Intravenous Immunoglobulin Market Size, Share & Industry Analysis By Indication (Primary Immunodeficiency, Chronic Inflammatory Demyelinating Polyneuropathy (CIDP), Guillain-Barré Syndrome (GBS), Immune Thrombocytopenic Purpura (ITP), Multifocal Motor Neuropathy (MMN)), Form (Liquid, Lyophilized), End User (Hospitals, Clinics, Homecare) & Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

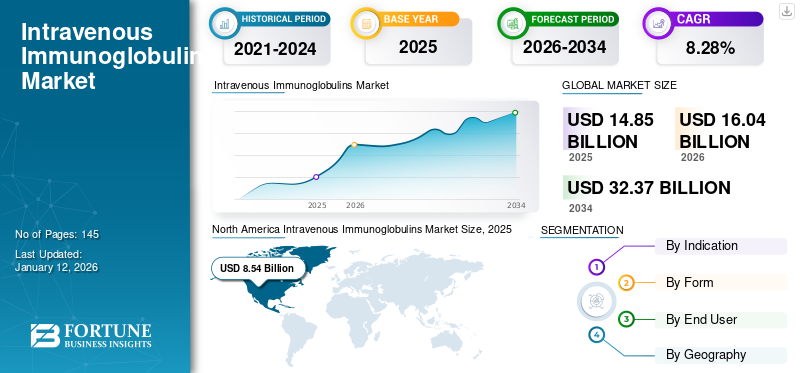

The intravenous immunoglobulins market size was valued at USD 14.85 billion in 2025 and is projected to grow from USD 16.04 billion in 2026 to USD 32.37 billion by 2034, exhibiting a CAGR of 8.28% during 2026-2034. North America dominated the intravenous immunoglobulins market with a market share of 74.53% in 2025.

Immunoglobulins are the glycoprotein molecules manufactured by the plasma or the white blood cells. Immunoglobulins form a very critical line of defense of the immune system by specially recognizing and binding itself to particular antigens such as bacteria and viruses and aid in their destruction.

Intravenous immunoglobulins are the immunoglobulins that are administered through the intravenous route. Intravenous immunoglobulins are the most common route of administration because most of the patients receiving immunoglobulins are in the hospital and clinical settings. This, coupled with the proven efficiency of the immunoglobulins as an effective treatment option for a number of immune diseases and the lack of training for homecare settings is also positively driving the Intravenous Immunoglobulin market growth.

Download Free sample to learn more about this report.

- North America witnessed a intravenous immunoglobulins market growth from USD 8.54 Billion in 2025 to USD 9.22 Billion in 2026.

Some of the other factors which are also contributing to the growth of the Market is its dominance in the both the developed and the developing markets. The ongoing R&D by major market players for the introduction of new and advanced intravenous immunoglobulins is expected to drive the Market growth in developed as well as emerging countries, during the forecast period 2026-2034.

Global Intravenous Immunoglobulins Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 14.85 billion

- 2026 Market Size: USD 16.04 billion

- 2034 Forecast Market Size: USD 32.37 billion

- CAGR: 8.28% from 2026–2034

Market Share:

- North America dominated the intravenous immunoglobulins market with a 74.53% share in 2025, driven by its role as a first-line treatment for several critical immune disorders, strong adoption of advanced intravenous immunoglobulin products, and a rising number of patient diagnoses.

- By indication, Primary Immunodeficiency (PI) is expected to retain the largest market share owing to increasing awareness, focused diagnosis initiatives, and high dependency on hospital-based administration of immunoglobulin therapies.

Key Country Highlights:

- United States: Increasing number of patients receiving immunoglobulins in clinical settings and strong presence of market leaders with diverse product portfolios are driving the market growth.

- Europe: Robust product pipelines of key companies, frequent regulatory approvals, and widespread hospital-based administration of immunoglobulin treatments support regional expansion.

- China: Growing awareness and diagnosis of primary immunodeficiencies, along with increased focus on expanding immunoglobulin therapy access, are propelling market growth.

