Animal Intestinal Health Market Size, Share & Industry Analysis, By Product Class (Probiotics, Prebiotics, Phytogenics, Organic Acids & Acidifiers, Digestive Enzymes, Immunostimulants), By Application (Feed Efficiency, Diarrhea & Scours, Enteric Pathogen Control, Dysbiosis, Weaning Stress, Gut Barrier & Immunity), By Animal Type ( Swine, Poultry, Bovine, Equine, Aquaculture, Canine), By Product Form (Powder, Granules, Liquid, Paste, Tablets), By Source (Microbial, Plant, Organic Acid/Chemical), By End User (Feed Mills, Producers, Clinics, Pet Owners), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

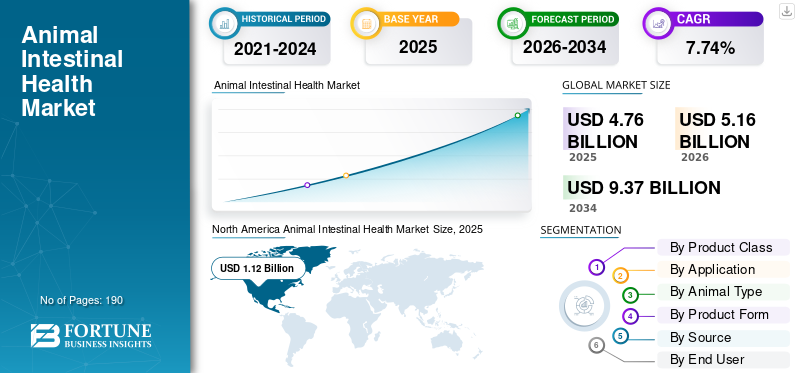

Animal Intestinal Health Market Overview

The global animal intestinal health market size was valued at USD 4.76 billion in 2025. The market is projected to grow from USD 5.16 billion in 2026 to USD 9.37 billion by 2034, exhibiting a CAGR of 7.74% during the forecast period. North America dominated the animal intestinal health market with a market share of 23.52% in 2025.

The global animal intestinal health market comprises products and solutions that improve gut balance, nutrient absorption, immunity, and overall digestive performance in animals. The market is gaining stronger importance as livestock, poultry, aquaculture, and companion animal producers focus on preventive health, better feed conversion, and reduced use of antibiotic growth promoters. Still, intensive farming, disease pressure, feed-cost volatility, and concerns about antimicrobial resistance continue to challenge animal productivity. Also, companies are placing greater focus on probiotics, postbiotics, organic acids, enzymes, phytogenic additives, and other gut-health solutions that help animals maintain stronger intestinal function, improve performance, and reduce health-related production losses.

Key companies such as Cargill Incorporated, DSM-Firmenich, Novozymes A/S, and Evonik Industries AG are expanding their offerings to boost their market positions.

- For instance, in November 2025, Evonik Industries AG showcased an enhanced version of Ecobiol at Poultry India 2025. The updated probiotic for poultry features an optimized outgrowth profile for faster onset of activity, supporting its focus on sustainable poultry production and improved gut-health performance.

Download Free sample to learn more about this report.

ANIMAL INTESTINAL HEALTH MARKET TRENDS

Expansion of Enzyme-Based Feed Solutions for Improved Nutrient Utilization is an Emerging Trend Observed

The global market is witnessing rising adoption of enzyme-based feed gut health solutions as producers seek better nutrient release, improved feed conversion, and lower feed wastage. Feed costs remain one of the largest expenses in livestock and poultry production, so enzymes are becoming important as they help animals digest complex feed ingredients more efficiently. This improves nutrient availability, supports gut function, and can reduce undigested nutrients that may disturb intestinal balance. As a result, feed enzyme solutions are increasingly used alongside probiotics, organic acids, and other gut health additives to support productivity, sustainability, and healthier animal performance.

