Architectural Services Market Size, Share & Industry Analysis, By Solution Type (Construction and Project Management, Urban Planning, Interior Design, Engineering Services, and Others), By End User (Residential, Government & Education, Healthcare, Manufacturing & Infrastructure, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

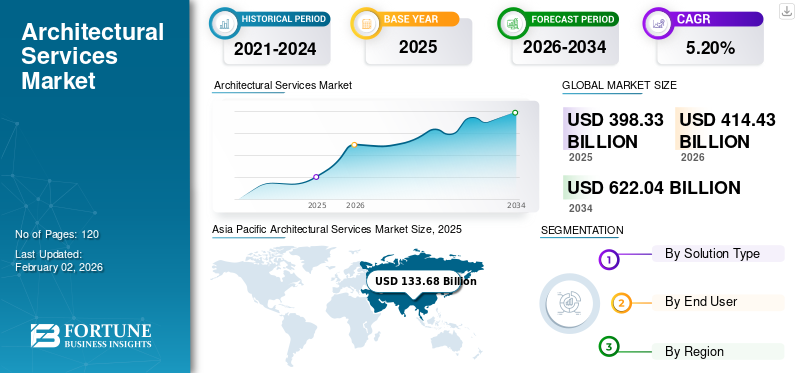

The global architectural services market size was valued at USD 398.33 billion in 2025 and is projected to grow from USD 414.43 billion in 2026 to USD 622.04 billion by 2034, exhibiting a CAGR of 5.20% during the forecast period. Asia Pacific dominated the global market with a share of 33.60% in 2025.

The market offers a wide array of professional services in many sectors, from planning and designing of construction projects to construction, project management, and specialist consultancy in areas including environmental sustainability and compliance with regulatory structures. A multitude of end-users arise, such as residential, commercial, government, and infrastructure sectors, with key drivers contributing to the need for innovative, functional, and sustainable buildings. Based on these trends, the market is expected to experience strong growth, arising from the growing rates of urbanization and increased demand for environmentally sustainable options, coupled with innovations in digital software and tools such as Building Information Modelling (BIM) and virtual reality.

Few major players in the market include global firms such as Gensler, AECOM, and Perkins&Will alongside local firms that have the scope to dominate local markets through specialist work, local knowledge, and expertise.

The COVID-19 pandemic disrupted the project timelines and created a lack of commercial projects; however, it also contributed to the increased uptake of online/remote collaboration and a renewed investment in sustainable designs. As economies reopened, opportunities for the recovery of the market grew, with a strong emphasis on resilient and adaptable architectural outcomes.

Download Free sample to learn more about this report.

IMPACT OF GENERATIVE AI

Generative AI Drives Transformation by Enhancing Efficiency, Fostering Innovation, and Promoting Sustainable Design Practices

Generative AI is transforming the global market for architectural partners, philanthropists, and related fields through increased efficiencies, innovation, and sustainability. By combining tools such as Autodesk Forma or DALL-E to assess and utilize a huge number of designs in seconds, evaluate their impact, optimize material usage, and provide real-time data, architects are able to develop energy-efficient solutions while promoting compliance. The advancement in technology is optimizing workflows, reducing timelines (i.e., volume studies in hours), and encouraging people to incorporate sustainable practices (provide evidence about environmental impact and recommendations for materials and eco-friendly products) aligned with the current global movement of green architecture. There are concerns amongst architects related to artificial intelligence replacing their jobs due to its ability to bring together exploration, creativity, and structural understanding and knowledge. However, the generative AI tool is not a threat, as it is a collaborative tool that supports outputs from the architects' experience and value. Additionally, the role of ethical consideration as it relates to data privacy and design disclosure or transparency must be assessed.

MARKET DYNAMICS

Architectural Services Market Trend

Rising Demand for Sustainable Materials and Smart Design for Efficient Construction

The market is adapting to new sustainable and smart design solutions due to the growing demand for sustainable buildings, and urban design is shifting to eco-friendly solutions. By using Building Information Modeling (BIM), generative AI designs, and virtual reality, different methods are being embedded into operations to speed up the design iteration process, as it provides a more sophisticated visualization of projects for the client.

The rise of modular construction using prefabricated parts to reduce budget and timeline aligns with sustainability goals. Growing smart city concepts, particularly in Asia Pacific and the Middle East regions, are also an emerging trend in the market. This is enabling architects to work in the data-driven design space and become a part of the ethnographic approach. It is also transitioning architects to tech-enabled designers rapidly.

Market Drivers

Urbanization and Environmental Awareness Boost Demand for Sustainable Architectural Solutions

Rapid urbanization, particularly in developing economies such as the Asia Pacific and the Middle East, drives the demand for new residential, commercial, and infrastructure projects as a result of increased population and urban migration. Factors such as government-led initiatives, including the smart city programs and affordable housing schemes, further expand the market as it focuses on innovative urban development and sustainable infrastructure.