- Japan: Rising expenditure on advanced immunoglobulin therapies and adoption of innovative treatment solutions are key factors fueling market demand.

Market Segmentation

"Increasing adoption of intravenous immunoglobulins as the most common treatment for primary immunodeficiency and dependency on immunoglobulin administration in hospital settings, is driving the market"

The adoption of intravenous immunoglobulin therapy as the first line of treatment for the primary immunodeficiency and other rare immunological and neurological diseases, is one of the most prominent leading to factors that are responsible for the intravenous immunoglobulin market growth in 2024. Primary Immunodeficiency (PI) segment is estimated to have the largest market share among the indication segment.

The Primary Immunodeficiency (PI) segment accounted for a market share of 28.6% in 2024 and is expected to increase during the forecast period. Increasing focus towards the diagnosis of primary immunodeficiency and the subsequent treatment based on the individual case and training of the patient, in most cases the patient is not adept in self-administration, is also driving the primary immunodeficiency segment.

- The primary immunodeficiency segment is expected to hold a 31.6% share in 2024.

The chronic inflammatory demyelinating polyneuropathy (CIDP) segment is estimated to grow at a slower CAGR during the forecast period. This is attributed to the comparatively lower prevalence of chronic inflammatory demyelinating polyneuropathy (CIDP). Currently, there is an existing dominance of the primary immunodeficiency (PI) as the indication for which intravenous immunoglobulin is the most prescribed for and this is expected to contribute to the growth of the market at higher CAGR during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

On the basis of indication, the intravenous immunoglobulin market segments include primary immunodeficiency (PI), chronic inflammatory demyelinating polyneuropathy (CIDP), Guillain-Barré syndrome (GBS), immune thrombocytopenic purpura (ITP), multifocal motor neuropathy (MMN), and others. The primary immunodeficiency (PI) segment accounted for 28.6% share of the global Market in 2024. On the basis of form, the global immunoglobulins market segments include liquid, and lyophilized. On the basis of end user, the market segments include hospitals, clinics, and homecare.

Regional Analysis

North America Intravenous Immunoglobulins Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

"An Increase In The Number Of Immunodeficiences Diagnoses Due To Greater Awareness, along with Increasing Adoption of Immunoglobulins Expected to Result in the Highest CAGR in the Asia Pacific"

The IVIG market in North America was valued at USD 11.09 Billion in 2024 and is anticipated to account for a dominant share in the Market during the forecast period. The primary driving factor for the significant and strong growth of the industry is the fact that it is the first line of treatment for a number of critical immune disorders. With the increase in contributing factors of such as the increasing number of patients and the efficiency of the intravenous immunoglobulins as treatment option, is expected to give rise to a significant demand for immunoglobulins. In developed countries, the adoption of advanced intravenous immunoglobulins is growing alongside the increasing number of indications that are approved. India and China in the Asia Pacific region are experiencing growth in the immunoglobulins due to increased diagnosis of primary immunodefiencies in the population. In terms of the dominance of indication, primary immunodeficiency is the most dominating indication in these developing regions. However, in countries like Japan, there is increased adoption and expenditure towards advanced immunoglobulins and Japan holds significant revenue shares in these advanced immunoglobulins. In Latin America and Middle East & Africa, the intravenous immunoglobulins will be popular due to the lack of self-administration of immunoglobulins in these regions.

Key Market Players

"Key market players such as Grifols S.A., CSL Behring and Shire (Takeda Pharmaceutical Company Limited) are anticipated to be the leading players in global Market"

Grifols, S.A., emerged as the leading player with the highest intravenous immunoglobulin market share in 2017, as the company has a number of product offerings in the across a wide range of indications and it is the commonly used route of administration, and these product offerings dominate a substantial portion of market share. The company accounts for the highest market revenue from regions such as North America and Europe. In addition, other market players are also getting product approvals such as Shire (Takeda Pharmaceutical Company Limited). The company received regulatory approvals for the immunoglobulin product offering of CUVITRU. Other players operating in the global market are CSL Behring, Grifols, S.A., Kedrion S.p.A, Octapharma, Bio Products Laboratory Ltd., Biotest AG, China Biologic Products Holdings, Inc., LFB SA and Shanghai RAAS Blood Products Co., Ltd.