- For instance, in January 2026, AB Vista showcased Ultra-25 D, a 25-hydroxy vitamin D₃ source and metabolite of vitamin D. Ultra-25 D offers higher bioavailability than traditional vitamin D₃, allowing producers to use less while maintaining performance. Such developments expand the company’s presence across the animal biosolutions value chain, underscoring how feed enzymes are becoming a strategic focus area in animal nutrition and gut health.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Livestock Production to Meet Global Protein Demand is Driving Market Growth

The market is growing as livestock producers increase output to meet rising demand for meat, milk, eggs, and aquaculture products. Higher animal production creates more pressure on farms to improve feed conversion, reduce disease-related losses, and maintain stronger digestive performance across large herds and flocks. Since gut health directly affects nutrient absorption, immunity, growth rate, and productivity, producers are increasingly adopting probiotics, enzymes, organic acids, postbiotics, and other intestinal health additives. As a result, rising animal protein demand is creating steady demand for gut-health solutions that help producers improve performance while using feed and natural resources more efficiently.

- For instance, in February 2025, Novonesis acquired DSM-Firmenich’s share of the Feed Enzyme Alliance for USD 1.70 billion. The growing global protein demand, along with increasing land and water scarcity, requires innovative solutions, and the acquisition would strengthen its position across the animal biosolutions value chain.

MARKET RESTRAINTS

High Cost of Specialty Gut-Health Additives Limits Wider Adoption to Restrain Market Growth

The major restraint faced by the global market is the high cost of specialty gut-health additives and advanced enzyme solutions. These gut health products often need specialized strains, controlled fermentation, encapsulation, stability testing, and species-specific validation, which increases production and formulation costs. As feed already accounts for a major share of livestock production costs, small and medium producers may delay adoption when product benefits are not immediately visible or when meat, milk, egg, or aquaculture margins are under pressure. This creates a cost-benefit challenge as larger commercial farms can more easily justify premium gut-health additives, while price-sensitive farms may continue using lower-cost conventional feed additives.

- For instance, a 2024 review on phytogenic feed additives highlighted that developing plant-derived antibiotic alternatives for livestock still faces challenges around sustainability, safety, and affordability, showing that cost and affordability remain practical barriers to the wider use of natural gut-health additives in animal production.

MARKET OPPORTUNITIES

Expansion of Probiotics and Postbiotics in Animal Feed Creating Growth Opportunities

A significant global animal intestinal health market growth opportunity is the rising use of probiotics and postbiotics in animal feed. As producers look for safer, more consistent ways to improve gut balance, immunity, and animal performance, demand for them is also rising. Probiotics help support beneficial gut bacteria, while postbiotics provide stable microbial-derived compounds that are easier to handle during feed processing and storage. This is becoming important as farms are under pressure to reduce antibiotic use, manage early-life stress, and improve feed conversion without affecting productivity. As a result, feed companies are expanding probiotic and postbiotic portfolios for poultry, swine, ruminants, aquaculture, and companion animals, creating new opportunities for differentiated gut-health products.

- For instance, in June 2025, DSM-Firmenich Animal Nutrition & Health launched the GutServ Biotix, a postbiotic solution designed to support piglet health, resilience, and performance, especially during stressful early-life stages such as weaning. The launch highlighted how companies are using postbiotic innovation to strengthen gut integrity and improve long-term animal performance.

MARKET CHALLENGES

Inconsistent Field Performance and Cost Pressure Limiting Farmer Confidence Remain a Key Market Challenge

A key challenge for the global market is inconsistent product performance across different farm conditions. Gut-health additives such as probiotics, phytogenic additives, organic acids, and enzymes can deliver strong benefits. Still, their results often depend on animal species, age, feed composition, disease pressure, storage stability, and farm management practices. This makes it difficult for producers to see the same level of improvement across all production systems. Additionally, many advanced gut-health products incur higher formulation and validation costs, which can reduce adoption among price-sensitive livestock producers. As a result, companies must invest more in species-specific trials, stable formulations, and clear return-on-investment data before farmers widely adopt these products.

- For instance, in October 2025, a review published titled ‘ The Role of Probiotics in Enhancing Animal Health: Mechanisms, Benefits, and Applications in Livestock and Companion Animals ’ highlighted that probiotics still face challenges such as strain-specific efficacy variation, regulatory limitations, and cost-effectiveness concerns in large-scale use, which directly reflects the market challenge of proving consistent and affordable gut-health benefits across commercial animal production systems.

Segmentation Analysis

By Product Class

High Commercial Acceptance of Probiotics Supporting Gut Health Led Segmental Growth

Based on product class, the market is categorized into probiotics, prebiotics, phytogenics/botanicals, organic acids & acidifiers, digestive enzymes, immunostimulants/gut barrier support products, and others.

