Apoptosis Assays Market Size, Share & Industry Analysis, By Product Type (Instrument, Kits, and Standalone Reagents & Consumables), By Assay Type (Caspase Activation Assays, Annexin V–Based Assays, DNA Fragmentation (TUNEL) Assays, Mitochondrial Dysfunction Assays, and Others), By Detection Technology (Flow Cytometry, Fluorescence Microscopy, Spectrophotometry, and Others), By End-user (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Hospitals & Clinical Research Laboratories, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

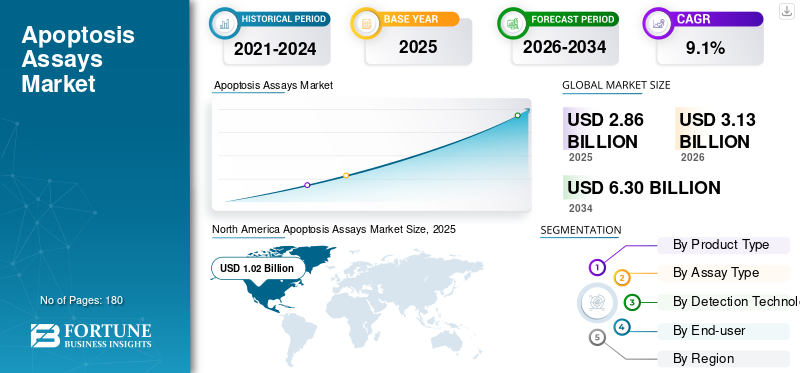

The global apoptosis assays market size was valued at USD 2.86 billion in 2025. The market is projected to grow from USD 3.13 billion in 2026 to USD 6.30 billion by 2034, exhibiting a CAGR of 9.1% during the forecast period. North America dominated the apoptosis assays market with a market share of 35.66% in 2025.

Apoptosis assays include tools such as kits, standalone reagents & consumables, and instruments used to detect and quantify programmed cell death. These assays provide readouts that include phosphatidylserine externalization (Annexin V), caspase activation, DNA fragmentation (TUNEL), and mitochondrial dysfunction. The market growth is attributed to the rising demand for apoptosis assays as research tools for detecting programmed cell death in preclinical studies, drug screening, and high-throughput investigations across oncology, autoimmune diseases, and toxicology.

Furthermore, Thermo Fisher Scientific Inc., Merck KGaA, Danaher, and Revvity accounted for the majority of the market share due to their strong supply network and global reach, with offices in both developed and developing countries.

Download Free sample to learn more about this report.

APOPTOSIS ASSAYS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 2.86 Billion

- 2026 Market Size: USD 3.13 Billion

- 2034 Forecast Market Size: USD 6.30 Billion

- CAGR: 9.1% from 2026–2034

- North America dominated the apoptosis assays market with a 35.66% share in 2025.

- The flow cytometry segment is projected to hold 35.2% of the market in 2026.

- The pharmaceutical & biotechnology companies segment is projected to account for 42.6% of the market in 2026.

North America

North America reached USD 1.02 billion in 2025, accounting for 35.66% of global market revenue.

Asia Pacific

Asia Pacific is projected to reach USD 0.99 billion by 2026, ranking as the second-largest regional market.

Europe

Europe is projected to reach USD 0.74 billion by 2026, growing at a CAGR of 8.0%.

U.S.

The market is projected to reach USD 0.98 billion by 2026, accounting for 31.4% of global revenue.

Japan

The market is projected to reach USD 0.20 billion by 2026, representing 6.4% of global revenue.

Read More

APOPTOSIS ASSAYS MARKET TRENDS

Workflow Automation Across Laboratories to Emerge as a Key Market Trend

Currently, there has been a shift toward workflow automation, including sample preparation, acquisition templates, and cloud-based analysis/reporting. This has enhanced reproducibility in screening, thereby reducing dependency on individual researchers.