Moreover, advancements in technology, such as generative AI and Building Information Modeling (BIM), have improved design integrity, compressed project timeframes, and opened up the prospect of data-driven solutions by stimulating demand, especially from clients seeking efficiency and cost savings. Growing environmental awareness has increased the demand for buildings that focus on green principles, with certifications including LEED and BREEAM becoming a necessity for end-users across the residential, healthcare, and public sectors. Additionally, an increase in spending on public infrastructure, including transportation and educational facilities, represents a lucrative growth, especially in the North American and European regions, indicating a continued architectural services market growth.

Market Restraints

Economic Volatility and Use of Outdated Technology Limit Market Growth

Many globally dispersed regulatory regimes (altering requirements for building codes, zoning plans, regulations, and others) make it difficult for architecture firms to manage the compliance processes and costs, causing delays. In addition, the market is also facing issues related to economic volatility, including the rising costs of construction materials, rising interest rates, and its impact on risk investment for clients, particularly in countries with unstable economic and currency conditions such as in South America. In addition to these economic restraints, different forms of technologies, such as generative AI, building information modeling, and virtual reality tools, has higher cost associated with its integration, which creates additional barriers for small and mid-sized firms to be competitive.

Another barrier to growth, particularly in developing regions such as Africa, is the shortage of trained architects and engineers who are capable of working with both traditional designs and new digital tools that are necessary for contemporary architectural services practice. Many firms continue to rely on outdated processes, creating resistance to adopting new methods. Additionally, concerns over data privacy discourage architects from using digital tools, slowing innovation and limiting market growth.

Market Opportunities

Labor Shortages and Cost Pressures Drive Off-Site Construction, Transforming Architectural Services Practices

The rise of modular and prefabricated construction can be attributed to several factors aimed at addressing traditional construction problems. In off-site construction, creating components such as modular or panel systems in a factory-controlled environment offers reduced construction time, better quality control, and less exposure to variables (such as weather). This, in turn, leads to greater consistency in the manufacturing process and better cost predictability. This efficiency appeals to industries facing labor shortages, rising material costs, and strict project deadlines, making modular construction and prefabricated solutions attractive for commercial, education, healthcare, and residential projects.

The shift toward off-site construction affects the market, requiring new skills, design approaches, and models from architects. Designing for modular or prefabricated systems requires a unique perspective. Architects need to emphasize standardization and modularity while ensuring coordination of the architectural design with the manufacturing process. This often requires preparation for connections between modules, transportation, and MEP systems in the factory building. Therefore, firms are developing these skills and increasingly investing in training and expertise to maintain a competitive advantage in the marketplace and respond to clients' demand for more efficient construction methodologies.

SEGMENTATION ANALYSIS

By Solution Type

Construction and Project Management Leads as they Deliver Large-Scale Projects on Time and Within Budget

The market is segmented by solution type into construction and project management, urban planning, interior design, engineering services, and others.

The construction and project management segment is projected to dominate the market with a share of 34.09% in 2026, mainly due to its predominant role in the overall coordination and successful delivery of large-scale residential, commercial, and infrastructure projects. This segment involves overseeing timelines, budgets, resource allocation, and quality control to ensure projects are completed efficiently and to client specifications.

Urban planning is experiencing substantial growth over the forecast period as governments and developers increasingly emphasize sustainable urban development and smart city projects, especially in urbanizing regions.

The interior design segment is anticipated to grow with the highest CAGR over the forecast period. This growth is driven by potential opportunities, largely due to users' demand for customized, attractive, and functional spaces in residential and commercial construction projects. This demand is further fueled by trends related to luxury and sustainability.

Engineering services is a crucial segment as larger projects require an expert to ensure the structural integrity of a project and provide technical expertise. Additionally, engineering services play a vital role in complex trades being used and integrated across all types of projects.

Other specialized services, such as architectural advisory, building code advice and consultation, advice on legal compliance requirements, and innovative new technologies such as BIM and AR/VR, fall into this category. These services contribute an unprecedented amount of revenue to expand, largely due to regulators’ needs, regulatory expertise on building regulations and legislation, and clients’ demand to incorporate new, higher technologies into their design work.

By End User

To know how our report can help streamline your business, Speak to Analyst

Manufacturing & Infrastructure Dominate due to Heavy Investments in Large-Scale Public Projects and Urban Development

The market is segmented by end user into residential, government & education, healthcare, manufacturing & infrastructure, and others.

The manufacturing & infrastructure segment is projected to dominate the market with a share of 35.05% in 2026. Its demand is driven by massive public infrastructure and industrial projects in urbanizing geographies that receive heavy investment for transportation and energy developments.