The probiotics segment dominated the animal intestinal health market share. These probiotics are widely used to support gut microbiota balance, immunity, feed conversion, and disease resistance. Their adoption is increasing as producers move away from antibiotic growth promoters and seek preventive feed solutions to improve animal performance. Also, they have strong commercial acceptance, as they can be used in feed, water, premix, and pet supplement formats, making them more flexible than many other gut-health products and a core part of animal intestinal health programs.

- For instance, in April 2026, IFF launched PureStrong, a new probiotic developed exclusively for canine digestive health—such developments to drive growth in the segment.

The prebiotics segment is expected to grow at a CAGR of 8.67% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

New Product Launches in Feed Efficiency Propelled Growth in Segment

Based on application, the market is segmented into feed efficiency, diarrhea & scours, enteric pathogen control, dysbiosis, weaning stress, gut barrier & immunity, and others.

In 2025, the feed efficiency segment dominated the market. The high share is allocated to feed efficiency as gut-health products help animals extract more nutrients from feed and convert those nutrients into weight gain, milk, eggs, or meat more efficiently. Feed is one of the largest cost components in animal production, prompting producers to prioritize solutions that improve digestion, reduce waste, and maintain gut balance under intensive farming conditions.

- For instance, in October 2025, Bioiberica launched three new products in its Nucleoforce range for science-backed animal immune and intestinal health. The solutions of Nucleoforce Immunity, Nucleoforce Performance, and Nucleoforce High Flowability (HF) target immune and intestinal health in the pet, livestock, and aquaculture markets.

The gut barrier & immunity segment is projected to grow at a CAGR of 9.00% during the forecast period.

By Animal Type

Strong Focus on Expanding Poultry Production Boosted Segmental Growth

Based on animal type, the market is segmented into swine, poultry, bovine, equine, aquaculture, canine, and others.

In 2025, the poultry segment accounted for the largest share of the market. Poultry production is highly intensive and has short production cycles. The production depends strongly on feed conversion, gut integrity, and flock uniformity. Broilers and layers are more sensitive to digestive imbalance, pathogen pressure, and feed changes. Thus, to maximize production, producers regularly use probiotics, enzymes, organic acids, and phytogenic additives. Poultry also faces strong global demand, which further pushes integrators to adopt scalable gut-health solutions.

- For instance, in January 2025, IFF launched Enviva DUO, a direct-fed microbial (DFM) solution for poultry production. This blend of two non-spore-forming bacterial strains is designed to support the growth of beneficial gut bacteria during challenging conditions and to encourage a favorable nutribiotic state for the interaction among nutrition, the microbiome, and gut and immune function.

The aquaculture segment is projected to grow at a CAGR of 10.26% during the forecast period.

By Product Form

Compatibility with Dry Formulations Strengthened their Commercial Importance and Boosted Dry Powder/Premix Segmental Growth

Based on product form, the market is segmented into dry powder/premix, granules/pellets, liquid, paste/gel, tablets/capsules, and others.

In 2025, the dry powder/premix segment accounted for the largest share of the market. Most commercial gut-health additives are incorporated directly into feed through premixes, concentrates, and compound feed offered in dry/ powder form. The form is easier for feed mills and integrators to handle, dose, blend, store, transport, and scale across large animal populations. Dry formulations are also more compatible with probiotics, enzymes, organic acids, yeast derivatives, and phytogenic products when stability and uniform distribution are required. As a result, dry powder and premix formats remain the preferred commercial routes for broad adoption across livestock and poultry.

- For instance, in May 2026, Jaguar Health, Inc. launched Neonorm Dog, a new extension of the Company's Neonorm franchise for companion animals. Neonorm Dog was designed to provide dog owners with access to a plant-based, non-prescription product intended to support normal stool formation, gut hydration, and bowel health. These plant-based products are developed to support proper hydration and bowel health in pre-weaned foals and calves. Neonorm products contain a standardized botanical extract derived from the sustainably harvested Croton lechleri tree, which acts locally in the gut.

The tablets/capsules segment is projected to grow at a CAGR of 9.96% during the forecast period.

By Source

Increasing Importance of Microbial-Derived Products in Gut Health Boosted Segmental Growth

Based on source, the market is segmented into microbial-derived, plant-derived, organic acid/chemical-derived, and others.

