Immunoglobulin Market Size, Share & Industry Analysis, By Product Type (Intravenous Immunoglobulin (IVIG) {Primary Immunodeficiency, Secondary Immunodeficiency, Chronic Inflammatory Demyelinating Polyneuropathy, Guillain-Barré Syndrome, Immune Thrombocytopenic Purpura, Multifocal Motor Neuropathy, and Others} and Subcutaneous Immunoglobulin (SCIG) {Primary Immunodeficiency, Secondary Immunodeficiency, Chronic Inflammatory Demyelinating Polyneuropathy, and Others}), By Form (Liquid and Lyophilized), By End User (Hospitals, Clinics, and Homecare), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

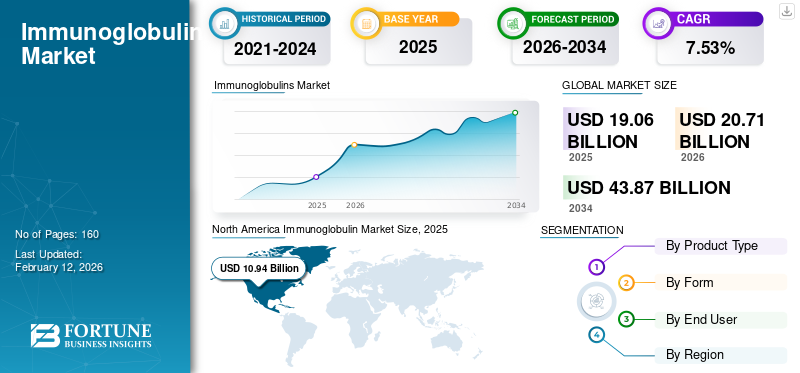

Immunoglobulin Market Size and Future Outlook

The global immunoglobulin market size was valued at USD 22.15 billion in 2025. The market is projected to grow from USD 24.44 billion in 2026 to USD 43.68 billion by 2034, exhibiting a CAGR of 7.53% during the forecast period. North America dominated the global immunoglobulin market with a market share of 49.39% in 2025.

The global market has been experiencing growth in recent years. The global market is driven by the increasing prevalence of autoimmune disorders and the growing use of immunoglobulins as first-line treatments. Key companies operating in the market are investing in research and development to innovate and develop more effective immunoglobulins to address the growing market trend. Also, government support and prompt regulatory approvals for new product launches further strengthen market growth.

- For instance, in September 2025, Kedrion S.p.A. received approval from the U.S. FDA for QIVIGY, a new 10% Immunoglobulin for intravenous use, indicated for treatment of adults with primary humoral immunodeficiency (PI).

Moreover, key players in the immunoglobulin treatment industry, such as CSL, Octapharma AG, and Takeda Pharmaceutical Company Limited, are expanding their product offerings to strengthen their market positions.

Download Free sample to learn more about this report.

Immunoglobulin Market KEY TAKEAWAYS

- 2025 Market Size: USD 22.15 billion

- 2026 Market Size: USD 24.44 billion

- 2034 Forecast Market Size: USD 43.68 billion

- CAGR: 7.53% from 2026–2034

- North America dominated the immunoglobulin market with a 49.39% share in 2025.

- The Intravenous Immunoglobulin (IVIG) segment accounted for the largest market share in 2025.

- The liquid segment dominated the global market by form in 2025.

Asia Pacific

Asia Pacific is projected to reach USD 3.71 billion in 2026, driven by increasing healthcare investments and rising demand for immunoglobulin therapies.

North America

North America reached USD 11.46 billion in 2025, supported by innovative product launches and growing prevalence of immunodeficiency disorders.

Europe

Europe is projected to reach USD 3.91 billion in 2026, fueled by government support and expanding healthcare infrastructure.

U.S.

The market is estimated at USD 11.19 billion in 2026, driven by strong demand for advanced immunoglobulin therapies.

Japan

The market is valued at USD 1.41 billion in 2026, supported by increasing adoption of immunoglobulin treatments.

Read More

IMMUNOGLOBULIN MARKET TRENDS

Shift Toward Subcutaneous Administration Due to its Advantages is a Prominent Trend Observed

A major global trend in the market is shifting preference toward subcutaneous administration. The increasing preference for Subcutaneous Immunoglobulin (SCIG) is due to the several advantages of SC administration over IV. Subcutaneous administration offers easier administration, enhanced safety, and the ability for patients to self-administer these products, which can improve adherence rates. These factors promote patient adoption and support the global immunoglobulins market growth. Manufacturers are also pushing this trend through innovative product launches featuring SCIG formulation, more user-friendly delivery formats, and support programs.

