Anastomosis Devices Market Size, Share & Industry Analysis, By Product (Stapling Devices, Compression Devices, Suturing Devices, and Others), By Mode (Manual and Powered), By Application (Gastrointestinal Surgery, Colorectal Surgery, Bariatric Surgery, Thoracic Surgery, and Others), By End-user (Hospitals, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Anastomosis Devices Market Size and Future Outlook

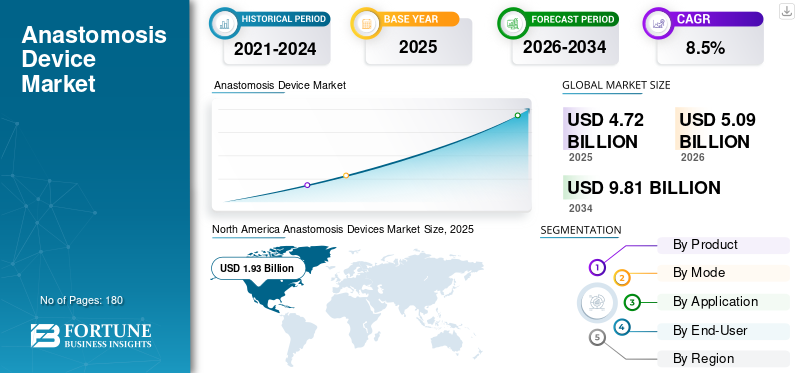

The global anastomosis devices market size was valued at USD 4.72 billion in 2025. The market is projected to grow from USD 5.09 billion in 2026 to USD 9.81 billion by 2034, exhibiting a CAGR of 8.5% during the forecast period. North America dominated the global market with a market share of 40.89% in 2025.

Anastomosis devices are specifically used to join two cut ends of the body’s tubes, mostly intestines, during surgical procedures. These devices play a prominent role in helping surgeons make the joint faster, more consistent, and more controlled than doing every stitch by hand, especially in busy hospitals. Market growth is prominently attributed to the increase prevalence of bariatric & gastrointestinal conditions, rising surgical volume of bowel cancer, and an increase in age-related problems. In addition, the focus of healthcare facilities to adopt technologically advanced devices for faster and better outcomes is also projected to have a positive impact on the market growth.

- For instance, in May 2024, Ethicon announced the launch of its ECHELON LINEAR cutter. The new device has been launched to reduce surgical risks.

Moreover, Medtronic, Johnson & Johnson MedTech, Intuitive Surgical, B. Braun Melsungen AG, and Meril Life Sciences are top market participants. They focus on crafting different advanced technologies to deliver improved products with greater precision and efficacy.

Download Free sample to learn more about this report.

ANASTOMOSIS DEVICES MARKET Key Takeaways

- 2025 Market Size: USD 4.72 billion

- 2026 Market Size: USD 5.09 billion

- 2034 Forecast Market Size: USD 9.81 billion

- CAGR: 8.5% from 2026–2034

- North America dominated the global market with a market share of 40.89% in 2025.

- Hospitals are expected to account for an 80.1% market share in 2026, supported by high surgical procedure volumes.

- The suturing devices segment is expected to increase at a CAGR of 8.5% in the coming years.

North America

North America reached USD 1.93 billion in 2025, driven by the rising prevalence of colorectal disorders and continued technological advancements in surgical devices.

Europe

Europe is projected to attain USD 1.37 billion in 2026, supported by increasing investments in product innovation and the growing burden of age-related diseases.

Asia Pacific

Asia Pacific is expected to reach USD 1.16 billion in 2026, benefiting from improving healthcare infrastructure and favorable investments by leading industry participants.

U.S.

The market is estimated at approximately USD 1.77 billion in 2026, accounting for nearly 34.9% of global market revenue, supported by strong healthcare spending and advanced surgical adoption.

Japan

The market is expected to reach around USD 0.20 billion in 2026, representing roughly 4.0% of global revenue, driven by an aging population and increasing demand for surgical procedures.

Read More

ANASTOMOSIS DEVICES MARKET TRENDS

Shift Toward Better and User-Friendly Designs is One of the Important Trends

The market is observing a trend of preference for devices that are easier to handle and more consistent in performance. Market players are improving ergonomics, reliability, and the ability to work in tight spaces. In addition, the market is also witnessing the adoption of devices that are compatible with robotic systems, which provide specific access and workflow needs. Moreover, hospitals are increasingly looking for solutions that reduce procedure time and support repeatable results.