In 2025, microbial-derived products dominated the source segment as probiotics, postbiotics, yeast derivatives, and microbial enzymes are a major part of intestinal health solutions used in modern animal nutrition. These products directly support gut microbiota balance, immune function, nutrient digestion, and resilience under stress conditions. These solutions also have strong scientific and commercial acceptance as companies can develop specific strains and formulations for poultry, swine, ruminants, pets, and aquaculture. As a result, microbial-derived ingredients are expected to remain the leading source category in the market.

- For instance, in March 2025, IFF extended its three-strain Bacillus probiotic Enviva PRO to pigs, highlighting that the product supports optimal gut function, nutrient digestion, performance, and reduced diarrhea frequency in post-weaning piglets.

The plant-derived segment is projected to grow at a CAGR of 8.32% during the forecast period.

By End User

High Volume Utilization by Feed Mills & Integrators Segment Led to Dominance in Market

Based on end user, the market is segmented into feed mills & integrators, livestock producers/farms, veterinary clinics & hospitals, pet owners, aquaculture producers, and others.

By end user, the feed mills & integrators segment dominated the market. The segment dominated as they purchase and apply gut-health additives at scale across large livestock and poultry production systems. These users can blend probiotics, enzymes, organic acids, and phytogenic products into feed more consistently than individual farms, which improves dosage accuracy, cost efficiency, and product reach. Integrators also have stronger technical teams and performance monitoring systems, so they are more likely to adopt validated gut-health solutions.

- For instance, in 2025, Kemin expanded the availability of CLOSTAT across the entire pig production cycle, noting that the probiotic supports microbiome management, preventive intestinal health, reduced reliance on antibiotics, and improved performance from farrowing to finishing.

The others segment is projected to grow at a CAGR of 6.84% over the projected period.

Animal Intestinal Health Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Animal Intestinal Health Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 1.05 billion and maintained its leading position in 2025 at USD 1.12 billion. The market is growing in North America as livestock and poultry producers increasingly adopt probiotics, enzymes, postbiotics, and organic acids to improve feed efficiency and reduce reliance on antibiotics. Strong commercial farming systems and rising demand for antibiotic-free meat and dairy products are supporting wider use of gut-health additives.

U.S. Animal Intestinal Health Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 1.11 billion in 2026, accounting for roughly 21.58% of the global market.

Europe

Europe is projected to grow at 6.78% over the coming years, the second-highest among all regions, and reach a valuation of USD 1.26 billion by 2026. The European market is anticipated to grow due to a strict focus on antimicrobial reduction, animal welfare, and sustainable livestock production.

U.K. Animal Intestinal Health Market

The U.K. market is estimated at around USD 0.15 billion in 2026, representing roughly 2.90% of the global market.

Germany Animal Intestinal Health Market

Germany's market is projected to reach approximately USD 0.24 billion in 2026, equivalent to around 4.67% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 2.03 billion in 2026 and secure the position of the third-largest region in the market. Asia Pacific is growing strongly owing to large poultry, swine, dairy, and aquaculture populations, along with rising meat, egg, milk, and seafood consumption. This creates a higher need for gut-health products that improve disease resistance, feed conversion, and farm productivity.

Japan Animal Intestinal Health Market

The Japanese market is estimated at around USD 0.19 billion in 2026, accounting for approximately 3.59% of the global market.

China Animal Intestinal Health Market

China's market is projected to be one of the largest globally, with 2026 revenues estimated at around USD 0.67 billion, representing approximately 12.97% of global sales.

India Animal Intestinal Health Market

The Indian market is estimated at around USD 0.34 billion in 2026, accounting for roughly 6.53% of global revenue.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The market in Latin America is estimated to reach a valuation of USD 0.43 billion in 2026. Latin America is witnessing growth, with the rising adoption of feed additives helping producers improve gut health, animal performance, and feed utilization.

Middle East & Africa Animal Intestinal Health Market

The GCC is set to reach USD 0.08 billion in 2026.

