Artificial Heart Market Size, Share & Industry Analysis, By Product (Total Artificial Heart (TAH), Ventricular Assist Device, and Others), By Application (Bridge to Transplant (BTT), Bridge to Candidacy (BTC), Destination Therapy (DT), and Bridge to Recovery (BTR)), By End-user (Hospitals and ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Artificial Heart Market Overview

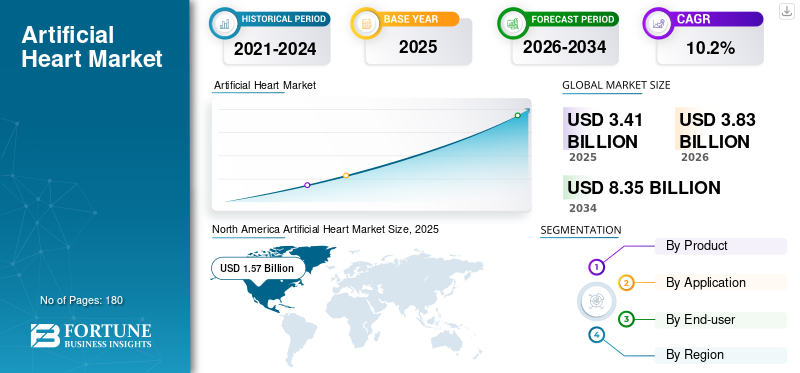

The artificial heart market size was valued at USD 3.41 billion in 2025. The market is projected to grow from USD 3.83 billion in 2026 to USD 8.35 billion by 2034, exhibiting a CAGR of 10.2% during the forecast period. North America dominated the artificial heart market with a market share of 46.04% in 2025.

An artificial heart is a mechanical device, usually made of metal and plastic, that replaces the failed ventricles of the human heart to pump blood throughout the body. Demand for this product is rising as cardiovascular disease remains the leading cause of death worldwide, and a growing pool of patients progresses to advanced heart failure, where medicines alone are often not enough. Similarly, artificial heart technologies are being used across more clinical pathways, from bridge-to-transplant and bridge-to-candidacy to destination therapy and short-term recovery support.

Furthermore, Johnson & Johnson, Abbott, Shenzhen Core Medical Technology, and Berlin Heart GmbH held the largest market share, driven by the limited market presence of other players and market consolidation.

Download Free sample to learn more about this report.

ARTIFICIAL HEART MARKET TRENDS

Shift from a Transplant-only Narrative to a Broader Heart-failure Support Ecosystem is Emerging Market Trend

A notable trend in this market is the widening role of artificial heart technologies across the full spectrum of advanced circulatory support. Historically, the discussion centered mainly on bridge-to-transplant. The market is increasingly defined by a more diversified treatment mix that includes destination therapy, bridge-to-candidacy, bridge-to-recovery, and short-term intervention support. This is significant as it reduces dependence on one narrow patient pathway and strengthens the commercial relevance of VADs in everyday advanced heart failure care.

Another visible trend is the coexistence of durable and temporary platforms. Durable VADs remain central in long-term management, while temporary and percutaneous systems are being used more actively in acute decompensation, cardiogenic shock, and high-risk cardiac procedures. Additionally, growth is still from a smaller base. However, recent CARMAT implant and sales updates suggest that the segment is moving from an earlier developmental phase toward more structured commercialization in selected centers. The relaunch of ISHLT’s IMACS registry also points to a broader industry push toward better data capture, benchmarking, and therapy optimization in mechanical circulatory support.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Advanced Heart Failure Burden is Expanding the Need for Mechanical Circulatory Support

One of the strongest forces behind market growth is the steady rise in patients living with severe cardiac dysfunction, especially those who do not respond adequately to drug therapy or conventional interventions. Cardiovascular disease continues to account for a very large share of global mortality, and the advanced heart failure population is becoming more visible as diagnosis improves and patients survive longer with chronic disease. This creates a wider clinical window for artificial heart therapies, particularly VADs, which can stabilize patients. Similarly, they await transplant, allow time for candidacy assessment, or serve as long-term support for people who are not transplant eligible.

