosurgery packs, ophthalmic surgery packs, orthopedic surgery packs, and other procedure packs.

The other procedure packs segment led the global custom procedure packs market share in 2024. The other procedures include surgeries, such as gynecological surgery, urological surgery, bariatric surgery, and others. The increase in the number of other surgical procedures and the adoption of these packs for them is considerably high, especially in hospitals. The other procedure packs segment is projected to dominate the market with a share of 43.08% in 2026.

Furthermore, these packs streamline surgeries by providing pre-arranged, tailored sets of instruments and supplies, reducing preparation time for operations and ensuring surgical efficiency, which is further expected to propel the segment’s growth during 2025-2032.

- For instance, according to the data published by the American Society for Metabolic and Bariatric Surgery, the estimated number of bariatric surgeries that happened in 2021 in the U.S. was around 262,893. Thus, the growing number of surgeries heightened the adoption and utilization of CPPs.

The anesthesia packs segment registered a significant share of the market in 2024. Anesthesia packs are used in multiple surgeries, including knee and hip replacements, heart surgeries, and others. The robust utilization of these packs in a number of surgeries is promoting segmental growth.

The orthopedic surgery packs, cardiovascular surgery packs, ophthalmic surgery packs and neurosurgery packs segments together had a desirable market share in 2024. Thus, market players are emphasizing the launches of innovative products to help the end-users.

- For instance, in April 2023, Cardinal Health announced the launch of its state-of-the-art hair management drape, Stray Away, specifically designed and manufactured to help minimize hair from obstructing the surgical area and to improve patient preparation time and experience.

To know how our report can help streamline your business, Speak to Analyst

By End-user Analysis

Increasing Number of Inpatient Surgeries in Hospitals to Boost Hospitals Segment Growth

By end-user, the market is segmented into hospitals, clinics, ambulatory surgery centers, and others.

The hospitals segment gained a dominant market share in 2024. The hospital segment is further divided into operating room, intensive care unit (ICU), outpatient department, and others. The segment dominance is attributed to an increasing number of hospitals across the globe, an increase in the prevalence of chronic disease, and a rise in the number of inpatient surgeries, resulting in increased demand for these products in hospitals. The hospitals segment is projected to dominate the market with a share of 40.35% in 2026.

The ambulatory surgical centers segment held a significant market share. The growth was attributable to an increase in the number of ambulatory surgery centers that provide high-quality surgical procedures with low-cost care for patients. Furthermore, the usage of these products reduces the preparation time for operations. It ensures more surgeries every day, promotes the usage of these packs and propels the growth of the segment.

- For instance, according to the data published in the Ambulatory Surgery Center Association and ASCA Foundation journal, there are more than 5,900 Medicare-certified ASCs in 50 states of the U.S., with an estimated 22.5 million procedures every year.

In addition, the clinics segment is anticipated to register a moderate CAGR during the forecast period. These institutions handle minor surgical procedures, and the requirement for cost-efficient and safe instruments for performing these procedures in clinics is contributing to the market growth.

Moreover, the others segment held a lower share in the market. However, the growing usage of these procedure packs in academic institutes and for research purposes is expected to propel the growth of the segment.

REGIONAL INSIGHTS

Geographically, the market is studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Custom Procedure Packs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the global market with a revenue of USD 3.62 billion in 2024. The region held a significant share of the global market due to robust healthcare infrastructure and an increase in the number of ophthalmological, orthopedic, and general surgeries in the region. Additionally, increased awareness about the benefits of using packs and product launches is also anticipated to drive the growth of the market in the region. The U.S. market is expected to reach USD 3.8 billion by 2026.

- For instance, according to the data published by the American Society for Metabolic and Bariatric Surgery, the estimated number of bariatric surgeries that happened in 2021 in the U.S. was around 262,893. Thus, the growing number of surgeries heightened the adoption and utilization of these packs in the region.

Europe

Europe held a significant market share in 2024 and is anticipated to expand at a moderate growth rate during 2025-2032. Advanced healthcare infrastructure and a rise in the number of surgeries escalated the adoption of these products for surgeries in the European region. The UK market is anticipated to reach USD 0.4 billion by 2026, while the Germany market is estimated to reach USD 0.54 billion by 2026.

- For instance, according to data reported in Eurostat, around 1.14 million caesarean sections were performed alone in the European Union in 2021. Such a growing number of gynecological surgeries propels product adoption in the market.

Asia Pacific

Furthermore, the Asia Pacific is expected to expand at the highest CAGR during the forecast period. The rise in the aging population of countries, such as India and China, requires medical intervention with surgical assistance, which is expected to grow the revenue of the region during the forecast period. The Japan market is forecast to reach USD 0.55 billion by 2026, the China market is set to reach USD 0.4 billion by 2026, and the India market is poised to reach USD 0.15 billion by 2026.