The residential segment is maintaining a positive growth as demand for housing drives employment and appears unaffected by recent economic turmoil. This is due to population growth and urbanization, which fuel demand for affordable housing to luxury or multi-family developments.

The government and education segment is anticipated to grow at the highest CAGR. This growth is driven by increasing public spending on educational facilities, smart cities, and sustainable public infrastructure, suggesting long-term investing for broader societal benefits. Demand for specialized healthcare buildings, including hospitals and clinics, is growing steadily due to aging populations and modernizing healthcare.

The others segment, which has specific verticals in retail, hospitality, and other niche areas, is also growing due to increased consumer demand for experiential space and connection, as retail considers adaptive reuse for mixed-use buildings and hospitality through unique and sustainable designs.

ARCHITECTURAL SERVICES MARKET REGIONAL OUTLOOK

Geographically, the market is segmented into Asia Pacific, North America, Europe, South America and the Middle East & Africa.

Asia Pacific

Asia Pacific Architectural Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market was valued at USD 133.68 billion in 2025, capturing 33.60% of global revenue, and is estimated to reach USD 139.62 billion in 2026. in the architectural services landscape, driven by rapid urbanization, growing populations, and extensive infrastructure development. The growing demand for apartments, hotels, restaurants, and commercial and industrial spaces remains strong in developing countries. Government investment in smart city initiatives and sustainable urban development further supports growth as countries build modern transportation systems and public facilities to improve quality of life. There is also an increasing adoption of new technologies, such as Building Information Modeling (BIM) and generative AI, which are enabling faster building design delivery. Simultaneously, the region aims for green architecture, encouraging the growth of the AEC (architectural, engineering and construction) consulting service market. The Japan market is projected to reach USD 25.81 billion by 2026, the China market is projected to reach USD 54.76 billion by 2026, and the India market is projected to reach USD 18.48 billion by 2026.

Download Free sample to learn more about this report.

China's architectural services industry continues to grow due to its world-record urban development projects and government-backed infrastructure initiatives associated with smart cities, high-speed rail, and mass public transportation. Demand for residential and commercial space remains higher, and sustainability in sectors such as the built environment is gaining traction as clients increasingly inquire about green building standards and energy efficiency. Technologies including BIM and AI design tools have advanced the industry, and the demand for specialists in areas of heritage conservation and regulatory consulting is growing as countries face complex institutional systems to assess regulatory compliance outcomes.

To know how our report can help streamline your business, Speak to Analyst

North America

North America contributed 28.50% to the global market in 2025, with a valuation of USD 113.66 billion, and is projected to reach USD 117.7 billion in 2026. The North American region has notable residential, healthcare, and infrastructure projects, driving significant growth in architectural services, driven by technology. There is a focus on sustainable buildings, including the growing demand for green building certifications, such as LEED, which help drive commercial opportunities. Emerging technologies (including generative AI and digital twins) are aiding in increasing the project efficiency and enhancing client engagement. Additionally, specialized services such as building code consulting and a push toward modernizing outdated infrastructure present additional strong opportunities for consultants in the North American market. The U.S. market is projected to reach USD 93.03 billion by 2026.

South America

Architectural services in South America are driven by investments in infrastructure and urban expansion within the residential and industrial sectors. The government invests in affordable housing and public infrastructure projects (particularly those related to transportation networks) to drive the market forward. The industry embraces innovative design, using sustainable materials and energy-efficient buildings. Technologies such as BIM are being adopted, but adoption is limited due to high costs. Specialized services including regulatory consulting can help with projects initiated within a fragmented framework of building codes. The emergence of new markets in South America favors redesign as these regions continue to shape and define urban footprint.

Europe

Europe accounted for USD 84.71 billion in 2025, representing 21.30% of the global market share, and is projected to reach USD 87.99 billion in 2026. Forward-looking projects characterize the European market, however some of the most notable developments are in historical retrofits that refresh past builds while recognizing historic needs. Overall, there is a steady demand for residential and commercial buildings as well as public sector investments in educational facilities and healthcare sectors. Furthermore, the European market notices the introduction of new technologies (for example, VR/AR and BIM) to visualize the design and provide better assurance around the design elements from site layout to existing conditions output. There is a strong and recent adoption of comprehensive eco-strategies and energy-efficient design approaches, driven by increasingly stringent regulatory mandates. Therefore, due to the region's complex regulatory landscape, there is continued demand for specialized regulated services (either through consultants, partnerships, or co-design), including regulatory services, historical restoration, and other heritage services. The UK market is projected to reach USD 18.41 billion by 2026, while the Germany market is projected to reach USD 20.85 billion by 2026.