- For instance, in June 2023, Grifols, S.A. started marketing XEMBIFY, its 20% subcutaneous immunoglobulin, in Spain to boost growth.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for Treatment of Immunodeficiency Diseases to Fuel Market Growth

One of the principal factors driving immunoglobulin market growth is rising global demand for immunoglobulins to treat immunodeficiency diseases. The rising prevalence of these immunodeficiency diseases, such as Primary Immunodeficiency (PI), Chronic Inflammatory Demyelinating Polyneuropathy (CIDP), Guillain-Barré syndrome, and Multifocal Motor Neuropathy (MMN), among others, is driving demand for immunoglobulins. This increasing prevalence is resulting in a growing global patient population, further driving the growth of the market.

- For instance, in February 2025, the U.S. Pharmacist published an article titled ‘Primary Immunodeficiency Etiology and Incidence’ stating that approximately 1-2% of the U.S. population is affected by some PIDDs.

MARKET RESTRAINTS

Stringent Government Regulations in Several Countries to Limit Adoption of Products

One of the significant factors restraining market growth is the stringent government regulations governing the market. These immunoglobulins are derived from plasma and are subjected to stringent safety standards and manufacturing guidelines. Government bodies in the U.S., China, and other emerging countries ensure that the plasma collected and delivered meets all applicable quality, safety, and potency criteria.

- For instance, in the U.S., the Food and Drug Administration (FDA) oversees the collection, processing, and distribution of blood and plasma products by private companies under two national laws: The Public Health Service (PHS) Act and the Federal Food, Drug, and Cosmetic (FD&C) Act.

MARKET OPPORTUNITIES

Expanding Manufacturing Capacity to Offer Significant Opportunity for Market Players

One significant challenge for the market is supply chain disruptions caused by limited plasma availability and low production capacity among key players. Thus, improving plasma manufacturing capacity to meet the increasing demand for immunoglobulins creates a major growth opportunity for the market. Increasing investments by key players in new fractionation lines, higher-throughput purification, and expanded packaging offer significant growth opportunities.

- For instance, in February 2025, Octapharma AG invested in expanding its manufacturing facilities in Vienna to meet rising demand for human plasma-based medicines.

MARKET CHALLENGES

High Costs Associated with Immunoglobulin Therapies Pose a Critical Challenge to Market Growth

Immunoglobulins are administered for the treatment of various immunodeficiency conditions, such as primary immunodeficiency, CIDP, SID, and other diseases, as well as a plethora of other conditions, including autoimmune, infectious, and inflammatory states. However, the cost of immunoglobulin therapy is high, and inadequate reimbursement policies and high out-of-pocket costs are hindering market growth. Also, drug shortages due to irregular supply chains further add to the prices of these immunoglobulins, contributing to high prices.

- For instance, in December 2024, Myasthenia Gravis community published an article titled ‘VIG treatment for MG linked with high medical costs in Norway: Study reported that Myasthenia Gravis (MG) patients in Norway who were treated with Intravenous Immunoglobulin (IVIG) had 2.3 times higher direct medical costs during the first year after a diagnosis than those who didn’t receive IVIG treatment. These factors limit the adoption of immunoglobulin and pose a critical challenge to its growth potential.

Segmentation Analysis

By Product Type

High Utilization of IVIG to Position Them in Leading Position, Resulting in Segmental Dominance

Based on product type, the market is categorized into Intravenous Immunoglobulin (IVIG) and Subcutaneous Immunoglobulin (SCIG). The IVIG segment is further sub-segmented into primary immunodeficiency, secondary immunodeficiency, chronic inflammatory demyelinating polyneuropathy, Guillain-Barré syndrome, immune thrombocytopenic purpura, multifocal motor neuropathy, and others. The SCIG segment is further divided into primary immunodeficiency, secondary immunodeficiency, chronic inflammatory demyelinating polyneuropathy, and others.

Among these, the Intravenous Immunoglobulin (IVIG) segment dominated the immunoglobulin market share in 2025. The segment's dominance is attributed to high utilization in hospital settings. Also, high-burden neuro-immunology indications, where rapid-onset symptoms are managed with IVIG, are a key driver of the segment's growth. Such factors increased IVIG consumption and encouraged key companies to launch new products and to secure regulatory approvals. Furthermore, strategic collaborations among key companies and the launch of new products offering innovative solutions support market growth.