Regulatory indications also reinforce this demand. FDA documentation for the HeartMate 3 states that the device is intended for short and long-term mechanical circulatory support, including bridge-to-transplant, myocardial recovery, and destination therapy. Temporary support devices are also gaining relevance in cardiogenic shock and in high-risk interventions as FDA materials for Impella note its approved use in high-risk PCI and for short-term hemodynamic support. Together, these factors are widening the addressable patient pool and supporting steady market expansion across both durable and temporary segments.

MARKET RESTRAINTS

High Device Cost and Complex Care Pathways Continue to Limit Product Adoption

Despite its clinical value, the market faces a restraints including financial barrier. These devices are expensive to manufacture, implant, and manage, and the true cost extends beyond the initial hardware. Patients often require highly specialized surgery, long ICU stays, advanced imaging, anticoagulation management, intensive follow-up, and access to experienced multidisciplinary teams that naturally concentrates demand in major tertiary centers and transplant-capable institutions, leaving many hospitals unable to adopt the therapy at scale.

Total artificial heart systems are especially affected as they involve narrower patient selection, higher procedural complexity, and a smaller trained-center base. Even when reimbursement is available, administrators and clinicians must weigh the cost of device programs against procedural volume, survival outcomes, and resource intensity. In emerging markets, the issue becomes sharper as the infrastructure for mechanical circulatory support is still developing. This slows penetration, particularly outside large metropolitan referral centers. As a result, market growth remains strong but uneven, with adoption moving fastest in health systems that can support complex perioperative care, long-term monitoring, and complication management.

MARKET OPPORTUNITIES

Unmet Transplant Demand Creates Room for Broader Use of Artificial Heart Therapies

A major opportunity for the market lies in the gap between the number of patients needing advanced cardiac replacement therapy and the limited supply of donor hearts. Transplant remains the standard for many end-stage patients. However, donor availability is inherently constrained, and transplant systems are built around scarce organs, strict eligibility criteria, and time-sensitive matching. OPTN/UNOS data infrastructure exists precisely as waiting-list management and donor allocation are central bottlenecks in the U.S. transplant system. In this environment, artificial heart technologies become more than temporary rescue tools as they evolve as strategic therapies that help patients survive longer, remain eligible, or avoid immediate transplant dependency altogether. This is especially relevant for destination therapy, bridge-to-candidacy, and bridge-to-decision use cases, where clinicians need time to stabilize end-organ function, assess comorbidities, or determine transplant suitability.

The market opportunity is expanding as manufacturers scale production and add implanting centers. CARMAT has publicly stated that it increased manufacturing capacity and expanded its hospital footprint, showing how the market can widen when technology availability improves alongside clinical confidence. Over time, this combination of donor shortage and therapy maturation can meaningfully expand commercial demand.

MARKET CHALLENGES

Clinical Risk, Training Intensity, and Uneven Access Complicate Market Growth

A significant challenge for the market is building enough clinical capability to use them safely and consistently. Mechanical circulatory support demands highly trained surgeons, heart-failure specialists, perfusion and ICU teams, and robust post-implant management protocols. Complications such as bleeding, thrombosis, infection, stroke, right-heart failure, and device-related issues can quickly affect outcomes and confidence in therapy use. Thus, adoption depends as much on center experience as on product performance.

Additionally, there is also an increased complexitiy when patient selection is narrow, and procedure volumes are still limited. Temporary support devices face their own barriers, including appropriate timing of escalation, case selection, and variability in practice patterns across hospitals. This creates a layered problem as companies must invest in physician education, center activation, technical support, and real-world evidence generation, while providers must justify program economics and maintain specialized teams. Until access broadens and clinical familiarity deepens across more centers, market growth will continue, but with a clear bias toward major referral institutions and better-funded health systems.

Segmentation Analysis

By Product

Wide Adoption and Indications of Ventricular Assist Device to Drive Segment Growth

Based on product, the market is segmented into Total Artificial Heart (TAH), ventricular assist device, and others.

To know how our report can help streamline your business, Speak to Analyst

Ventricular assist devices account for the largest share of the market as they serve a much broader clinical population than total artificial heart systems. In practice, VADs are used across bridge-to-transplant, bridge-to-candidacy, bridge-to-recovery, and destination therapy settings, making them relevant in both chronic advanced heart failure and acute circulatory support.

