Anatomic Pathology Market Size, Share & Industry Analysis By Type (Products [Instruments {Microtomes, Tissue Processing Systems, Stainers, and Others} and Consumables] and Services), By Application (Disease Diagnosis, Drug Discovery, and Others), By Technique (Serology & Immunology, Coagulation Tests, Blood Routine Examination, and Others), By End User (Hospitals & ASCs, Clinical Laboratories, Blood Banks, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

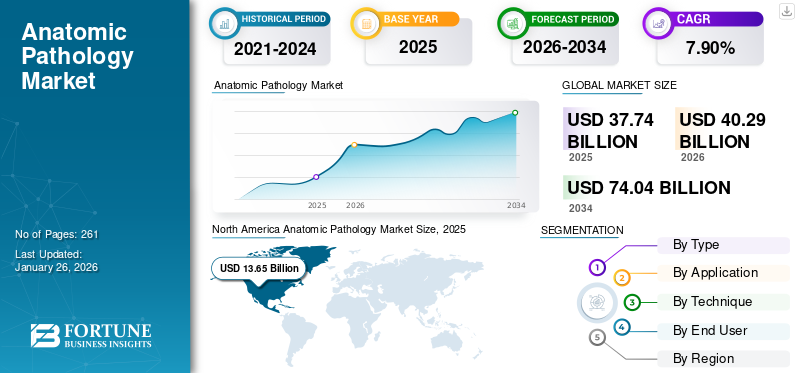

The global anatomic pathology market size was valued at USD 37.74 billion in 2025 and is projected to grow from USD 40.29 billion in 2026 to USD 74.04 billion by 2034, exhibiting a CAGR of 7.90% during the forecast period. North America dominated the anatomic pathology market with a market share of 36.18% in 2025.

Anatomic Pathology is a medical specialty that focuses on disease diagnosis through the examination of tissues, organs, and bodily fluids. The growing generality of chronic conditions, including cancer, inflammatory diseases, and others, is resulting in an increasing patient pool in healthcare settings globally. The rising number of patient admissions is further supporting the demand for histopathology, immunohistochemistry, and other tests, thereby driving the adoption rate of products and services in the market.

- For instance, according to data published by the American Cancer Society in 2025, approximately 2.0 million new cancer cases are estimated to occur in the U.S.

Moreover, the increasing strategic initiatives by governmental organizations to improve healthcare infrastructure and diagnostics are mostly to boost test volumes among the patient population in the market. Such initiatives are aimed at raising awareness about personalized medicine and companion diagnostics. This, coupled with a growing focus on research and development activities to develop and introduce novel instruments and consumables among key players, including Cardinal Health, F. Hoffmann-La Roche Ltd., and others, is expected to drive the market growth globally.

Download Free sample to learn more about this report.

Anatomic Pathology MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 37.74 billion

- 2026 Market Size: USD 40.29 billion

- 2034 Forecast Market Size: USD 74.04 billion

- CAGR: 7.90% from 2026–2034

- North America dominated the anatomic pathology market with a 36.18% share in 2025.

- Disease diagnosis segment led with a 71.64% share in 2026.

- Histopathology segment accounted for a 45.62% share in 2026.

North American

North America reached USD 13.65 billion in 2025, driven by strong diagnostic infrastructure and high test volumes.

Europe

The European region is projected to record a growth rate of 7.3% and reach a valuation of USD 9.98 billion in 2026.

Asia Pacific

Asia Pacific accounted for USD 11.07 billion in 2025, supported by rising chronic disease cases and expanding diagnostics access.

U.S.

Market estimated at USD 12.69 billion in 2026, supported by high pathology test volumes and advanced healthcare systems.

Japan

Growth supported by aging population and increasing demand for advanced diagnostic pathology services.

Read More

Market Dynamics

Market Drivers

Increasing Prevalence of Chronic Disorders to Augment Market Growth

The increasing prevalence of chronic conditions, such as inflammatory bowel diseases, autoimmune disorders, and cancer, among the patient population is supporting the growing demand for pathology tests. However, this is boosting the adoption rate of anatomic pathology products including stainers and tissue processing systems in the market.

- For instance, according to data published by the Centers for Disease Control & Prevention (CDC) in 2024, the prevalence of inflammatory bowel disease is estimated to be between 2.4 and 3.1 million in the U.S.

Moreover, the growing innovations in early detection and screening are enabling clinicians to diagnose suspicious lesions earlier among patients, which is boosting the number of anatomy pathology tests globally. This, along with the focus of key players on integrating technology such as artificial intelligence and digital pathology, among others, into their products, is further expected to augment the adoption and demand for these products in the market.

