Smartphone Market Size, Share & Industry Analysis, By Operating System (Android, iOS, Windows and Others), By Distribution Channel (OEMs Stores, Retailer and E-commerce) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

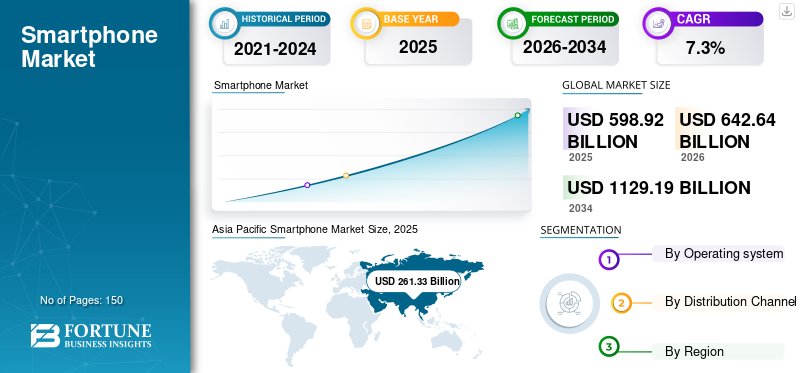

The global smartphone market size of USD 598.92 billion in 2025 and is projected to expand from USD 642.64 billion in 2026 to USD 1129.19 billion by 2034, growing at a CAGR of 7.30% over the forecast period. Asia Pacific dominated the smartphone market with a market share of 43.63% in 2025.

The global COVID-19 pandemic has been unprecedented and staggering, with smartphones experiencing lower-than-anticipated demand across all regions compared to pre-pandemic levels.

A smartphone is a mobile handset that empowers advanced access to internet-based facilities and other digital functions. Platforms including, iOS, Android, Windows Phone and others, support a broad range of applications created by third-party originators. Factors such as the governmental support to develop telecom infrastructure, budget-centric product launch, growing 5G technology, Artificial Intelligence (AI) and other technologies and importantly, the increasing disposable income are contributing to the market growth.

Additionally, the Global System for Mobile Communications (GSMA) stated that the utilization of mobile phones specifically reduces travel for leisure and commuting. By 2025, it could result in a doubling of the avoided emissions leveraged by mobile technologies seen in 2018. As a result, it boosted the manufacturing need and usage amongst the end-users. The GSMA also stated that there would be 75.0% smartphone adoption by 2022.

Download Free sample to learn more about this report.

Global Smartphone Market Overview

Market Size & Share:

- 2025 Market Value: USD 598.92 billion

- 2026 Estimate: USD 642.64 billion

- 2034 Forecast: USD 1129.19 billion

- CAGR (2026–2034): 7.3%

- Top Region: Asia Pacific – driven by 5G infrastructure, vast user base, and local production

- Fastest-Growing Country: India – propelled by digital initiatives, 5G adoption, and PLI incentives

- Top OS Segment: Android – dominates global share with a customizable, open ecosystem

- High-Growth OS Segment: iOS – gaining popularity in developing markets among young users

Key Trends and Drivers:

- 5G transformation: Accelerated shift toward 5G-enabled smartphones for high-speed connectivity

- AI & sensor integration: Enhanced human-system interaction drives smart features and applications

- E-commerce dominance: Online sales and M-commerce fueling smartphone demand across regions

- Government push: National digitalization plans and telecom reforms supporting broader adoption

- OEM innovation: Top brands launching advanced models with camera, charging, and UI upgrades

- Work-from-home culture: Sustained remote work boosting need for smart, connected devices

Market Challenges:

- Semiconductor shortages: Ongoing supply chain issues impacting production and availability

- Trade disruptions: U.S.–China tensions and COVID-related restrictions affecting global logistics

- High component costs: Increased input costs raising final product prices in key regions

- Security concerns: Risks from counterfeit sensors and biometric spoofing hinder user trust

Market Opportunities:

- Emerging market growth: Smartphone adoption rising in Africa, Southeast Asia, and Latin America

- Retail expansion: OEM-owned stores and retail partnerships growing in India and other APAC markets

- IoT convergence: Rising use of smartphones in smart homes, healthcare, and fleet systems

- Eco-friendly innovation: GSMA-led green initiatives positioning smartphones in climate solutions

The leading companies, such as Samsung, Apple, Inc., Sony Group corporation, Oppo and Vivo, among others, are constantly unveiling innovative mobile products with 5G technology, which in turn, is fueling the market growth. For instance, in October 2021, Sony Group Corporation introduced ‘Xperia PRO-I product,’ which combines autofocus and advanced image processing, 4K 120p video recording, 1.0-type sensor and other features to offer an innovative experience to its end-users.