Middle East & Africa

The market in Middle East & Africa reached USD 40.53 billion in 2025, representing 10.20% of total market revenue, and is projected to reach USD 42.57 billion in 2026. Ambitious infrastructure projects drive the Middle East & Africa markets, including the smart cities and major commercial development schemes. The desire for a distinct architectural identity drives the market alongside a growing emphasis on sustainability in urban planning, with investments supported by the governments and aligned with broader efforts to diversify the economy across various public sector domains. Technology such as generative AI and BIM are increasingly utilized to ensure better design efficiencies while satisfying the projects' environmental conditions. There is increased demand for specialized services, especially concerning sustainability and legal compliance issues associated with complex regulatory frameworks and approvals processes.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Drive the Market due to Diverse Project Expertise and Advanced Technology Adoption

The market is substantially influenced by firms including Gensler, AECOM, Perkins&Will, HDR, and Foster + Partners. These companies are highly successful due to their diverse portfolios, as they develop a deeper expertise in each project type. As distinguished firms, they innovate and set benchmarks for the industry, executing commercial, residential, infrastructure, and sustainable design projects at scale. These firms have access to industry standards in technologies, including Building Information Modeling, generative AI, and virtual reality, to achieve innovative solutions to the streaming demand for environmentally compliant and intelligent designs. By operating globally, these firms can meet regional needs, using sustainable and regulatory requirements as competitive advantages. Other regional players in the market are more specialized, including Nikken Sekkei in the Asia Pacific and Zaha Hadid Architects in the Middle East, whose projects deliver diversity to the market through regionally tailored and often iconic buildings.

Long List of Companies Studied (including but not limited to)

- Gensler (U.S.)

- AECOM (U.S.)

- Perkins&Will (U.S.)

- HDR (U.S.)

- Arcadis (Netherlands)

- Sweco (Sweden)

- HKS (U.S.)

- Nikken Sekkei (Japan)

- Stantec (Canada)

- Foster + Partners (U.K.)

- Zaha Hadid Architects (U.K.)

- BDP (U.K.)

- Perkins Eastman (U.S.)

- NBBJ (U.S.)

- Kohn Pedersen Fox Associates (U.S.)

- GMP Architekten (Germany)

- Lemay (Canada)

- Aedas (Hong Kong)

- DP Architects (Singapore)

- Morphogenesis (India)

KEY INDUSTRY DEVELOPMENTS

- October 2024: Perkins & Will completed their newest museum, dedicated to the 16th-century Curtain Theatre in Shoreditch, London. The Curtain Theatre was an influential Shakespearean venue, possibly hosting original performances of plays such as Romeo and Juliet. It is now a permanent location for the archaeological finds and history of the site.

- September 2024: Gensler launched the "Reimagining Resiliency, Securing Sustainability" pilot program through its Charitable Gift Fund, partnering with the University of Tennessee, Knoxville, and Lawrence Technological University to advance sustainable design education. Each institution received a USD 100,000 donation to develop interdisciplinary undergraduate courses. This initiative aims to equip future design professionals with skills for sustainable practices and serve as a model for other universities.

- February 2024: Springhouse Architects, led by Sheri Scott, merged with Studiyo-b Architects, led by Todd Yoby, to operate as Springhouse Architects, expanding their residential, commercial, and multi-family design services across Cincinnati, Dayton, and Columbus.

- February 2024: SRG Partnership, an architecture firm in the Pacific Northwest with a commendable reputation for innovative and sustainable design, partnered with CannonDesign. This partnership will support CannonDesign's continued regional evolution by bringing their group of engaged architects and designers to support transformative projects across education, healthcare, and civic.

- November 2023: AECOM, a global infrastructure consulting firm, signed a MoU as the reconstruction delivery partner for Kyiv's Boryspil International Airport, Ukraine's largest airport. AECOM will provide infrastructure advisory support, including asset assessment, design, engineering, program management, and construction management, while also aiding the broader reconstruction of Ukraine's aviation sector, aligning with national restoration plans under the Ministry of Community, Territory, and Infrastructure Development.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, solution types, and leading end users of the services. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.9% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Solution Type

By End User

By Region

|

|

Companies Profiled in the Report |

Gensler (U.S.), AECOM (U.S.), Perkins&Will (U.S.), HDR (U.S.), Arcadis (Netherlands), Sweco (Sweden), HKS (U.S.), Nikken Sekkei (Japan), Stantec (Canada), Foster + Partners (U.K.) |

Frequently Asked Questions

The market is projected to reach USD 622.04 billion by 2034.

In 2025, the market was valued at USD 398.33 billion.

The market is projected to grow at a CAGR of 5.20% during the forecast period.

The construction and project management segment is expected to lead the market in terms of revenue.

Urbanization, technology, and environmental awareness drive demand for sustainable and innovative architectural solutions, fueling market growth.

Gensler, AECOM, Perkins&Will, HDR, and Foster + Partners are the top players in the market.

Asia Pacific is expected to hold the highest market share.

By end user, the government & education is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us