In response, key players are launching advanced instruments that differentiate on throughput, automation hooks, and integrated analytics, making apoptosis panels easier for non-expert labs.

- For instance, in June 2023, BD launched the BD FACSDuet Premium System, a robotic tool automating sample preparation for clinical flow cytometry

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Drug Discovery, Toxicology, and Cell Therapy Applications to Drive the Market Growth

In recent years, the requirement for apoptosis assays has been increasing among pharmaceutical industry & biotechnology companies. These assays provide a fast and interpretable efficacy/toxicity readout across 2D/3D models and high-throughput screens in drug discovery and other applications.

Additionally, the growing demand for standardized assays with reproducible analysis among pharmaceutical companies is driving the adoption of validated apoptosis kits, as well as cytometry platforms and cloud-based analysis solutions. As a result, key players are being involved in collaborations with life science companies to support workflows, thereby augmenting the global apoptosis assays market growth.

- For instance, in August 2022, BD collaborated with Labcorp to develop, manufacture, and commercialize flow cytometry-based companion diagnostics for matching cancer patients with targeted treatments.

MARKET RESTRAINTS

Data Variability and Protocol Sensitivity Across Labs to Restrict Market Growth

In several scenarios, the apoptosis readouts diverge sharply depending on the cell type, staining conditions, fluorophore choices, timing, compensation, and whether the assays capture early or late apoptosis.

This has made cross-study comparability difficult and increased repeat runs. As a result, many buyers are hesitant to expand assay breadth, as method harmonization is time-consuming in regulated environments. Such a scenario is anticipated to hinder the market expansion over the forecast period.

MARKET OPPORTUNITIES

Multiplexed, High-Content Apoptosis Profiling to Offer Lucrative Growth Opportunities

In recent years, there has been a surge in pairing apoptosis with phenotyping, metabolic state, and internalization in the same experiment. Additionally, the imaging-enabled flow and spectral platforms are expected to support more comprehensive characterization of apoptosis.

This is anticipated to offer a significant opportunity for key players to launch an instrument with advanced imaging capabilities, thereby broadening the adoption of screening formats across oncology and immunology research.

- In June 2021, Thermo Fisher Scientific Inc. launched the Invitrogen Attune CytPix Flow Cytometer, which combines acoustic focusing flow cytometry with high-speed imaging for the analysis of fluorescent data and brightfield cell morphology.

MARKET CHALLENGES

High Cost of Instrument to Challenge Market Expansion

Typically, advanced instruments such as Flow cytometers, fluorescence microscopes, and high-content systems are expensive. Additionally, the maintenance and upgrades add high costs, increasing overall expenses.

- For instance, in December 2025, LabX mentioned that the price of flow cytometers ranges from USD 50,000 to 500,000, depending on the features.

These higher costs are limiting their adoption in academic labs, small biotechs, and emerging countries, which is expected to challenge market expansion in the coming years.

Segmentation Analysis

By Product Type

Benefits Such as Reproducibility to Drive Kits Segment Growth

Based on product type segmentation, the market is segmented into instruments, kits, and standalone reagents & consumables.

To know how our report can help streamline your business, Speak to Analyst

The kits segment accounted for the major market share in 2025. The kits improve reproducibility as compared to assembling reagents. As a result, the “one box” kits are highly preferred, where timing, temperature, and staining conditions strongly affect the outcome. This is expected to drive the segment’s growth during the forecast period.

In addition, the standalone reagents & consumables segment is projected to grow at a CAGR of 9.4% during the forecast period.

By Assay Type

Wide Usage of Caspase Activation Assays in Primary Screening to Drive the Caspase Activation Segment Growth

By assay type, the market is categorized into caspase activation assays, annexin V-based assays, DNA fragmentation (TUNEL) assays, mitochondrial dysfunction assays, and others.