List of Key Companies Profiled

- Shire (Takeda Pharmaceutical Company Limited)

- CSL Behring

- Grifols, S.A.

- Kedrion S.p.A

- Octapharma

- Bio Products Laboratory Ltd.

- Biotest AG

- China Biologic Products Holdings, Inc.

- LFB SA

- Shanghai RAAS Blood Products Co., Ltd.

Report Coverage

Immunoglobulins, also referred to as antibodies, are the glycoprotein molecules manufactured by the plasma or the white blood cells. Immunoglobulins form a very critical line of defense of the immune system by specially recognizing and binding itself to particular antigens such as bacteria and viruses and aid in their destruction. In certain individuals, immunoglobulins have to be administered for the treatment and management of diseases such as primary immunodeficiency (PI). Intravenous immunoglobulins are the most popular form of immunoglobulins, due to the no requirement of self-administration and the easy administration in hospital and clinic settings.

The intravenous immunoglobulin market report provides qualitative and quantitative insights on industry trends and detailed analysis of market size & growth rate for all possible segments in the market. The market segments include indication, form, and end user. On the basis of indication, the market is categorized into (primary immunodeficiency, chronic inflammatory demyelinating polyneuropathy (CIDP), Guillain-Barré syndrome (GBS), immune thrombocytopenic purpura (ITP), multifocal motor neuropathy (MMN) and others).

On the basis of form, the market can be segmented into liquid and lyophilized. On the basis of end user, the market can be segmented into hospitals, clinics and homecare. Geographically, the market is segmented into five major regions, which are North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The regions are further categorized into countries.

Along with this, the report analysis comprises of market dynamics and competitive landscape. Additionally, the report offers insights on the pipeline analysis, overview of regulatory scenario by key regions, key industry developments, number of primary immunodeficiency (PI) patients by key countries and reimbursement scenario.

Key Industry Developments

- In May 2019, the FDA approved the prior approval supplement (PAS) for ADMA Biologics, Inc.’s product offering of BIVIGAM and subsequently ADMA announced that it will begin the commercial sales of the product

- In April 2019, a novel intravenous immunoglobulin by ADMA Biologics, Inc. to be utilised for the treatment of primary immunodeficiency called Asceniv (Immune Globulin Intravenous, Human – slra 10%, Liquid), received the FDA approval

Report Scope & Segmentation

Request for Customization to gain extensive market insights.

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 8.28% from 2026-2034 |

|

By Indication |

|

|

By Form |

|

|

By End User |

|

|

By Geography |

|

Frequently Asked Questions

According to Fortune Business Insights, the Intravenous Immunoglobulins Market was valued at USD 16.04 Billion in 2026 and is projected to reach USD 32.37 Billion by 2034.

In 2025, the Intravenous Immunoglobulins Market was valued at USD 14.85 Billion.

Growing at a CAGR of 8.28%, the Intravenous Immunoglobulins Market will exhibit steady growth in the forecast period (2026-2034)

Primary Immunodeficiency segment is expected to be the leading segment in Intravenous Immunoglobulins Market during the forecast period.

The market growth is driven by increasing prevalence of immune disorders, growing awareness and diagnosis of primary immunodeficiencies, and the widespread use of IVIG in hospital settings.

Grifols S.A., CSL Behring and Shire (Takeda Pharmaceutical Company Limited) are the leading market players in Intravenous Immunoglobulins Market.

North America is expected to hold the highest market share in the Intravenous Immunoglobulins Market.

Growing dependency on immunoglobulin administration in hospital settings is one of the trends of Intravenous Immunoglobulins Market.

- 2021-2034

- 2025

- 2021-2024

- 145

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us