COVID-19 IMPACT

Disrupted Demand and Supply Negatively Affected the Shipments

In March 2020, the World Health Organization declared COVID-19 a pandemic. It has certainly affected almost every market. It has severely disrupted the balance of demand and supply in the mobile phone sector. And as a result, the shipments declined. The primary reason is a nationwide lockdown across China, India, U.K., U.S. and other major countries.

In few countries, the increasing cost was attributed to component shortages specifically the semiconductor components during the pandemic, higher logistics costs, currency/tax devaluations, quarantine mandates, travel restrictions and others. The COVID-19 pandemic is still continuing to affect consumer buying behavior as it has once again started to affect.

In accordance, reinforced work from home guidelines and factory shutdown in multiple countries owing to the 2nd wave in 2021, accompanied by retail businesses’ closure and restrictions on online-deliveries affected the sales in the Q2 and Q3 of 2021 after a strong start in the beginning of 2021. However, the market participants were well-prepared for the disruption this time ahead of demand in the Q2 and Q3 of 2021.

As a result, on a long-term basis, the work from home concept, adoption of 5G technology and other factors have improved buying behavior that has shown positive market growth. Additionally, the International Data Corporation (IDC) stated that smartphone shipments saw a 7.7% growth in 2021 compared to 2020. Thus, the global market is estimated to witness strong growth in the forecast period.

LATEST TRENDS

Download Free sample to learn more about this report.

Ever-growing Demand for 5G-Compatible Smartphone to Add Impetus

In the current era, 5G is a trending feature in mobile phones, specifically across the U.S., India, China, South Korea, U.K., Japan and others. The 5G-compatibility is anticipated to replace the existing handset within the next five years. This trend is due to their ease of shift towards embedded services such as cloud storage, content subscription and access to the high-speed network.

For instance, Global System for Mobile Communications (GSMA) stated that, by 2025, 20% of global connections would have 5G connections with strong development across North America, Asia Pacific and Europe. Internet of Things (IoT) would be an integral part of the 5G era.

The amplified demand for virtual and augmented reality is also improving the market presence of 5G-compatible mobile handsets. In addition, the availability of low-cost, low-power consumption with fast charging capability is creating top spot across the globe.

It is, therefore, brightening the smartphone market growth across developing and developed countries.

DRIVING FACTORS

Increasing Adoption of Human-System Interaction to Bolster the Market Growth

In the current period, the human-system interaction phenomenon is predominantly driving the technology market across the globe. In accordance, mobile phone manufacturers and suppliers could explore opportunities from the prevailing trends. Mobile phone connectivity discovers its application in automobiles, fleet management operations, healthcare devices, smart metering, personnel traffic, infrastructure security systems connectivity and others. Mobile sensors have opened new dimensions in human-computer interaction that boost demand.

Additionally, the governmental bodies across the countries, including India, China, Taiwan, the U.S. and others, in partnership with leading companies, are relying more on offering digital information, education and other related services, which have certainly fueled the demand. That is eventually boosting the global market growth. For instance, in April 2021, Apple, Inc. committed to propelling 5G technology and silicon engineering by investing USD 430.00 billion in the U.S to support American innovation strategies for the next 5-years.

As a result, the accumulative practices in increased adoption of human-system interaction are bolstering the global mobile phone market growth.

RESTRAINING FACTORS

Shift in Trade Activities coupled with Semiconductor Components Shortage to impede Market Growth

The market is mainly dominated by China, India, U.S., South Korea and Japan. However, with the change in China-U.S. trade activities, COVID-19 pandemic period and the unavailability of raw materials have hampered the global market. Large organizations are heavily suffering due to high production volume and supply chain operations, whereas small and medium enterprises experience limited impact. In addition, the shortage of semiconductor components is directly hampering the market as these components are vital parts of overall product usage and innovation strategies.