Therefore, the growing prevalence of chronic conditions is expected to drive the penetration rate, thereby contributing to the global anatomic pathology market growth. Other factors include the rising emphasis of prominent players toward research and development activities to launch innovative products and services.

Other Prominent Drivers

- Shift Toward Precision Medicine to Drive Market Growth: Integration of biomarker testing and molecular diagnostics with anatomic pathology enables more accurate and personalized treatment decisions.

- Expanding Healthcare Infrastructure to Fuel Market Growth: The growth in hospital networks, diagnostic centers, and laboratory modernization projects across the Asia Pacific, Middle East, and Latin America is boosting market penetration.

- Supportive Reimbursement and Screening Programs to Support Market Growth: Governments and insurers are expanding coverage for diagnostic tests, especially for cancer screening and histopathology services.

Market Restraints

High Cost Associated with Advanced Products to Limit Product Adoption

There are increasing technological advancements in anatomic pathology instruments, such as stainers, tissue processing systems, microtomes, and others. However, the high cost associated with these advanced devices is expected to hamper the demand and adoption of these devices in the market.

The high capital investment and integration costs associated with advanced technologies, such as molecular diagnostic platforms and whole-slide imaging (WSI) systems, make the adoption of these products challenging for small and mid-sized pathology laboratories. The additional operational costs, including slide preparation, quality control, and others, further contribute to the financial burden, thereby limiting the penetration rate of these devices, especially in emerging countries such as Brazil and Mexico.

- For instance, according to a 2020 study published by Europe PMC, it was reported that 93% of respondents believed that POCT could improve their care, and 56% identified having a POCT in their home as a top priority.

Therefore, all the above-mentioned factors, coupled with a stringent regulatory scenario for approving these products, are responsible for the reduced demand and adoption rate of these products, which is further expected to hinder market growth.

Market Opportunities

Rising Number of Oncology-Focused Clinical Trials to Create Market Opportunities

There is a growing number of research and development activities aimed at studying potential candidates to develop innovative drugs for chronic disorders, such as cancer and others. The clinical trials for cancer-based therapies such as immunotherapies, gene therapies, and others require strong biomarker assessment, tissue-based companion diagnostics, and histopathologic evaluation. This is further augmenting the demand for advanced molecular and digital platforms.

The increasing number of clinical trials is creating numerous opportunities for manufacturers and clinical laboratories to collaborate with contract research organizations that offer specialized testing services and infrastructure. These collaborations, along with technological advancements, accelerate the validation and approval of these products. However, it enables early access to novel drugs and thereby further augmenting demand for them in the market.

- According to data published by ScienceDirect, a significant rise in oncology research was observed, from 638 registered trials starting in 2000 to 6,571 in 2021.

Market Challenges

Limited Diagnosis in Developing Countries to Hinder Market Growth

There is a growing focus on strategic initiatives among governmental and non-governmental organizations to raise awareness about the early detection and monitoring of diseases among the patient population. However, there is an increasing prevalence of delayed diagnosis of chronic conditions owing to distinct factors. Such factors are delayed referrals of patients with chronic conditions, along with limited expertise among pathologists and histotechnologists to identify chronic diseases, especially in emerging countries.

Lack of clinical awareness, limited number of clinical laboratories and other healthcare settings, underequipped regional centers, inadequate access to reagents and quality control systems, among others, are some of the vital factors resulting in delayed specialist care, further leading to postponement of diagnosis among patients, especially in developing countries, such as India, Mexico, and South Africa, among others, thereby limiting the product adoption rate in the market.

- For instance, according to data published by Springer Nature in 2022, the density of pathologists is less than 4 per million population in Africa.

Other Prominent Challenges

- Regulatory Barriers Hinder Market Growth: New AI-based and molecular pathology solutions face lengthy validation and regulatory approval processes, which further slow commercialization.

- Emergence of Substitute Technologies to Limit the Market Growth: Non-tissue-based testing methods, such as liquid biopsies and advanced imaging, are beginning to complement or replace traditional pathology in selected areas.

- Inconsistent Reimbursement Policies Hamper Market Growth: Uneven insurance coverage for pathology tests in developing regions continues to hinder market growth.

Anatomic Pathology Market Trends

Growing Technological Advancements to Fuel Product Demand

There is an increasing focus on incorporating technological advancements into anatomic pathology devices, which is transforming the market landscape. The integration of artificial intelligence, digital pathology, molecular diagnostics, and other technologies is improving laboratory workflows, enhancing diagnostic accuracy, and expanding the clinical utility of pathology data. The growing number of benefits of the technology integration, such as digitization of glass slides, remote consultations, artificial intelligence based image analysis, improved tissue sampling, among others is supporting the penetration rate and demand, further driving the focus of key players toward R&D activities to develop and introduce advanced devices in the market, thereby expected to boost the adoption rate for these products in the market.