- For instance, in July 2024, KabaFusion partnered with GC Biopharma U.S., Inc. to distribute ALYGLO (Immune Globulin Intravenous, Human-stwk) 10% Liquid for Adults, for the treatment of patients with Primary Humoral Immunodeficiency (PI). Such developments are expected to drive the segment's growth.

The Subcutaneous Immunoglobulin (SCIG) segment is expected to grow at a CAGR of 11.18% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Form

Increasing Use of Ready-to-Use Format of Liquid Immunoglobulin to Lead Segmental Growth

Based on the form, the market is segmented into liquid and lyophilized.

In 2025, the liquid segment dominated the global market by form. This dominance of liquid immunoglobulin was mainly due to its ready-to-use format, which made it easier to use. They also reduce the risk of contamination and do not need reconstitution, reducing preparation time. These advantages result in higher adoption. Underscoring these advantages, many key companies are streamlining their resources toward innovative product launches and leading segmental growth.

- In January 2025, CSL Behring launched a 10g prefilled syringe for Hizentra (Immune Globulin Subcutaneous [Human] 20% Liquid). The Hizentra prefilled syringes enabled people living with Primary Immunodeficiency (PI) and Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) to elevate their treatment experience.

The lyophilized segment is projected to grow at a CAGR of 2.97% during the forecast period for the global market.

By End User

Preference toward Hospital Settings by Healthcare Providers to Place Them in Dominating Market Position

Based on end user, the market is segmented into hospitals, clinics, and home care.

In 2025, the hospital segment dominated the global market by end user. Immunoglobulins are mainly administered to immunocompromised patients in high doses. Healthcare providers prefer hospital settings, making patient monitoring easier. These settings also have established healthcare infrastructure and well-structured reimbursement pathways, facilitating the treatment of large patient volumes. Furthermore, increasing collaboration among key companies to broaden adoption reinforces the segment's dominance.

- For instance, in November 2025, KORU Medical Systems, Inc. signed a development agreement with a global pharmaceutical company. The agreement enabled broad collaboration on next-generation infusion systems for Subcutaneous Immunoglobulin (SCIg) therapy in clinical programs.

The home care segment is projected to grow at a CAGR of 9.18% during the study period.

Immunoglobulin Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Immunoglobulin Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America maintained a strong presence in the global market, reaching USD 11.46 billion in 2025, accounting for 60.12% share, and is expected to reach USD 12.47 billion in 2026. The market in North America is expected to increase significantly over the forecast period, driven by innovative immunoglobulin launches, an expanding pipeline of candidate therapies, and the rising prevalence of immunodeficiency diseases, which are fueling demand. These factors are enabling market growth.

U.S. Immunoglobulin Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market can be estimated at around USD 11.19 billion in 2026, accounting for roughly 45.80% of the global market.

Europe

In 2025, Europe generated USD 3.63 billion, contributing 19.04% to global market revenue, and is projected to grow to USD 3.91 billion in 2026. The region is expected to experience robust growth driven by government support for shared infrastructure development.

U.K. Immunoglobulin Market

The U.K. market size is estimated at around USD 1.04 billion in 2026, representing roughly 4.25% of the global market.

Germany Immunoglobulin Market

Germany’s market is projected to reach approximately USD 1.24 billion in 2026, equivalent to around 5.09% of the global market.

Asia Pacific

The Asia Pacific market accounted for USD 3.38 billion in 2025, representing 17.74% of the global industry, and is expected to reach USD 3.71 billion in 2026, and secure the position of the third-largest region in the market.

Japan Immunoglobulin Market

The Japanese market value in 2026 is estimated at USD 1.41 billion, accounting for approximately 5.76% of the global market.

China Immunoglobulin Market

China’s market is projected to be among the largest worldwide, with 2026 revenues estimated at around USD 2.12 billion, accounting for approximately 8.66% of global sales.

India Immunoglobulin Market

The Indian market in 2026 is estimated at around USD 0.68 billion, accounting for roughly 2.76% of global revenue.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. Latin America contributed 2.23% to the global market in 2025, with a valuation of USD 0.43 billion, and is projected to reach USD 0.45 billion in 2026.In 2025, Middle East & Africa represented USD 0.17 billion, accounting for 0.87% of the worldwide market, and is projected to grow to USD 0.18 billion in 2026. The region is experiencing market growth driven by increased investment and government initiatives. In the Middle East & Africa, the GCC is set to reach USD 0.30 billion in 2026.