In case of a component shortage, the companies are establishing semiconductor manufacturing facilities that might minimize the shortage. However, the shortage will affect the market at least until the end of 2022. The fake sensors applications to generate fake face recognition, fingerprints are also anticipated to hamper the global market growth.

SEGMENTATION

By Operating System Analysis

iOS Segment to Capture Highest CAGR Attributed to Growing Apple Phones’ Popularity

In terms of operating system, the market is categorized into android, iOS, windows and others.

iOS segment is anticipated to grow exponentially owing to the rising demand for Apple phones. Additionally, Apple phones are witnessing growing demand from developing countries, such as India, China and South Africa and others, especially from the young population. iOS is more document-friendly than others and generates less heat than other OS.

The android segment holds the major shares in the market. Developed by Google LLC, android OS is utilized in almost every handset except Apple products and a few others. It offers a customizable user interface, affordable continuous development and an open ecosystem. That results in the highest shares in the market.

Windows and others segment are witnessing slow growth as approximately 90.0% of the market is captured by android and iOS segments. The expanding demand for android and iOS has lowered the demand for windows and others segment.

By Distribution Channel Analysis

To know how our report can help streamline your business, Speak to Analyst

Fast-tracked Online Buying Behaviors to Help E-commerce Segment Gain Highest CAGR

By distribution channel, the market is segmented into retailers, OEMs stores and e-commerce.

E-commerce segment is in the best position to lead the market in terms of CAGR in the forecast period. The work from home concept and augmented online buying facilities are boosting the E-commerce segment growth.

Apart from this, as a form of E-commerce, the ‘M-commerce’ concept is boosting the buying and selling of goods via mobile phones. Online purchases are more or less via E-commerce sector, thus, propelling its demand.

OEMs are original equipment manufacturers. They are predominantly launching their factory outlets across the countries without seeking help from third parties. As a result, the outlets are growing across the countries. For instance, in March 2021, Vivo Mobile Communication Co., Ltd. stated that the company is opening 150 exclusive stores in India to drive smartphone market share. However, the COVID-19 pandemic forced companies to shut their stores, thus, widening the buying from E-commerce sites.

Whereas, retailers are probable to capture considerable market shares in the forecast period attributed to their prerequisite across developing and low population countries.

REGIONAL INSIGHTS

The market is categorized into North America, Europe, Asia Pacific, the Middle East & Africa, and South America, further divided into countries.

Asia Pacific Smartphone Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia Pacific is best positioned to lead the market with the highest CAGR over the forecast period. It is attributed to the vastly developing telecom sector and large customer base. Additionally, the region is increasingly investing in mobile networks with 5G technology, internet of things (IoT) and others that, in turn, propelling the market growth.

Moreover, the leading market participants are continuously introducing innovative products that are eventually fueling market growth. For instance, in January 2022, Vivo Mobile Communication Co., Ltd launched ‘V23 and V23 Pro’ in India. These products are India’s 1st color-changing smartphone. Its back panel changes color when exposed to artificial UV rays and sunlight.

India

The governmental Schemes Coupled with Technological Advancement to Portray Highest CAGR for India Market

India is considered one of the most lucrative markets. The reasons could be improved digital infrastructure, intensifying acceptance of E-commerce, surging internet usage and 5G-compatible phone availability. India has experienced intensified export owing to the production-linked incentive (PLI) scheme that boosted the global mobile production center for manufacturers across the country. For instance, the India Brand Equity Foundation stated that, during January-September 2020, India exported 10.9 million smartphones. This, in turn, is bolstering the growth of the market across the country.

North America

North America is one of the stable markets and, therefore, could gain impetus in handset repairing activities. The key market participants, such as Apple, Inc., SAMSUNG, Huawei Device Co., Ltd. are emphasizing product expansion across Canada that has expanded their market presence. For instance, in November 2021, Huawei Device Co., Ltd. stated that the company is on the verge of releasing mobile handsets across Canada to provide better services to customers.