- According to data published by the Mayo Clinic in 2025, it was reported that more than 50% of surgical pathology cases were being digitized and interpreted by pathologists through digital pathology.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Increasing Number of Product Approvals to Led Products Segment Dominance

Based on type, the market is bifurcated into products and services. The market is further divided into instruments and consumables. Moreover, the instruments segment is classified into microtomes, tissue processing systems, stainers, and others.

The products segment is projected to dominate the market with a share of 63.13% in 2026. The growth is primarily driven by the increasing number of anatomic pathology tests, leading to a growing demand for technologically advanced devices worldwide. This, coupled with the growing focus of prominent players toward receiving product regulatory approvals, is further anticipated to support the segmental growth.

- In May 2024, Indica Labs, LLC., one of the players of digital pathology solutions, received U.S. FDA approval for HALO AP Dx, an enterprise digital platform for primary diagnosis with an aim to strengthen its product portfolio in the U.S. This approval enabled HALO AP Dx to be utilized in conjunction with the Hamamatsu NanoZoomer S360MD Slide scanner for in-vitro diagnostic use.

To know how our report can help streamline your business, Speak to Analyst

By Application

Increasing Prevalence of Chronic Diseases Led to Dominance of Disease Diagnosis Segment

Based on application, the market is classified into disease diagnosis, drug discovery, and others.

The disease diagnosis segment is expected to lead the market, contributing 71.64% globally in 2026. Further, in 2025, the segment is anticipated to dominate with a 71.6% share. The dominant share is owing to the growing prevalence of chronic conditions such as cancer, autoimmune disorders, further resulting in a growing number of anatomic pathology tests globally. This, along with increasing focus among prominent players toward mergers and collaborations to strengthen their presence, is anticipated to contribute to the segmental growth in the market.

- For instance, according to data published by the Australian Government, it was reported that an estimated 162,163 cancer cases were diagnosed in Australia in 2022.

The drug discovery segment is expected to grow at a CAGR of 7.7% over the forecast period.

By Technique

Growing Number of Histopathology Tests Led to Segment Dominance

On the basis of technique, the market is segmented into histopathology, immunohistochemistry (IHC), in-situ hybridization, molecular pathology, and others.

The histopathology segment will account for 45.62% market share in 2026. By technique, the histopathology segment accounted for a 45.9% share in 2024. The growth is owing to the increasing prevalence of chronic conditions such as cancer and infectious diseases, among others. It results in a growing number of histopathology slides being examined, thereby contributing to the growth of the segment.

- For instance, according to statistics published by the Royal College of Pathologists for 2025, around 20.0 million histopathology slides are examined each year in the U.K.

The segment of molecular pathology is poised for growth, with a forecasted rate of 8.3% across the period.

By End User

Increasing Number of Hospitals & ASCs Led to Segmental Dominance

Based on end user, the market is divided into hospitals & ASCs, specialty clinics, clinical laboratories, and others.

The hospitals & ASCs segment segment is expected to account for 56.54% of the market in 2026. The increasing prevalence of chronic diseases, a rising patient pool, and a growing number of hospitals are some of the crucial factors contributing to the segmental growth in the market. Furthermore, the segment is set to hold a 56.6% share in 2025.

- For instance, according to statistics published by the American Hospital Association (AHA) in 2025, there are approximately 6,093 hospitals in the U.S.

In addition, clinical laboratory end-users are projected to grow at a CAGR of 7.7% during the study period.

Anatomic Pathology Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Anatomic Pathology Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for USD 13.65 billion in 2025, representing 36.18% of the global market share, and is projected to reach USD 14.63 billion in 2026. The dominance of the region is attributed to several factors, including the growing prevalence of chronic disorders, the rising number of anatomic pathology tests, the development of healthcare infrastructure, adequate reimbursement policies, the increasing number of product approvals among prominent players, the growing adoption of technologically advanced devices, and others. In 2026, the U.S. market is estimated to reach USD 12.69 billion.

- For instance, according to data published by the Centers for Disease Control & Prevention (CDC) in 2024, approximately 350 million tests are performed annually in the U.S.