- For instance, according to the data published by the Australian Institute of Health and Welfare, in the 2020-2021 period, 146,000 coronary angiography procedures were performed on patients admitted to hospitals. This scenario propels product adoption for performing efficient surgeries and thereby contributes to the growth of the segment.

Rest of The World

Latin America and the Middle East & Africa regions accounted for a considerable share in 2024. The increasing initiatives by global and regional players to penetrate the market and enhance the product adoption of these packs in developing countries are anticipated to promote regional growth.

Key Industry Players

Medline Industries, LP, Cardinal Health, and Mölnlycke Health Care AB Hold Significant Market Position Owing to Diversified Product Portfolio

The competitive landscape of the global market reflects a fragmented structure. Some prominent players in the market include Medline Industries, LP, Cardinal Health, and Mölnlycke Health Care AB, which held a significant position in the global market in 2024 due to their established market presence, including a larger customer base and innovative product launches. Also, a robust product portfolio for various packs and an established distribution network across the globe are the major factors for these companies' dominant market position.

- For instance, in February 2023, Medline Industries, LP signed a strategic partnership with Alberta Surgical Group. This agreement ensured the reliable flow of supplies to reduce the wait time for orthopaedic surgeons and to meet patient care demands.

Some of the other prominent players in the market, such as B. Braun SE, PAUL HARTMANN AG, Unisurge, Kimal, PrionTex, and others. Kimal offers a strong product portfolio, including products for cardiology, laparoscopy, and radiology surgeries, coupled with an expanded supply chain in 70 countries. Furthermore, the introduction of innovative packs and strategic initiatives to expand their geographical footprint, this aspect favors the market position of the companies.

Similarly, PrionTex, DeRoyal Industries, Inc., AMS ALIGNED MEDICAL SOLUTIONS, McKesson Medical-Surgical Inc., Core Medical, and other companies

List of Top Custom Procedure Packs Companies

- Cardinal Health (U.S.)

- PAUL HARTMANN AG (Germany)

- Unisurge (U.K.)

- Mölnlycke Health Care AB (Sweden)

- Medline Industries, LP (U.S.)

- PrionTex (South Africa)

- Kimal (U.K.)

- O&M Halyard (U.S.)

- B. Braun SE (Germany)

KEY INDUSTRY DEVELOPMENTS:

- February 2023: Kimal announced its participation in the Pan Arab Interventional Radiology Society (PAIRS) Annual Congress to be held at the Grand Hyatt Hotel in Dubai, with the goal of showcasing its custom procedure packs solutions for Interventional, Non-Vascular, HSG, Drainage, Embolization, Catheter Insertion and Neuro Radiology procedures.

- March 2022: Cardinal Health launched a surgical incise drape with antiseptic Chlorhexidine Gluconate, which helps to reduce the risk of surgical site infections (SSIs), which are associated with surgical site contamination.

- March 2022: Medline Industries, LP collaborated with the University Hospital Enhanced Recovery after Surgery (UH ERAS) Team to create a customized direct-to-patient kit for surgical procedures to enhance patients' surgical experience from pre-surgery through recovery.

- February 2022: Cardinal Health announced the partnership with Kinaxi’s RapidResponse, a concurrent planning platform that helps to improve overall planning, supplier management, risk management, and inventory capabilities of the company, along with that, it increased medical product visibility and supply chain agility.

- December 2021: O&M Halyard announced the acquisition of American Contract Systems (ACS), a Minnesota-based provider of kitting and sterilization services for Custom Procedure Tray (CPT) solutions. This acquisition exceeds the ability to fulfil the surgical procedure tray demand of customers.

REPORT COVERAGE

The report encompasses the global custom procedure packs market analysis. The market report covers and analyses the crucial segments such as product, end-user, and geography. Furthermore, the report features insights into the prevalence of key diseases, number of key surgical procedures, industry developments, pricing of these packs by key players, percentage (%) of kits by key procedures, business profiles of dominant players, and the COVID-19 pandemic impact on the market. Additionally, it highlights the market trends and competitive market share analysis of the overall global market forecast.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.11% from 2026-2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Product Type

|

|

By End-user

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market is projected to grow from USD 8.59 billion in 2026 to USD 12.79 billion by 2034.

The market is projected to grow at a CAGR of 5.11% during the forecast period.

The North America market size was USD 3.79 billion in 2025.

The others procedure packs segment is the foremost segment in the global market.

North America held the dominant global market with a share of 46.12% in 2025.

Increasing number of surgical procedures for diseases such as cardiovascular, neurological, orthopedic, ophthalmology, and others.

Medline Industries, LP, Cardinal Health, and O&M Halyard are the foremost players in the global market.

Significant benefits of utilizing these packs and the ability to improve and simplify the workflow for healthcare professionals in the market.

- 2021-2034

- 2025

- 2021-2024

- 143

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us