- For instance, in November 205, Medtronic announced the launch of its Signia Circular Stapler with Tri-Staple technology. The device offers superior benefits for open and laparoscopic surgeries.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Number of Abdominal and Bowel Surgeries to Accelerate Market Growth

A growing number of bowel and abdominal procedures across the globe is prominently driving the global anastomosis devices market growth. In these types of surgical procedures, body pathways must be reconnected. In addition, as hospitals handle more complex cases, they prefer tools that help surgeons complete joining steps quickly and consistently. Due to such demand for technologically sound products, top companies are focusing on the launch of new products, further propelling the market growth.

- For instance, in April 2025, Intuitive Surgical received FDA approval for its SP SureForm 45 staplers. The product is beneficial in urological, thoracic, and colorectal surgical procedures.

MARKET RESTRAINTS

High Cost of Devices to Hamper Market Growth

Many anastomosis devices, especially branded staplers and reloads, are expensive, and hospitals buy them through strict value committees. Even if a device is clinically preferred, purchasing teams may push for lower-cost options, reuse policies, or limited standardization to control budgets. In addition, when hospitals face staffing shortages or budget cuts, they may delay switching to newer joining systems unless there is a clear operational benefit and training support from the supplier.

MARKET OPPORTUNITIES

Growing Preference for Suture-less Procedures to Offer Favorable Market Growth Opportunities

A strong opportunity is growth in suture-less or alternative connection methods that aim to simplify the joining step and reduce variability. Newer technologies, such as magnetic compression to offer better patient outcomes. These approaches are still new, but they attract attention as they promise a simpler workflow and could reduce certain failure risks if proven at scale.

MARKET CHALLENGES

Training and Technique Differences Across Surgeons Pose a Critical Challenge to Market Growth

Training and Technique differences across surgeons offer a considerable challenge for market growth. Even a good device needs correct sizing, placement, and handling. Hospitals with many rotating staff or new surgeons may see slower adoption as teams need training, practice, and confidence with the device steps. If staff are not fully comfortable, they may prefer older, familiar methods.

Segmentation Analysis

By Product

Superior Functionality of Stapling Devices to Drive Segment Growth

In terms of product, the market is categorized into stapling devices, compression devices, suturing devices, and others.

Stapling devices are set to register for the largest anastomosis devices market share as they are the most widely used, most available, and fastest way to reconnect tissue in many surgeries. Hospitals prefer staplers as they fit existing workflows and are supported by broad supplier networks. Moreover, technological advancements in staplers are also estimated to drive segment growth.

- For instance, in January 2025, Genesis Medtech announced the launch of its new stapler iReach Omnia in China. The new stapler is capable of 90-degree articulation.

The suturing devices segment is expected to increase at a CAGR of 8.5% in the coming years.

To know how our report can help streamline your business, Speak to Analyst

By Mode

Superior Access and Availability of Manual Devices to Accelerate Segment Growth

By mode, the market is bifurcated into manual and powered.

In 2025, the manual segment dominated the global market. The market growth is attributed to the substantial availability and access to manual devices across the globe. In addition, many surgeons are trained on manual staplers and suturing techniques, so switching to powered systems may be seen as optional rather than required. Manual tools also avoid battery/console dependencies and are often perceived as simpler in setup.

The powered segment is predicted to surge with a CAGR of 9.7% during the projected period.

By Application

High Prevalence of Bowel Conditions Accelerated Colorectal Surgery Segment Growth

On the basis of application, the market is segregated into gastrointestinal surgery, colorectal surgery, bariatric surgery, thoracic surgery, and others.

In 2025, the colorectal surgery segment dominated the global market. Colorectal surgery is a leading application as reconnection of the bowel is a standard step in many procedures, making demand steady and high volume. These surgeries are performed frequently for cancer and other bowel conditions. Hospitals also focus strongly on reducing complications in this area, as problems can lead to major costs and patient harm.

The bariatric surgery segment is expected to grow with a CAGR of 9.0% in the coming years.

By End-User

Higher Patient Visits in Hospitals to Boost Segment Growth

Based on end-user, the market is segmented into hospitals, specialty clinics, and others.

In 2025, hospitals held the highest market share as most surgeries requiring anastomosis are done in fully equipped operating rooms with specialized staff and post-operative care. Hospitals handle a wide mix of routine and complex cases, and they perform higher procedure volumes than smaller facilities. They also have structured purchasing systems, training support, and the ability to adopt newer surgical workflows. Furthermore, the segment is set to hold 80.1% share in 2026.

The specialty clinics segment is set to rise at a CAGR of 9.8% in the coming years.

Anastomosis Devices Market Regional Outlook

By geography, the market is segregated into Europe, Asia Pacific, Latin America, North America, and the Middle East & Africa.