Europe

North America accounted for USD 13.65 billion in 2025, representing 36.18% of the global market share, and is projected to reach USD 14.63 billion in 2026. During the study period, the European region is projected to record a growth rate of 7.3% and reach a valuation of USD 9.98 billion in 2026. A growing number of test volumes and stringent regulatory standards are some of the factors supporting the rising focus of key players toward the introduction of novel products and services in the market. Other factors include widespread implementation of digital pathology systems, increasing demand for these products and services, improving healthcare access, and strategic government initiatives, among others. Backed by these factors, countries such as the U.K. are expected to record the valuation of USD 1.97 billion, Germany to record USD 2.2 billion in 2026, and France to record USD 1.71 billion in 2025.

Asia Pacific

In 2025, Asia Pacific held 29.33% of the global market, reaching a valuation of USD 11.07 billion, and is projected to grow to USD 11.78 billion in 2026. In the region, India is projected to reach USD 2.4 billion, while China is expected to reach USD 3.62 billion by 2026.

Latin America and the Middle East & Africa

The Latin America region captured 6.32% of the global market in 2025, generating USD 2.38 billion in revenue, and is projected to reach USD 2.53 billion in 2026. Middle East & Africa contributed approximately USD 1.3 billion to the global market in 2025, accounting for 3.45% share, and is expected to reach USD 1.38 billion in 2026. The growing prevalence of chronic diseases, rising awareness about early disease diagnosis, increasing healthcare modernization projects, and improvement in healthcare systems drive product adoption in these regions. In the Middle East & Africa, GCC is set to attain the value of USD 0.37 billion in 2025.

Competitive Landscape

Key Industry Players

Increasing Number of Product Launches Among Key Players to Contribute to Their Dominance

A robust and diversified product portfolio of technologically advanced anatomic pathology instruments, including whole-slide imaging systems, coupled with a significant global brand presence, is one of the crucial factors supporting the dominance of these players in the market. Cardinal Health, F. Hoffmann-La Roche Ltd., and Leica Microsystems are prominent players in the market in 2024. Moreover, the growing focus of key players on receiving product approvals for these products is anticipated to support the global anatomic pathology market share.

- For instance, in June 2024, F. Hoffmann-La Roche Ltd. received U.S. FDA approval for its whole-slide imaging system, the Roche Digital Pathology Dx (VENTANA DP 200), with the aim of strengthening its product portfolio globally.

Other key players, including Avantor, Inc., and others, are also growing in the market, owing to their growing strategic initiatives toward expanding their geographical presence in the emerging countries to strengthen their brand presence in the market.

List of Key Anatomic Pathology Companies Profiled

- Cardinal Health (U.S.)

- Hoffmann-La Roche Ltd. (Switzerland)

- Avantor Inc. (U.S.)

- Danaher Corporation (U.S.)

- SLMP, LLC. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Indica Labs, LLC. (U.S.)

- Hologic, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2025 – Labcorp collaborated with F. Hoffmann-La Roche Ltd., to implement the company's FDA-cleared VENTANA DP 600 and DP 200 slide scanners with an aim to support the diagnosis of chronic conditions among patients.

- September 2025 – StatLab Medical Products, a subsidiary of SLMP, LLC, launched PiSmart S1 single-hopper slide printer with an aim to strengthen its product portfolio.

- July 2025 – PathAI, one of the global players in artificial intelligence and digital pathology solutions, launched its Precision Pathology Network (PPN), a digital anatomic pathology laboratories network powered by PathAI’s AISight 1 Image Management System (IMS).

- March 2025 – Techcyte launched Fusion, a standards-based SaaS platform designed to unify anatomic and clinical pathology workflows, aiming to strengthen its product portfolio.

- August 2024 – StatLab Medical Products, a subsidiary of SLMP, LLC, acquired Diapath S.p.A., a prominent player in histology and cytology products and equipment, with an aim to strengthen its presence in the anatomic pathology market.

REPORT COVERAGE

The market report provides a detailed global anatomic pathology market analysis, focusing on key aspects such as leading companies, types, applications, techniques, and end-users. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.90% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Type

By Application

By Technique

By End User

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 37.74 billion in 2025 and is projected to reach USD 74.04 billion by 2034.

In 2025, the North America regional market value stood at USD 13.65 billion.

Growing at a CAGR of 7.90%, the market will exhibit steady growth over the forecast period.

By type, the products segment is the leading segment in this market.

The introduction of technologically advanced products is one of the major factors driving the market's growth.

Cardinal Health and F. Hoffmann-La Roche Ltd., are the major players in the global market.

North America dominated the anatomic pathology market with a market share of 36.18% in 2025.

The growing prevalence of chronic disorders, increasing technological advancements in devices, and others are some of the vital factors anticipated to fuel the adoption of these products worldwide.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us