South Africa Immunoglobulin Market

The South African market is projected to reach approximately USD 0.07 billion by 2026, accounting for roughly 0.28% of the global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on New Product Launches by Key Players to Propel Market Progress

The global market is highly consolidated, with companies such as Octapharma AG, Grifols, S.A., Takeda Pharmaceutical Company Limited, and CSL holding significant market share. Strategic partnerships, new product launches, regulatory approvals, and increasing investments in the sector drive these companies' market share.

- For instance, in June 2025, Takeda Pharmaceutical Company Limited received Orphan Drug Designation from the Japanese Ministry of Health, Labour and Welfare (MHLW) for mezagitamab, an immunoglobulin IgG1 for the potential indication of chronic immune thrombocytopenia (ITP), such developments aimed to drive market growth.

Other notable players in the global market include Kedrion S.p.A. and Johnson & Johnson. These companies are expected to prioritize expanding manufacturing capacity, strategic collaborations, and new product launches to strengthen their position during the forecast period for the global market.

LIST OF KEY IMMUNOGLOBULIN COMPANIES PROFILED

- CSL (Australia)

- Takeda Pharmaceutical Company Limited (Japan)

- Grifols, S.A. (Spain)

- Kedrion S.p.A (Italy)

- Octapharma AG (Switzerland)

- ADMA Biologics, Inc. (U.S.)

- Taibang Biologic Group (China Biologic Products Holdings, Inc.) (China)

- LFB Group (France)

- Shanghai RAAS Blood Products Co., Ltd (China)

- GC Biopharma Corp (South Korea)

KEY INDUSTRY DEVELOPMENTS

- May 2025: Grifols, S.A. submitted an Investigational New Drug (IND) application to the U.S. FDA to initiate a Phase 2 trial evaluating its Immunoglobulin (IG) drops, GRF312 Ophthalmic Solution, as a potential new treatment for Dry Eye Disease (DED).

- April 2025: Amgen received U.S. FDA approval for UPLIZNA as the only treatment for adults living with Immunoglobulin G4-related disease (IgG4-RD). IgG4-RD is a chronic and debilitating immune-mediated inflammatory condition that can affect multiple organs.

- April 2025: CSL Behring launched ANDEMBRY Subcutaneous Injection 200 mg Pen (garadacimab), a novel human anti-activated Factor XII monoclonal antibody for the prevention of acute attacks of Hereditary Angioedema (HAE) in Japan.

- December 2024: Takeda Pharmaceutical Company Limited announced the approval of HYQVIA 10% S.C. (subcutaneous) injection set in Japan for patients with agammaglobulinemia or hypogammaglobulinemia.

- October 2024: GC Biopharma collaborated with Novelty Nobility, a company specializing in the development of antibody-based therapeutics, to jointly research and develop a novel treatment for geographic atrophy (GA).

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.53% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Form, End User, and Region |

|

By Product Type |

· Intravenous Immunoglobulin (IVIG) o Primary Immunodeficiency o Secondary Immunodeficiency o Chronic Inflammatory Demyelinating Polyneuropathy o Guillain-Barré Syndrome o Immune Thrombocytopenic Purpura o Multifocal Motor Neuropathy o Others · Subcutaneous Immunoglobulin (SCIG) o Primary Immunodeficiency o Secondary Immunodeficiency o Chronic Inflammatory Demyelinating Polyneuropathy o Others |

|

By Form |

· Liquid · Lyophilized |

|

By End User |

· Hospitals · Clinics · Homecare |

|

By Region |

· North America (By Product Type, Form, End User, and Country) o U.S. o Canada · Europe (By Product Type, Form, End User, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Product Type, Form, End User, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Product Type, Form, End User, and Country/Sub-region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Product Type, Form, End User, and Country/Sub-region) o GCC o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 22.15 billion in 2025 and is projected to reach USD 43.68 billion by 2034.

In 2025, North Americas market value stood at USD 10.94 billion.

The market is expected to grow at a CAGR of 7.53% over the forecast period.

By product type, the Intravenous Immunoglobulin (IVIG) segment is expected to lead the market.

The increasing prevalence of immunodeficiency diseases is fueling market demand and boosting market growth.

Octapharma AG, Takeda Pharmaceutical Company Limited, and CSL are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 160

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us