Additionally, the Total Artificial Heart (TAH) segment is projected to grow at a CAGR of 15.2% during the forecast period.

By Application

Destination Therapy Leads as it Addresses Patients Who Need Long-Term Support

By application, the market is classified into Bridge to Transplant (BTT), Bridge to Candidacy (BTC), Destination Therapy (DT), and Bridge to Recovery (BTR).

Destination therapy holds the highest share by application as a large portion of advanced heart failure patients are either ineligible for transplant or may not receive a donor organ in time. This makes long-term mechanical support a practical treatment pathway rather than a temporary bridge alone. Moreover, the segment is projected to hold a 35.4% share in 2026.

Additionally, the Bridge to Recovery (BTR) segment is estimated to grow at a CAGR of 8.9% during the forecast period.

By End-user

Hospitals and ASCs Lead as Artificial Heart Therapies Require Concentrated Infrastructure, Procedural Expertise, and Intensive Follow-Up

On the basis of end-user, the market is classified into hospitals and ASCs, specialty clinics, and others.

Hospitals and ambulatory surgical settings are the leading end-user segment as artificial heart implantation and management require specialized infrastructure that smaller facilities typically lack. These therapies depend on surgical capability, imaging support, ICU care, anticoagulation management, and multidisciplinary coordination before and after the procedure. Even temporary support systems are often deployed in high-acuity hospital environments where rapid escalation decisions can be made. Furthermore, the segment is set to hold a 73.8% share in 2026.

In addition, the specialty clinics segment is projected to grow at a CAGR of 13.2% during the forecast period.

Artificial Heart Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America Artificial Heart Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest artificial heart market share in 2024, at USD 1.39 billion, and reached USD 1.57 billion in 2025. North America is expected to record strong growth in the market due to the high burden of advanced heart failure, broad availability of transplant and mechanical circulatory support programs, and faster adoption of ventricular assist devices across both durable and temporary support settings. The region also benefits from favorable awareness among clinicians, relatively better access to reimbursement, strong concentration of tertiary cardiac centers, and continued product commercialization by major device manufacturers. In addition, growing use of destination therapy and bridge-to-decision strategies is expanding the eligible patient pool beyond only transplant-linked cases.

U.S. Artificial Heart Market

In 2026, the U.S. market is forecasted to represent USD 1.59 billion, capturing 41.5% of total global revenue.

Europe

Europe is expected to achieve a 9.9% growth rate in the coming years, the second-highest globally, reaching USD 1.02 billion by 2026. Europe is projected to grow steadily due to its established cardiac surgery infrastructure, the increasing use of ventricular assist devices in key countries such as Germany, France, Italy, Spain, and the U.K., and the gradual expansion of advanced heart failure treatment pathways. The region is also benefiting from rising clinical familiarity with artificial heart support technologies, improving hospital capabilities, and broader acceptance of both bridge-to-transplant and destination therapy approaches. Growth is further supported by ongoing technology development and the increasing penetration of specialized implant centers across Western Europe and in selected parts of the Rest of Europe.

U.K. Artificial Heart Market

The U.K. market is projected to reach USD 0.13 billion by 2026, accounting for 3.4% of the global market revenue.

Germany Artificial Heart Market

Germany's market is forecasted to reach about USD 0.22 billion by 2026, representing roughly 5.8% of global revenue.

Asia Pacific

In 2026, the Asia Pacific market is predicted to be valued at USD 0.78 billion, ranking as the third-largest globally. Asia Pacific is likely to witness the fastest growth due to its large patient population, rising prevalence of cardiovascular disease, improving diagnosis of advanced heart failure, and gradual expansion of high-acuity cardiac care infrastructure. Demand is increasing as major countries such as China, Japan, India, and Australia as they continue to strengthen tertiary care capacity and adopt more sophisticated circulatory support technologies. The market is also benefiting from improving healthcare expenditure, growing physician awareness, and expanding access to temporary and percutaneous ventricular assist devices, which support adoption even in markets where long-term implant penetration is still developing.

Japan Artificial Heart Market

Japan is projected to generate approximately USD 0.18 billion in revenue by 2026, contributing nearly 4.8% to the global market.