South Africa Animal Intestinal Health Market

The South African market is projected to reach approximately USD 0.03 billion by 2026, accounting for roughly 0.56% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

New Product Launches by Key Players to Propel Market Progress

The global animal intestinal health market is moderately consolidated, with large multinational feed and biosolution companies leading through global distribution, strong R&D, and broad species coverage. Companies such as Cargill, Incorporated, Novozymes A/S, Evonik Industries AG, Kemin Industries, Inc. have an advantage as they can supply feed mills, integrators, livestock producers, and aquaculture customers at scale. Their leading position is supported by science-backed probiotics, postbiotics, enzymes, yeast derivatives, organic acids, and phytogenic solutions that directly address feed efficiency, antibiotic reduction, gut microbiota balance, and animal performance.

- For instance, in July 2022, Kemin Industries launched ENTEROSURE to control the growth of pathogenic bacteria in poultry and livestock. The probiotic solution promotes a healthy microbiome, drives intestinal resilience, manages gut health challenges, and improves animal productivity.

Other notable players in the global market include ADM, Alltech, IFF., and BASF SE. New products are focusing on postbiotics, heat-stable probiotics, waterline-applied direct-fed microbials, optimized enzyme systems, and lifecycle-based gut-health programs. As a result, companies that can prove consistent field performance, feed-processing stability, and measurable return on investment are expected to gain stronger market share over the forecast period.

LIST OF KEY ANIMAL INTESTINAL HEALTH COMPANIES PROFILED IN REPORT

- Cargill, Incorporated (U.S.)

- dsm-firmenich (Switzerland)

- Novozymes A/S (Denmark)

- Evonik Industries AG (Germany)

- Kemin Industries, Inc. (U.S.)

- ADM (U.S.)

- Alltech (U.S.)

- International Flavors & Fragrances Inc. (U.S.)

- Nutreco (The Netherlands)

- BASF SE. (Germany)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Lallemand Animal Nutrition launched LEVUCELL Trivantage, a feed supplement for dairy, beef, and equine nutrition in the U.S. The launch expanded microbial-based gut-health solutions for ruminants and equine producers seeking simpler feed programs.

- June 2024: IFF received EU-wide regulatory approval and expanded launch of Axtra XAP and SyncraAVI for poultry feed. Syncra AVI is an enzyme-probiotic complex designed to improve poultry performance and feed efficiency. This strengthened the use of combined enzyme and probiotic solutions for poultry gut-health and productivity programs.

- March 2024: Novus International, Inc. acquired BioResource International, Inc., including enzyme and direct-fed microbial products such as CIBENZA and EnzaPro. The development strengthened the company’s portfolio, innovation pipeline, fermentation capabilities, and gut-health segment.

- January 2023: Nutreco collaborated with BiomEdit to develop next-generation feed additives using microbiome technology. The collaboration focused on Biome-actives for aquaculture, poultry, swine, and cattle. This created a platform for future microbiome-based gut-health additives across livestock and aquaculture.

- June 2020: DSM-Firmenich acquired Erber Group, including Biomin and Romer Labs, for an enterprise value of USD 1,113.6 million. Biomin’s specialty animal nutrition business included gut health performance management, mycotoxin risk management, and feed safety solutions. The acquisition expanded DSM’s specialty animal nutrition and health portfolio.

REPORT COVERAGE

The global animal intestinal health market report covers products and solutions used to improve digestive balance, nutrient absorption, gut microbiota, immunity, and overall animal performance. The report provides a detailed global analysis of the market by product class, application, animal type, product form, source, end user, and region. It studies the role of gut-health solutions in improving feed conversion, reducing diarrhea and scours, controlling enteric pathogens, managing dysbiosis, supporting weaning stress, and strengthening gut barrier function. As a result, the report helps identify which product categories and animal groups are likely to generate stronger demand, where companies are investing in innovation, and how feed mills, livestock producers, veterinary clinics, pet owners, and aquaculture producers are adopting intestinal-health products.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.74% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Class, Application, Animal Type, Product Form, Source, End User, and Region |

| By Product Class |

|

| By Application |

|

| By Animal Type |

|

| By Product Form |

|

| By Source |

|

| By End User |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.76 billion in 2025 and is projected to reach USD 9.37 billion by 2034.

In 2025, the market value stood at USD 1.12 billion.

The market is expected to grow at a CAGR of 7.74% over the forecast period of 2026-2034.

The probiotics product class segment is expected to lead the market.

Rising livestock production to meet global protein demand is driving market growth.

Cargill, Incorporated, DSM-Firmenich, Novozymes A/S, Evonik Industries AG, and Kemin Industries, Inc. are the top players in the market.

North America held the largest global market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us