Europe

The automotive and telecom industries across Europe are spending heavily on IoT-enabled product manufacturing. In accordance, the augmented consumption of consumer electronics across Germany, U.K., Italy and other countries is complementing the growth in the region. For instance, in July 2020, Samsung partnered with the German Federal Office for Information Security (BSI), Deutsche Telekom Security GmbH and Bundesdruckerei (bdr) to develop a security architecture that is hardware-based. It is permitting the country people to securely store their National ID on their handset as an eID. This partnership is supporting eGovernment initiative of the Country.

To know how our report can help streamline your business, Speak to Analyst

Middle East and Africa and South America

The Middle East and Africa and South America are projected to witness a substantial growth rate. Consumers are purchasing high-end electronic devices owing to their rising disposable income levels. The major players are also launching industry-leading products in these regions, thus encouraging market growth. For instance, IDC stated that Apple, Inc., in Q4 2020, witnessed double-digit growth in Gulf countries. In October 2021, Vivo Mobile Communication Co., Ltd. launched Y33s in the Kenya market.

KEY INDUSTRY PLAYERS

Leading Market Participants Unveil State-of-the-art Products for Deep Market Penetration

Leading market participants are introducing innovative devices to fulfill end-users demands. The upcoming period in the shadow of the COVID-19 pandemic has enforced work from home practices that bolstered the demand. For instance, in September 2021, Apple Inc. announced iPhone 13 and 13 mini mobile phones that feature innovative sensor-shift optical image stabilization (OIS) and dual-camera system.

Vivo Mobile Communication Co., Ltd. Partnered with Jamboshop Limited to Expand its Market Presence

Vivo Mobile Communication Co., Ltd. is strengthening its global presence by combining its forces with other local companies and local retailers to promote and develop innovative handset technologies across the countries. The company is mainly emphasizing mobile imaging technology. For instance, in April 2021, Vivo Mobile Communication Co., Ltd. partnered with Jamboshop Limited, Kenya’s online retailer, to increase its footprint across the country.

LIST OF KEY COMPANIES PROFILED:

- Apple Inc. (U.S.)

- SAMSUNG (South Korea)

- Oppo (China)

- Huawei Device Co., Ltd. (China)

- OnePlus (China)

- Sony Group Corporation (Japan)

- Xiaomi (China)

- HTC Corporation (Taiwan)

- Google LLC (U.S.)

- ZTE Corporation (China)

KEY INDUSTRY DEVELOPMENTS:

- August 2021: Samsung introduced the ‘Galaxy Z Flip3 5G’ and ‘Galaxy Z Fold3 5G’, the innovative foldable mobile phone. With iconic design, both the devices are built with flagship innovation, offering a unique user experience to work, play and watch.

- September 2019: Huawei Device Co., Ltd. in Munich unveiled new smartphone series, ‘HUAWEI Mate 30’. The iconic series features a top Kirin 990 5G SoC, super sensing cone camera, quad camera system with futuristic halo ring design.

REPORT COVERAGE

The smartphone market report provides detailed information regarding various insights into the industry. Some of them are growth drivers, restraints, competitive landscape, regional analysis, and challenges. It further offers an analytical depiction of the market trends and estimations to illustrate the forthcoming investment pockets. The market is quantitatively analyzed from 2022 to 2029 to provide financial competency. The information gathered in the report has been taken from several primary and secondary sources.

Request for Customization to gain extensive market insights.

Report Scope and Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026 – 2034 |

|

Historical Period |

2021–2024 |

|

Unit |

Value (USD billion) and Volume (Bn Units) |

|

Segmentation |

Operating System, Distribution Channel and Region |

|

By Operating System |

|

|

By Distribution Channel |

|

|

By Region |

|

Frequently Asked Questions

Fortune Business Insights says the market stood at USD 598.92 billion in 2025.

Fortune Business Insights says that the market will reach USD 1129.19 billion in 2034.

The market will exhibit strong growth, registering a CAGR of 7.3% during the forecast period.

Augmenting human-system interaction is expected to drive the market.

SAMSUNG, Apple, Inc., Xiaomi, Oppo and Huawei Device Co., Ltd. are the top companies in the global market.

Asia Pacific is expected to capture the highest CAGR in the market.

Fast-tracked demand for 5G-compatible device is a key market trend.

iOS segment is expected to capture the highest CAGR in the market.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us