China Artificial Heart Market

China's market is forecast to reach approximately USD 0.21 billion by 2026, contributing about 5.6% to global revenues.

India Artificial Heart Market

India is forecast to contribute approximately USD 0.08 billion to the market by 2026, corresponding to about 2.1% of global revenues.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate artificial heart market growth, with Latin America expected to reach around USD 0.15 billion by 2026. Latin America is expected to grow at a moderate pace, supported by improving access to advanced cardiac treatment in major urban centers, particularly in Brazil and Mexico. Growth in the region is being driven by rising recognition of severe heart failure, gradual development of specialized cardiac hospitals, and increasing referral of complex patients to tertiary centers capable of managing mechanical circulatory support. Additionally, the Middle East & Africa region is projected to grow from a smaller base, mainly due to expanding healthcare infrastructure in higher-income markets, especially in GCC countries, and the improved availability of specialized cardiac care in selected centers.

GCC Artificial Heart Market

By 2026, the GCC is expected to generate approximately USD 0.05 billion in the market, accounting for nearly 1.2% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Ongoing Technological Advancements and Development of Products in Clinical Trials Enhance Market Competition

The market is highly consolidated, with few key players accounting for most of the revenue. This gives the industry a clear, large-player dominance pattern rather than a fragmented structure. Johnson & Johnson, Abbott, and Shenzhen Core Medical Technology were the major companies in 2025. Beyond these leaders, competition is more specialized and regional. Companies such as SynCardia, CARMAT, Berlin Heart, EVAHEART, and several China-based players compete in narrower niches such as total artificial heart systems, pediatric support, or regional markets.

Moreover, other key players, such as BrioHealth Technologies, Sun Medical Technology Research, and Rocor Medical Technology, compete through ongoing technological advancements and the development of products in clinical trials.

LIST OF KEY ARTIFICIAL HEART COMPANIES PROFILED

- Johnson & Johnson (U.S.)

- Abbott (U.S.)

- Shenzhen Core Medical Technology (China)

- Berlin Heart GmbH (Germany)

- BrioHealth Technologies (China)

- Sun Medical Technology Research (Japan)

- SynCardia Systems (U.S.)

- Rocor Medical Technology (China)

- CARMAT (France)

- Jarvik Heart (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2025: CARMAT reported 42 Aeson implants in 2024 and continued strong momentum into 2025, highlighting the growing commercialization of its total artificial heart.

- December 2024: Johnson & Johnson MedTech announced that the U.S. Food and Drug Administration (FDA) has expanded the indications for the Impella 5.5 with SmartAssist and Impella CP with SmartAssist heart pumps, granting Premarket Approval (PMA) for use in specific pediatric patients with symptomatic Acute Decompensated Heart Failure (ADHF) and cardiogenic shock.

- October 2024: ABIOMED announced that the Impella ECP pivotal study demonstrated safety and efficacy in high-risk PCI.

- July 2024: CARMAT reported a strong acceleration in Aeson sales momentum, expansion to 42 trained hospitals in 14 countries, and commercial openings in additional European countries.

- May 2024: Sun Medical announced the new commercial launch of EVAHEART 2 C03 and the end of sales for C02, marking an updated product offering in Japan’s implantable VAD market.

- April 2024: Picard Medical and SynCardia announced plans to become publicly traded through a merger with Altitude Acquisition Corp., aimed at supporting SynCardia’s next growth phase.

- April 2024: ABIOMED announced that a randomized controlled trial confirmed Impella CP improved survival in heart attack patients with cardiogenic shock, a major evidence milestone for percutaneous support.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Application, End-user, and Region |

| By Product |

|

| By Application |

|

| By End-user |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.41 billion in 2025 and is projected to reach USD 8.35 billion by 2034.

In 2025, the North America market value stood at USD 1.57 billion.

The market is expected to exhibit a CAGR of 10.2% during the forecast period of 2026-2034.

The ventricular assist device segment led the market by product.

The key factors driving the market are the rising advanced heart failure burden and increasing need of artificial heart.

Johnson & Johnson, Abbott, Shenzhen Core Medical Technology, and Berlin Heart GmbH are some of the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us