The caspase activation assays segment held the largest market share in 2025. The segment’s growth is attributed to the widespread use of caspase activation assays as primary screening readouts in drug discovery. Additionally, these assays are homogeneous and plate-friendly, which is further driving their adoption. Moreover, the segment is projected to hold a 36.3% share in 2026.

Additionally, the annexin V-based assays segment is estimated to grow at a CAGR of 9.4% during the forecast period.

By Detection Technology

Rising Apoptosis Assay Demand and Frequent Product Launches Drives Flow Cytometry Segment Growth

By detection technology, the market is categorized into flow cytometry, fluorescence microscopy, spectrophotometry, and others.

The flow cytometry segment held the largest market share in 2025. The segment’s growth is attributed to the increasing number of product launches by key players, driven by the growing significance of apoptosis assays in measuring heterogeneous responses in populations. Moreover, the segment is projected to hold a 35.2% share in 2026.

- For instance, in May 2025, Thermo Fisher Scientific Inc. launched the Invitrogen Attune Xenith Flow Cytometer, a spectral-enabled system for immunology and immuno-oncology research.

Additionally, the fluorescence microscopy segment is estimated to grow at a CAGR of 9.1% during the forecast period.

By End-user

Rising R&D Activity and Growing Pharma Presence Drives Pharmaceutical & Biotechnology Companies Segment Growth

On the basis of end-user, the market is classified into pharmaceutical & biotechnology companies, academic & research institutes, hospitals & clinical research laboratories, and others.

In 2025, pharmaceutical & biotechnology companies dominated the market by end-users. The segment’s growth is mainly due to the increasing number of pharmaceutical companies, which are driving R&D initiatives and increasing the need for apoptosis assays. Furthermore, the segment is set to hold a 42.6% share in 2026.

In addition, the academic & research institutes segment is projected to grow at a CAGR of 9.0% during the forecast period.

Apoptosis Assays Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Apoptosis Assays Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America held the major revenue in 2024 at USD 0.93 billion and reached USD 1.02 billion in 2025. The growth is mainly due to extensive NIH-funded academic research and the concentration of pharmaceutical companies in the region.

- For instance, in August 2025, Cross River Therapy reported that the U.S. hosts over 5,000 pharmaceutical companies.

U.S Apoptosis Assays Market

In 2026, the U.S. market is projected to account for USD 0.98 billion, holding 31.4% of the global market revenue.

Europe

Europe is projected to witness an 8.0% growth rate in the forthcoming years, the third-highest worldwide, reaching a value of USD 0.74 billion by 2026. Countries such as Germany, the U.K., and France are increasingly investing in translational research, oncology clinical trials, and toxicology testing, thereby driving the demand for apoptosis assays.

U.K Apoptosis Assays Market

The U.K. market is predicted to reach USD 0.14 billion by 2026, holding 4.5% of the global market revenue.

Germany Apoptosis Assays Market

Germany's apoptosis assays market is expected to hit approximately USD 0.15 billion by 2026, accounting for around 4.9% of the global revenue.

Asia Pacific

In 2026, the Asia Pacific is projected to reach the value of USD 0.99 billion, ranking as the second-largest region in the global market.

Japan Apoptosis Assays Market

Japan is anticipated to reach USD 0.20 billion in 2026, accounting for approximately 6.4% of the global revenue.

China Apoptosis Assays Market

China is set to reach a value of USD 0.38 billion by 2026, accounting for 12.1% share of the apoptosis assays market.

India Apoptosis Assays Market

India’s apoptosis assays market is projected to account for USD 0.11 billion by 2026, representing 3.6% share of the global industry.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa regions are expected to experience moderate growth in this market over the forecast period. Latin America’s market is projected to reach a value of USD 0.17 billion by 2026. The growth is attributed to increasing government support to improve the R&D scenario in these regions.