North America

North America Anastomosis Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the leading share in 2024, valuing at USD 1.79 billion, and also registered the highest share in 2025, with USD 1.93 billion. Market growth in the region is attributed to the higher prevalence of colorectal conditions and technological advancements.

U.S. Anastomosis Devices Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1.77 billion in 2026, accounting for roughly 34.9% of global market sales.

Europe

Europe is projected to record a growth rate of 8.0% in the coming years and reach a valuation of USD 1.37 billion by 2026. The region is estimated to witness considerable market growth due to rising investments in new product development and the growing incidence of age-related conditions.

U.K. Anastomosis Devices Market

The U.K. market in 2026 is estimated at around USD 0.23 billion, representing roughly 4.5% of global market revenues.

Germany Anastomosis Devices Market

Germany’s market is projected to reach approximately USD 0.31 billion in 2026, equivalent to around 6.1% of global market sales.

Asia Pacific

Asia Pacific is predicted to reach USD 1.16 billion in 2026 and hold the third-largest market position. Improving healthcare infrastructure, coupled with favorable investments by global market players, is also estimated to accelerate regional growth.

Japan Anastomosis Devices Market

The Japan market in 2026 is expected at around USD 0.20 billion, holding roughly 4.0% of global market revenues.

China Anastomosis Devices Market

The market in China is set to reach USD 0.39 billion in 2026, representing roughly 7.6% of global market sales.

India Anastomosis Devices Market

The India market in 2026 is predicted at around USD 0.26 billion, accounting for approximately 5.1% of global market revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are set to register moderate growth in the coming years. The Latin America market is anticipated to reach USD 0.32 billion in 2026. In the Middle East & Africa, the GCC is projected to reach a valuation of USD 0.06 billion in 2026.

South Africa Anastomosis Devices Market

The market in South Africa is expected to reach USD 0.03 billion in 2026, representing around 0.49% of global market revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Top Companies Emphasize Strategic Investments and Technological Advancements to Maintain Their Dominance

The global anastomosis devices market grasps a semi-consolidated market structure, establishing major producers, including Medtronic, Johnson & Johnson MedTech, Intuitive Surgical, B. Braun Melsungen AG, and Meril Life Sciences. Several planned efforts, including massive investments and product approvals, are boosting market share.

- For instance, in March 2025, RevMedica and Qaelon Medical announced a strategic partnership with each other for the development of advanced surgical stapling devices.

NiTi Surgical Solutions, Synovis Micro Companies, Alliance, Reach Surgical, and Frankenman International are other top players in the market. They concentrate on partnerships to fuel their market share.

LIST OF KEY ANASTOMOSIS DEVICE COMPANIES PROFILED

- Medtronic plc (Ireland)

- Johnson & Johnson (U.S.)

- Intuitive Surgical, Inc. (U.S.)

- Braun Melsungen AG (Germany)

- Meril Life Sciences Pvt. Ltd. (India)

- NiTi Surgical Solutions Ltd. (Israel)

- Synovis Micro Companies Alliance, Inc. (U.S.)

- Reach Surgical, Inc. (U.S.)

- Frankenman International Ltd. (China)

- Purple Surgical International Ltd. (U.K.)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Corza Medical announced the launch of its ophthalmic surgical suture for better surgical outcomes.

- March 2025: GT Metabolic Solutions, Inc. received FDA approval for its MagDI System. The new device is introduced to enable magnet-assisted surgeries.

- September 2022: Teleflex completed the acquisition of Standard Bariatrics. The company took this strategic step to consolidate its presence in stapling technology.

- March 2022: Panther Healthcare announced the launch of a powered surgical stapler. The new product offers automatic control of tissue compression.

- December 2021: Intuitive Surgical received FDA approval for its 8 mm SureForm 30 curved-tip stapler. The product can be utilized in pediatric, thoracic, gynecological, and urologic surgical procedures.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.5% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product, Mode, Application, End-User, and Region |

|

By Product |

|

|

By Mode |

|

|

By Application |

|

|

By End-User |

|

|

By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.72 billion in 2025 and is projected to reach USD 9.81 billion by 2034.

In 2025, the market value stood at USD 1.93 billion.

The market is expected to exhibit a CAGR of 8.5% during the forecast period of 2026-2034.

By product, the stapling devices segment is expected to lead the market.

Rising emphasis on minimally invasive surgical procedures, coupled with the rising prevalence of colorectal conditions, is driving market expansion.

Medtronic, Johnson & Johnson MedTech, Intuitive Surgical, B. Braun Melsungen AG, and Meril Life Sciences are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us