GCC Apoptosis Assays Market

GCC apoptosis assays market is anticipated to account for USD 0.08 billion by 2026, representing 2.4% share of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Broad Portfolio of End-to-End Solutions to Strengthen the Market Position of Key Players

In 2025, Thermo Fisher Scientific Inc., Merck KGaA, and Danaher accounted for the highest global apoptosis assays market share. The dominance is attributed to diversified portfolio of apoptosis assay kits, spanning reagents, and advanced instruments of these companies.

Other major players, including Revvity and BD, among others, are consistently launching new instruments and kits critical for pharma and CRO customers to increase their market share in a competitive environment.

LIST OF KEY APOPTOSIS ASSAYS COMPANIES PROFILED

- Thermo Fisher Scientific Inc. (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- BD (U.S.)

- Revvity (U.S.)

- Danaher (U.S.)

- Promega Corporation (U.S.)

- Takara Bio Inc. (Japan)

- Enzo Biochem Inc. (U.S.)

- Biotium (U.S.)

- United States Biological (U.S.)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Revvity launched pHSense reagents to deliver accurate, high-throughput, and scalable insights in drug discovery internalization studies.

- November 2024: Revvity, in collaboration with Scale Biosciences, launched the TotalSeq Phenocyte solution for high-parameter single-cell protein profiling to identify rare cell subtypes in immunology and oncology research.

- March 2024: Beckman Coulter, Inc. launched the CytoFLEX nano flow cytometer for research use, including apoptosis assays.

- December 2023: Danaher completed the acquisition of Abcam plc to gain access to its apoptosis kits portfolio.

- September 2022: BD launched BD Research Cloud, a cloud-based software solution streamlining flow cytometry workflows for immunology, virology, oncology, and infectious disease research.

REPORT COVERAGE

The report provides a comprehensive analysis across all segments, encompassing key drivers, trends, opportunities, restraints, and challenges. It also provides key insights on technological advancements, new product launches, key industry developments, company market share analysis, and profiles of prominent companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.1% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Assay Type, Detection Technology, End-user, and Region |

|

By Product Type |

· Instrument · Kits · Standalone Reagents & Consumables |

|

By Assay Type |

· Caspase Activation Assays · Annexin V–Based Assays · DNA Fragmentation (TUNEL) Assays · Mitochondrial Dysfunction Assays · Others |

|

By Detection Technology |

· Flow Cytometry · Fluorescence Microscopy · Spectrophotometry · Others |

|

By End-user |

· Pharmaceutical & Biotechnology Companies · Academic & Research Institutes · Hospitals & Clinical Research Laboratories · Others |

|

By Geography |

· North America (By Product Type, Assay Type, Detection Technology, End-user, and Country) o U.S. (Product Type) o Canada (Product Type) · Europe (By Product Type, Assay Type, Detection Technology, End-user, and Country/Sub-region) o Germany (Product Type) o U.K. (Product Type) o France (Product Type) o Spain (Product Type) o Italy (Product Type) o Scandinavia (Product Type) o Rest of Europe (Product Type) · Asia Pacific (By Product Type, Assay Type, Detection Technology, End-user, and Country/Sub-region) o China (Product Type) o Japan (Product Type) o India (Product Type) o Australia (Product Type) o Southeast Asia (Product Type) o Rest of Asia Pacific (Product Type) · Latin America (By Size, Procedure, End-user and Country/Sub-region) o Brazil (Product Type) o Mexico (Product Type) o Rest of Latin America (Product Type) · Middle East & Africa (By Product Type, Assay Type, Detection Technology, End-user, and Country/Sub-region) o GCC (Product Type) o South Africa (Product Type) o Rest of the Middle East & Africa (Product Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.86 billion in 2025 and is projected to reach USD 6.30 billion by 2034.

In 2025, the North America market value stood at USD 1.02 billion.

The market is expected to exhibit a CAGR of 9.1% during the forecast period of 2026-2034.

The kits segment led the market by product type in 2025.

The key factors driving the market are the expanding drug discovery applications and others.

Thermo Fisher Scientific Inc., Merck KGaA, and Danaher are some of the major players in the market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us